SiC MOSFET Gate Drivers Market Insights

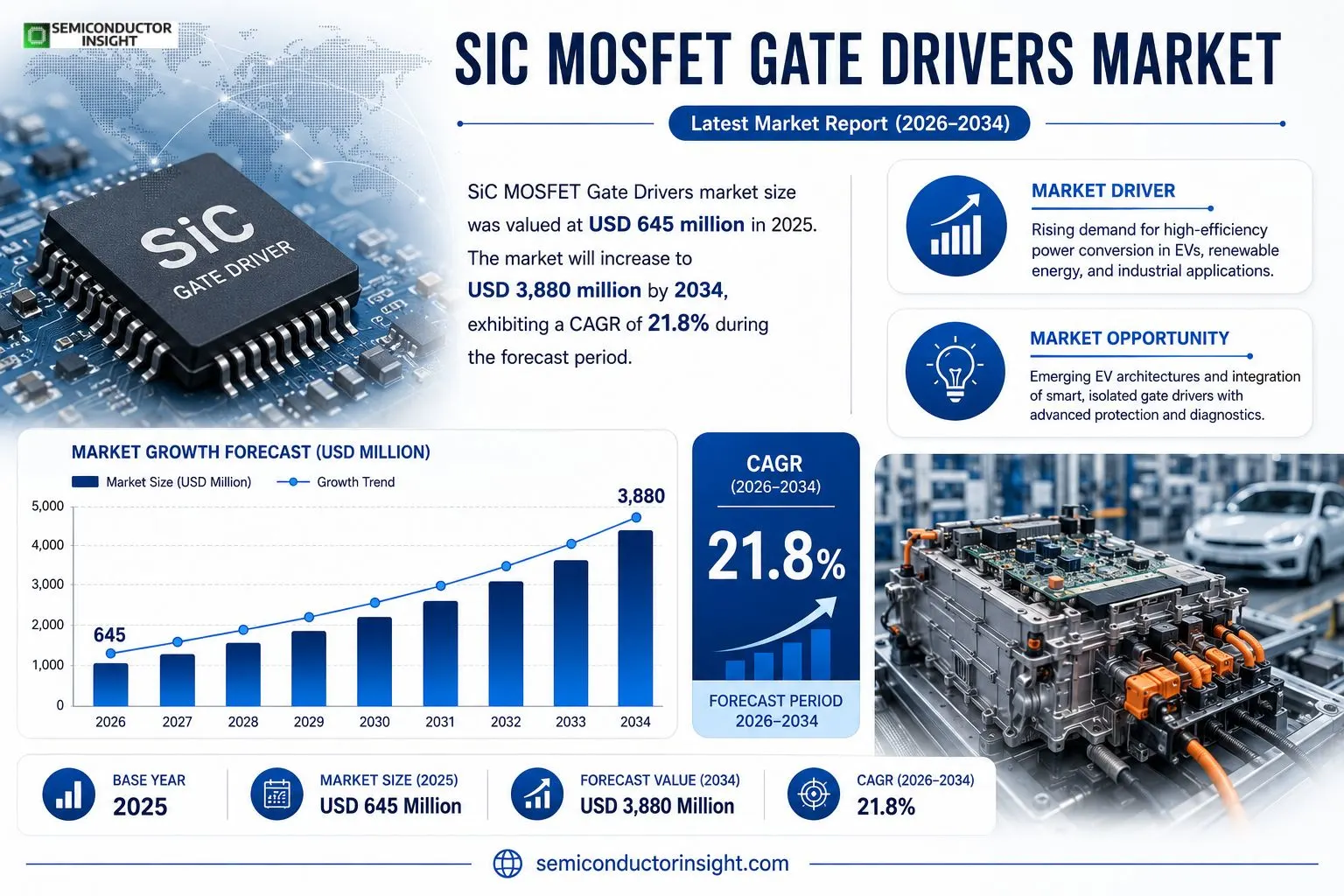

SiC MOSFET Gate Drivers market size was valued at USD 645 million in 2025. The market will increase from USD 3,880 million by 2034, showing a CAGR of 21.8 % during the forecast period.

A SiC MOSFET gate driver converts a low‑power PWM or logic signal into the high‑voltage gate drive required for fast and safe switching of silicon‑carbide MOSFETs. Because SiC devices exhibit much higher dv/dt and di/dt than silicon counterparts, drivers incorporate features such as active Miller clamp, negative gate‑off capability, and strong common‑mode transient immunity.The upstream driver sits between digital controllers (MCU/DSP/FPGA) and the power switch, often requiring isolated bias supplies, gate resistors/RC networks, and protection circuits like desaturation detection. Downstream, these drivers are embedded in EV traction inverters, fast chargers, renewable‑energy converters and industrial drives where efficiency, EMI reduction and reliability are critical.

MARKET DRIVERS

Efficiency Gains in Power Conversion

The superior bandgap of silicon‑carbide enables voltage thresholds well above 3 V, allowing SiC MOSFET Gate Drivers Market participants to design converters that lose less than half the energy of comparable silicon solutions. This efficiency lift translates directly into lower operating costs for data‑center, automotive and rail‑transit customers, prompting OEMs to revise bill‑of‑materials in favor of SiC‑based topologies.

Regulatory Momentum for Low‑Carbon Systems

Stringent emissions standards across Europe, China and the United States force manufacturers to adopt architectures that minimize loss. Because gate‑driver losses dominate the thermal budget in high‑frequency applications, regulators indirectly boost demand for drivers that can switch at 500 kHz while keeping dissipation under 10 mW. Companies that align product roadmaps with these policies gain immediate market traction.

➤ “Every 1 % improvement in converter efficiency can shave up to $200 k from a 2 MW offshore wind inverter over its lifetime.”

This cost‑per‑watt insight has sparked a wave of investment in SiC driver ICs tailored for renewable‑energy converters, where project financiers scrutinize levelized cost of electricity. The ripple effect is evident in the escalating design wins announced by major inverter manufacturers during the last fiscal year.

MARKET CHALLENGES

Thermal Management Constraints

Although SiC devices tolerate higher temperatures, the accompanying gate‑driver circuitry still requires precise thermal control. In high‑density power modules, insufficient heat‑sinking can lead to timing drift, eroding reliability. End‑users therefore demand comprehensive thermal‑simulation tools, adding to development overhead and slowing adoption cycles.

Other Challenges

Supply‑Chain Vulnerabilities

The limited number of fabs capable of producing high‑quality SiC wafers creates a bottleneck. When wafer yields dip, lead times for driver‑compatible silicon‑carbide MOSFETs extend beyond six months, inflating inventory costs and forcing OEMs to retain safety stock, which compresses margins.

MARKET RESTRAINTS

Cost Differential Versus Silicon

The price premium of SiC MOSFETsoften 2–3 × silicon equivalentscascades to gate‑driver solutions, especially when integrated with isolated gate‑driver topologies. For cost‑sensitive segments such as HVAC or consumer‑grade power supplies, the incremental expense outweighs perceived efficiency benefits, limiting market penetration in volume‑driven categories.

MARKET OPPORTUNITIES

Emerging EV Power‑train Architectures

Next‑generation electric‑vehicle platforms are migrating from 48 V to 800 V systems to reduce conductor mass. This voltage jump necessitates driver architectures that can handle fast turn‑on/turn‑off transients without sacrificing isolation. Firms that bundle SiC MOSFET gate drivers with advanced digital control loops are positioned to capture a sizable share of the upcoming EV power‑train redesign wave.

SiC MOSFET Gate Drivers Market Trends

Elevated Switching Demands Redefine Driver Architecture

The migration toward SiC power devices forces engineers to treat the gate‑driver as a performance‑critical block rather than a simple switch. Because SiC MOSFETs exhibit markedly higher dv/dt and di/dt, drivers now embed active Miller‑clamp circuits, negative gate‑off capability, and hardened common‑mode rejection. These functions suppress parasitic turn‑on and limit voltage overshoot, directly translating into higher inverter efficiency and lower electromagnetic interference. In automotive traction inverters and fast‑charge stations, the tighter control loop reduces thermal stress on the switch and extends system service life.

Other Trends

Design Architecture Shifts

Manufacturers are consolidating discrete bias supplies, isolation stages, and protection networks into single‑chip or system‑in‑package solutions. The trend reflects customer pressure for reduced board area, simplified layout, and accelerated time‑to‑market. Integrated temperature and current sensors enable real‑time diagnostics, while digital interfaces allow firmware‑based fault‑handling strategies. This evolution supports a co‑design model where the driver is embedded within SiC power modules, fostering a tighter supply chain and longer design cycles that favor vendors offering comprehensive reference designs.

Pricing Dynamics and Premium Segmentation

Average selling price hovers around US$128 per unit, yet gross margins range widely from 20 % to 40 % across the supplier base. Volume‑driven, low‑cost drivers face downward pressure as SiC adoption matures, but segments that combine reinforced isolation, on‑chip sensing, and full automotive qualification retain pricing power. Procurement teams increasingly require multi‑sourcing and regional production, which reshapes market share and incentivizes suppliers to guarantee supply continuity through localized fabs.The confluence of higher switching ambition, integrated functionality, and nuanced pricing creates a competitive landscape where differentiation hinges on isolation robustness, transient immunity, and depth of application support. Companies that can bundle validated protection chains with detailed EMI‑thermal guidelines are likely to capture design‑win opportunities in EV traction, renewable‑energy converters, and high‑end industrial drives. The observed trends suggest that the SiC MOSFET Gate Drivers Market will continue to reward technical depth and ecosystem alignment over pure cost leadership.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive Landscape of SiC MOSFET Gate Drivers Market

Infineon Technologies dominates the SiC MOSFET gate‑driver arena, leveraging a portfolio that blends isolated driver ICs with extensive automotive qualification kits. Its capacity to deliver high‑CMTI isolation, active Miller‑clamp logic, and integrated temperature sensing has translated into a sizable share of the $645 million market recorded in 2025. The company’s close ties with silicon‑carbide wafer suppliers enable a stable supply chain, a factor that many OEMs cite when selecting a primary driver source. Beyond Infineon, the top‑five vendors collectively account for roughly sixty percent of revenue, a concentration that reinforces the importance of long‑term foundry partnerships and robust design‑win support programs.Other manufacturers carve out relevance through specialized architectures or regional focus. STMicroelectronics and onsemi provide cost‑effective non‑isolated families while still meeting automotive safety standards, whereas Wolfspeed’s heritage in SiC substrates drives a premium line of galvanically isolated drivers with ultra‑fast fault response. ROHM and Power Integrations differentiate themselves by embedding current‑monitoring loops directly in the driver silicon. NXP, Microchip Technology, Texas Instruments, and Skyworks broaden the ecosystem with mixed‑signal interfaces and software‑defined protection schemes. Analog Devices and Renesas further diversify the market by offering drivers that integrate digital signal processing for adaptive switching, while Mitsubishi Electric and Fujitsu target high‑power industrial converters with rugged packaging and extended temperature ranges.

List of Key SiC MOSFET Gate Drivers Companies Profiled

- Infineon Technologies

- STMicroelectronics

- onsemi

- Wolfspeed

- ROHM Semiconductor

- Power Integrations

- NXP Semiconductors

- Microchip Technology

- Texas Instruments

- Skyworks Solutions

- Analog Devices

- Renesas Electronics

- Mitsubishi Electric

- Fujitsu

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Isolation‑Centric Segment

|

| By Application |

|

Automotive‑Driven Segment

|

| By End User |

|

OEM‑Centric Segment

|

| By Gate Bias Scheme |

|

Active‑Control Segment

|

| By Channel |

|

Multi‑Channel Segment

|

Regional Analysis: SiC MOSFET Gate Drivers Market

North America

OEMs in the United States are embedding SiC gate drivers into next‑generation inverters, seeking to shrink thermal envelopes while boosting efficiency. The shift reflects a strategic response to evolving fuel‑economy regulations.

Canadian manufacturers targeting high‑power motor applications value the robustness of SiC drivers, especially where duty cycles demand rapid switching and reduced losses.

Recent mergers among semiconductor firms have streamlined component sourcing, giving North American assemblers better control over lead times and design iterations.

Federal grants directed at high‑efficiency power electronics nurture innovation pipelines, encouraging early‑stage ventures to specialize in SiC gate driver architectures.

Europe

European automakers are accelerating the adoption of silicon‑carbide gate drivers to meet the European Union’s stringent CO₂ targets. German and French manufacturers are integrating these components into both passenger‑car and commercial‑vehicle platforms, emphasizing compactness and thermal resilience. Simultaneously, the region’s industrial sectorparticularly in wind‑turbine converters and rail tractionleverages the high‑frequency capability of SiC drivers to improve system density. Policy incentives, such as the EU’s Green Deal funding, create a favorable environment for joint ventures between local chip designers and vehicle engineers. These dynamics collectively position Europe as a fast‑moving follower that translates North American advances into market‑specific solutions, especially where regulatory compliance drives engineering choices.

Asia‑Pacific

In Asia‑Pacific, China’s aggressive rollout of electric buses and renewable‑energy‑linked grids fuels demand for SiC MOSFET gate drivers that can tolerate elevated junction temperatures. Japanese firms, long‑standing leaders in power electronics, are tailoring driver topologies to suit high‑speed rail applications, where efficiency translates directly into operational cost savings. South Korean manufacturers are channeling investments into fab capacity upgrades, seeking to capture a share of the expanding automotive market. The region’s diverse regulatory landscape prompts varied adoption rates, but a clear trend emerges: manufacturers are prioritizing semiconductor solutions that enable tighter integration and lower system weight, aligning with broader electrification goals across the Pacific basin.

South America

South American markets, while smaller in absolute volume, are witnessing a strategic shift as utility providers modernize distribution networks. Nations such as Brazil and Chile are experimenting with SiC‑based inverter modules for solar farms, where the gate driver’s ability to operate at higher switching frequencies reduces inverter size and improves land utilisation. Automotive imports increasingly feature SiC‑enabled powertrains, especially in premium segments, prompting local assemblers to retrofit existing platforms. Although fiscal constraints temper rapid expansion, the region’s focus on cost‑effective efficiency gains makes the technology appealing for both grid and mobility applications.

Middle East & Africa

The Middle East’s investment in large‑scale solar projects creates a niche for SiC MOSFET gate drivers that can handle the high thermal loads typical of desert environments. Emirates‑based power‑generation firms prioritize components with robust voltage tolerance to ensure reliability under intense irradiance. In Africa, emerging economies are exploring off‑grid renewable solutions, where compact, high‑efficiency drivers enable rapid deployment of micro‑grids. While overall market depth remains modest, the convergence of renewable‑energy ambitions and a growing appetite for energy‑efficient industrial equipment positions the region as a fertile ground for early adopters seeking performance advantages over traditional silicon solutions.

Report Scope

This market research report provides a comprehensive analysis of the SiC MOSFET Gate Drivers Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of SiC MOSFET Gate Drivers Market?

-> SiC MOSFET Gate Drivers Market was valued at USD 645 million in 2025 and is expected to reach USD 2612 million by 2032, growing at a CAGR of 21.7% during the forecast period.

Which key companies operate in SiC MOSFET Gate Drivers Market?

-> Key players include Infineon, STMicroelectronics, onsemi, Wolfspeed, ROHM, Power Integrations, NXP, Microchip Technology, Texas Instruments, Skyworks, among others.

What are the key growth drivers?

-> Key growth drivers include the transition to higher efficiency and power density in power electronics, rapid EV adoption, expanding renewable‑energy inverter deployments, and the need for fast, reliable switching in industrial drives.

Which region dominates the market?

-> Asia‑Pacific shows the strongest growth momentum, driven by robust automotive EV production and industrial automation demand, while North America and Europe also represent significant markets.

What are the emerging trends?

-> Emerging trends include system‑oriented drivers integrating isolated power, current/temperature sensing, digital interfaces, active Miller clamp, and soft‑shutdown strategies, as well as increased focus on functional‑safety qualification and multi‑sourcing strategies.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...