Galvanic Isolated High-side Switch Market Insights

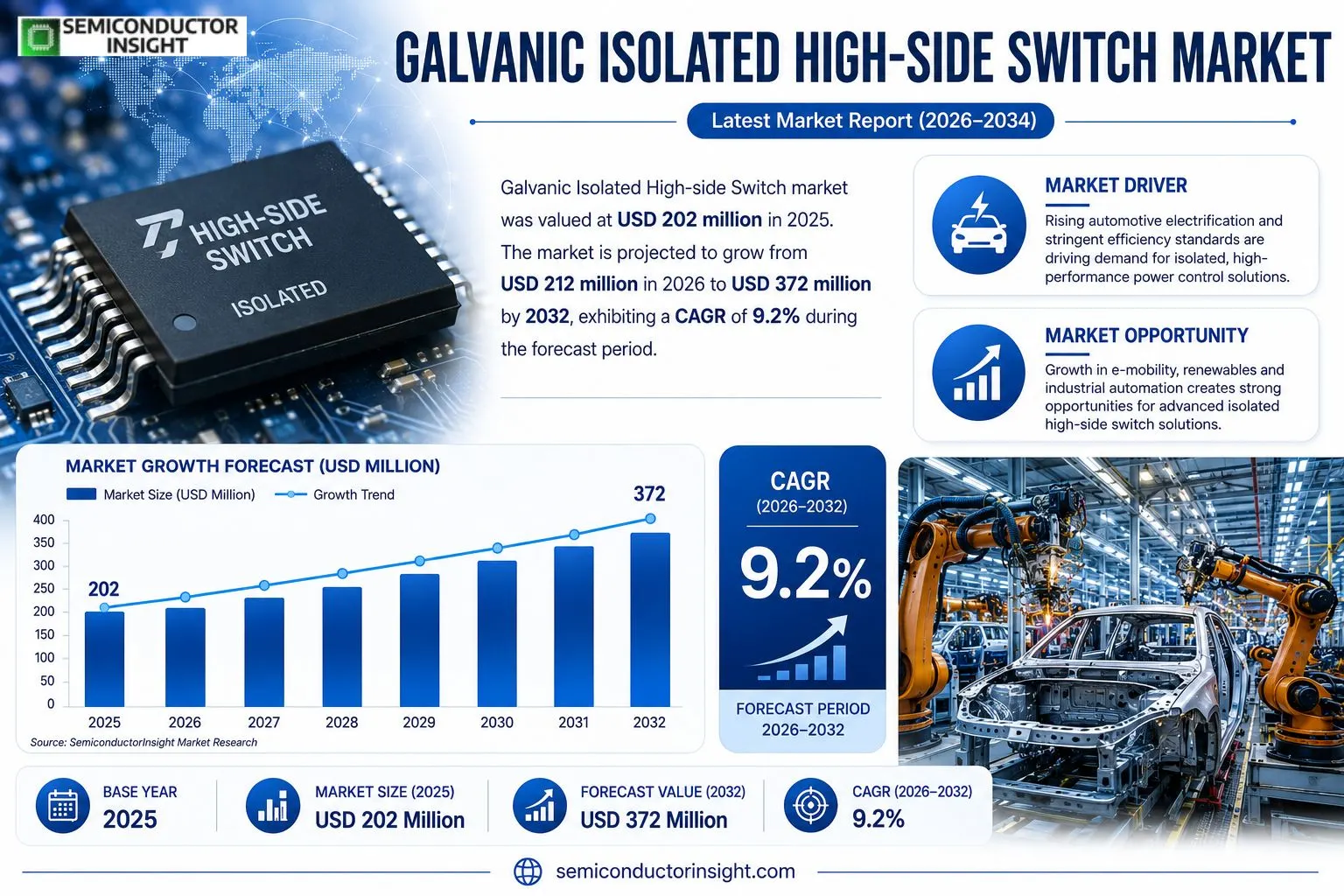

Galvanic Isolated High-side Switch market size was valued at USD 202 million in 2025. The market is projected to grow from USD 212 million in 2026 to USD 372 million by 2032, exhibiting a CAGR of 9.2% during the forecast period.

Galvanic Isolated High-side Switch is a high‑side load control device with galvanic isolation that separates the control and power domains, improving safety, noise immunity, and fault containment while integrating switching control, protection, and diagnostics for reliable operation in harsh electrical environments. In 2025 production reached roughly 34 million units at an average price of USD 6.5 per unit.The market is being shaped by stricter safety standards and rising electromagnetic complexity in automotive and industrial power systems. As electrification progresses, designers prioritize isolation to protect control units and reduce noise coupling; therefore suppliers that embed isolation, protection and diagnostics into compact architectures gain pricing stability despite intensifying competition.

MARKET DRIVERS

Increasing Automotive Electrification

The shift toward electric propulsion in cars, trucks and two‑wheelers forces designers to adopt components that can handle higher voltages without compromising safety. Galvanic Isolated High-side Switch Market suppliers benefit because their devices provide the necessary isolation while supporting fast switching, which is essential for regenerative braking and battery management systems.

Stringent Power‑Efficiency Standards

Regulatory bodies worldwide have tightened limits on loss and heat dissipation for power electronics. Manufacturers now favor switches that combine low on‑resistance with robust isolation, a combination that directly aligns with the core attributes of galvanic‑isolated high‑side switches. This alignment drives purchasing decisions across OEMs and Tier‑1 suppliers.

➤ Design teams that prioritize safety and efficiency are increasingly turning to galvanic isolation as a baseline requirement rather than an optional feature.

Beyond automotive, the rise of renewable‑energy inverters and industrial motor drives creates a parallel demand curve. Engineers in these sectors cite the ability of high‑side switches to protect downstream circuitry from common‑mode transients as a decisive factor when specifying components.

MARKET CHALLENGES

Cost‑Sensitive Procurement Practices

While performance metrics favor galvanic isolated solutions, many OEMs operate under tight cost constraints. The premium associated with additional isolation stages can tilt the balance toward less expensive, non‑isolated alternatives, especially in low‑volume applications where economies of scale are limited.

Other Challenges

Reliability Under Extreme Temperatures

Deployments in automotive under‑hood environments and offshore wind turbines expose devices to temperature swings beyond typical specifications. Ensuring long‑term reliability in such conditions remains a technical hurdle that manufacturers must address through rigorous qualification programs.Supply‑chain volatility, driven by geopolitical tensions and semiconductor shortages, further complicates the ability of vendors to meet lead‑time expectations, forcing some customers to opt for readily available substitutes.

MARKET RESTRAINTS

Complex Integration Requirements

Integrating galvanic isolated high‑side switches often demands redesign of PCB layouts to accommodate isolation pads and creepage distances. For legacy platforms, the redesign effort can be perceived as too disruptive, leading firms to defer adoption until the next product refresh.In addition, the need for specialized driver circuitry raises the overall component count, which can clash with design goals aimed at minimizing board space and simplifying assembly processes.Regulatory certification processes for safety‑critical applications add another layer of delay. Obtaining approvals such as ISO 26262 for automotive or IEC 60730 for industrial equipment can extend time‑to‑market, tempering enthusiasm for immediate deployment.

MARKET OPPORTUNITIES

Emerging E‑Mobility Segments

Electric scooters, micro‑mobility devices and autonomous delivery robots are entering mass production. Their power architectures rely heavily on compact, high‑efficiency switching solutions, positioning galvanic isolated high‑side switches as a natural fit for these niche yet rapidly scaling markets.Another promising avenue lies in grid‑edge storage solutions, where inverter modules must handle bidirectional power flow while maintaining strict isolation from the utility network. Vendors that can certify their switches for such scenarios stand to capture a share of the expanding distributed‑energy‑resource sector.Finally, collaborations between semiconductor firms and software providers are spawning smart‑control platforms that can dynamically reconfigure switch topology for optimal performance. This convergence creates a fertile ground for differentiated product offerings that embed diagnostic and predictive‑maintenance capabilities directly within the switch package.

Galvanic Isolated High-side Switch Market Trends

Safety‑Centric Integration Gains Traction

In 2025 the segment generated roughly $202 million from 34 million units priced at an average of $6.5 each. Capacity utilisation hovered around 71 %, delivering a robust gross margin of 45 %. These figures reflect a market that rewards designs which fuse isolation, protection and diagnostics into a single silicon footprint. Automotive and industrial engineers are tightening safety specifications while the electromagnetic environment grows more crowded, prompting a shift toward devices that can block fault currents and suppress noise without adding external components. The resulting architecture‑level savings keep total system cost competitive, even as buyers demand higher voltage ratings and tighter fault‑containment performance.

Other Trends

Supply‑Chain Consolidation and Value Engineering

Up‑stream suppliers such as Shin‑Etsu Chemical and SUMCO provide the silicon wafers and specialty resins that underpin the isolation barrier, while mid‑stream teams handle architecture definition, protection logic and thermal reliability. The tight coupling of these stages enables manufacturers to achieve the 71 % utilisation rate noted above and to preserve the 45 % margin by reducing the bill of materials. Integration also spreads qualification expenses across long‑lifecycle programs, a factor that strengthens profitability in platforms where redesign costs are prohibitive. Consequently, firms that lock‑in strategic wafer partners and streamline tape‑out schedules are better positioned to meet downstream demand without eroding price stability.

Automotive Electrification Reinforces Demand

The acceleration of vehicle electrification is converting isolation from a convenience into a prerequisite. OEMs such as Toyota, Volkswagen and BYD are specifying high‑side switches that can survive high‑voltage, high‑current transients while maintaining diagnostic visibility. Because system downtime translates directly into warranty exposure, manufacturers that can guarantee long‑term reliability while minimizing peripheral component count are gaining preference. The downstream ripple effect is evident in the industrial arena as well, where companies like Siemens and Schneider Electric are adopting the same devices to protect motor‑drive subsystems. For market participants, the strategic imperative is clear: align product roadmaps with the safety‑first ethos of electrified platforms, leverage the existing margin cushion, and exploit the established supply network to defend against price pressure as competition intensifies.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive dynamics in the Galvanic Isolated High‑side Switch market

The segment is anchored by a handful of large‑scale semiconductor firms that command the majority of volume. STMicroelectronics and Infineon dominate owing to deep automotive portfolios, extensive verification infrastructure, and the ability to embed isolation, protection and diagnostics within a single silicon block. Their pricing power stems from economies of scale in wafer processing and a mature supply chain that keeps capacity utilization near optimal levels. Texas Instruments leverages its analog expertise to offer highly configurable high‑side switches that appeal to industrial OEMs seeking flexible design windows. These leaders have systematically broadened product families across 12 V and 24 V families, thereby locking in long‑term platform agreements with Tier‑1 vehicle manufacturers and reducing the incentive for customers to engage lower‑margin niche suppliers.Beyond the top tier, a dense constellation of midsized players adds depth to the ecosystem. Diodes Incorporated, ROHM, Renesas, Fuji Electric, Microchip Technology and ON Semiconductor each specialize in particular voltage ranges or interface standards such as PWM or SPI, carving out profitable niches in regional automotive clusters or in high‑performance industrial drives. NXP Semiconductors, Analog Devices and Maxim Integrated (now part of ADI) pursue differentiated value through advanced diagnostics and built‑in self‑test features, targeting safety‑critical applications where failure cost outweighs unit price. Companies like Toshiba and Cypress Semiconductor (now under Infineon) focus on niche markets such as electric‑bus powertrains and renewable‑energy inverters, where bespoke reliability credentials are a decisive factor. This layered structure creates a competitive arena where scale‑driven pricing coexists with differentiated technology that can command premium spreads.

List of Key Galvanic Isolated High-side Switch Companies Profiled

- STMicroelectronics

- Infineon Technologies

- Diodes Incorporated

- ROHM Semiconductor

- Renesas Electronics

- Fuji Electric

- Texas Instruments

- Microchip Technology

- ON Semiconductor

- Toshiba Electronic Devices

- NXP Semiconductors

- Analog Devices

- Maxim Integrated (ADIT)

- Cypress Semiconductor

- Fairchild Semiconductor

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

12V Controller provides robust isolation for low‑voltage automotive domains, simplifying board layouts and reducing external component count.

|

| By Application |

|

Automotive drives demand for galvanic isolation due to stringent safety standards and growing electrical complexity.

|

| By End User |

|

OEMs prioritize integrated high‑side switches to streamline platform development.

|

| By Integration Strategy |

|

Embedded Isolation is increasingly favored for its ability to shave board area and simplify validation.

|

| By Safety Regulation Focus |

|

Functional Safety shapes product roadmaps as manufacturers align isolation performance with safety integrity levels.

|

Regional Analysis: Galvanic Isolated High-side Switch Market

North America

Vehicle manufacturers are integrating Galvanic Isolated High-side Switches to safeguard battery management systems against transient spikes, a move that improves durability while meeting consumer expectations for longer range and faster charging. The technology’s ability to isolate high‑current paths without sacrificing response time is reshaping power‑train architecture across the continent.

Factories that operate 24/7 are replacing legacy relays with galvanically isolated switches to reduce downtime caused by fault propagation. The quieter switching profile supports precision motor drives, which in turn allows manufacturers to squeeze higher throughput from existing production lines.

Recent amendments to UL and IEC standards emphasize isolation performance, prompting OEMs to reconsider component selection. Companies that pre‑emptively align product designs with these expectations are gaining a compliance head‑start that translates into smoother market entry.

The concentration of silicon‑on‑insulator wafer suppliers in the region has encouraged North American firms to develop vertical integration strategies, minimizing lead‑time risk and securing a stable supply of high‑performance isolation substrates.

Europe

European manufacturers are leveraging Galvanic Isolated High-side Switches to satisfy the continent’s aggressive targets for vehicle electrification and grid‑connected renewable installations. German and French OEMs view isolation as a safety net that enables higher voltage architectures, while the United Kingdom’s push for offshore wind infrastructure creates demand for robust inverter modules. The regulatory environment, shaped by EU directives on electromagnetic compatibility, forces component suppliers to prove isolation integrity across a broad temperature envelope, nudging the market toward more resilient designs. Consequently, cross‑border consortia are emerging, pooling R&D resources to accelerate the qualification of next‑generation switches for both automotive and energy sectors.

Asia‑Pacific

Asia‑Pacific’s rapid industrialization, especially in China, India, and Vietnam, fuels a steady appetite for power‑efficient modules that contain fault currents. Manufacturers in these economies are adopting Galvanic Isolated High-side Switches to meet both domestic energy‑efficiency mandates and the expectations of customers. The region’s burgeoning electric‑vehicle market benefits from isolation technology that protects high‑voltage battery packs, while semiconductor hubs in Taiwan and South Korea are experimenting with advanced packaging that further reduces parasitic losses. This blend of demand and manufacturing capability positions the Asia‑Pacific as a future growth engine, though it still trails North America in overall market size.

South America

In South America, the market is shaped by a mix of legacy power‑distribution challenges and emerging renewable‑energy projects. Brazil’s investment in solar‑farm inverters has spotlighted the necessity for switches that can isolate high‑current strings without compromising efficiency. Meanwhile, automotive assemblers in Argentina are beginning to incorporate galvanic isolation into low‑volume electric‑vehicle prototypes, testing the technology’s durability in tropical climates. The region’s limited local silicon‑on‑insulator capacity pushes firms to form import agreements, encouraging the development of service‑oriented partnerships that focus on after‑sales support and field reliability.

Middle East & Africa

The Middle East & Africa sees Galvanic Isolated High-side Switch adoption primarily in oil‑field automation and nascent solar‑energy installations. United Arab Emirates and Saudi Arabia are retrofitting existing power‑distribution networks with isolation‑centric controllers to improve safety in harsh desert conditions. In Africa, cell‑tower operators are experimenting with the switches to protect base‑station power supplies from lightning strikes, a common hazard that threatens uptime. Though overall market volume remains modest, the strategic relevance of isolation for critical infrastructure is prompting early‑stage collaborations between multinational vendors and regional utilities.

Report Scope

This market research report provides a comprehensive analysis of the Galvanic Isolated High-side Switch Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Galvanic Isolated High-side Switch Market?

-> Galvanic Isolated High-side Switch Market was valued at USD 202 million in 2025 and is expected to reach USD 372 million by 2032.

Which key companies operate in Galvanic Isolated High-side Switch Market?

-> Key players include STMicroelectronics, Infineon, Diodes Incorporated, ROHM, Renesas, Fuji Electric, Texas Instruments, Microchip, onsemi, Toshiba, among others.

What are the key growth drivers?

-> Key growth drivers include stricter safety regulations, rising electromagnetic complexity in automotive and industrial power systems, and the broader electrification trend that demands robust galvanic isolation for reliability and fault containment.

Which region dominates the market?

-> The market is ly balanced with major automotive and industrial applications across all regions; no single region distinctly dominates at present.

What are the emerging trends?

-> Emerging trends include integration of isolation, protection and diagnostics into compact architectures, increased platform reuse to spread qualification costs, and a focus on achieving higher reliability while reducing bill‑of‑materials through component minimisation.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...