Position Encoding Chip Market Insights

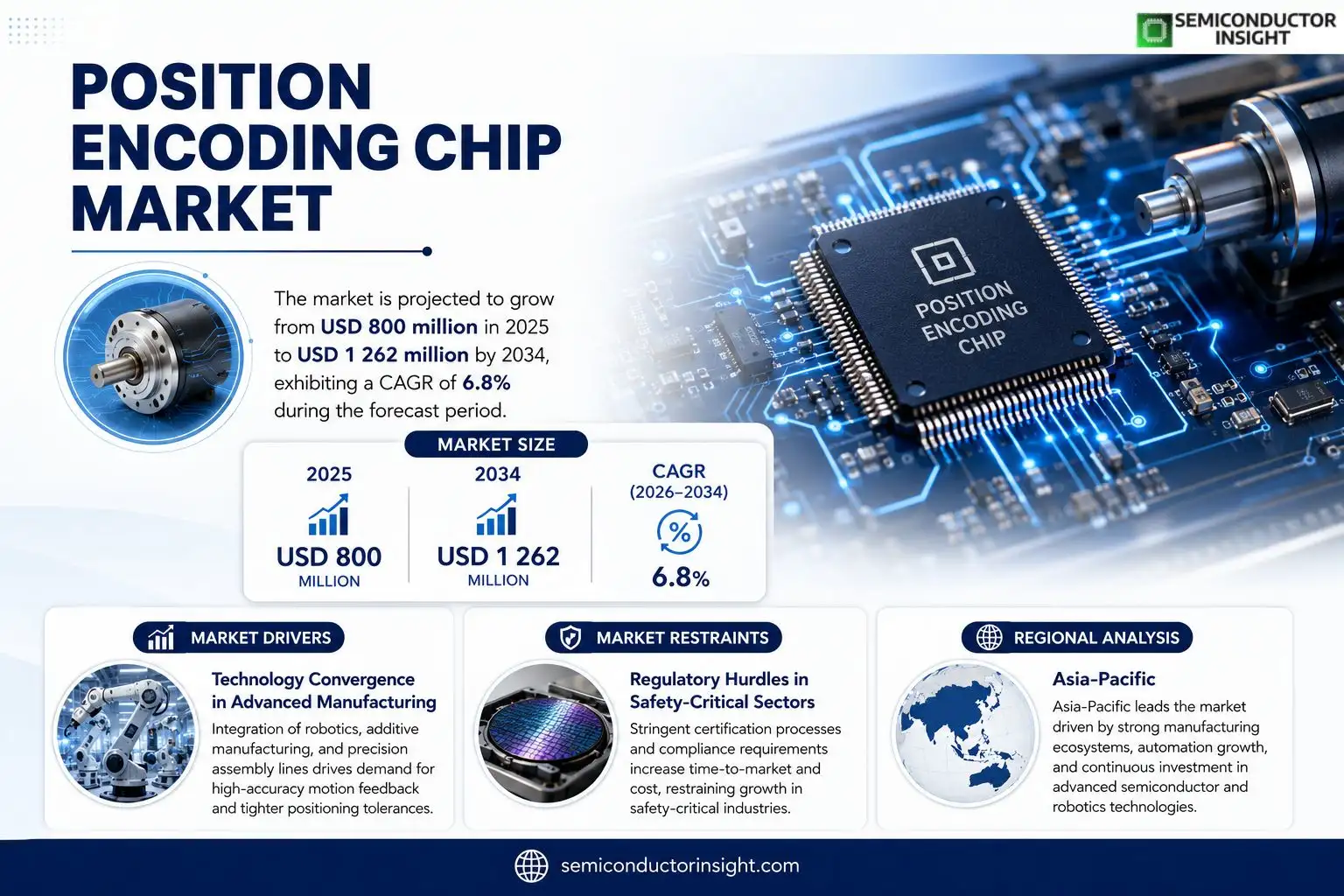

Position Encoding Chip market size was valued at USD 800 million in 2025. The market is projected to grow from USD 800 million in 2025 to USD 1 262 million by 2034, exhibiting a CAGR of 6.8% during the forecast period.

A position encoding chip is a dedicated ASIC that translates linear or rotary displacement into recognizable electrical or digital signals. Typically paired with rotary or linear encoders, the chip captures pulse, quadrature or absolute code outputs, decodes them and computes motion parameters such as position, direction and velocity before delivering the results via parallel, serial or bus interfaces (SPI, SSI, BiSS, ABI). These chips are integral to servo‑motor control, industrial automation, robotics, CNC machine tools and precision instrumentation where high‑accuracy feedback is mandatory.The market is expanding because manufacturers are upgrading factory automation lines and robotics systems that demand tighter positioning tolerances. Concurrently, the rise of electric‑vehicle power‑train assembly and renewable‑energy equipment adds further demand for reliable motion feedback solutions. Leading suppliersincluding ams OSRAM, Allegro MicroSystems, Infineon Technologies, Melexis and NXP Semiconductorsare broadening their portfolios with mixed‑signal front‑ends and advanced interface options to capture emerging opportunities.

MARKET DRIVERS

Technology Convergence in Advanced Manufacturing

The integration of robotics, additive manufacturing, and high‑precision assembly lines has heightened demand for accurate motion feedback. Position Encoding Chip Market participants are benefitting from factories that require sub‑micron resolution to maintain product quality while reducing cycle times. This shift reflects a broader move toward digital twins, where precise position data feeds simulation models that drive productivity gains.

Expansion of Autonomous Vehicle Platforms

Self‑driving cars and delivery drones rely on positional awareness to navigate complex environments. The surge in prototype testing and limited‑run production creates a niche where high‑integrity encoders are preferred over conventional sensors. Companies that can deliver chips tolerant to vibration and temperature extremes find a receptive client base within Position Encoding Chip Market.

➤ “Manufacturers that embed robust position‑encoding solutions into their equipment report up to 15 % improvement in line throughput.”

Beyond automotive, industrial IoT gateways increasingly embed compact encoders to provide real‑time location tagging for assets. This trend fuels a cascade of orders that, while modest in volume, command premium pricing because of the reliability requirements imposed by mission‑critical applications.

MARKET CHALLENGES

Supply‑Chain Bottlenecks for Specialized Materials

Fabricating high‑resolution chips demands rare‑earth substrates and ultra‑pure silicon wafers. Recent geopolitical tensions have constrained the flow of these inputs, leading to longer lead times and higher unit costs. Suppliers that cannot secure a stable feedstock risk losing contracts to rivals with diversified sourcing strategies.

Other Challenges

Design Complexity

Engineering teams must balance resolution, power consumption, and form factor within tight mechanical envelopes. This multi‑objective optimization often extends development cycles, delaying time‑to‑market for new encoder generations.

MARKET RESTRAINTS

Regulatory Hurdles in Safety‑Critical Sectors

Industries such as aerospace and medical equipment subject position‑encoding components to rigorous certification processes. The cost and time associated with obtaining functional safety approvals (e.g., ISO 26262, IEC 60601) act as a barrier for smaller entrants, consolidating market share among established players.

Price Sensitivity in High‑Volume Consumer Goods

When encoders are incorporated into mass‑produced consumer appliances, price pressures tighten. Margins shrink, prompting manufacturers to favor lower‑cost alternatives, even if those alternatives deliver slightly reduced performance. This dynamic limits the upside potential for premium‑priced chips in certain segments of Position Encoding Chip Market.

MARKET OPPORTUNITIES

Emerging Edge‑AI Devices

Edge‑AI modules that perform on‑device inference for robotics and smart infrastructure require precise position data to calibrate algorithms in real time. Embedding next‑generation encoding chips directly onto AI boards eliminates external wiring, reducing latency and improving system reliability. This integration opens a revenue stream for vendors that can co‑design chips with AI silicon partners.

Customizable ASIC Solutions for Niche Applications

Companies that offer application‑specific integrated circuits (ASICs) incorporating position‑encoding functionality can address specialized markets such as satellite docking mechanisms and high‑precision surgical robots. The willingness of these end‑users to pay a premium for turnkey solutions translates into higher average contract values within Position Encoding Chip Market.

Position Encoding Chip Market Trends

Integration of High‑Precision Interfaces

The latest wave of integration centers on embedding advanced signal‑conditioning circuits directly into the Position Encoding Chip. Manufacturers are consolidating analog front‑ends, decoding logic, and serial bus drivers onto a single die, thereby shrinking board footprints and reducing latency. This shift matters because modern servo‑motor controllers and robotic joints demand sub‑microsecond response times; any extra conversion stage can jeopardize closed‑loop stability. By delivering end‑to‑end functionality within the chip, suppliers enable system designers to eliminate peripheral components, lower BOM costs, and accelerate time‑to‑market for high‑performance equipment. The trend also creates a competitive moat: firms that master mixed‑signal design and advanced packaging gain a distinct advantage in sectors where precision and reliability are non‑negotiable.

Other Trends

Shift Toward Modular Automation Platforms

Industrial customers increasingly favor modular automation architectures that can be re‑configured on the fly. In this context, Position Encoding Chips are being offered as plug‑and‑play modules compatible with a variety of encoder familiesrotary, linear, magnetic, and optical. The modular approach simplifies integration across legacy lines and new installations alike, reducing engineering overhead. Vendors that provide comprehensive software libraries and standardized communication stacks (e.g., SPI, SSI, BiSS) position themselves as preferred partners for system integrators seeking scalability without sacrificing accuracy.

Emergence of AI‑Enabled Motion Control

Artificial‑intelligence algorithms are entering motion‑control loops to predict load variations and optimize trajectory planning. Position Encoding Chips are adapting by exposing richer diagnostic datasuch as jitter, temperature drift, and signal‑to‑noise ratiosthrough high‑speed serial interfaces. This richer telemetry feeds AI models that fine‑tune motor currents in real time, improving energy efficiency and extending equipment life. The implication for the market is twofold: chip designers must embed higher‑resolution ADCs and more robust error‑correction features, while end‑users gain the ability to implement predictive maintenance strategies that were previously limited to larger, costlier controller platforms.

COMPETITIVE LANDSCAPE

Key Industry Players

Position Encoding Chip Market – Competitive Overview

The segment is dominated by a handful of multinational semiconductor houses that combine deep analog IP portfolios with high‑volume silicon manufacturing. ams OSRAM, Infineon Technologies and Texas Instruments each operate vertically integrated lines, from wafer fab to final ASIC, which enables them to lock in the bulk of revenue that flows from industrial automation, robotics and precision tooling. Their product road‑maps emphasize multi‑protocol interfaces (SPI, SSI, BiSS) and robust packaging that satisfies the tight reliability margins demanded by servo‑motor drives. Because these firms command extensive design services and distribution channels, they shape pricing benchmarks and set performance baselines that smaller rivals must align with.Beyond the tier‑one group, a constellation of specialised firms targets niche encoder formats and emerging application zones. Allegro MicroSystems and NXP Semiconductors leverage differentiated magnetic‑sensor expertise to supply absolute‑code chips for automotive actuation. Analog Devices and Melexis focus on mixed‑signal front‑ends optimized for linear encoder feedback in CNC machinery. Companies such as iC‑Haus, TDK‑Micronas and MagnTek carve out market share by tailoring ASICs to compact, low‑power robots and new‑energy equipment, where size and energy efficiency outweigh sheer throughput. This fragmented layer intensifies competition on customization, speed to market and support services, compelling the larger players to pursue strategic partnerships or acquisitions to broaden their niche coverage.

List of Key Position Encoding Chip Companies Profiled

- ams OSRAM

- Allegro MicroSystems

- Infineon Technologies

- Melexis

- NXP Semiconductors

- TDK-Micronas

- iC-Haus

- Analog Devices

- Texas Instruments

- Renesas Electronics

- Broadcom

- ROHM Semiconductor

- Toshiba

- STMicroelectronics

- Microchip Technology

- MagnTek

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Analog Signal Output

|

| By Application |

|

Industrial Automation

|

| By End User |

|

Servo Motor Systems

|

| By Encoding Method |

|

Absolute Encoding

|

| By Measurement Object |

|

Rotary Position Encoding

|

Regional Analysis: Position Encoding Chip Market

Asia-Pacific

Recent fab expansions in Taiwan and South Korea have pushed wafer throughput to levels that comfortably satisfy the rising demand for high‑density encoding chips. The strategic focus on 300‑mm platforms reduces per‑unit cost, giving regional players a cost advantage that rivals outside the area find hard to replicate.

Multi‑tiered supplier networks, backed by diversified logistics hubs in Singapore and Hong Kong, have insulated the market from recent disruptions. Companies now favor regional sourcing agreements that embed buffer inventories at key nodes, ensuring steady component flow for volume production.

Collaborative research consortia linking universities, fab operators, and chip designers accelerate the migration toward 5‑nanometer encoding architectures. The emphasis on low‑power, high‑precision designs fuels differentiated offerings for emerging workloads such as generative AI inference.

Harmonized standards across the Association of Southeast Asian Nations (ASEAN) streamline certification pathways, allowing firms to introduce new encoding solutions across multiple markets with minimal compliance friction, an advantage that accelerates time‑to‑market.

North America

North America remains a critical design hub for Position Encoding Chip Market, with most leading architecture firms headquartered in the United States. The region’s strength lies in its deep talent pool and robust venture ecosystem, which together foster rapid prototype cycles. However, domestic fab capacity is limited, prompting companies to rely on offshore manufacturing while retaining design and testing functions at home. This split creates strategic tension: firms must balance intellectual‑property protection with the logistical complexities of cross‑border production. Emerging policy incentives aimed at reshoring semiconductor equipment hint at a possible shift, yet the timeline for material impact remains uncertain.

Europe

European stakeholders view Position Encoding Chip Market through the prism of sovereign technology agendas. The EU’s emphasis on supply‑chain security has led to collaborative projects that integrate encoding chips into automotive and industrial automation platforms. While Europe lacks the sheer volume capacity of Asia‑Pacific, its strength resides in high‑value niche applications, particularly in safety‑critical systems where certification rigor is paramount. The region’s regulatory framework, anchored by strict data‑privacy and emissions standards, shapes product specifications, encouraging designs that prioritize energy efficiency without sacrificing precision.

South America

In South America, market momentum is modest but gaining traction as local manufacturers explore edge‑computing deployments for agricultural technology and smart‑city initiatives. Countries such as Brazil and Chile are investing in research partnerships that bring encoding expertise to home‑grown IoT devices. The principal challenge remains limited fab infrastructure, which forces firms to import most components. Nonetheless, growing governmental interest in digital transformation offers a pathway for the region to develop a more self‑sufficient ecosystem over the next decade.

Middle East & Africa

The Middle East & Africa segment is characterized by nascent adoption of advanced encoding chips, primarily driven by data‑center expansion in the Gulf and telecom upgrades across Sub‑Saharan networks. Investment funds in the United Arab Emirates are beginning to back chip‑design start‑ups, marking a shift from pure consumption to modest co‑development. Infrastructure constraints and a shortage of specialized engineering talent temper rapid growth, yet strategic alliances with Asian manufacturers provide a bridge that could accelerate capability building if local policy frameworks continue to support high‑tech diversification.

Report Scope

This market research report provides a comprehensive analysis of the Position Encoding Chip Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Position Encoding Chip Market?

-> Position Encoding Chip Market was valued at USD 800 million in 2025 and is expected to reach USD 1262 million by 2034, growing at a CAGR of 6.8% during the forecast period.

Which key companies operate in Position Encoding Chip Market?

-> Key players include ams OSRAM, Allegro MicroSystems, Infineon Technologies, Melexis, NXP Semiconductors, TDK‑Micronas, iC‑Haus, Analog Devices, Texas Instruments, Renesas Electronics, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for high‑precision position feedback in industrial automation, robotics, CNC machine tools, new energy equipment, and expanding servo‑motor control applications.

Which region dominates the market?

-> Regional data is not explicitly disclosed in the reference; however, strong manufacturing and automation activity in Asia, particularly China, suggests a leading role.

What are the emerging trends?

-> Emerging trends include integration of Position Encoding Chips with AI‑enabled predictive maintenance, higher‑resolution absolute encoding, and growing use in electric‑vehicle powertrains and smart‑factory systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...