High-performance Quantum Encryption Chip Market Insights

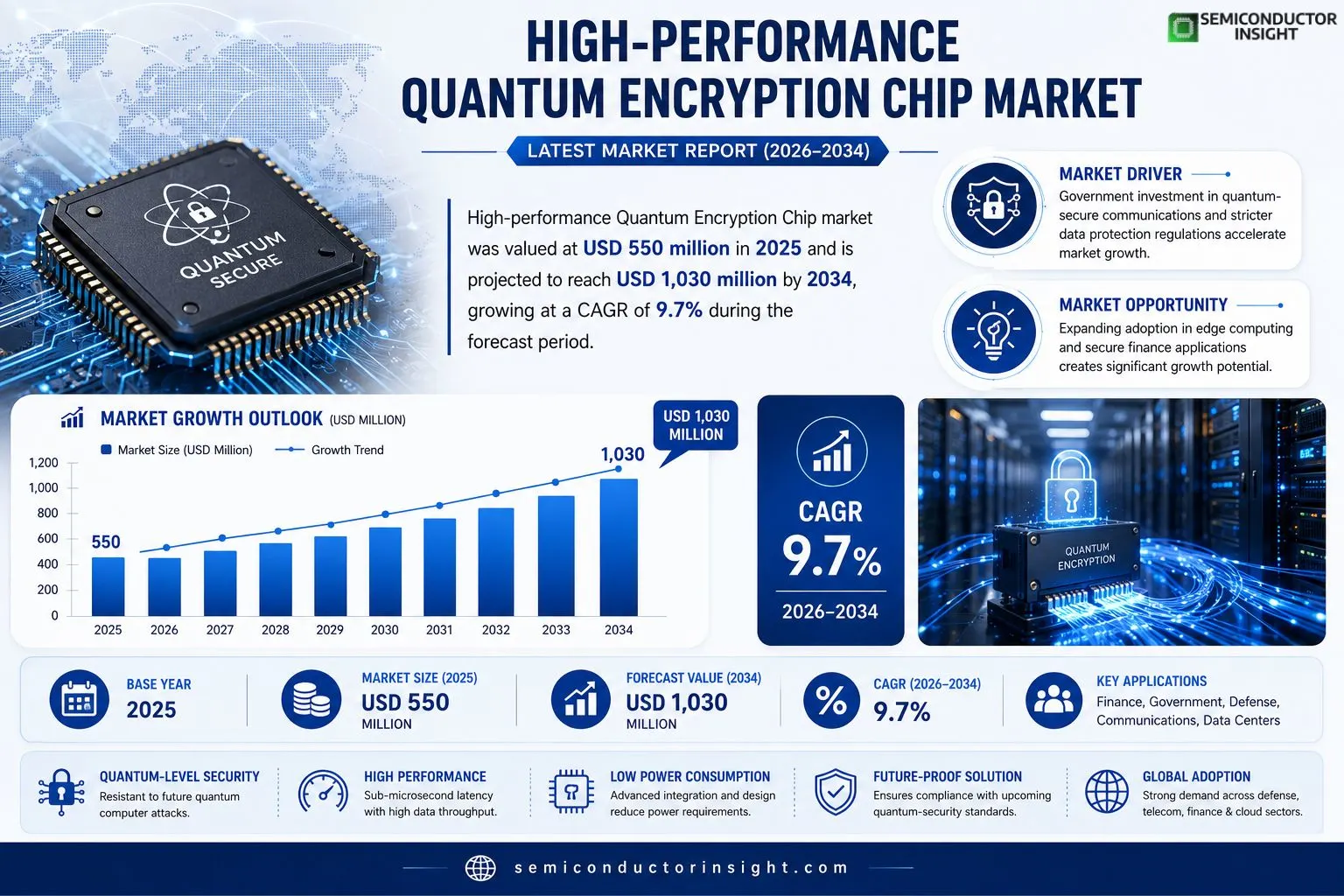

High-performance Quantum Encryption Chip market size was valued at USD 550 million in 2025. The market is projected to grow from USD 550 million in 2025 to USD 1,030 million by 2034, exhibiting a CAGR of 9.7% during the forecast period.

A high‑performance quantum encryption chip is a semiconductor device that exploits quantum‑mechanical principles such as superposition and entanglement to protect data transmission. Typical functions include quantum key distribution (QKD), quantum random number generation (QRNG) and acceleration of cryptographic algorithms, delivering resistance against future quantum‑computer attacks while maintaining low latency.The market is gaining momentum because governments are investing heavily in quantum‑secure communications, financial institutions are seeking ultra‑secure transaction channels, and data‑center operators require protection against emerging threats. Moreover, advances in photonic integration and solid‑state fabrication are lowering power consumption and enabling higher data rates, which encourages early adopters across defense and telecom sectors.

MARKET DRIVERS

Performance Demands from Cloud Service Providers

Leading hyperscale operators are allocating sizable CAPEX to retrofit data‑center fabric with quantum‑grade security. The move stems from an observable escalation in sophisticated cyber‑espionage campaigns, prompting providers to seek latency‑neutral encryption that does not compromise throughput. As a result, the High-performance Quantum Encryption Chip Market experiences a tangible uptick in procurement cycles.

Regulatory Momentum for Data Protection

New legislations across North America and Europe now mandate cryptographic techniques that resist quantum attacks. Companies that fail to align with these standards risk hefty penalties and eroded customer confidence. Consequently, firms are accelerating investments in chips that can guarantee future‑proof confidentiality, reinforcing market velocity.

➤ “Enterprises that prioritize quantum‑resilient hardware today will avoid costly retrofits when tomorrow’s standards become mandatory.”

Venture capital activity around startups specializing in cryogenic semiconductor processes adds another layer of financial momentum. The influx of growth funding enables rapid scaling of fabrication lines, which in turn shortens time‑to‑market for next‑generation modules.

MARKET CHALLENGES

Integration Complexity

Embedding quantum encryption cores into existing silicon architectures requires extensive redesign of system‑level interfaces. Engineers grapple with reconciling disparate clock domains and thermal envelopes, a reality that elongates development timelines and inflates engineering budgets.

Other Challenges

Supply‑Chain Constraints

The niche materialssuch as isotopically purified silicon and ultra‑pure superconductorsare sourced from a limited number of vendors. Any disruption in that supply chain translates directly into production bottlenecks, curbing the pace at which the High-performance Quantum Encryption Chip Market can expand.

MARKET RESTRAINTS

High Production Costs

The specialized lithography steps and low‑temperature packaging required for quantum‑grade chips drive unit costs well above those of conventional ASICs. For many mid‑market enterprises, the price premium remains a decisive barrier, limiting adoption to organizations with deep pockets or mission‑critical security mandates.

MARKET OPPORTUNITIES

Emerging Edge‑Computing Deployments

Edge nodes handling sensitive data streamssuch as autonomous vehicle telemetry and industrial IoTare beginning to require on‑device quantum protection. The convergence of low‑power chip designs with edge‑centric form factors creates a fertile niche where early adopters can differentiate through hardware‑based resilience without relying on cloud‑side safeguards.

High-performance Quantum Encryption Chip Market Trends

Rising Demand from Secure Finance and Government Networks

The adoption curve for high‑performance quantum encryption chips is steepening as financial institutions and sovereign agencies confront a wave of post‑quantum threats. Regulators are tightening data‑protection mandates, prompting banks to pilot quantum‑key‑distribution (QKD) links for inter‑branch settlement. Simultaneously, defense ministries are integrating quantum‑ready modules into classified communication backbones to safeguard command‑and‑control traffic. These forces converge on a common requirement: chips that deliver sub‑microsecond latency while preserving physical unclonable function security. Production volumes reached roughly 84,200 units in 2025, with an average unit price near USD 7,150, reflecting a nascent but price‑sensitive market. The escalation in procurement budgets is encouraging manufacturers to shift from discrete prototypes toward wafer‑scale integration, a move that promises lower power draw and higher data‑rate margins. Because the cost curve is gradually descending, early adopters are able to justify pilot projects that demonstrate ROI within two to three years.

Other Trends

Integration and Power Efficiency Advances

Design engineers are embedding quantum random‑number generators directly into the silicon substrate, eliminating the need for external entropy sources. This architectural compression reduces board space and cuts system‑level power consumption by up to 30 % compared with legacy modules. Concurrently, advances in cryogenic packaging enable operation at temperatures achievable with commercially available cooling solutions, sidestepping the cost barrier of deep‑cryogenic infrastructure. The result is a broader appeal to data‑center operators, who can now consider quantum‑secure acceleration as a drop‑in upgrade for latency‑critical workloads such as high‑frequency trading and encrypted cloud storage. Supply‑chain maturationevidenced by the emergence of dedicated photonic foundriesfurther stabilizes component lead times, allowing OEMs to plan multi‑year production ramps with greater confidence.

Emergence of Standardized Quantum Communication Frameworks

Interoperability standards are crystallizing around a handful of protocol suites that define key exchange, authentication, and error‑correction layers for quantum channels. As these specifications gain traction among national research networks, chip vendors are aligning product roadmaps to ensure compliance out‑of‑the‑box. This alignment mitigates integration risk for end‑users and accelerates marketplace acceptance, because customers no longer need bespoke firmware for each vendor’s device. Moreover, the regulatory push toward certifiable quantum‑secure solutions is fostering a competitive landscape where firms differentiate through validation processes rather than proprietary lock‑ins. For the High-performance Quantum Encryption Chip Market, the convergence of standards and certification pathways translates into a clearer value proposition for investors and a faster route to scale for manufacturers. Analysts anticipate that by 2027 the ratio of quantum‑secure endpoints to legacy devices will reach a tipping point, prompting enterprises to rewrite their security architectures around these chips.

COMPETITIVE LANDSCAPE

Key Industry Players

High‑performance Quantum Encryption Chip Market Competitive Landscape

Google’s quantum‑security unit commands the most visible share of the market, leveraging its cloud infrastructure and deep‑learning expertise to ship integrated quantum encryption chips that support both QKD and QRNG functions. The company’s aggressive IP portfolio and strategic collaborations with telecom operators have created a de‑facto standard for low‑latency, high‑throughput secure links, positioning Google as a benchmark for performance and scalability. Infineon complements this dominance with a strong semiconductor manufacturing base in Europe, delivering solid‑state quantum chips that emphasize power efficiency and mass‑production readiness. Their joint ventures with defense ministries reinforce a supply‑chain that can satisfy stringent government procurement criteria, shaping the market’s upper tier.Beyond the headline names, a constellation of specialized firms fuels innovation and regional diversification. Toshiba continues to exploit its photonic expertise, offering chips that integrate silicon‑photonic waveguides for ultra‑high data rates in Japanese and broader Asian networks. European entrants such as ID Quantique and QST GmbH focus on modular quantum modules tailored for finance and research institutions, while emerging players like PQShield, SEEQC, and Turing Quantum target niche defense contracts with hardened designs. Companies including C*Core Technology, QuantumCTek, SEALSQ, QuTech, MagiQ Technologies, and SecureRF round out the ecosystem, each contributing distinctive packaging or algorithmic approaches that broaden the technology’s applicability across data‑center, medical, and governmental segments.

List of Key High‑performance Quantum Encryption Chip Companies Profiled

- Infineon

- Toshiba

- ID Quantique

- PQShield

- SEEQC

- Turing Quantum

- C*Core Technology

- QuantumCTek

- SEALSQ

- QuTech

- QST GmbH

- MagiQ Technologies

- SecureRF

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Universal Chip

|

| By Application |

|

Finance

|

| By End User |

|

Financial Institutions

|

| By Technology |

|

Photonic Quantum Chip

|

| By Packaging |

|

Module‑Integrated Quantum Chip

|

Regional Analysis: High-performance Quantum Encryption Chip Market

North America

Federal programs such as the Quantum Initiative allocate billions toward chip‑level breakthroughs, while private labs leverage these funds to explore novel materials and error‑correction schemes. The intensity of this financing sustains a pipeline of prototypes that consistently outpace counterparts, reinforcing North America’s technical edge.

Fortune‑500 firms in banking and cloud computing have begun pilot programs, integrating quantum encryption chips into key‑management services. Their willingness to allocate budget early reflects confidence in the technology’s ability to mitigate future quantum‑based attacks.

Agencies such as NIST release draft standards that specifically reference quantum‑resistant hardware, prompting vendors to align product roadmaps with emerging compliance frameworks and giving buyers clear criteria for procurement.

Strategic stockpiling of critical substrates and the establishment of domestic fabs mitigate risks associated with geopolitical tensions, ensuring a reliable flow of components essential for high‑performance quantum chips.

Europe

European nations combine strong academic networks with coordinated policy initiatives, fostering a collaborative environment for quantum encryption chips. The European Union’s Horizon framework channels cross‑border funding toward joint ventures, encouraging standardisation across member states. Financial hubs in London, Frankfurt and Zurich view quantum‑grade security as a competitive differentiator, prompting early adopters to experiment with chip‑level integration. Meanwhile, data‑privacy regulations amplify demand for hardware that can guarantee confidentiality against future quantum threats, nudging vendors to tailor solutions for the continent’s stringent legal context.

Asia‑Pacific

Asia‑Pacific witnesses rapid escalation in governmental backing, particularly in Japan, South Korea and Singapore, where national strategies earmark quantum technologies as pillars of digital sovereignty. Corporate conglomerates in these economies are commissioning bespoke encryption solutions to protect cross‑border transactions and cloud infrastructures. Though the region lags in scale‑up capabilities compared with North America, aggressive talent recruitment and partnerships with Western fabs accelerate knowledge transfer, positioning the area for swift market entry once manufacturing bottlenecks ease.

South America

South America’s market remains nascent, yet recent policy shifts underscore a growing awareness of quantum security risks. Brazil’s technology ministries have initiated pilot projects within the banking sector, testing quantum chips in secure communications channels. While domestic manufacturing is limited, the region leverages import agreements with established suppliers, creating a foothold that could expand as local expertise matures and demand for resilient encryption intensifies.

Middle East & Africa

In the Middle East and Africa, selective investment drives early adoption, primarily among sovereign wealth funds and telecom operators seeking to safeguard critical infrastructure. Vision‑driven initiatives in the United Arab Emirates and Saudi Arabia pair public funding with partnerships to import cutting‑edge chips, while African nations focus on capacity‑building programs to develop a skilled workforce. The blend of financial muscle and strategic foresight lays groundwork for a gradual expansion of the High-performance Quantum Encryption Chip Market across these territories.

Report Scope

This market research report provides a comprehensive analysis of the High-performance Quantum Encryption Chip Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of High-performance Quantum Encryption Chip Market?

-> High-performance Quantum Encryption Chip Market was valued at USD 550 million in 2025 and is expected to reach USD 1030 million by 2034, growing at a CAGR of 9.7% during the forecast period.

Which key companies operate in High-performance Quantum Encryption Chip Market?

-> Key players include Google, Toshiba, PQShield, SEEQC, Infineon, Turing Quantum, C*Core Technology, QuantumCTek, and SEALSQ.

What are the key growth drivers?

-> Key growth drivers include development of quantum communication infrastructure, rising cybersecurity threats, demand for ultra‑high security in finance, government, defense, and data center sectors, and ongoing advances in chip integration and power efficiency.

Which region dominates the market?

-> Regional dominance is not explicitly defined in the reference; however, the market remains in early commercialization with strong interest across major economies, particularly in regions investing heavily in quantum communication networks.

What are the emerging trends?

-> Emerging trends include higher integration levels, lower power consumption, increased data rates, implementation of quantum‑level secure algorithms, and standardization efforts aimed at scalable production of quantum encryption chips.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...