Integrated High-side Switch Market Insights

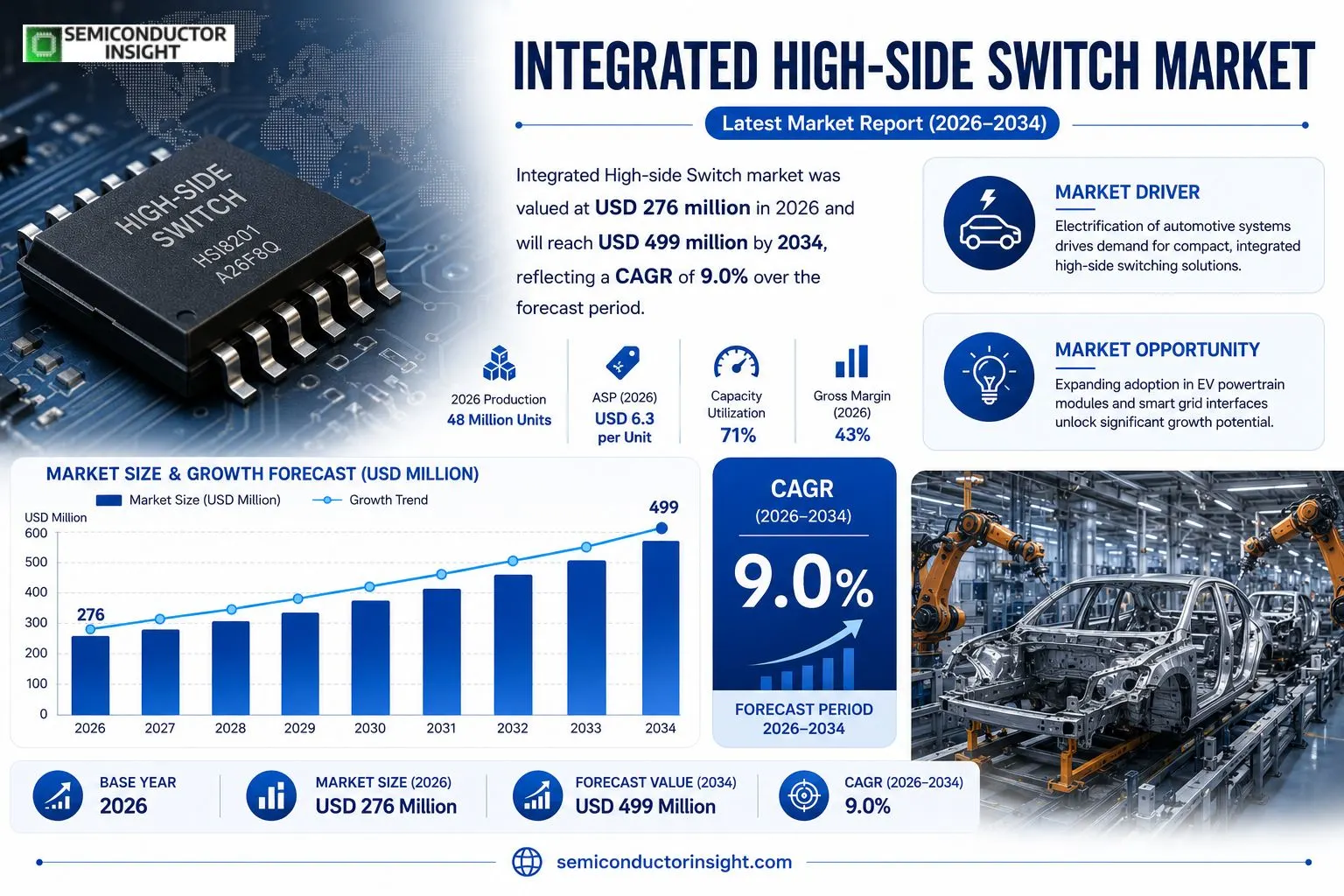

Integrated High-side Switch market was valued at USD 276 million in 2026 and will reach USD 499 million by 2034, reflecting a CAGR of 9.0 % over the forecast period.

Integrated High-side Switch is a monolithic power device that combines the high‑side switching element with control logic, protection features and basic diagnostics, allowing safer and more compact load management while reducing external components and overall system complexity.In 2026 production totaled roughly 48 million units at an average selling price of USD 6.3 per unit; the industry operated at a capacity utilization of about 71 % and delivered an average gross margin near 43 %, underscoring how integration‑driven bill‑of‑materials savings sustain profitability.

MARKET DRIVERS

Electrification of Automotive Systems

The rise of electric‑drive architectures demands precise control of power distribution. Integrated High-side Switch Market players are benefitting from the shift because a single chip can combine MOSFET, driver, and protection functions, reducing board space and simplifying thermal design. OEMs are increasingly specifying such devices to meet weight‑saving targets and to accelerate development cycles.

Growth of Industrial IoT Nodes

Edge devices operating in harsh environments rely on robust power gating. By embedding fault‑handling and diagnostics, integrated high‑side switches enable longer uptime and lower maintenance costs, a proposition that resonates with manufacturers of smart factories. Factory automation leaders view this capability as a competitive differentiator for modular equipment platforms.

➤ “A single‑sourced high‑side solution can cut PCB area by up to 40 % while delivering twice the reliability of discrete assemblies.”

Beyond automotive and factory floors, renewable‑energy converters are adopting these switches to manage inverters and battery‑management systems. The ability to meet stringent safety standards without a proliferation of external components translates into faster time‑to‑market for clean‑energy projects.

MARKET CHALLENGES

Cost Sensitivity in High‑Volume Segments

While integration offers functional benefits, the price premium associated with advanced silicon processes can erode margins in mass‑produced consumer electronics. Tier‑1 suppliers are pressured to negotiate volume discounts, which can delay the adoption of newer device families.

Other Challenges

Thermal Management Complexity

As power densities climb, designers must account for cumulative heat generated by the integrated switch and surrounding components. Inadequate thermal pathways can negate the reliability gains promised by integration, prompting additional cooling measures that increase overall system cost.

MARKET RESTRAINTS

Supply‑Chain Bottlenecks for Advanced Nodes

The semiconductor industry continues to experience wafer‑fab capacity constraints, especially for 28 nm and smaller CMOS technologies used in high‑performance high‑side switches. Lead times extending beyond 12 weeks discourage some manufacturers from qualifying new parts, reinforcing reliance on legacy discrete solutions.Regulatory scrutiny around electromagnetic compatibility also adds a layer of testing that can delay product launches, particularly in automotive applications where safety certifications are non‑negotiable.

MARKET OPPORTUNITIES

Expansion into Power‑train‑Control Modules

Developers of next‑generation EV power‑train modules are evaluating integrated high‑side switches to replace multiple discrete FETs and drivers. The consolidation promises a 15 % reduction in overall module weight, directly supporting vehicle range targets. Early adopters stand to gain a technology lead that can be packaged as a value‑added service.

Smart Grid Interface Applications

Grid‑tie inverters and micro‑grid controllers require precise switching under fault conditions. Embedded protection logic within integrated devices can fulfill UL‑1741 and IEC‑61850 requirements without external safety circuits, opening a niche where system integrators can differentiate their offerings.Finally, the convergence of automotive and industrial standards around functional safety (ISO 26262, IEC 61508) creates a cross‑sector demand for components that are pre‑qualified for safety integrity levels. Companies that align product roadmaps with these standards can capture a share of the emerging safety‑critical market segment.

Integrated High-side Switch Market Trends

Platform Consolidation Fuels Integration

The automotive and industrial sectors are redesigning power architectures to embed the high‑side switch directly within control modules. By merging the switching element, protection logic, and diagnostic functions, system designers eliminate separate protection chips and reduce wiring complexity. This shift cuts board space by roughly 30 % and lowers the Bill‑of‑Materials, a benefit that translates into measurable weight savings for electric vehicle platforms. Manufacturers that can certify a single monolithic device across multiple vehicle families gain a strategic advantage because validation effort is amortized over larger production runs. The trend toward consolidated platforms also encourages OEMs to lock‑in suppliers early in the design cycle, creating a barrier to entry for newer entrants that lack proven qualification pedigrees.

Other Trends

Margin Resilience Through BOM Reduction

In 2026 the average gross margin for Integrated High-side Switch producers hovered around 43 %, a figure sustained despite modest pricing pressure in commoditized segments. The margin buffer stems largely from the Bill‑of‑Materials advantage; integrating protection and diagnostics eliminates the need for discrete components that traditionally carry higher unit costs and add failure points. Facilities that maintain a capacity utilization near 71 % can spread fixed overhead across a larger output, further protecting profitability. Companies that align product roadmaps with long‑life automotive platforms also benefit from economies of scale, as recurring orders diminish the impact of short‑term price fluctuations.

Thermal and Reliability Engineering as Differentiators

Thermal management has become a decisive factor in product selection, especially as power densities climb in modern drive‑by‑wire systems. Vendors that invest in silicon‑level thermal modeling and robust die‑attach materials achieve lower junction temperatures, which directly improves mean‑time‑between‑failures. Reliable operation across a wide temperature envelope also reduces warranty claims for end‑users, reinforcing the business case for higher‑priced, reliability‑focused solutions. The competitive landscape now rewards firms that can demonstrate consistent performance in harsh automotive environments while still offering a compact footprint, positioning them to capture premium contracts in next‑generation electric powertrain applications.

COMPETITIVE LANDSCAPE

Key Industry Players

Integrated High‑side Switch Market – Competitive Overview

The market is currently anchored by a handful of semiconductor giants whose foundry capacity and system‑level expertise allow them to command the bulk of revenue. STMicroelectronics and Infineon Technologies together account for roughly a third of 2026 sales, leveraging deep automotive portfolios and extensive validation programs that translate into higher gross margins. Their products tend to integrate multi‑channel architectures with SPI or PWM interfaces, satisfying OEM demands for reduced wiring and streamlined qualification cycles. This concentration creates a tiered structure: Tier‑1 suppliers dominate platform‑level contracts with automakers, while a secondary tier of specialized firms targets niche power‑train segments and industrial automation, where customization and rapid time‑to‑market are decisive.Beyond the dominant duopoly, a diverse set of manufacturers occupies strategic niches. Diodes Incorporated, ROHM Semiconductor, and Renesas Electronics focus on compact 12 V and 24 V controllers for body‑control modules, exploiting their analog‑design heritage. Fuji Electric and onsemi differentiate through robust thermal management suites that appeal to high‑current industrial drives. Texas Instruments and Microchip Technology prioritize developer‑friendly integration tools, attracting designers of modular inverter platforms. Toshiba and NXP Semiconductors add value with proprietary protection algorithms, while Analog Devices and Maxim Integrated (now part of Analog) emphasize precision current‑sensing features for next‑generation electric‑vehicle architectures. This breadth of capabilities ensures that competition remains focused on functional depth rather than price alone.

List of Key Integrated High-side Switch Companies Profiled

- STMicroelectronics

- Infineon Technologies

- Diodes Incorporated

- ROHM Semiconductor

- Renesas Electronics

- Fuji Electric

- Texas Instruments

- Microchip Technology

- onsemi

- Toshiba

- NXP Semiconductors

- Analog Devices

- Maxim Integrated

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Leading Segment is the 24V Controller, which resonates strongly with automotive and industrial power architectures. Its integration of protection and control reduces external component count and simplifies board layout.

|

| By Application |

|

Leading Segment is Automotive, where system‑level integration drives design choices. Integrated high‑side switches support power‑train electrification and advanced driver‑assist features.

|

| By End User |

|

Leading Segment is Vehicle manufacturers, who prioritize platform consistency and lifecycle cost.

|

| By Integration Level |

|

Leading Segment is the Smart Diagnostic Integrated Switch, which adds on‑chip health monitoring.

|

| By Power Rating |

|

Leading Segment is Medium Voltage (48V‑400V), which strikes a balance between performance and thermal management.

|

Regional Analysis: Integrated High-side Switch Market

North America

R&D spending in silicon‑carbide and gallium‑nitride devices has intensified, positioning North America as a testing ground for next‑generation high‑side switches that promise higher efficiency and smaller footprints.

Federal efficiency mandates for electric vehicles and industrial equipment push manufacturers to adopt power‑stage solutions that meet tighter loss thresholds, stimulating demand for advanced switches.

Tier‑1 automotive suppliers increasingly require integrated modules that combine switching, protection and diagnostic functions, driving consolidation among component vendors.

Established fabs leverage scale to offer competitive pricing, while agile start‑ups differentiate through specialized material technologies and rapid prototype cycles.

Europe

European manufacturers are capitalising on stringent emissions regulations that compel automotive OEMs to adopt more efficient power‑train architectures. Germany’s engineering clusters integrate high‑side switches into both passenger‑car and heavy‑duty platforms, emphasising reliability under harsh thermal cycles. Scandinavia’s focus on renewable‑energy installations drives demand for switches that can tolerate wide voltage ranges in solar‑inverter applications. The region’s emphasis on circular‑economy principles encourages vendors to design products with longer service lives and easier end‑of‑life recovery, influencing material choices and packaging strategies. Collaborative standards bodies, such as IEC, streamline qualification processes, allowing European firms to bring compliant modules to market faster than many rivals.

Asia‑Pacific

In Asia‑Pacific, rapid electrification of two‑wheelers and the proliferation of smart‑home appliances create a broad base for high‑side switch adoption. Chinese manufacturers benefit from government subsidies for electric‑vehicle production, prompting local fabs to integrate high‑performance switches directly onto power modules. Japan’s legacy semiconductor houses focus on miniaturisation, delivering ultra‑compact switches for portable medical devices. Meanwhile, Southeast Asian assemblers leverage cost‑effective assembly lines to meet the volume demands of consumer electronics, often opting for integrated solutions that reduce board count. The region’s diverse regulatory landscape leads vendors to tailor product line‑ups to accommodate varying safety and efficiency thresholds.

South America

South American markets are influenced by growing renewable‑energy projects, particularly wind farms in Brazil and solar arrays in Chile. Project developers require robust switches capable of handling intermittent generation and high fault currents, guiding suppliers toward ruggedised designs. Automotive production, while smaller than in other regions, is shifting toward hybrid models, nudging local OEMs to source switches that balance cost with durability in tropical climates. Trade agreements within Mercosur also facilitate cross‑border component flow, allowing regional distributors to consolidate inventory and offer more competitive pricing to end‑users.

Middle East & Africa

The Middle East’s focus on data‑center expansion and oil‑field automation fuels demand for high‑side switches that can operate reliably under extreme temperature swings. Gulf states invest heavily in smart‑grid infrastructure, where integrated switches serve as critical nodes for load‑balancing and fault isolation. In Africa, expanding off‑grid solar solutions demand rugged, low‑maintenance power‑stage components, prompting vendors to emphasise long‑life packaging and simple field‑replaceability. Regional procurement strategies often prioritise suppliers with strong after‑sales support, shaping the competitive landscape toward firms that can deliver rapid technical assistance.

Report Scope

This market research report provides a comprehensive analysis of the Integrated High-side Switch Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Integrated High-side Switch Market?

-> Integrated High-side Switch Market was valued at USD 276 million in 2026 and is expected to reach USD 499 million by 2034.

Which key companies operate in Integrated High-side Switch Market?

-> Key players include STMicroelectronics, Infineon, Diodes Incorporated, ROHM, Renesas, Fuji Electric, Texas Instruments, Microchip, onsemi, Toshiba, among others.

What are the key growth drivers?

-> Key growth drivers include the push for higher integration and reduced system complexity in automotive and industrial automation, demand for compact high-side load management, and the need for robust protection that lowers BOM and field failures.

Which region dominates the market?

-> Asia dominates the market, driven by major automotive OEMs and industrial automation demand, while Europe and North America also hold significant shares.

What are the emerging trends?

-> Emerging trends include deeper integration of control, diagnostics and protection functions, improved thermal performance, and broader platform‑level adoption across automotive and industrial applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...