CW DFB Laser Chip Market Insights

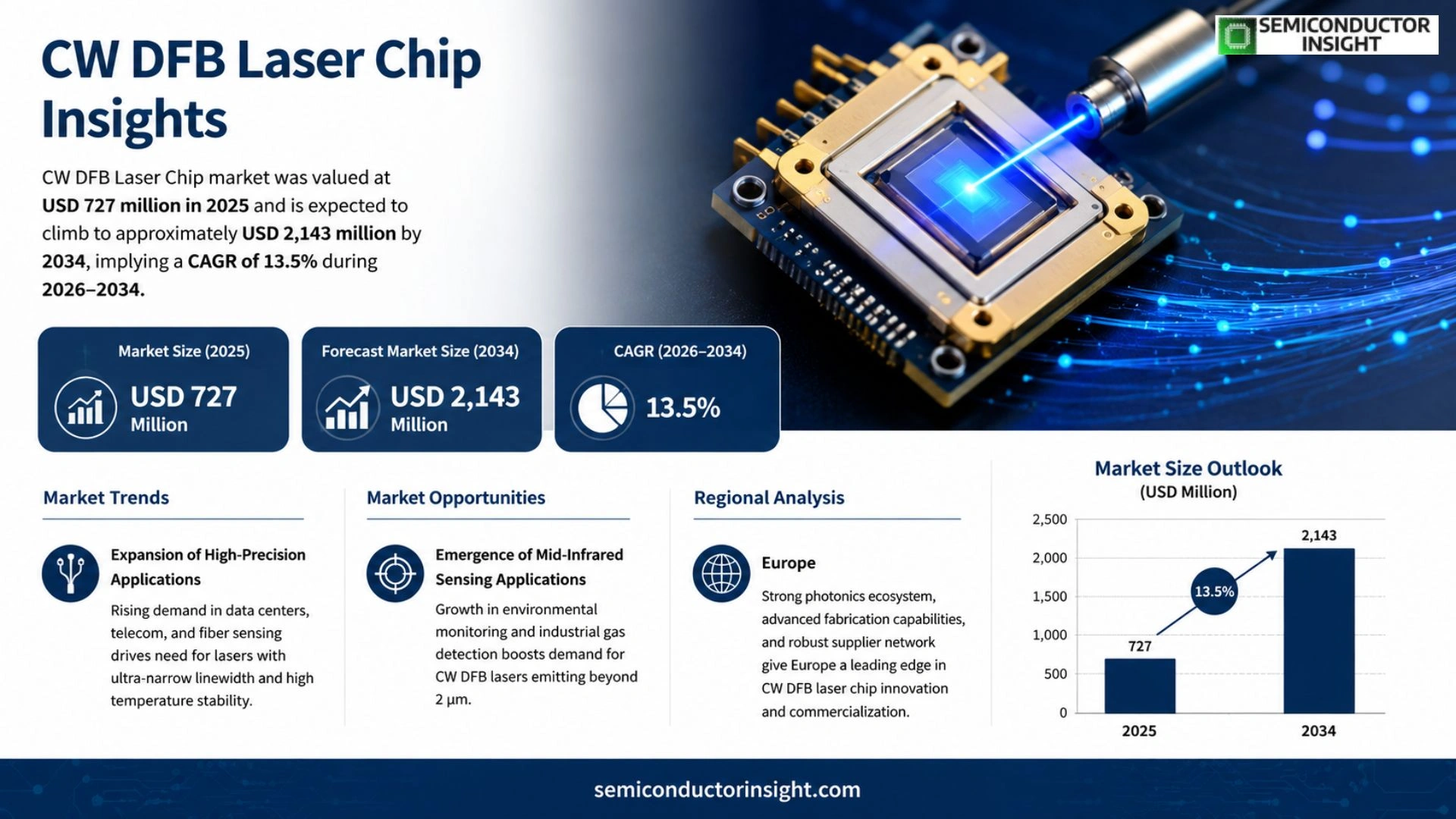

CW DFB Laser Chip market was valued at USD 727 million in 2025 and is expected to climb to approximately USD 2,143 million by 2034, implying a compound annual growth rate of roughly 13.5 % over the forecast horizon.

CW DFB Laser Chip operates as a continuous‑wave distributed feedback device that delivers a single longitudinal mode output through integrated gratings within its active region. Its narrow linewidth, high edge‑mode suppression ratio and strong temperature stability make it a fundamental light‑source component for optical communication links, gas‑sensing modules, spectral analysis instruments and high‑precision measurement systems.

Market expansion stems from heightened spending on broadband infrastructure, accelerating adoption of data‑center interconnects and growing demand for low‑power, high‑reliability sensing solutions. Technological advances in epitaxial material quality, low‑noise packaging and silicon photonic integration further enhance device performance while reducing cost per unit. Meanwhile, policy initiatives promoting domestic optoelectronic capabilities reinforce supply‑chain resilience across key regions.

MARKET DRIVERS

Rising Demand for High‑Speed Data Links

The surge in telecommunications infrastructure,particularly 5G roll‑outs and metro‑area network upgrades,has forced equipment makers to seek components that can sustain narrow linewidth and high output power. CW DFB Laser Chip Market suppliers that can guarantee tight wavelength control are becoming preferred partners, because operators cannot compromise on signal integrity.

Growth of Integrated Photonics Platforms

Manufacturers of silicon photonics and compound‑semiconductor modules are embedding continuous‑wave distributed feedback lasers to achieve compact, energy‑efficient solutions. This trend pushes vendors to invest in wafer‑scale production lines, which in turn lowers unit costs and widens the addressable customer base.

➤ Customers are now valuing module reliability as much as raw performance, prompting a shift toward lasers with proven long‑term stability.

Finally, the expanding use of lidar in autonomous‑vehicle prototypes has introduced a parallel revenue stream. Suppliers that can adapt their CW DFB designs to meet the tight pulse‑width specifications of ranging systems stand to capture a sizable slice of this emerging market.

MARKET CHALLENGES

Stringent Temperature‑Control Requirements

Many end‑applications operate in environments where temperature swings exceed ±30 °C. Maintaining single‑mode operation across that range forces manufacturers to implement sophisticated packaging and active cooling, which adds to bill‑of‑materials and complicates supply chains.

Other Challenges

Supply‑Chain Volatility

The reliance on rare‑earth substrates and specialty epitaxial processes means that geopolitical tensions or raw‑material shortages can quickly translate into lead‑time spikes, eroding customer confidence.

MARKET RESTRAINTS

Capital‑Intensive Manufacturing Footprint

Establishing a clean‑room capable of producing high‑yield CW DFB chips requires multi‑million‑dollar investment. Smaller players often lack the financial bandwidth to scale, creating a market dominated by a few large incumbents and limiting competitive pricing.

Moreover, the necessity for rigorous qualification cycles,especially for aerospace and defense contracts,extends time‑to‑market. Companies that cannot absorb the upfront testing costs may forfeit contracts, constraining overall market expansion.

MARKET OPPORTUNITIES

Emergence of Mid‑Infrared Sensing Applications

Mid‑infrared spectroscopy, driven by environmental monitoring and industrial gas detection, increasingly relies on CW DFB sources that emit beyond 2 µm. Companies that can extend their wavelength palette while preserving low noise will unlock a niche yet rapidly growing segment.

The advent of quantum‑key‑distribution (QKD) networks also presents a fertile arena. Because QKD protocols demand stable, narrow‑linewidth lasers, entrants that align their product roadmaps with quantum‑communication standards could secure long‑term contracts with research institutions and telecom operators.

Finally, strategic collaborations between laser foundries and foundry‑agnostic packaging firms are reshaping the value chain. By offering turn‑key solutions that combine epitaxial expertise with advanced assembly, these alliances reduce entry barriers for OEMs seeking to embed CW DFB chips into next‑generation photonic integrated circuits.

CW DFB Laser Chip Market Trends

Expansion of High‑Precision Applications

CW DFB Laser Chip Market is seeing a noticeable shift toward applications that demand sub‑kilohertz linewidth and high temperature stability. Data‑center upgrades and the rollout of next‑generation fiber networks have created a steady stream of orders for chips that can maintain phase coherence over long distances. Simultaneously, industrial gas‑sensing installations are adopting narrower‑linewidth devices to improve detection limits, especially in energy and environmental monitoring. This convergence of communication and sensing needs is raising the average selling price for premium chips while preserving healthy margins for manufacturers that can deliver consistent wafer yields.

Other Trends

Supply‑Side Consolidation and Technology Integration

On the supply side, manufacturers with in‑house epitaxial growth are gaining decisive advantage because they control the 40 % material cost component and can respond quickly to yield fluctuations. The 25 % processing cost tied to photolithography and etching is being reduced through the adoption of silicon‑photonic integration platforms, which also lower the 15 % packaging expense by enabling higher‑density module assembly. Companies that have coupled wafer‑scale process control with advanced packaging are establishing a de‑facto barrier to entry, concentrating market share among a handful of players capable of delivering both low‑linewidth and higher‑power variants.

Pricing Dynamics Across Product Segments

Standard communication‑grade DFB chips are experiencing gradual price erosion as production volumes climb, whereas chips targeting ultra‑narrow linewidth (<1 kHz) and special‑wavelength bands retain premium pricing because of their limited production runs and higher R&D intensity. This bifurcated pricing structure sustains overall profitability for CW DFB Laser Chip Market while prompting vendors to diversify portfolios between high‑volume, cost‑competitive items and niche, high‑margin solutions.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive Landscape of CW DFB Laser Chip Market

Coherent dominates the high‑power segment by leveraging a vertically integrated supply chain that spans epitaxial growth, wafer fabrication, and advanced packaging. Its ability to deliver consistent yields above 85 % has forced other manufacturers to either specialize in niche wavelengths or invest heavily in process automation. Lumentum, with a broad portfolio of C‑band devices, competes closely on price‑to‑performance ratios, thanks to large‑scale production in its North American fabs. Sumitomo Electric and Mitsubishi Electric each control critical epitaxial technology in Japan, enabling them to secure contracts for data‑center interconnects where temperature stability is paramount. Furukawa Electric distinguishes itself through silicon‑photonic hybrid integration, positioning its chips as core components for next‑generation coherent transceivers. The market structure therefore reflects a tiered hierarchy: a handful of vertically integrated leaders capture the bulk of high‑margin contracts, while a second layer of specialized firms targets application‑specific niches.

Beyond the primary tier, a diverse set of companies sustains the ecosystem by focusing on specialized wavelengths, ultra‑narrow linewidths, or cost‑effective sensor solutions. YUANJIE TECHNOLOGY and Henan Shijia Photons Technology have built regional dominance in the Chinese gas‑sensing market by offering sub‑10 kHz linewidth chips at competitive prices. Applied Optoelectronics and Macom supply mid‑range power modules for fiber‑access equipment, emphasizing modularity and rapid time‑to‑market. LuxNet Corporation and Xiamen Sanan Integrated concentrate on tunable DFB platforms that cater to emerging scientific instrumentation. LiVe Optronics, WaveSplitter Technologies, Inc., and DenseLight Semiconductors address high‑precision metrology and quantum‑information use cases, where performance outweighs cost considerations. Their presence creates a vibrant competitive pressure that encourages continual innovation across the value chain.

List of Key CW DFB Laser Chip Companies Profiled

- Coherent, Lumentum, Sumitomo Electric, Mitsubishi Electric, Furukawa Electric

- Coherent, Lumentum, Sumitomo Electric

- YUANJIE TECHNOLOGY, Henan Shijia Photons Technology, Applied Optoelectronics, Macom, LuxNet Corporation, Xiamen Sanan Integrated, LiVe Optronics, WaveSplitter Technologies, Inc., DenseLight Semiconductors

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Low‑Power Application Chip is favored for compact sensing modules because it offers minimal thermal load, simplifies system cooling, and aligns with cost‑sensitive deployment scenarios.

|

| By Application |

|

Optical Communication Networks remain the dominant demand driver as operators upgrade to higher‑capacity fiber infrastructures and data‑center interconnects.

|

| By End User |

|

Communication Equipment Manufacturers prioritize reliability and integration simplicity to meet the aggressive rollout schedules of broadband networks.

|

| By Wavelength |

|

C‑Band dominates because it aligns with existing ITU‑standardized optical fiber windows, simplifying network equipment design.

|

| By Power Level |

|

Medium‑Power Modular Chip is increasingly attractive for data‑center interconnects and high‑resolution spectroscopy where output power must balance signal strength and thermal management.

|

Regional Analysis: CW DFB Laser Chip Market

Europe

Collaborative programs funded by the EU accelerate chip‑level innovations, enabling joint access to test facilities that would be prohibitively costly for a single entity.

Localized silicon‑on‑insulator wafer sources reduce exposure to geopolitical shocks, ensuring a steadier flow of raw material for laser fabrication.

Growth in precision spectroscopy drives requests for ultra‑stable continuous‑wave sources, prompting vendors to offer tailored linewidth solutions.

Tax credits for high‑tech manufacturing in several EU member states lower capital expenses for expanding cleanroom capacity.

North America

The United States continues to leverage its extensive telecom backbone, but CW DFB Laser Chip niche is shaped more by defense contracts than by commercial roll‑outs. Federal research labs finance long‑term investigations into low‑noise architectures, yet the commercial translation often lags behind European timelines. Companies that can bridge this gap,by packaging laboratory‑grade lasers into ruggedized modules,stand to capture contracts with both defense and emerging data‑center players seeking precise wavelength control. Supply continuity remains a concern, as reliance on imported substrates can introduce latency; recent initiatives to localize silicon substrate production aim to mitigate that risk.

Asia‑Pacific

In the Asia‑Pacific corridor, rapid expansion of 5G and forthcoming 6G deployments fuels a pragmatic appetite for cost‑effective laser solutions. While the region boasts high‑volume manufacturing capability, the emphasis is on scaling mature designs rather than pioneering ultra‑narrow linewidth sources. Domestic foundries are beginning to upgrade their epitaxial growth tools, yet the learning curve means that current offerings often trail behind the performance envelope of European and North American products. Market entrants that can provide reliable, mid‑range performance at competitive pricing are gaining traction among telecom operators looking to balance performance with capital constraints.

South America

South American adoption of CW DFB laser chips is still in an exploratory phase, with most activity centered around research institutions and pilot projects in Brazil and Chile. The region’s limited local fab capacity forces reliance on imports, which elevates component cost and stretches lead times. Nevertheless, emerging applications in agricultural sensing and environmental monitoring are creating niche demand pockets. Firms that can supply turn‑key solutions,including calibration services,are better positioned to establish footholds before larger multinational players enter the market.

Middle East & Africa

Growth prospects in the Middle East and Africa hinge on strategic infrastructure programs, particularly in smart‑city initiatives and defense modernization. Investment in optical‑backhaul networks is prompting interest in reliable continuous‑wave sources, yet the market remains fragmented. Local distributors often act as intermediaries, adding another layer to the supply chain. Companies that can navigate regional procurement processes and offer on‑site technical support are likely to win contracts that prioritize reliability over sheer performance.

Report Scope

This market research report provides a comprehensive analysis of the CW DFB Laser Chip Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of CW DFB Laser Chip Market?

-> CW DFB Laser Chip Market was valued at USD 727 million in 2025 and is expected to reach USD 1662 million by 2032 with a CAGR of 13.5%.

Which key companies operate in CW DFB Laser Chip Market?

-> Key players include Coherent, Sumitomo Electric, Mitsubishi Electric, Furukawa Electric, Lumentum, Broadcom, YUANJIE TECHNOLOGY, Henan Shijia Photons Technology, Applied Optoelectronics (AOI), Macom, LuxNet Corporation, Xiamen Sanan Integrated, LiVe Optronics Company, WaveSplitter Technologies, Inc., DenseLight Semiconductors.

What are the key growth drivers?

-> Key growth drivers include policy support for broadband and intelligent manufacturing, rising demand from data centers and urban optical networks, increased adoption in gas sensing and fiber‑optic sensing, and technological advances such as improved epitaxial material quality, low‑noise design, high‑stability packaging, and silicon optical integration.

Which region dominates the market?

-> Asia-Pacific leads the market due to strong telecom infrastructure upgrades, extensive data‑center expansion, and high adoption in sensing applications, while Europe remains a significant contributor.

What are the emerging trends?

-> Emerging trends include silicon‑photonic integration, ultra‑narrow linewidth and high‑power premium segments, higher‑density optical modules, and collaborative development between chip manufacturers and packaging/module providers.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...