Dynamic Random-access Memory (DRAM) ICs Market Insights

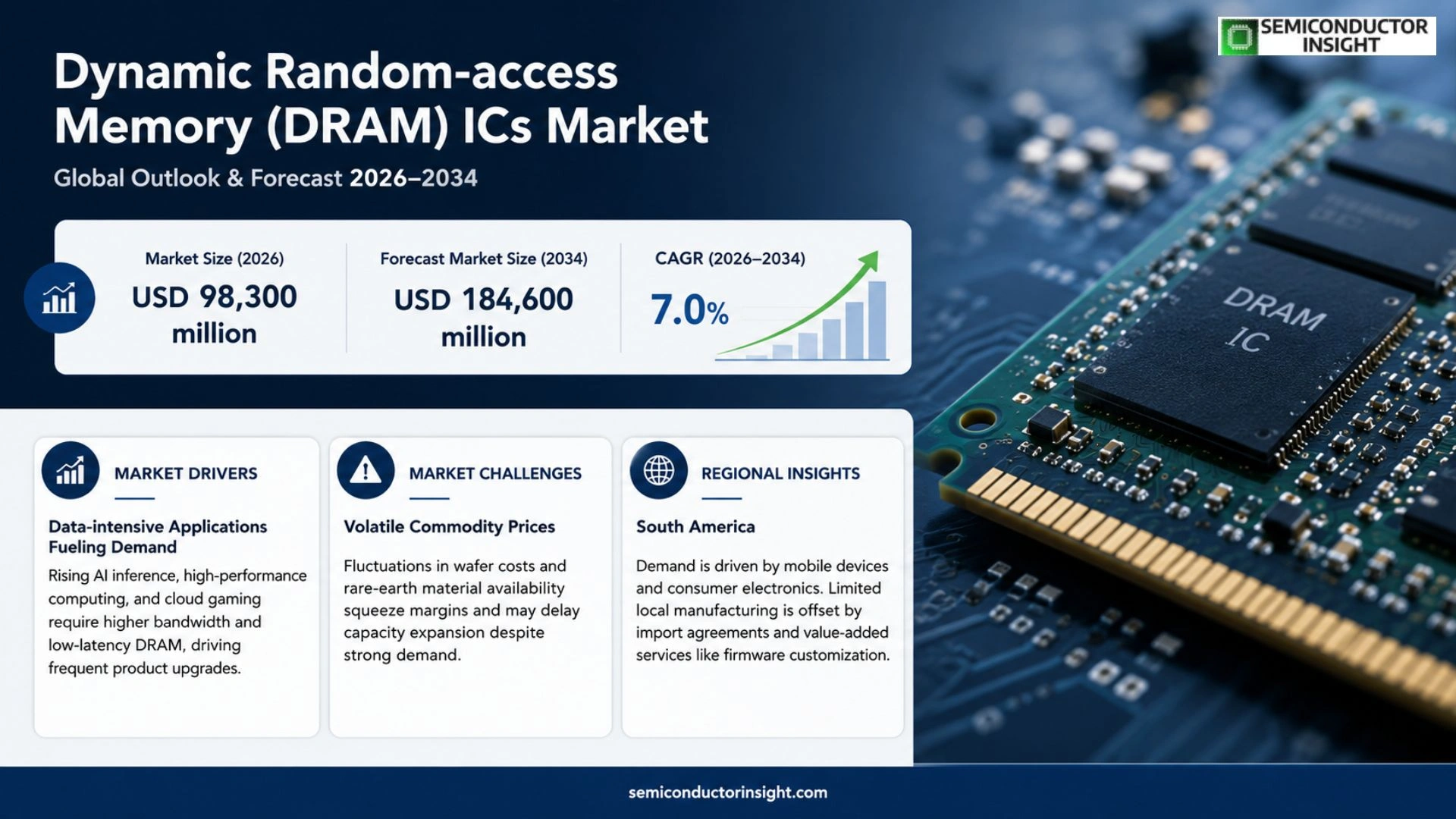

Global Dynamic Random-access Memory (DRAM) ICs market is projected to grow from USD 100,450 million in 2025 to USD 184,600 million by 2034, exhibiting a CAGR of approximately 7.0% during the forecast period.

Dynamic Random‑access Memory (DRAM) ICs are volatile semiconductor memory devices that store data as electrical charges within capacitors and require periodic refreshing to retain information integrity. Their hallmark attributes,high access speed, low cost per bit, and high integration density,make DRAM the primary system memory across personal computers, servers, data‑center platforms, smartphones, automotive electronics and artificial‑intelligence workloads. Architecturally DRAM comprises cell arrays, sense amplifiers, row‑and‑column decoders and control circuitry; performance is measured by capacity, process‑technology node, operating frequency, power consumption and bandwidth. Depending on application demands DRAM products are offered as DDR, LPDDR, GDDR or High‑Bandwidth Memory (HBM) variants.

MARKET DRIVERS

Data‑intensive Applications Fueling Demand

The surge in artificial‑intelligence inference, high‑performance computing, and cloud gaming has pushed server manufacturers to prioritize higher bandwidth memory. Latency‑critical workloads now require DRAM modules that can sustain multi‑gigabyte per second transfers, prompting OEMs to refresh product lines more frequently than in the past.

Cost‑per‑Bit Decline Enhances Viability

Advances in lithography and wafer‑scale integration have trimmed the cost‑per‑bit of DRAM chips to historic lows. This reduction allows device makers to embed larger memory footprints without eroding profit margins, thereby expanding the addressable market across consumer electronics and automotive infotainment. Economies of scale are now a tangible lever for price‑sensitive segments.

➤ Manufacturers that can accelerate time‑to‑market for next‑gen DDR5 and LPDDR5X will capture the bulk of incremental spend.

In parallel, the rollout of 5G infrastructure demands edge‑computing nodes with sufficient on‑board memory to process streaming data locally. The convergence of these forces creates a self‑reinforcing loop where capacity upgrades beget new use‑cases, further stimulating Dynamic Random-access Memory (DRAM) ICs Market.

MARKET CHALLENGES

Volatile Commodity Prices

The semiconductor supply chain remains sensitive to fluctuations in silicon wafer costs and rare‑earth material availability. When raw‑material prices spike, manufacturers face squeezed margins, compelling some to defer capacity expansions despite strong demand signals.

Other Challenges

Yield Variability in Advanced Nodes

Transitioning to sub‑20 nm process technologies has introduced higher defect densities, which can impair yield rates. Lower yields translate into higher per‑unit costs and can delay the introduction of higher‑density DRAM products.

MARKET RESTRAINTS

Regulatory and Trade Pressures

Tightening export controls on high‑performance memory chips in certain jurisdictions restrict cross‑border sales, limiting the ability of manufacturers to serve global OEMs from a single production hub. Companies must now navigate a patchwork of licensing regimes, which adds compliance overhead and operational friction.

Furthermore, growing environmental scrutiny around semiconductor fabrication,particularly concerning water usage and chemical waste,has prompted stricter permitting processes. Sustainability mandates can extend project timelines and increase capex, thereby dampening short‑term capacity additions.

MARKET OPPORTUNITIES

Emerging Form‑Factors for Edge AI

Edge AI devices, ranging from autonomous drones to smart sensors, require compact memory solutions that balance power efficiency with performance. The development of stacked‑die DRAM and on‑package memory architectures opens a niche where suppliers can command premium pricing while addressing space constraints.

Additionally, the automotive sector’s shift toward advanced driver‑assistance systems (ADAS) and in‑vehicle infotainment creates demand for memory that can operate reliably across a wide temperature envelope. Automotive‑grade DRAM offerings, certified for extended reliability, represent a growth corridor that remains under‑penetrated.

Finally, strategic partnerships between memory fabs and foundries specializing in heterogeneous integration are fostering new product roadmaps that blend DRAM with logic dies. Such co‑design initiatives could unlock system‑level efficiencies, positioning early adopters to outpace competitors in performance‑critical markets.

Dynamic Random-access Memory (DRAM) ICs Market Trends

AI and Cloud Computing Demands Elevate DRAM Bandwidth Requirements

The surge in artificial‑intelligence workloads and the scaling of cloud infrastructures have reshaped the demand profile for volatile memory. Data‑center operators now prioritize latency‑critical, high‑bandwidth modules to sustain real‑time inference and large‑scale model training. Consequently, memory suppliers have accelerated the transition from legacy DDR generations to newer standards that deliver double‑digit frequency improvements while retaining cost efficiency. This shift raises the bar for silicon process nodes and encourages system architects to redesign server boards around wider memory channels, unlocking performance margins previously unattainable with older parts. In parallel, high‑performance computing clusters that support scientific simulations are leveraging the same high‑frequency DRAM to reduce memory bottlenecks, further amplifying pressure on the supply chain.

Other Trends

Supply‑Chain Concentration and Geopolitical Exposure

Production of DRAM remains clustered in a handful of facilities located in East Asia. When geopolitical friction or natural events disrupt those fabs, the global inventory buffer contracts sharply, prompting price volatility that ripples through downstream manufacturers. Buyers in automotive and industrial sectors, which rely on predictable component pricing for long‑term product planning, are compelled to adopt multi‑sourcing strategies or secure forward contracts. Raw silicon wafer availability, which experiences periodic shortfalls, adds another layer of cost pressure, prompting manufacturers to optimize yield through advanced test and binning methods. At the same time, the capital intensity of advanced lithography limits the entry of new players, reinforcing the dominance of incumbent fabs and heightening the sector’s sensitivity to external shocks.

Emergence of Low‑Power Mobile DRAM Variants

Within Dynamic Random-access Memory (DRAM) ICs Market, the rise of 5G‑enabled handsets and immersive extended‑reality experiences has spurred demand for memory that balances speed with power restraint. LPDDR families respond by integrating adaptive voltage scaling and on‑die error correction, extending battery life without sacrificing throughput. This parallel growth path sees handset OEMs adopt higher‑density packages while system‑level designers embed these parts into wearables and edge gateways. In autonomous‑vehicle platforms, the need for deterministic memory access drives adoption of specialized DRAM with error‑detecting capabilities, nudging the market toward tighter integration with safety‑critical processors. The simultaneous pursuit of higher bandwidth and lower energy draws investment toward process refinements that shrink cell capacitance, a trend likely to influence future server‑grade modules as well.

COMPETITIVE LANDSCAPE

Key Industry Players

Dynamic Random-access Memory (DRAM) ICs Market – Competitive Overview

Samsung Electronics remains the dominant force in the DRAM arena, leveraging its advanced 4‑nanometer process line to supply high‑density DDR5 and HBM solutions for data‑center servers and AI accelerators. The company’s vertical integration,from wafer fabrication to final testing,affords it pricing flexibility and rapid response to capacity spikes, reinforcing its leadership in both volume and premium segments. SK Hynix follows closely, differentiating itself through aggressive scaling of stacked‑die technologies and a robust portfolio that includes LPDDR5X for mobile platforms. Micron Technology complements the Korean duopoly by focusing on specialty parts such as GDDR7 for graphics and bespoke automotive memory, thereby carving out niche revenue streams while maintaining a solid share of the broader DRAM market.

Beyond the three giants, a cohort of smaller yet technically sophisticated firms sustains the ecosystem. Taiwan‑based Powerchip and Nanya continue to invest in mature‑node fabs that serve cost‑sensitive PC and consumer‑electronics segments. Winbond and ISSI specialize in low‑power LPDDR and automotive‑grade parts, catering to the expanding IoT and vehicle‑infotainment markets. Chinese entrants such as ChangXin Memory Technologies and GigaDevice are accelerating their roadmap to challenge incumbents in the mid‑range DDR market, while Alliance Memory and Etron focus on niche industrial and edge‑computing applications. This layered competitive structure creates a dynamic where scale, technology leadership, and application‑specific expertise each generate distinct strategic advantages.

List of Key DRAM Companies Profiled

- Samsung Electronics Co., Ltd.

- SK Hynix Inc.

- Micron Technology, Inc.

- Nanya Technology Corporation

- Winbond Electronics Corporation

- Powerchip Technology Corporation

- GigaDevice Semiconductor Inc.

- ChangXin Memory Technologies Co., Ltd.

- Alliance Memory, Inc.

- Integrated Silicon Solution Inc. (ISSI)

- Etron Technology, Inc.

- Kingston Technology Company

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

DDR remains the foundational memory architecture for a broad range of computing platforms.

|

| By Application |

|

Data Centers & Cloud Computing drives the most strategic demand for DRAM.

|

| By End User |

|

Enterprise Servers are emerging as the dominant end‑user for advanced DRAM solutions.

|

| By Process Technology |

|

Advanced Process Node shapes competitive advantage for leading manufacturers.

|

| By Performance Tier |

|

High‑Bandwidth Tier is critical for graphics‑intensive and AI training platforms.

|

Regional Analysis: Dynamic Random-access Memory (DRAM) ICs Market

Asia‑Pacific

Fab consolidation continues as owners rationalize capacity to balance yield improvement with capital efficiency. Tier‑1 fabs prioritize triple‑patterned lithography for 1z‑class DRAM, while emerging players explore 300‑mm platforms to lower per‑die cost. This shift influences procurement strategies for OEMs that now assess facility reliability alongside raw‑material sourcing.

Recent geopolitical frictions have prompted a modest re‑shoring of critical substrate suppliers. Companies diversify logistics routes, integrating maritime and overland corridors to safeguard inventory buffers for high‑growth segments such as 5G‑enabled devices.

Major manufacturers deepen alliances with design‑house consortia, offering early‑access silicon to secure silicon‑first customers. Simultaneously, niche firms leverage specialty process extensions,low‑voltage and extreme‑temperature variants,to capture niche industrial IoT markets.

The rise of on‑device AI accelerators drives demand for high‑bandwidth, low‑latency DRAM modules. Automotive manufacturers also experiment with DRAM‑backed infotainment clusters, prompting suppliers to certify products against automotive reliability standards.

North America

North America remains a significant consumer of DRAM ICs, with demand shaped by cloud service providers and semiconductor‑design firms headquartered in the United States. The region’s emphasis on security‑focused architectures pushes vendors to offer memory solutions featuring built‑in encryption and error‑correction capabilities. Concurrently, the presence of advanced test and validation facilities enables quicker iteration cycles, granting American customers an edge in time‑sensitive product launches. Policy incentives targeting domestic fab expansion, though modest compared with Asia‑Pacific, signal a strategic desire to retain a portion of the value chain within the continent.

Europe

Europe’s DRAM market dynamics are driven by its strong automotive and industrial automation sectors. OEMs require memory that can operate reliably across wide temperature ranges, prompting suppliers to adapt their process controls for extended‑life parts. The European Union’s sustainability agenda also nudges manufacturers toward greener production methods, influencing material selection and waste‑management practices. Collaborative research programs between academia and industry foster breakthroughs in low‑power DRAM, aligning with the region’s push for energy‑efficient computing.

South America

South America’s consumption pattern is anchored in consumer electronics, particularly mobile devices that serve as primary connectivity tools. While the region lacks large‑scale fabrication capacity, it benefits from strategic import agreements that lower tariff burdens on memory modules. Local distributors focus on value‑added services, such as firmware customization for region‑specific market needs, thereby creating modest differentiation in a price‑sensitive landscape.

Middle East & Africa

In the Middle East & Africa, growth is linked to expanding data‑center footprints and increasing adoption of smart‑city initiatives. Governments are investing in digital infrastructure, prompting enterprises to upgrade server memory to sustain higher workloads. The market is still nascent, but the combination of rising broadband penetration and public‑sector digitization projects suggests a gradual escalation in DRAM procurement, especially for enterprise‑grade solutions.

Report Scope

This market research report provides a comprehensive analysis of the Dynamic Random-access Memory (DRAM) ICs Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Dynamic Random-access Memory (DRAM) ICs Market?

-> Dynamic Random-access Memory (DRAM) ICs market is projected to grow from USD 184,600 million by 2034

Which key companies operate in Dynamic Random-access Memory (DRAM) ICs Market?

-> Key players include Samsung Electronics Co., Ltd., SK Hynix Inc., Micron Technology, Inc., Nanya Technology Corporation, Winbond Electronics Corporation, Powerchip Technology Corporation, GigaDevice Semiconductor Inc., ChangXin Memory Technologies Co., Ltd., Alliance Memory, Inc., Integrated Silicon Solution Inc. (ISSI), and Etron Technology, Inc.

What are the key growth drivers?

-> Key growth drivers include rapid expansion of cloud computing, artificial intelligence, high‑performance computing, edge and 5G deployments, increasing data‑center capacity, and growing automotive electronics demand.

Which region dominates the market?

-> Asia dominates the DRAM IC market, driven by major manufacturing hubs in South Korea and Taiwan, followed by strong demand from China’s data‑center and consumer‑electronics sectors.

What are the emerging trends?

-> Emerging trends include adoption of high‑bandwidth memory (HBM), migration to DDR5 and LPDDR5, increased use of stacked and hybrid DRAM architectures, and growing integration of DRAM in AI‑enabled edge devices and autonomous vehicles.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...