High-Side FET Drivers Market Insights

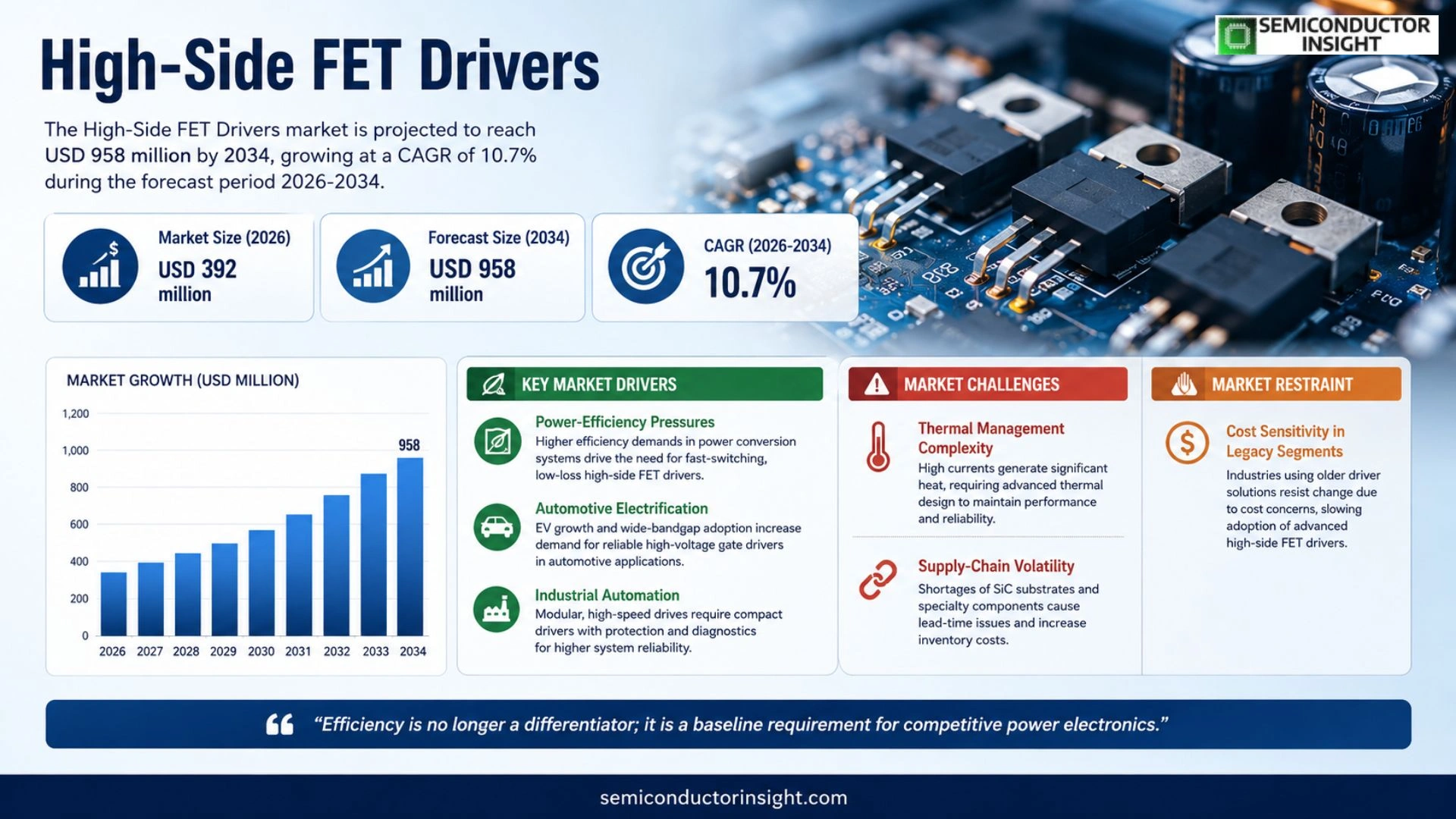

Global High-Side FET Drivers market size was valued at USD 384 million in 2025. The market is projected to grow from USD 958 million by 2034, exhibiting a CAGR of 10.7 % during the forecast period.

High‑Side FET Drivers are high‑side gate‑driver integrated circuits that translate low‑voltage control signals into robust gate‑drive waveforms for power MOSFETs, enabling fast switching, built‑in protection and efficient power conversion in automotive electrification platforms and industrial automation equipment.

The expansion stems from accelerating electric‑vehicle adoption, tighter safety regulations for high‑voltage systems and growing automation intensity across factories. Vendors such as STMicroelectronics, Infineon and Texas Instruments are strengthening their positions by embedding diagnostics, high‑voltage isolation and accelerated design‑in services that reduce system cost and shorten time‑to‑market.

MARKET DRIVERS

Power‑Efficiency Pressures

The push for lower losses in DC‑DC converters and motor‑drive systems has moved designers toward High‑Side FET Drivers Market solutions that can switch quickly while keeping conduction loss to a minimum. This trend is reinforced by tighter energy‑consumption standards in data‑center power supplies, where every watt saved translates directly into operational cost reductions.

Automotive Electrification

Electrified power‑train architectures rely on precise gate control for high‑voltage nodes, making robust high‑side drivers indispensable. As manufacturers broaden their EV line‑ups, the demand for drivers that can operate reliably over a wide temperature envelope and survive automotive‑grade stress testing has surged.

➤ “Efficiency is no longer a differentiator; it is a baseline requirement for competitive power electronics.”

In industrial automation, the shift toward modular, high‑speed drives places a premium on driver ICs that combine low‑gate charge with integrated protection features. Vendors that embed thermal shutdown and fault‑monitoring within a compact footprint are capturing a disproportionate share of new system designs.

MARKET CHALLENGES

Thermal Management Complexity

High‑current operation forces designers to address heat dissipation early in the layout stage. Inadequate thermal paths can degrade switching performance, leading to premature failure in high‑density applications such as railway traction converters.

Other Challenges

Supply‑Chain Volatility

Component shortages for silicon carbide substrates and specialty passives have introduced lead‑time uncertainties, compelling OEMs to hold larger safety stocks and potentially inflating total cost of ownership.

Concurrently, the need for compliance with increasingly stringent electromagnetic‑interference (EMI) regulations adds design overhead, as manufacturers must incorporate additional filtering or shielding to meet certification thresholds.

MARKET RESTRAINTS

Cost Sensitivity in Legacy Segments

Industries that have traditionally relied on bipolar transistors or older MOSFET driver families are reluctant to overhaul existing Bill‑of‑Materials. The perceived premium of advanced high‑side drivers, despite long‑term savings, slows adoption in cost‑tight equipment.

Design‑Tool Fragmentation

The ecosystem of simulation and verification tools for high‑side driver topologies remains uneven. Engineers often face steep learning curves when integrating new IP blocks, which can extend development cycles and deter smaller firms from pursuing the latest driver architectures.

MARKET OPPORTUNITIES

Integration with SiC Power Modules

Silicon‑carbide power devices are gaining traction in high‑voltage applications, and the demand for driver ICs that can handle their rapid voltage transitions is rising. Companies that co‑design drivers alongside SiC switches stand to benefit from bundled solutions that simplify system integration.

Emerging Renewable‑Energy Installations

Large‑scale solar inverters and wind‑turbine converters require drivers capable of sustained high‑frequency operation while maintaining reliability under fluctuating environmental conditions. Tailoring driver families for these renewable‑energy niches opens a sizable revenue channel as global clean‑energy capacity expands.

High-Side FET Drivers Market Trends

Higher Integration Drives System-Level Efficiency

High‑Side FET Drivers Market is moving beyond basic gate‑drive functionality toward tightly integrated modules that embed protection, diagnostics and high‑voltage isolation. This evolution stems from automotive electrification, where voltage levels climb and safety regulations tighten, and from industrial automation, where dense power stages demand lower electromagnetic emissions. By consolidating multiple functions into a single silicon block, suppliers reduce board‑level component count, which translates into smaller footprints and lower overall system loss. Customers that adopt these integrated solutions see faster time‑to‑market because the design‑in effort shrinks; the driver IC already satisfies the bulk of the reliability tests required for vehicle or factory‑equipment qualification. Consequently, the value proposition shifts from pure cost per unit to total cost of ownership, rewarding vendors that can demonstrate measurable reductions in failure rates and energy waste. Such integration also eases thermal management, as fewer discrete components reduce localized heating, further enhancing reliability in harsh automotive environments.

Other Trends

Supply‑Chain Stability and Capacity Utilization

Supply‑chain stability and capacity utilization have become pivotal in shaping the competitive landscape. The upstream ecosystem,silicon wafers from firms such as Shin‑Etsu and GlobalWafers and advanced packaging substrates from Ibiden and AT&S,underpins the ability to meet steady demand. In 2025, capacity utilization hovered around the mid‑60 percent range, indicating that manufacturers retain headroom to absorb spikes in automotive program launches without compromising yield. Firms that synchronize wafer procurement with production schedules can protect gross margins, which typically settle near the half‑mark. Moreover, consistent packaging reliability limits field returns, reinforcing the reputation of suppliers that manage both material quality and test throughput diligently. Maintaining this balance enables suppliers to deliver consistent lead times, a factor that many automotive OEMs now flag as a strategic risk.

Design‑In Depth and Qualification Speed as Competitive Levers

Design‑in depth and qualification speed now serve as decisive levers for market participants. Companies that offer extensive application support, from reference designs to accelerated test kits, enable OEMs to compress qualification cycles that previously stretched over months. Multi‑channel driver families that span low, medium and high‑voltage segments allow a single product line to serve diverse vehicle subsystems, fostering platform reuse across model generations. This breadth reduces engineering effort and spreads development costs, a benefit that directly influences profitability in a market where pricing pressure remains intense. In High‑Side FET Drivers Market, the firms that couple manufacturing stability with demonstrable system‑level savings are best positioned to preserve margin headroom while meeting rising expectations for reliability and efficiency. Consequently, the competitive agenda centers on building a portfolio that can be instantly adapted to emerging voltage domains and safety standards.

COMPETITIVE LANDSCAPE

Key Industry Players

High‑Side FET Drivers – Competitive Overview

The market is anchored by a handful of global semiconductor firms that combine deep automotive design expertise with large‑scale silicon procurement. Infineon, Texas Instruments and STMicroelectronics together command the bulk of revenue, largely because they can qualify devices across multiple voltage families while maintaining a consistent gross‑margin profile. Their ability to ship fully qualified, automotive‑grade parts from multiple foundry partners reduces lead‑time for Tier‑1 OEMs and reinforces a defensible pricing position. Each of these leaders has rolled out driver families that embed protection, diagnostics and bootstrap charge‑pump circuits, which translates into lower system‑level component counts for vehicle electrification programs.

Beyond the tier‑one cohort, a diverse set of niche specialists adds depth to the competitive set. ROHM and Renesas focus on medium‑voltage, single‑channel architectures that appeal to industrial motor‑drive designers, while Diodes Incorporated and Fuji Electric excel in high‑voltage, multi‑channel modules for traction‑inverter applications. ON Semiconductor and Microchip leverage flexible packaging options to serve low‑cost automotive subsystems, whereas Toshiba and NXP target emerging markets such as electric‑bus power‑train controllers. The breadth of these players creates a landscape where design‑in depth and application‑specific support are as decisive as raw shipment volumes.

List of Key High‑Side FET Drivers Companies Profiled

- Infineon – broad portfolio with integrated protection and automotive qualification.

- Texas Instruments – extensive driver families covering low‑ to high‑voltage segments.

- STMicroelectronics – focuses on high‑reliability drivers for power‑train and industrial automation.

- ON Semiconductor – strong in cost‑effective solutions for automotive body‑control modules.

- ROHM Semiconductor – medium‑voltage, single‑channel drivers aimed at motor‑drive markets.

- Renesas Electronics – offers integrated diagnostics for industrial power converters.

- Diodes Incorporated – high‑voltage, multi‑channel families for traction‑inverter designs.

- Fuji Electric – specializes in high‑voltage isolation and robust packaging for railway applications.

- Microchip Technology – provides flexible SOIC/TSSOP options for low‑cost automotive subsystems.

- Toshiba – leverages its power‑device legacy to deliver high‑voltage driver modules for EV chargers.

- NXP Semiconductors – focuses on secure, automotive‑grade drivers with integrated safety features.

- Analog Devices – combines precision analog front‑ends with driver ICs for industrial automation.

- Maxim Integrated – delivers niche low‑power drivers for battery‑management systems.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Integrated Protection Drivers are emerging as the leading type because they embed over‑current, over‑temperature and undervoltage lockout directly within the gate‑drive IC, reducing board‑level component count and minimizing failure points. • Customers value the ability to shorten design‑in cycles by sourcing a single IC that delivers both drive strength and safety functions. • Suppliers that provide robust isolation and low‑noise performance gain stronger design‑in relationships with automotive OEMs and industrial equipment makers. |

| By Application |

|

Automotive Powertrain dominates qualitative demand due to the push for higher voltage architectures and stricter safety standards. • High‑side drivers that deliver superior EMC performance and integrated diagnostics enable vehicle manufacturers to meet reliability targets while reducing overall system cost. • In industrial motor drives, robustness against harsh temperature cycles and ability to support dense power stages make high‑integration drivers the preferred choice. |

| By End User |

|

OEM Automotive Engineers are the primary decision‑makers, seeking drivers that simplify qualification across multiple vehicle programs. • Preference for families that offer scalable voltage ranges and consistent pin‑compatible footprints accelerates platform reuse. • Close collaboration with suppliers that provide comprehensive design‑in support and accelerated testing kits is a decisive advantage. |

| By Integration Level |

|

System‑in‑Package (SiP) Solutions are gaining traction as they combine high‑side driver, protection, and diagnostics into a compact footprint. • This integration reduces PCB real‑estate and improves thermal performance, which is critical for densely packed automotive converters. • Vendors that can assure reliable assembly and long‑term reliability under high‑voltage stress differentiate themselves in a competitive market. |

| By Voltage Range |

|

High‑Voltage (>60 V) Drivers are identified as the most strategically important segment because emerging EV architectures are moving toward 400‑800 V systems. • Designers prioritize devices that combine high isolation, low gate‑charge loss, and robust latch‑up protection to sustain efficiency at elevated stresses. • Suppliers that can deliver consistent performance across the entire voltage envelope enable smoother migration for OEMs upgrading from medium‑voltage platforms. |

Regional Analysis: High-Side FET Drivers Market

North America

Vehicle manufacturers are integrating High‑Side FET Drivers into power‑train modules to manage battery‑to‑motor conversion more efficiently. The drivers’ ability to handle rapid transient loads while preserving gate integrity is reshaping inverter design, prompting a shift toward consolidated driver‑controller solutions.

Factories upgrading to flexible manufacturing cells rely on drivers that combine high voltage handling with low EMI footprints. This enables smoother integration with variable‑frequency drives, reducing the need for ancillary filtering components.

Portable power supplies and high‑performance audio amplifiers are benefitting from compact driver packages that deliver fast switching without sacrificing reliability, supporting the trend toward thinner, more power‑dense devices.

EDA tools are now embedding reference designs for High‑Side FET Drivers, shortening time‑to‑market for system integrators. The enhanced simulation accuracy helps engineers anticipate thermal and gate‑drive challenges early in the development cycle.

Europe

European manufacturers are capitalizing on stringent emission regulations to accelerate the adoption of electric drivetrains, which in turn fuels demand for robust driver solutions. Companies in Germany and France are collaborating with semiconductor foundries to co‑develop drivers that can operate at higher temperatures, allowing for tighter packaging in power modules. The region’s strong focus on sustainability also drives innovation in driver efficiency, as OEMs seek to reduce overall system losses.

Asia‑Pacific

The Asia‑Pacific landscape is shaped by a mix of rapid consumer electronics growth and emerging electric‑vehicle infrastructure. Chinese and South Korean firms are leveraging scale to produce cost‑effective driver families, while also investing in SiC‑compatible designs that cater to high‑power automotive applications. In India, expanding industrial parks are prompting a need for drivers that can handle wide voltage ranges, encouraging local suppliers to diversify their portfolios.

South America

South American markets are experiencing a gradual shift toward renewable‑energy projects, particularly solar‑farm installations that rely on inverter technologies. The region’s manufacturers are beginning to source High‑Side FET Drivers that provide reliable gate control under fluctuating environmental conditions, a requirement for outdoor power systems. Local design houses are also exploring partnerships with North American vendors to gain access to advanced driver IP.

Middle East & Africa

In the Middle East and Africa, the convergence of oil‑reducing initiatives and data‑center expansion is creating niche opportunities for driver technologies that support high‑density power conversion. Gulf states are funding pilot projects that test driver‑centric architectures in utility‑scale storage, while African telecom operators are prioritizing drivers that can sustain long‑duration operation in harsh climates. The emerging demand is steering regional suppliers toward more rugged driver packages.

Report Scope

This market research report provides a comprehensive analysis of the High-Side FET Drivers Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of High-Side FET Drivers Market?

-> High-Side FET Drivers market size was valued at USD 384 million in 2025. The market is projected to grow from USD 958 million by 2034, exhibiting a CAGR of 10.7 %

Which key companies operate in High-Side FET Drivers Market?

-> Key players include STMicroelectronics, Infineon, Diodes Incorporated, ROHM, Renesas, Fuji Electric, Texas Instruments, Microchip, onsemi, Toshiba.

What are the key growth drivers?

-> Key growth drivers include automotive electrification, industrial automation, higher voltage domains, and the demand for integrated protection and diagnostics within drivers.

Which region dominates the market?

-> Asia-Pacific leads the market, driven by major automotive OEMs such as Toyota and BYD, as well as growing industrial automation adoption.

What are the emerging trends?

-> Emerging trends include greater integration of protection, diagnostics, and high‑voltage isolation, as well as platform‑level reuse across vehicle and industrial programs to reduce design‑in time and overall system cost.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...