Non-isolated Low-side Gate Drivers Market Insights

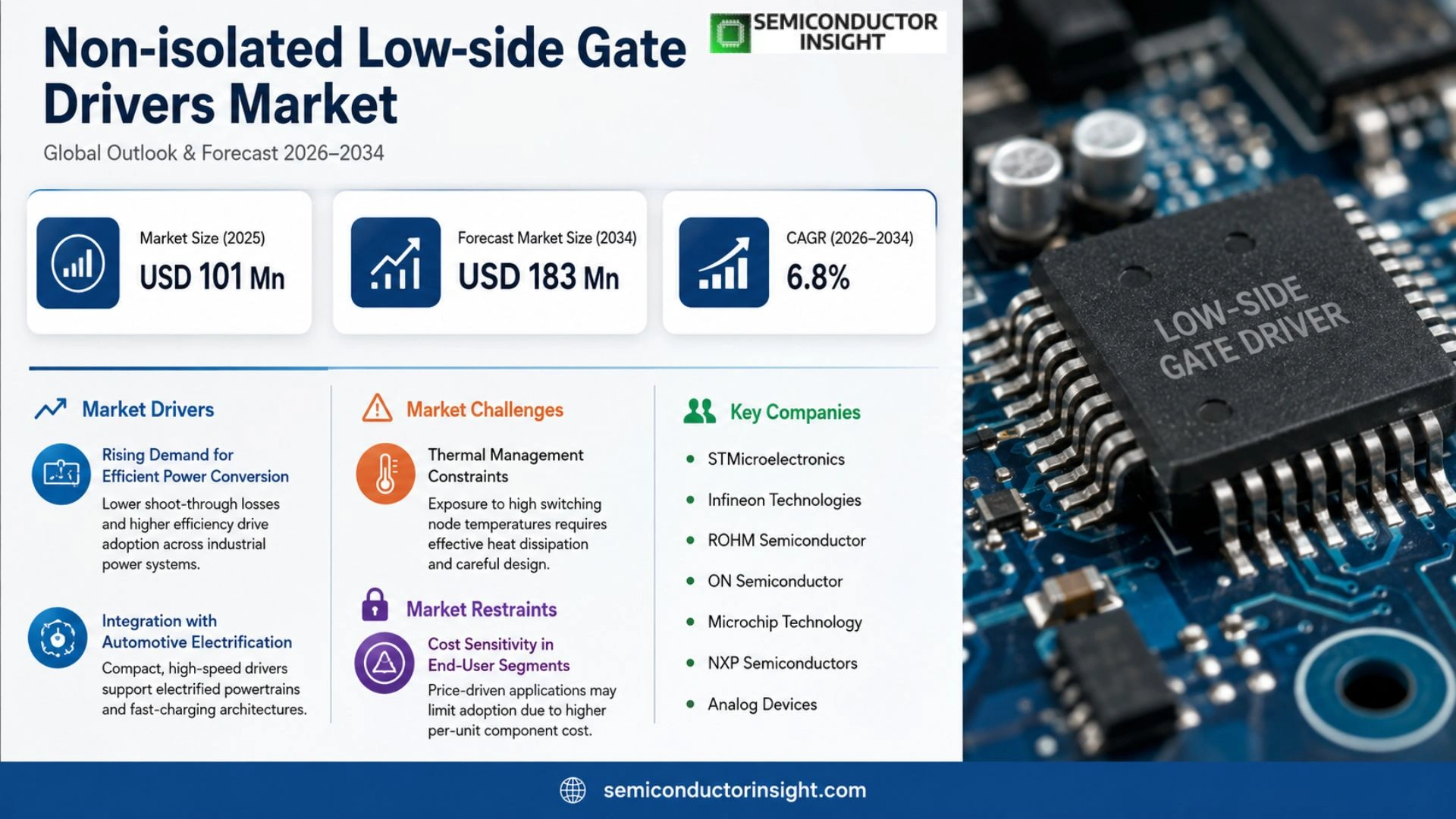

Non-isolated Low-side Gate Drivers market was valued at USD 101 million in 2025. The market is projected to reach USD 183 million by 2034, exhibiting a CAGR of 6.8 % during the forecast period.

Non‑isolated Low‑side Gate Drivers are compact driver ICs that switch low‑side MOSFETs without galvanic isolation. They translate logic‑level commands into fast, high‑current gate pulses while integrating protection features, which improves switching efficiency and reduces system cost in dense power stages. In 2025 production was roughly 79 million units at an average price of USD 1.4 per unit, reflecting strong adoption across consumer electronics, industrial equipment and automotive subsystems.

MARKET DRIVERS

Rising Demand for Efficient Power Conversion

is benefiting from manufacturers’ quest to trim losses in switched‑mode power supplies. By placing the driver on the low‑side switch, designers can achieve lower shoot‑through currents, which translates into measurable energy savings across a broad range of industrial equipment. This efficiency advantage is prompting OEMs to replace legacy bipolar drivers with modern low‑side solutions.

Integration with Automotive Electrification

Automotive power‑train architectures are increasingly relying on high‑frequency gate control to meet emission standards and to support fast‑charging capabilities. Low‑side gate drivers, with their compact footprint and straightforward layout, fit naturally into these designs, enabling manufacturers to meet weight and space constraints without sacrificing performance.

➤ The shift toward silicon‑carbide switching devices amplifies the need for precise low‑side control, positioning the Non‑isolated Low‑side Gate Drivers Market for accelerated adoption.

Consequently, equipment vendors are embedding these drivers into power modules that service everything from robotics to renewable‑energy converters, creating a virtuous cycle that reinforces demand across multiple end‑use sectors.

MARKET CHALLENGES

Thermal Management Constraints

Low‑side gate drivers operate directly on the switching node, exposing them to rapid temperature fluctuations. In high‑current applications, insufficient heat sinking can lead to drift in switching thresholds, forcing engineers to allocate additional board area for thermal mitigation.

Other Challenges

Supply Chain Volatility

Component shortages for MOSFETs and driver ICs have introduced lead‑time uncertainty, compelling system integrators to maintain larger inventories or redesign circuits around alternative part families.

MARKET RESTRAINTS

Cost Sensitivity in End‑User Segments

While low‑side gate drivers offer performance benefits, many price‑driven markets,such as consumer appliances,evaluate total system cost on a per‑unit basis. The incremental premium of a specialized driver can become a barrier when volume discounts are limited.

Moreover, compliance with emerging electromagnetic‑interference (EMI) standards often necessitates additional filtering components, which erodes the cost advantage that low‑side topologies traditionally provide.

MARKET OPPORTUNITIES

Expansion into Renewable Energy Systems

Solar inverters and wind‑turbine converters are migrating toward higher switching frequencies to improve power density. The non‑isolated low‑side driver’s ability to synchronize with advanced PWM schemes makes it a natural fit for these renewable‑energy platforms, opening a sizable growth avenue.

In parallel, the emergence of 48‑V architectures in data‑center power distribution presents an untapped niche. By leveraging low‑side drivers, designers can simplify the gate‑control circuitry while maintaining the fast response required by high‑performance workloads.

Non-isolated Low-side Gate Drivers Market Trends

Cost‑efficiency and Integration Drive Demand

In 2025 the market recorded revenue of $101 million, and the forecast points toward $163 million by 2032, reflecting an average annual expansion of roughly 6.8 percent. The surge is anchored in the relentless push for slimmer power architectures across consumer gadgets, factory automation and vehicle subsystems. Designers favor non‑isolated low‑side drivers because they deliver rapid gate transitions while eliminating the bulk and expense of isolation barriers. That combination translates into lower bill‑of‑materials and tighter thermal budgets, a decisive advantage for portable electronics and compact industrial modules. As system‑on‑chip strategies become mainstream, the ability to embed a proven driver directly adjacent to a low‑side MOSFET shortens board layouts and accelerates time‑to‑market, reinforcing the upward trajectory of the segment.

Other Trends

Supply‑chain Resilience and Material Costs

Production volumes hovered near 79 million units in 2025, yet capacity utilization lingered at 63 percent, indicating spare headroom that can absorb short‑term disruptions. The upstream reliance on silicon wafers and high‑grade substrates from suppliers such as Shin‑Etsu, SUMCO and GlobalWafers has prompted manufacturers to lock in long‑term contracts, thereby dampening price volatility. Gross margins remain healthy at about 55 percent, a testament to disciplined yield management and the economies of scale achieved through standardized driver platforms. Companies that tighten test‑flow efficiency and sustain a stable supply of premium packaging, especially in SOT‑23 and SC70 formats, are better positioned to protect profitability as volumes climb.

Noise Immunity and High‑Frequency Operation

The shift toward higher switching frequencies places greater emphasis on dV/dt robustness and electromagnetic compatibility. Recent design iterations incorporate tighter output stage optimization and enhanced fault‑handling logic, allowing drivers to maintain stable operation even as parasitic inductances shrink. This technical refinement is critical for automotive power‑train modules where regenerative braking and fast‑charge cycles demand swift, noise‑tolerant gating. Likewise, industrial equipment adopting variable‑frequency drives benefits from reduced acoustic emissions and lower heat generation. Vendors that can certify their drivers across a broader voltage envelope,extending beyond the traditional below‑10 V band,unlock new application windows, especially in emerging electric‑vehicle platforms and high‑performance computing power supplies.

COMPETITIVE LANDSCAPE

Key Industry Players

Non‑isolated Low‑side Gate Drivers: Competitive Overview

STMicroelectronics commands the upper tier of the market, leveraging its extensive analog‑power portfolio and deep automotive design experience to secure a dominant share of volume shipments. Its product families integrate high‑speed drive capability with built‑in protection, enabling OEMs to shrink bill‑of‑materials and accelerate time‑to‑market. The overall structure centers on a handful of multinational silicon houses that couple robust design‑for‑manufacturability processes with global supply‑chain reach, while retaining flexibility to tailor variants for high‑frequency consumer devices and rugged industrial controllers. Margins remain healthy because platform standardization reduces engineering overhead and the company exploits economies of scale across its diversified end‑markets. Its recent migration to 28‑nm embedded flash technology has further tightened cost per gate while preserving thermal performance.

Beyond the front‑runner, a constellation of specialized firms competes on differentiated performance attributes. ROHM and Infineon emphasize low‑noise, high‑voltage tolerance for automotive subsystems, whereas ON Semiconductor and NXP focus on compact packaging solutions for mobile and IoT gadgets. Analog Devices and Power Integrations offer ultra‑fast edge rates targeting power‑train converters, while Skyworks and Microchip supply cost‑optimized drivers for mass‑produced consumer electronics. Renesas, IXYS, Diodes Incorporated, and Texas Instruments round out the field, each carving niche positions through application‑specific features such as enhanced dV/dt robustness or proprietary safety functions. Customers such as Apple and Volkswagen have repeatedly selected these alternate suppliers to diversify risk and capture unique feature sets, reinforcing the fragmented yet dynamic nature of the supply ecosystem.

List of Key Non‑isolated Low‑side Gate Drivers Companies Profiled

- STMicroelectronics

- Infineon Technologies

- ROHM Semiconductor

- ON Semiconductor

- Microchip Technology

- NXP Semiconductors

- Analog Devices

- Power Integrations

- Skyworks Solutions

- Renesas Electronics

- IXYS Corporation

- Diodes Incorporated

- Texas Instruments

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Single-Channel

|

| By Application |

|

Consumer Electronics

|

| By End User |

|

Device Manufacturers

|

| By Voltage |

|

10‑20V

|

| By Package |

|

SOT‑23

|

Regional Analysis: Non-isolated Low-side Gate Drivers Market

North America

Major vehicle manufacturers are embedding Non‑isolated Low‑side Gate Drivers into power‑train modules to meet tighter efficiency targets. Their design cycles now prioritize components that can survive high‑temperature environments while delivering lower switching losses, prompting collaborations with semiconductor specialists that can guarantee long‑term reliability.

Factories upgrading to smart‑factory paradigms rely on precise motor control, a domain where low‑side gate drivers excel. The push for smaller footprints on control boards drives demand for integrated solutions that blend high‑speed switching with built‑in protection features.

Portable power supplies and high‑performance chargers increasingly adopt these drivers to improve power density. Designers value the combination of low on‑resistance and fast recovery characteristics, which directly supports longer battery life in emerging devices.

Stringent safety and electromagnetic compatibility rules compel manufacturers to select gate drivers that demonstrate proven compliance. Certification pathways in the United States reinforce a preference for proven silicon platforms, influencing supplier selection across multiple end‑markets.

Europe

European manufacturers are capitalising on a strong commitment to sustainability, which translates into heightened interest in efficient power conversion. Automotive firms in the region, especially those focusing on premium electric models, demand gate drivers that can operate reliably under dense packaging constraints. Meanwhile, the region’s industrial sector benefits from a mature standards ecosystem that encourages early adoption of components meeting the latest IEC guidelines. Suppliers that integrate advanced thermal‑management techniques into their designs find a receptive market, as original equipment manufacturers look to minimise system‑level cooling requirements. The strategic interplay between stringent EU directives and a highly skilled engineering workforce creates a fertile environment for innovation in the Non‑isolated Low‑side Gate Drivers Market.

Asia‑Pacific

Asia‑Pacific exhibits a rapid shift from volume‑driven production to value‑added design, particularly in China, Japan, and South Korea. Local automotive assemblers are scaling electric vehicle line‑ups, prompting a surge in demand for gate drivers that balance cost efficiency with performance. At the same time, the region’s burgeoning renewable‑energy initiatives, such as large‑scale solar inverters, require power‑stage components that can handle fluctuating loads. Companies that can offer design‑for‑manufacturability while maintaining high thermal resilience are gaining traction among contract manufacturers seeking to optimise supply‑chain lead times. The convergence of aggressive government incentives and an expanding pool of engineering talent is reshaping how the market evolves across the region.

South America

In South America, market growth is anchored by incremental adoption of electric mobility in Brazil and Argentina, where governmental policies provide modest subsidies for cleaner transport. Industrial users, especially in mining and agro‑processing, are upgrading legacy motor‑control systems to improve energy efficiency, creating a niche for robust low‑side gate drivers. Suppliers that can navigate fragmented distribution networks and provide localized technical support are securing footholds in this environment. The region’s emphasis on cost‑sensitive solutions, combined with a growing awareness of lifecycle savings, drives a careful selection process that favours proven silicon technology with a clear reliability record.

Middle East & Africa

The Middle East & Africa market is differentiating itself through large‑scale infrastructure projects that demand high‑performance power electronics. In the Gulf Cooperation Council states, data‑center expansions and renewable‑energy farms are prompting system integrators to specify gate drivers that can survive harsh thermal cycles while maintaining efficiency. African nations, meanwhile, are focusing on off‑grid power solutions where compact, low‑loss drivers enable longer battery operation. Vendors that pair robust product portfolios with on‑ground training programs are better positioned to capture contracts, as local engineers seek guidance on integrating these components into diverse applications.

Report Scope

This market research report provides a comprehensive analysis of the Non-isolated Low-side Gate Drivers Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Non-isolated Low-side Gate Drivers Market?

-> Non-isolated Low-side Gate Drivers market was valued at USD 101 million in 2025. The market is projected to reach USD 183 million by 2034

Which key companies operate in Non-isolated Low-side Gate Drivers Market?

-> Key players include STMicroelectronics, Infineon, Rohm Semiconductor, ON Semiconductor, Microchip Technology, Renesas Electronics, NXP Semiconductors, Power Integrations, Skyworks, Analog Devices, IXYS, Diodes, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for cost‑efficient, compact power control in consumer electronics, industrial equipment, and automotive subsystems; migration toward higher switching frequencies; need for fast response and low parasitics; and increased focus on robustness against noise and wider operating margins.

Which region dominates the market?

-> Asia leads the market due to its large consumer electronics manufacturing base, expansive automotive production, and strong industrial equipment sector, while North America and Europe remain significant contributors.

What are the emerging trends?

-> Emerging trends include integration of advanced protection features, optimization for higher dV/dt robustness, noise‑immunity designs, and tighter design‑in cycles that reduce time‑to‑market for new applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...