Fully-Protected High-side Switch Market Insights

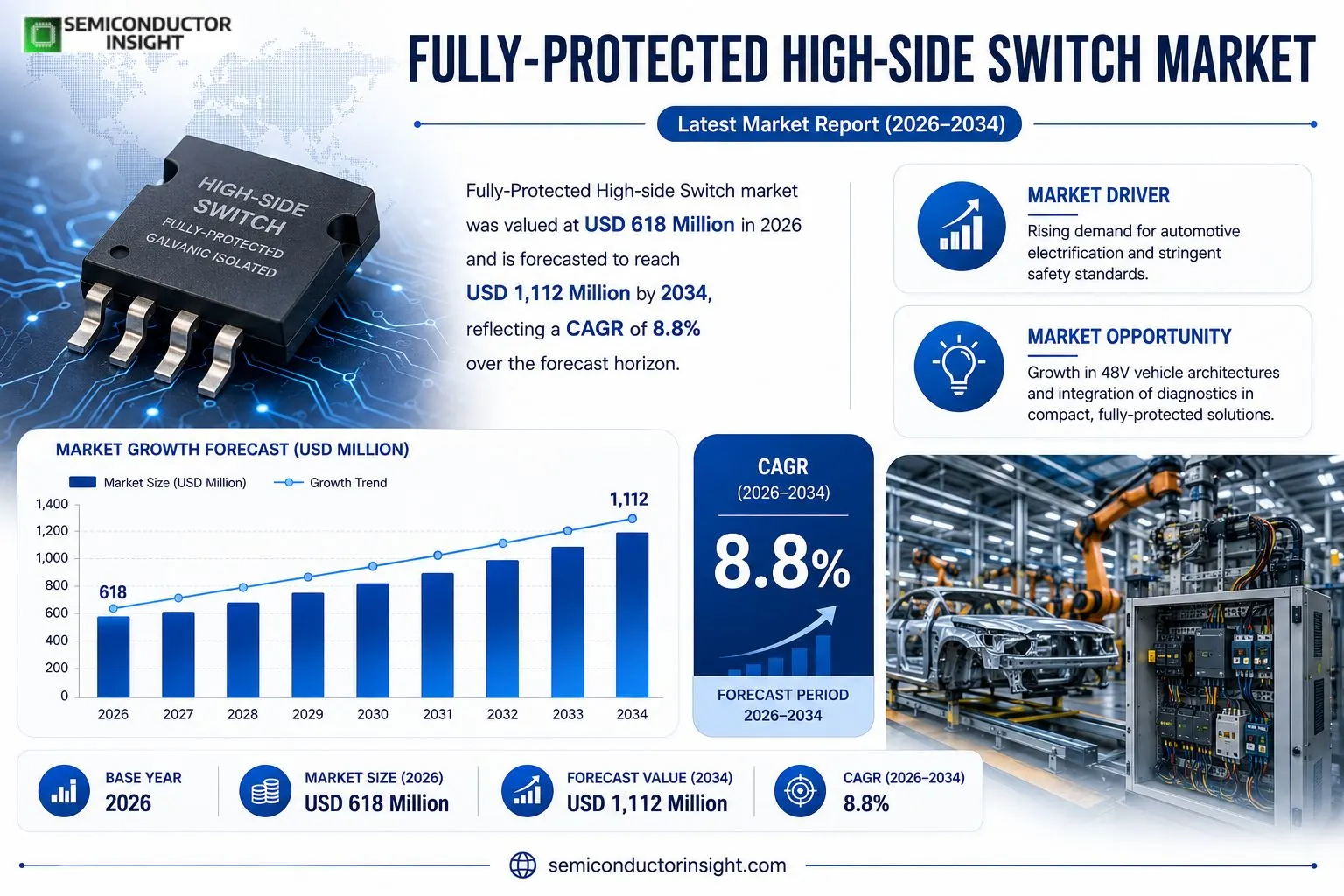

Fully-Protected High-side Switch market size was valued at USD 618 million in 2026 and is forecasted to reach USD 1,112 million by 2034, reflecting a CAGR of 8.8 % over the forecast horizon.

Galvanic Isolated High-side Switches are high‑side load control devices that embed galvanic isolation between control and power domains while delivering switching, protection and diagnostic functions. The architecture provides strong noise immunity and reliable fault containment for automotive and industrial power systems. In 2026 production reached roughly 111 million units at an average price of USD 6.1 per unit; capacity utilization stood at about 71 % and gross margins averaged 43 %.The upward trajectory stems from tightening safety standards, growing electromagnetic‑interference challenges, and expanding electrification that makes isolation a functional requirement rather than an optional premium. Upstream suppliers such as Shin‑Etsu Chemical, SUMCO and JSR provide silicon wafers and photoresists, while downstream customers include BYD, Toyota, Siemens and Rockwell Automation. Leading manufacturersincluding STMicroelectronics, Infineon, Diodes Incorporated, ROHM and Renesasare concentrating on integrating protection logic and diagnostics into compact modules to sustain margins as competition intensifies.

MARKET DRIVERS

Rising Demand for Automotive Electrification

The shift toward electric powertrains has elevated the importance of on‑board power distribution modules. Manufacturers now require switches that can guarantee isolation while handling high current bursts during acceleration and regenerative braking. Because failure modes directly affect vehicle range and safety, designers are migrating to fully‑protected topologies that combine intrinsic short‑circuit immunity with low on‑resistance, thereby reducing wiring complexity and improving overall efficiency.

Expansion of Renewable‑Energy Power Converters

Solar‑inverter and wind‑turbine platforms increasingly operate in harsh outdoor environments where voltage spikes are common. Fully‑protected high‑side switches offer a “plug‑and‑play” safety envelope that eliminates the need for external protection components, shortening the bill of materials and accelerating time‑to‑market. This integration advantage is especially compelling for Tier‑1 suppliers who must meet stringent EPC contracts while maintaining competitive margins.

➤ “Reliability is no longer optional; it forms the baseline for system certification in both automotive and renewable sectors.”

Consequently, OEMs and EPC firms alike view the protected switch as a strategic enabler. The combined effect of tighter OEM specifications and the push for modular converter designs generates a steady inflow of design wins for vendors that can provide validated, fully‑protected high‑side solutions.

MARKET CHALLENGES

Cost Sensitivity in Mass‑Market Applications

While the functional benefits are clear, the added silicon area and manufacturing steps inflate unit cost. Low‑volume automotive lines and consumer‑grade power supplies often operate on razor‑thin profit margins, prompting specifiers to weigh the expense of protection against the perceived risk. In markets where price elasticity dominates, many designers still opt for separate protection circuits to preserve cost targets.

Other Challenges

Thermal Management Constraints

The integration of protection structures within the switch die increases power density. Without adequate heat‑spreading strategies, junction temperatures can approach critical limits during peak load events, forcing designers to allocate additional board space for heat sinks or to derate the device, thereby negating some of the layout savings the protected architecture promises.

MARKET RESTRAINTS

Stringent Certification Requirements

Automotive safety standards such as ISO‑26262 and functional‑safety clauses in IEC 61800 demand extensive validation of protective mechanisms. Achieving compliance often requires lengthy qualification cycles, additional test equipment, and repetitive failure‑mode analysis. Companies that cannot absorb these upfront expenditures may defer adoption, slowing overall market penetration.

MARKET OPPORTUNITIES

Emergence of 48‑V Vehicle Architectures

The introduction of 48‑volt systems in mild‑hybrid and e‑powertrain platforms creates a niche where traditional low‑voltage switches struggle with safety margins. Fully‑protected high‑side switches can bridge this gap by delivering robust isolation at intermediate voltage levels, opening a sizable opportunity for semiconductor firms to capture a segment that is rapidly gaining design attention across the automotive supply chain.

Fully-Protected High-side Switch Market Trends

Integration of Isolation as a System Standard

Fully-Protected High-side Switch Market is being reshaped by tightening automotive safety regulations and more hostile electromagnetic environments in industrial power systems. Manufacturers are shifting from offering isolation as an optional premium to embedding it as a baseline function, because the cost of system‑level failure now outweighs the incremental price of a protected device. In 2026, average unit pricing hovered around USD 6.1 while capacity utilization reached roughly 71 %, indicating that factories are running close to optimal throughput without sacrificing quality. Gross margins of about 43 % reflect the value captured through reduced downstream component count and simpler certification pathways. As vehicle electrification pushes operating voltages higher, customers prioritize switches that combine galvanic isolation, fault containment and on‑chip diagnostics, driving a re‑allocation of engineering resources toward compact, integrated architectures.

Other Trends

Supply‑Chain Coordination and Design Complexity

Upstream, the market relies on a narrow set of silicon wafer and epoxy mold providers such as Shin‑Etsu Chemical and Sumitomo Bakelite. Their ability to maintain consistent material quality under rising demand directly influences yield rates in the midstream design phase, where system architecture, protection logic and reliability engineering converge. Companies that can synchronize tape‑out schedules with supplier capacity are able to lock in tighter tolerances and lower test‑cycle times, a competitive edge in an industry where product lifecycles extend over several vehicle generations. Downstream, automotive OEMs like BYD and Toyota are specifying Fully‑Protected High‑side Switches to meet stricter functional safety standards, while industrial players such as Siemens are leveraging the same devices to safeguard automation lines from transient over‑voltages. This dual‑track demand forces vendors to balance volume production with the need for customizable diagnostic features, creating a nuanced risk‑return profile for each product family.

Competitive Positioning and Margin Sustainability

Key participantsincluding STMicroelectronics, Infineon, and Texas Instrumentsare differentiating through platform‑level reuse that stabilizes pricing across generations, while investing in thermal‑management techniques that preserve reliability at higher current densities. The firms that convert isolation performance into tangible system‑cost reductions are better placed to protect their margins as rivals intensify price pressure. Consequently, strategic moves such as expanding in‑house wafer capabilities or forming long‑term material supply agreements are becoming essential levers for maintaining profitability within the Fully‑Protected High‑side Switch Market.

COMPETITIVE LANDSCAPE

Key Industry Players

Fully‑Protected High‑Side Switch Market – Competitive Overview

In 2026 the segment generated roughly $618 million and is slated to reach $1,112 million by 2034, delivering an 8.8 % compound annual growth. The landscape is dominated by a handful of silicon power specialists that command the bulk of volume and margin. STMicroelectronics and Infineon lead with integrated isolation‑plus‑protection families that are embedded in major automotive platforms, leveraging deep relationships with OEMs such as Toyota and Volkswagen. Their scale enables low‑cost wafer procurement and long‑run pricing stability, which sustains the ~43 % gross margin observed across the sector. Parallel to the leaders, Texas Instruments and ON Semiconductor have broadened their portfolios to cover dual‑channel PWM‑controlled devices, appealing to industrial system integrators seeking a single‑chip solution that reduces board count.Beyond the tier‑one incumbents, a diverse set of niche players contributes differentiated technology or regional reach. Diodes Incorporated, ROHM Semiconductor, and Renesas Electronics focus on high‑voltage, low‑loss designs for electric‑vehicle power‑train modules. Fuji Electric and Toshiba concentrate on ruggedized units for factory automation, often partnering with system integrators like Siemens and Schneider Electric. Smaller firms such as NXP, Analog Devices, and Maxim Integrated (now part of ADI) supply specialty interfaces and diagnostic features that address emerging safety standards. The competitive pressure forces all participants to embed diagnostic intelligence and extend lifecycle support, turning isolation performance into a decisive value proposition for customers.

List of Key Fully‑Protected High‑Side Switch Companies Profiled

- STMicroelectronics

- Infineon Technologies

- Diodes Incorporated

- ROHM Semiconductor

- Renesas Electronics

- Fuji Electric

- Texas Instruments

- Microchip Technology

- ON Semiconductor

- Toshiba

- NXP Semiconductors

- Analog Devices

- Maxim Integrated

- Cypress Semiconductor

- Silicon Labs

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Galvanic Isolated Switches

|

| By Application |

|

Automotive Powertrain

|

| By End User |

|

Tier‑1 Suppliers

|

| By Isolation Architecture |

|

SiC‑Based Isolation

|

| By Functional Integration |

|

Switch‑with‑Telemetry

|

Regional Analysis: Fully-Protected High-side Switch Market

North America

Vehicle manufacturers are embedding fully‑protected high‑side switches to safeguard electric power‑train modules against harsh electrical spikes, a practice that improves reliability while supporting tighter packaging constraints. The trend reflects a broader shift toward electronic architectures that prioritize safety at the silicon level.

Factories adopting Industry 4.0 principles rely on uninterrupted power flow; fully‑protected switches deliver the isolation needed for motor drives and robotics, reducing fault propagation and simplifying maintenance regimes.

Portable devices and wearables benefit from compact protection schemes that allow higher battery voltages without sacrificing safety, encouraging designers to specify fully‑protected solutions as a baseline component.

Harmonized safety standards across North America drive a preference for hardware‑level safeguards, prompting manufacturers to incorporate fully‑protected switches early in the design process to streamline certification pathways.

Europe

European manufacturers are reconfiguring power‑distribution strategies to align with the continent’s aggressive energy‑efficiency directives. In sectors such as rail transport and offshore wind, fully‑protected high‑side switches are valued for their ability to tolerate fluctuating grid conditions while preserving equipment integrity. The region’s strong emphasis on sustainability encourages manufacturers to adopt components that minimize waste through extended service life, thereby supporting circular‑economy goals. Additionally, collaborative research programs funded by EU bodies accelerate the integration of advanced silicon technologies, reinforcing Europe’s position as a hub for innovative protective solutions.

Asia‑Pacific

The Asia‑Pacific landscape is shaped by rapid electrification of mobility and a surge in smart‑factory deployments. Suppliers in Japan, South Korea, and emerging markets such as Vietnam are tailoring fully‑protected high‑side switches to meet diverse voltage specifications, a response to fragmented power‑system architectures. Customer demand focuses on devices that combine high current capability with robust isolation, enabling compact designs for electric scooters and compact industrial inverters. Regional trade agreements facilitate cross‑border component flow, allowing manufacturers to source advanced protective switches without compromising on lead‑time or compliance with local safety codes.

South America

In South America, the drive toward renewable‑energy integration in national grids creates a need for resilient power‑conversion hardware. Fully‑protected high‑side switches are being adopted in solar‑farm inverters and hydro‑electric control systems to mitigate the impact of voltage surges caused by variable generation patterns. Market participants recognize that device reliability directly influences project financing, prompting a cautious yet growing preference for high‑integrity protection solutions. Local engineering firms are also collaborating with silicon providers to customize switch designs that address climatic challenges such as high humidity and temperature extremes.

Middle East & Africa

The Middle East & Africa region experiences a dual challenge of expanding industrial capacity while managing harsh operating environments. Fully‑protected high‑side switches are increasingly specified for oil‑field automation and desert‑based solar installations, where voltage spikes from lightning and equipment switching are common. Companies prioritize devices that combine rugged packaging with precise fault detection, reducing the need for extensive external protection circuitry. Strategic partnerships between regional distributors and international silicon vendors are enabling faster technology transfer, positioning the market to benefit from emerging safety standards that emphasize built‑in hardware safeguards.

Report Scope

This market research report provides a comprehensive analysis of the Fully-Protected High-side Switch Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Fully-Protected High-side Switch Market?

-> Fully-Protected High-side Switch Market was valued at USD 618 million in 2026 and is expected to reach USD 1112 million by 2034 (CAGR 8.8%).

Which key companies operate in Fully-Protected High-side Switch Market?

-> Key players include STMicroelectronics, Infineon, Diodes Incorporated, ROHM, Renesas, Fuji Electric, Texas Instruments, Microchip, onsemi, and Toshiba, among others.

What are the key growth drivers?

-> Key growth drivers include rising safety standards, increasing electromagnetic interference in automotive and industrial power systems, expanding electrification that raises voltage and current requirements, and the functional need for galvanic isolation to reduce system risk and improve uptime.

Which region dominates the market?

-> Asia-Pacific leads the market, driven by major automotive manufacturers and industrial adopters such as BYD, SAIC Motor, Geely Auto, and Toyota.

What are the emerging trends?

-> Emerging trends include integration of isolation, protection and diagnostics into compact architectures, platform‑level reuse to stabilize pricing, and the shift of isolation from a premium feature to a functional requirement in next‑generation power systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...