Weak Magnetic Detection Sensor Market Insights

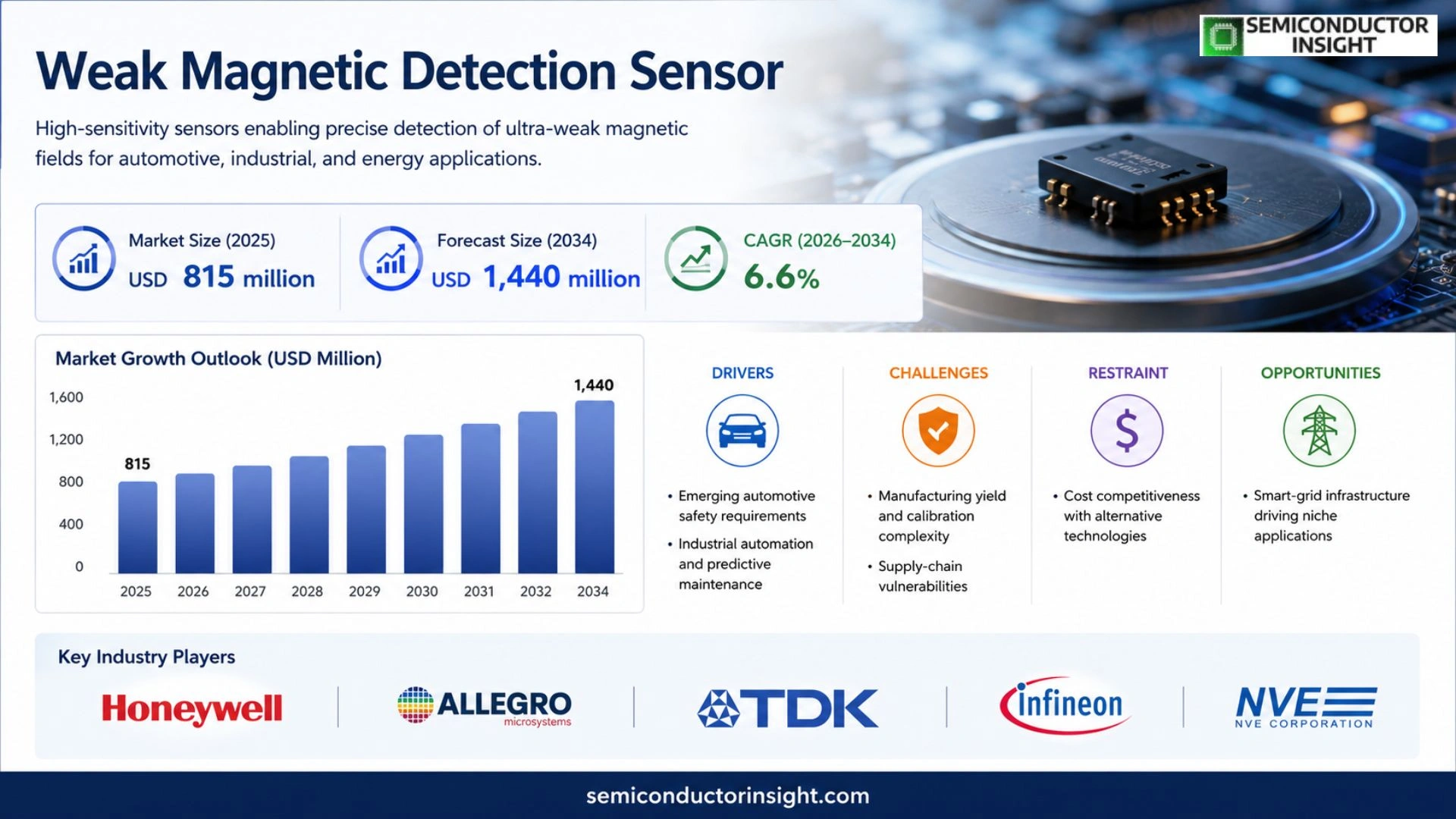

Global Weak Magnetic Detection Sensor market size was valued at USD 815 million in 2025 and is projected to reach USD 1,440 million by 2034, exhibiting a CAGR of approximately 6.6% during the forecast period.

Weak magnetic detection sensors are devices designed to sense and quantify low‑intensity magnetic fields with high precision. Typically based on Hall‑effect or magnetoresistive principles, these sensors deliver low‑noise output and are employed across automotive systems, consumer electronics, industrial automation, and medical equipment for functions such as position tracking, speed measurement, current monitoring and navigation.

The market is gaining momentum because expanding IoT deployments, autonomous‑driving platforms and smart‑manufacturing demand accurate magnetic field data; however, challenges remain around material costs and integration complexity. Recent collaborations among leading chip makers aim to improve sensitivity while reducing power consumption, positioning weak magnetic detection sensors as essential components in emerging smart‑device ecosystems.

MARKET DRIVERS

Emerging Automotive Safety Requirements

Regulators in North America and Europe have tightened standards for vehicle stability systems, prompting manufacturers to integrate more sensitive detection elements. The demand for precise low‑field measurement aligns directly with the capabilities of weak magnetic detection sensors, creating a measurable uptick in component orders.

Industrial Automation and Predictive Maintenance

Factories are adopting condition‑monitoring solutions that rely on subtle magnetic signatures to flag bearing wear or motor degradation. As uptime becomes a cost‑critical metric, buyers are willing to invest in sensors that can discern fields as low as a few nanotesla.

➤ Clients cite reduced false‑alarm rates and longer service intervals as the primary justification for upgrading to weak magnetic detection technology.

Beyond these two forces, the rollout of smart‑grid infrastructure is creating niche applications where low‑intensity magnetic field monitoring supports fault detection in power lines, further expanding the addressable market.

MARKET CHALLENGES

Manufacturing Yield and Calibration Complexity

Producing sensors with sub‑nanotesla accuracy demands tight process controls. Variability in thin‑film deposition can lead to calibration drift, forcing end users to allocate additional resources for periodic verification.

Other Challenges

Supply‑Chain Vulnerabilities

The reliance on specialty alloys and rare‑earth materials exposes the sector to geopolitical fluctuations, potentially inflating unit costs during periods of restricted export.

MARKET RESTRAINTS

Cost Competitiveness with Alternative Technologies

While weak magnetic detection sensors offer unparalleled precision, many customers still favor established hall‑effect or fluxgate devices due to lower upfront pricing. The price differential narrows only when volume discounts offset the higher engineering investment.

MARKET OPPORTUNITIES

Growth in Wearable Health Monitoring

Emerging biometric platforms seek to capture minute magnetic fluctuations associated with cardiac and neural activity. Integrating weak magnetic detection sensors into compact wearables could unlock a multi‑billion dollar segment, provided manufacturers can meet stringent power‑consumption benchmarks.

Weak Magnetic Detection Sensor Market Trends

Accelerated Adoption in Autonomous Driving

Automakers are integrating weak magnetic detection sensors into electric power‑train control and steering feedback loops to meet the precise positioning requirements of autonomous systems. The sensors’ Hall‑effect and magnetoresistive architectures deliver the low‑noise performance needed for real‑time wheel‑speed and torque calculations, allowing manufacturers to reduce reliance on mechanical encoders. This shift not only shortens calibration cycles but also aligns with industry pressure to lower vehicle weight and improve energy efficiency. As a result, component procurement budgets are being re‑allocated toward sensor modules that can be co‑designed with vehicle‑level electronic control units, creating a new supply‑chain dynamic that favors suppliers with advanced chip‑fabrication capabilities.

Other Trends

Supply‑Chain Constraints on Critical Materials

The upstream segment of the sensor ecosystem remains highly sensitive to the availability of rare‑earth magnetic alloys and high‑purity semiconductor substrates. Recent geopolitical tensions have tightened export controls, prompting key manufacturers to diversify sourcing and invest in regional material processing hubs. These actions increase capital intensity but also enhance resilience against sudden price spikes. For downstream integrators, the ripple effect translates into tighter bill‑of‑materials forecasts and a stronger emphasis on design‑for‑manufacturability, where sensor packaging tolerances are optimized to mitigate the impact of material variability. Companies that can secure stable material flows are positioning themselves to capture premium pricing for calibrated, high‑sensitivity units priced around $21 each in 2025.

Emerging Opportunities in Wearable Health Devices

Beyond automotive and industrial automation, the health‑tech sector is beginning to exploit the low‑power, high‑resolution characteristics of weak magnetic detection sensors for magnetic‑based motion tracking in wearable diagnostics. By embedding these sensors in wristbands and smart garments, manufacturers can deliver continuous monitoring of physiological signals without the battery drain associated with optical or inertial alternatives. This convergence of medical imaging requirements and IoT connectivity fuels a nascent market segment where sensor manufacturers collaborate directly with device designers to co‑develop algorithms that translate magnetic field fluctuations into actionable health metrics. The strategic implication is clear: firms that augment their sensor portfolios with bespoke firmware and integration services are likely to secure differentiated contracts with health‑care providers seeking next‑generation patient monitoring solutions.

COMPETITIVE LANDSCAPE

Key Industry Players

Weak Magnetic Detection Sensor Market – Competitive Overview

Honeywell remains the market anchor, leveraging its deep expertise in precision instrumentation and a global sales network that reaches automotive OEMs, industrial integrators, and medical device manufacturers. Its portfolio spans Hall‑effect and magnetoresistive sensors that are integrated into power‑train control units and high‑resolution navigation modules. The company’s recent acquisition of a niche magnetoresistive chip designer gives it a technological edge in low‑noise performance, allowing it to command premium pricing and capture a sizable share of the $815 million 2025 market. Parallel to Honeywell, Allegro MicroSystems and TDK occupy the upper tier with complementary strengths: Allegro’s aggressive roadmap in mini‑atured Hall‑effect dies caters to the fast‑growing IoT‑enabled consumer electronics segment, while TDK’s vertically integrated production line,from magnetic material (ferrite) supply to wafer‑level packaging,reduces lead times and improves cost‑competitiveness for large‑volume automotive contracts.

The remainder of the field comprises a blend of established semiconductor houses and specialist sensor firms that together shape a fragmented but highly innovative landscape. Melexis, Asahi Kasei Microdevices, and STMicroelectronics focus on application‑specific modules, embedding weak magnetic detection capability into motor‑control ASICs and smart‑grid sensors. Emerging challengers such as Sinomags Electrical Technology, Jiasheng Test Engineering, and MultiDimension Technology differentiate themselves through bespoke calibration services and rapid‑prototype services for niche industrial automation niches. Mid‑tier players including NXP Semiconductors, Bosch Sensortec, Infineon Technologies, MagnaChip Semiconductor, Texas Instruments, and Analog Devices broaden the competitive set by offering mixed‑signal solutions that combine magnetic sensing with temperature and pressure monitoring, thereby addressing the convergence trend in intelligent transportation and wearable health devices.

List of Key Weak Magnetic Detection Sensor Companies Profiled

- Honeywell

- Allegro MicroSystems

- Melexis

- TDK

- Asahi Kasei Microdevices

- Sinomags Electrical Technology

- Jiasheng Test Engineering

- MultiDimension Technology

- NXP Semiconductors

- STMicroelectronics

- Bosch Sensortec

- Infineon Technologies

- MagnaChip Semiconductor

- Texas Instruments

- Analog Devices

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Hall Effect Sensor is widely regarded as the foundational technology for weak magnetic detection.

|

| By Application |

|

Automotive Industry drives the most intense adoption of weak magnetic detection sensors.

|

| By End User |

|

Vehicle Systems represent the core end‑user group.

|

| By Sensitivity |

|

High Sensitivity continues to dominate development focus.

|

| By Integration Form |

|

System‑Integrated solutions are gaining traction across multiple verticals.

|

Regional Analysis: Weak Magnetic Detection Sensor Market

Europe

Major European carmakers have integrated weak magnetic sensors into electric drivetrain control units, citing improved fault isolation and reduced energy loss. Their procurement policies now prioritize suppliers that can deliver low‑noise modules compatible with existing vehicle networks, prompting a surge in specialized component offerings.

Factories upgrading to Industry 4.0 standards rely on magnetic detection to fine‑tune motor loads and anticipate mechanical degradation. System integrators favor sensors that fuse seamlessly with PLCs, enabling real‑time analytics without extensive hardware redesign.

EU directives on energy efficiency encourage the adoption of predictive maintenance tools. Companies that demonstrate measurable reductions in downtime through magnetic monitoring gain preferential treatment during certification audits.

Research consortia in Germany and the Benelux region are testing novel sensor alloys that operate reliably at higher temperatures, unlocking applications in aerospace and high‑speed rail where traditional solutions falter.

North America

North America’s commercial trajectory is defined by aggressive electric vehicle rollout targets and a robust defense procurement pipeline. U.S. defense agencies have begun specifying weak magnetic detection sensors for unmanned aerial systems, valuing their ability to provide redundant position verification. Meanwhile, the continent’s sizable consumer‑electronics sector leverages these sensors to enhance haptic feedback and low‑power Bluetooth devices. The competitive landscape forces original equipment manufacturers to negotiate tighter supply contracts, fostering a market where reliability and cost efficiency become decisive factors for success.

Asia‑Pacific

The Asia‑Pacific region is witnessing a rapid shift from mass‑production to value‑added manufacturing. Nations such as China, Japan, and South Korea are embedding magnetic sensors in high‑speed train propulsion and smart‑grid infrastructure, aiming to tighten operational margins. A growing emphasis on indigenous technology development reduces reliance on imported components, prompting local firms to invest in miniaturisation and MEMS‑based designs that cater to dense urban applications.

South America

In South America, sensor adoption is propelled by expanding renewable‑energy projects and a nascent electric‑bus fleet. Countries like Brazil and Chile are piloting magnetic detection within turbine generators to optimise load distribution. The region’s fragmented supply chain encourages partnerships between global sensor makers and regional system integrators, creating opportunities for joint‑venture models that address localized cost sensitivities.

Middle East & Africa

The Middle East & Africa market is characterised by infrastructure modernization and heightened interest in smart‑city initiatives. Oil‑rich economies are repurposing offshore platforms with magnetic monitoring to prolong equipment life and curtail unplanned shutdowns. African telecom operators are experimenting with low‑power sensors to support remote‑site monitoring, where energy constraints make the weak magnetic detection approach especially appealing.

Report Scope

This market research report provides a comprehensive analysis of the Weak Magnetic Detection Sensor Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Weak Magnetic Detection Sensor Market?

-> Weak Magnetic Detection Sensor market is projected to reach USD 1,440 million by 2034, exhibiting a CAGR of approximately 6.6%

Which key companies operate in Weak Magnetic Detection Sensor Market?

-> Key players include Honeywell, Allegro MicroSystems, Melexis, TDK, Asahi Kasei Microdevices, Sinomags Electrical Technology, JiashengTest Engineering, MultiDimension Technology.

What are the key growth drivers?

-> Key growth drivers include rapid expansion of the Internet of Things, autonomous driving, intelligent manufacturing, and rising demand for high‑precision magnetic field detection in automotive and industrial automation.

Which region dominates the market?

-> Asia‑Pacific holds the largest market share, propelled by strong automotive electronics production and consumer‑device manufacturing, while North America and Europe also exhibit solid growth.

What are the emerging trends?

-> Emerging trends include integration of weak magnetic sensors into smart wearables, medical imaging equipment, and next‑generation autonomous navigation systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...