Smart High-Side Switch Controller Market Insights

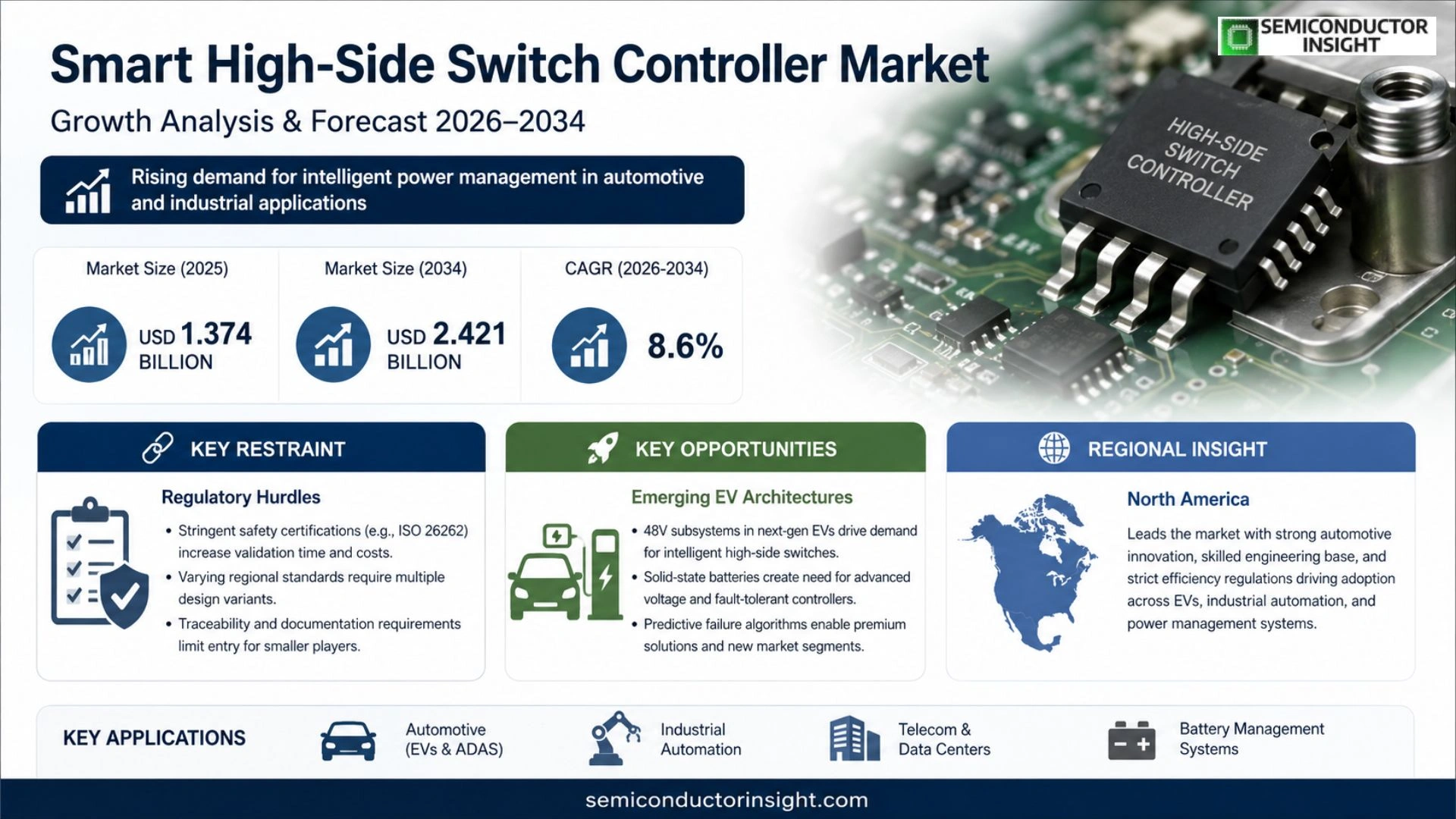

Global Smart High-Side Switch Controller market size was valued at USD 1.374 billion in 2025 and is forecasted to reach USD 2.421 billion by 2034, showing a CAGR of 8.6 % during the forecast period.

The device integrates high‑side load switching, protection functions and on‑chip diagnostics, enabling safer power distribution in passenger and commercial vehicles. In 2025 production reached roughly 295 million units with an average selling price of USD 5.1. Capacity utilization stood at about 68 % and gross margins averaged 40 %, reflecting value creation through functional integration and reduced external components.

Growth is fueled by the shift toward centralized electric architectures, where OEMs seek controllers that cut wiring complexity while improving fault isolation. While price pressure persists on high‑volume platforms, manufacturers that deliver scalable families and reuse qualified designs are better positioned to preserve profitability.

MARKET DRIVERS

Integration with Automotive Powertrains

The shift toward electrified propulsion systems has created a genuine need for precise high‑side switching solutions. Engineers now favor devices that can mitigate voltage spikes while providing real‑time diagnostics, a combination that directly benefits Smart High-Side Switch Controller Market. This alignment lowers failure rates in traction inverters and improves overall vehicle reliability.

Demand for Energy‑Efficient Designs

Regulatory pressure on fuel consumption forces OEMs to adopt components that minimize conduction losses. Modern controllers integrate synchronous rectification and adaptive gating, which translates into measurable improvements in battery endurance. Companies that embed these features can command premium pricing, reinforcing market momentum.

➤ “When a controller can adapt its switching profile on‑the‑fly, system architects gain both efficiency and safety, a dual advantage that fuels adoption across multiple vehicle platforms.”

Beyond automotive, industrial automation systems are embracing modular power architectures that rely on intelligent high‑side switches. The resulting flexibility shortens product development cycles and enables quick reconfiguration, further amplifying demand for sophisticated control ICs.

MARKET CHALLENGES

Technical Complexity

Designers must balance high voltage tolerance with tight thermal budgets, a trade‑off that often requires multi‑disciplinary expertise. The steep learning curve slows time‑to‑market for smaller suppliers, limiting their ability to compete with established players.

Other Challenges

Supply Chain Constraints

The semiconductor shortage continues to affect wafer allocations for niche power devices. Manufacturers experience longer lead times, which erodes flexibility and can force end users to postpone or down‑size projects.

MARKET RESTRAINTS

Regulatory Hurdles

Stringent safety certifications, such as ISO 26262 for automotive, impose additional validation steps. The cost and duration of compliance testing can deter new entrants and slow product refresh cycles.

Furthermore, differing regional emission standards compel manufacturers to maintain multiple design variants. This fragmentation raises engineering overhead and dilutes economies of scale.

Finally, the need for documented traceability in safety‑critical applications adds paperwork that many small firms find burdensome, limiting the pool of viable suppliers.

MARKET OPPORTUNITIES

Emerging EV Architectures

Next‑generation electric vehicles are embracing 48‑volt subsystems for auxiliary loads. This architecture relies heavily on intelligent high‑side switches to manage power distribution without incurring excessive weight. Manufacturers that tailor controllers for this voltage tier stand to capture a growing slice of the automotive sector.

In parallel, the rise of solid‑state battery packs introduces new voltage and fault‑tolerance requirements. Controllers equipped with predictive failure algorithms can differentiate themselves, opening premium market segments.

Industrial IoT deployments are also expanding, with edge devices demanding compact, low‑power switching solutions. Smart controllers that integrate communication protocols provide a seamless bridge between power management and data analytics, representing a fertile ground for differentiated products.

Smart High-Side Switch Controller Market Trends

Consolidation of Vehicle Power Architecture

In 2025 the segment generated roughly US$1.37 billion, and the trajectory points to about US$2.42 billion by 2032. The rise is not merely a function of volume – production topped 295 million units in 2025 – but reflects a shift toward centralized, software‑defined power distribution in both passenger and commercial vehicle platforms. OEMs are replacing scattered relays with an integrated controller that couples load switching, protection and on‑chip diagnostics. This configuration trims wiring harnesses, curtails validation cycles and improves fault isolation, delivering measurable cost savings that justify the higher unit price of US$5.1. As platforms mature, the same silicon family can be redeployed across multiple models, spreading qualification expense and reinforcing margins that hover near 40 %.

Other Trends

Supply‑Chain Maturation

Upstream inputs such as silicon wafers, photoresists and epoxy molding compounds are now sourced from a stable set of suppliers,including Shin‑Etsu, JSR and Shanghai Silicon Industry Group,allowing manufacturers to sustain a 68 % capacity utilization rate. The predictability of raw‑material quality reduces yield loss, which in turn supports the profitability of firms that can bundle integration benefits with consistent production yields.

Platform‑Level Design Standardization

Midstream engineers are aligning controller architectures with emerging automotive software standards, enabling a plug‑and‑play approach across different vehicle families. Standardized diagnostic APIs and unified PWM or SPI interfaces simplify firmware updates and reduce the engineering overhead required for each new platform. For tier‑one suppliers, this harmony accelerates time‑to‑market and permits volume‑driven cost reductions without sacrificing the advanced protection features that end‑users demand.

Diagnostic‑Heavy Value Proposition

Design teams are concentrating on embedding current‑sensing and self‑diagnostic blocks directly into the controller die. These features enable on‑vehicle fault detection without external components, cutting down on field failures and warranty costs. For customers such as BYD, Toyota and Volkswagen, the ability to view real‑time health metrics from a single IC translates into shorter service windows and higher vehicle uptime,an advantage that increasingly influences procurement decisions in a price‑sensitive market.

COMPETITIVE LANDSCAPE

Key Industry Players

Smart High‑Side Switch Controller Market: Competitive Landscape Overview

The segment is heavily front‑loaded by a handful of silicon power specialists whose portfolio breadth lets them address both 12 V and 24 V automotive architectures. Infineon leads the conversation with a family of integrated high‑side switches that couple load control, fault detection and diagnostic telemetry, a combination that has become a prerequisite for new vehicle electrical‑architecture strategies. STMicroelectronics follows closely, leveraging its automotive‑grade qualification framework to offer scalable devices that can be reused across multiple programs, thereby amortising development costs for OEMs. Texas Instruments differentiates through a strong analog‑to‑digital bridge, embedding precise current‑sense amplifiers that improve fault isolation without inflating BOM size. The market structure reflects a classic “top‑down” dynamic: a few global players secure the high‑volume platform contracts, while niche innovators chase differentiated features such as ultra‑low on‑resistance or advanced PWM interfaces. This hierarchy shapes pricing pressure, forcing all participants to compress margins through higher functional integration and platform‑wide reuse.

Beyond the tier‑one firms, a coalition of midsize and specialist companies is carving out valuable space in specific niches. ROHM focuses on compact, dual‑channel parts that appeal to electric‑bus manufacturers seeking reduced wiring complexity. Renesas capitalises on its strong relationship with Japanese OEMs, offering a differentiated SiC‑compatible switch line for next‑generation power‑train modules. Diodes Incorporated and Fuji Electric target industrial‑automation customers, emphasising robust thermal performance for harsh environments. onsemi and Microchip Technology lean on extensive automotive‑grade libraries to provide quick‑start reference designs that cut validation time. Toshiba, Analog Devices and NXP Semiconductors each bring unique IP – ranging from built‑in safety‑monitoring to SPI‑centric control schemes – that enables system architects to tailor solutions without extensive redesign. Their collective emphasis on application‑specific optimisation adds depth to the supply base, fostering competition that drives innovation and ultimately benefits end‑users through lower system‑integration costs.

List of Key Smart High‑Side Switch Controller Companies Profiled

- Infineon Technologies

- STMicroelectronics

- Texas Instruments

- NXP Semiconductors

- ROHM Semiconductor

- Renesas Electronics

- Diodes Incorporated

- Fuji Electric

- onsemi

- Microchip Technology

- Toshiba Electronic Devices & Storage

- Analog Devices

- Cypress Semiconductor

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

12V Controller is emerging as the leading type because it aligns well with the majority of vehicle architectures that continue to rely on lower voltage domains for auxiliary loads. – Integrators value the reduced component count that a single‑chip solution offers, simplifying board layouts and enhancing reliability. – The built‑in diagnostic functions enable early fault detection, supporting maintenance strategies that minimize vehicle downtime. – Designers appreciate the flexibility to embed protection features without additional external parts, which accelerates development cycles. |

| By Application |

|

Automotive dominates the application landscape as manufacturers pursue centralized power distribution strategies. – The combination of load switching, protection, and on‑chip diagnostics addresses the growing demand for safer, more observable electrical systems in both passenger and commercial vehicles. – Integrated controllers reduce wiring harness complexity, contributing to weight savings and improved fuel efficiency. – Software‑defined functionality enables over‑the‑air updates, aligning with the broader trend toward vehicle electrification and connectivity. |

| By End User |

|

Passenger Vehicles are the primary end‑user segment where the quest for compact, reliable power management drives adoption. – Automakers prioritize devices that can be reused across multiple vehicle platforms, spreading qualification costs and enhancing profitability. – The embedded diagnostics help service networks quickly isolate faults, reducing warranty claims and improving brand reputation. – End‑users appreciate the ability to support future software‑driven features without hardware redesign. |

| By Interface |

|

PWM Interface stands out as the preferred communication style for power‑train control modules because it simplifies timing integration and leverages existing motor control infrastructure. – Engineers value the deterministic behavior of PWM signals for precise load management. – The interface supports seamless scaling from low‑power accessory circuits to higher‑current power stages, fostering design reuse. |

| By Channel |

|

Dual Channel solutions are gaining traction as vehicle architectures consolidate multiple load paths into fewer control units. – They enable coordinated protection strategies across related circuits, improving overall system safety. – Dual‑channel devices reduce board space and component count, aligning with the industry’s focus on lightweight design. – The ability to share diagnostic data between channels supports advanced fault‑tolerant algorithms. |

Regional Analysis: Smart High-Side Switch Controller Market

North America

Vehicle manufacturers are integrating smart high‑side switches to meet stringent efficiency mandates, allowing finer torque control while reducing thermal stress on power‑train components. The shift toward electrified powertrains amplifies the relevance of precise current management, and OEMs are rewarding suppliers that can guarantee seamless firmware upgrades over the vehicle lifespan.

Factories modernising their automation lines are replacing legacy relays with intelligent switches that can self‑diagnose and adapt to variable load profiles. This transition minimizes unplanned stoppages and aligns with lean‑manufacturing imperatives, prompting a wave of retrofit projects across the Midwest.

Federal efficiency standards now reference power‑stage loss limits, nudging designers toward switches that combine low on‑resistance with active protection features. Compliance audits increasingly scrutinise controller firmware, making security patches a contractual necessity.

Proximity of silicon fabs to automotive clustering enables just‑in‑time deliveries, while diversified sourcing of passive components mitigates the occasional bottleneck that has plagued adjacent semiconductor segments.

Europe

European manufacturers are capitalising on the region’s strong emphasis on sustainability, prompting many automotive and renewable‑energy firms to embed smart high‑side switches within on‑board chargers and wind‑turbine converters. The European Union’s directive on energy‑intensive equipment forces original equipment manufacturers to demonstrate measurable reductions in power losses, turning intelligent control chips into a compliance lever. Concurrently, a wave of collaborative research programmes linking universities with Tier‑1 suppliers is fostering a pipeline of algorithms that anticipate fault conditions before they manifest, thereby extending equipment service intervals. Companies that align product roadmaps with these collaborative ecosystems are positioning themselves to capture design‑win opportunities across both the automotive and industrial sectors.

Asia‑Pacific

The Asia‑Pacific landscape is characterised by rapid adoption of electric mobility in China, India, and Southeast Asia, where cost‑sensitive manufacturers still demand high reliability. Local fabs have begun producing silicon‑on‑insulator (SOI) technologies that enable the high‑side switches to operate at elevated temperatures, a necessity given the region’s diverse climate zones. Meanwhile, industrial conglomerates in Japan and South Korea are integrating these controllers into robotics platforms that require deterministic switching to maintain precision in high‑speed assembly lines. The convergence of aggressive pricing pressure and a strong push for automation fuels an environment where vendors must balance performance with scalable manufacturing processes.

South America

In South America, the market is still nascent but benefits from growing renewable‑energy projects, especially solar farms in Brazil and Argentina. Project developers are turning to smart high‑side switches to optimise inverter efficiency and to provide remote monitoring capabilities essential for large‑scale deployments in remote locations. The region’s regulatory bodies are gradually adopting standards that mirror those of North America and Europe, nudging local manufacturers to upgrade legacy power‑stage designs. Early movers that can deliver robust, low‑maintenance solutions are likely to secure long‑term service contracts, which serve as a catalyst for market maturation.

Middle East & Africa

The Middle East & Africa sees a distinct driver in the oil‑and‑gas sector, where high‑side switches are employed to protect critical pump‑jacks and compression units operating under extreme temperatures. Recent investments in data‑center infrastructure across the United Arab Emirates also create demand for power‑distribution units that rely on intelligent switching to achieve tighter energy budgets. While the overall market size remains modest, the strategic importance of reliability in harsh environments encourages operators to adopt premium controllers that integrate predictive analytics, thereby reducing unplanned outages and extending equipment life.

Report Scope

This market research report provides a comprehensive analysis of the Smart High-Side Switch Controller Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as merges, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Smart High-Side Switch Controller Market?

-> Smart High-Side Switch Controller market size is forecasted to reach USD 2.421 billion by 2034, showing a CAGR of 8.6 % during the forecast period.

Which key companies operate in Smart High-Side Switch Controller Market?

-> Key players include STMicroelectronics, Infineon, Diodes Incorporated, ROHM, Renesas, Fuji Electric, Texas Instruments, Microchip, onsemi, Toshiba, among others.

What are the key growth drivers?

-> Key growth drivers include the shift toward centralized intelligent power distribution in vehicles, demand for wiring reduction, integration of load switching with on‑chip diagnostics and protection, and platform reuse that spreads qualification costs across long‑life programs.

Which region dominates the market?

-> Asia leads the market, driven by high production volumes in China, Japan, and South Korea, while Europe remains a significant contributor.

What are the emerging trends?

-> Emerging trends include software‑defined power architectures, AI/IoT‑enabled diagnostic intelligence, higher‑voltage dual‑channel controllers, and increased adoption of PWM and SPI interfaces for flexible vehicle control strategies.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...