Tactical Wi-Fi Interception System Market Insights

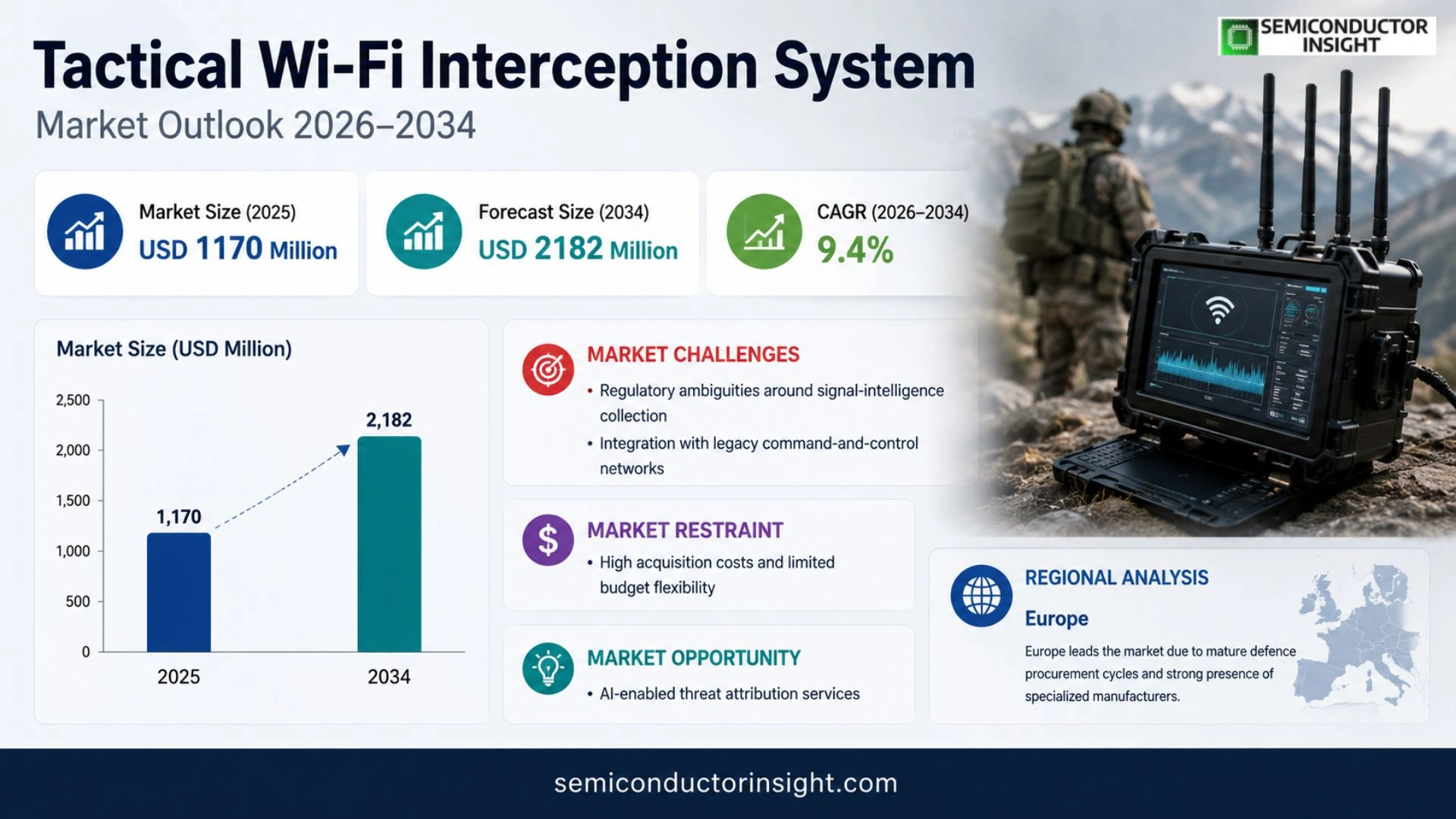

Global Tactical Wi-Fi Interception System market was valued at USD 1170 million in 2025 and will increase to USD 2182 million by 2034, reflecting a CAGR of 9.4% over the forecast period.

A Tactical Wi‑Fi Interception System is a field‑deployable solution that enables military units, intelligence agencies and law‑enforcement teams to covertly monitor, capture, decrypt and analyse traffic from IEEE 802.11 networks. The technology blends passive spectrum scanning with active exploitation techniques and remote‑management capabilities, allowing rapid on‑site or standoff deployment against both civilian and adversary devices.

Market expansion stems from heightened demand for real‑time electronic surveillance in contested environments, increased defence budgets allocating resources toward cyber‑electromagnetic operations, and tighter regulatory scrutiny that pushes authorised users toward vetted commercial offerings. Recent contracts announced in early 2024 by several national security agencies illustrate growing procurement activity, while advances in machine‑learning‑based packet analysis improve actionable intelligence extraction, further encouraging adoption.

MARKET DRIVERS

Escalating Cyber‑Threat Landscape in Forward Operating Areas

The proliferation of encrypted Wi‑Fi networks among hostile actors has compelled defense agencies to invest in sophisticated interception capabilities. Operators now demand tools that can capture, decrypt, and analyze traffic in real‑time, creating a clear impetus for growth in the Tactical Wi‑Fi Interception System Market. This pressure is amplified by recent incidents where compromised communications led to operational setbacks, prompting senior leadership to prioritize electronic surveillance as a core capability.

Advancements in Portable Signal‑Processing Hardware

Miniaturized ASICs and high‑speed FPGAs have shortened the latency between capture and decoding, allowing field units to act on intelligence within minutes rather than hours. Manufacturers are therefore rolling out next‑generation kits that integrate AI‑driven protocol identification, which directly boosts procurement budgets. The hardware evolution also reduces logistical footprints, aligning with the lean‑deployment strategies favored by modern armed forces.

➤ Stakeholders who align acquisition cycles with emerging firmware updates can secure a decisive advantage in contested electromagnetic environments.

Finally, the convergence of joint‑force initiatives across NATO and allied nations fosters common standards for Wi‑Fi interception, encouraging cross‑border procurement and shared research. Collaborative projects lower development risk and accelerate market adoption, positioning vendors that can certify to multinational specifications for long‑term contracts.

MARKET CHALLENGES

Regulatory Ambiguities Around Signal‑Intelligence Collection

National and international statutes governing electromagnetic surveillance remain fragmented, creating uncertainty for contractors seeking export licenses. Companies must navigate a patchwork of compliance regimes, which can delay deliveries and inflate legal costs. The lack of harmonized guidance also deters smaller innovators from entering the space, narrowing the competitive pool.

Other Challenges

Integration with Legacy Command‑and‑Control Networks

Many armed units still rely on aged C2 infrastructure that cannot readily ingest high‑volume intercepted data. Retrofitting these systems demands custom middleware, extending project timelines and increasing integration risk. Vendors that fail to offer seamless adapters may lose contracts to more adaptable rivals.

MARKET RESTRAINTS

High Acquisition Costs and Limited Budget Flexibility

Advanced interception platforms often exceed the standard procurement ceiling for many defense departments, especially those operating under constrained fiscal cycles. Decision‑makers must balance the immediate tactical advantage against long‑term sustainment expenses, which can result in postponed purchases or scaled‑down configurations. This cost sensitivity acts as a brake on rapid market expansion.

MARKET OPPORTUNITIES

AI‑Enabled Threat Attribution Services

There is a growing appetite for turnkey solutions that not only capture Wi‑Fi traffic but also attribute malicious actors using machine‑learning models trained on global threat feeds. Providers that can bundle interception hardware with cloud‑based analytics stand to capture a premium segment of the Tactical Wi‑Fi Interception System Market, especially as joint‑operations demand rapid, actionable intelligence.

Tactical Wi-Fi Interception System Market Trends

Growing Adoption of Mobile‑Deployed Interception Platforms

The past two years have seen operators prioritize systems that can be mounted on vehicles, UAVs, or carried by a single soldier. This shift reflects the demand for rapid repositioning in contested urban environments, where fixed installations become liabilities once the battle line moves. Vendors responding to this need are engineering lighter chassis, extending battery life, and embedding ruggedized antenna arrays that survive harsh weather. Procurement offices are revising tender criteria to award points for “deployment agility,” prompting a noticeable uptick in contracts for man‑portable and airborne solutions. For buyers, the trend translates into greater operational reach without additional logistical tail, while suppliers must balance performance against the cost pressures of scaling low‑volume production.

Other Trends

Regulatory Tightening and Export Controls

National security agencies across major economies have intensified scrutiny over the transfer of Wi‑Fi interception technology. Recent amendments to export‑control statutes now require end‑user certification for every system classified under “national security‑tier.” The consequence is a contraction of the traditional third‑party distribution channel; manufacturers are establishing in‑country subsidiaries or partnering with local defense firms to retain market access. This regulatory climate also encourages greater investment in domestically sourced components, reducing reliance on foreign supply chains that might be vulnerable to interdiction. Companies that can certify compliance early gain a competitive edge, while those lagging may face prolonged certification cycles that delay delivery schedules.

Integration of AI‑Driven Signal Analytics

Artificial‑intelligence algorithms are increasingly embedded within interception suites to automate the decryption and classification of captured traffic. Real‑time machine‑learning models can flag anomalous device behavior, prioritize high‑value targets, and even predict the next frequency hop, thereby shrinking the analyst’s response window from minutes to seconds. This capability has spurred a wave of strategic alliances between traditional hardware vendors and boutique AI firms, each seeking to offer a turnkey “intelligence‑as‑a‑service” proposition. From a business perspective, the fusion of AI with hardware creates recurring‑revenue opportunities through subscription‑based analytics platforms, while also raising questions about data sovereignty and the ethical management of harvested metadata.

COMPETITIVE LANDSCAPE

Key Industry Players

Tactical Wi‑Fi Interception System Market – Competitive Overview

Elbit Systems continues to dominate the tactical Wi‑Fi interception arena, leveraging its extensive defence portfolio and longstanding contracts with NATO members. The company’s flagship platform integrates passive spectrum scanning with an active exploitation suite, allowing field units to seize encrypted 802.11 traffic and deliver decoded payloads to central analysis nodes within minutes. This end‑to‑end capability has cemented Elbit’s position as the primary supplier for large‑scale military procurement programmes, especially in Europe and North America. Its financial muscle enables rapid iteration of firmware and the incorporation of emerging standards such as Wi‑Fi 6E, keeping the product line ahead of adversary counter‑measures. Consequently, the market’s structure is highly concentrated at the top, with a handful of defense contractors controlling the majority of high‑value contracts while smaller innovators compete on niche features and rapid‑deployment form factors.

Beyond the incumbent, a constellation of specialised firms injects diversity into the ecosystem. TheSpyPhone, Netline Communications Technologies, and NovoQuad Group each focus on man‑portable and covert solutions that prioritize low‑observable form‑factors for law‑enforcement operations. Sovereign Systems and NQ Defense have carved out niches in active‑exploitation modules, offering plug‑and‑play kits that can be mounted on UAV platforms. Companies such as Spectradome, Thespysolution, and PKI‑electronic supply component‑level encryption‑breakers and custom antenna arrays, enabling system integrators to tailor capabilities to regional regulatory constraints. This tiered landscape generates competitive pressure on pricing and accelerates feature differentiation, compelling the market leader to continuously broaden its portfolio while fostering a vibrant supply chain of agile, niche innovators.

List of Key Tactical Wi‑Fi Interception System Companies Profiled

- Elbit Systems

- Curtiss‑Wright

- TheSpyPhone

- Netline Communications Technologies

- NovoQuad Group

- Sovereign Systems

- NQ Defense

- TAR

- Shoghi

- Stratign

- Spectradome

- Thespysolution

- PKI‑electronic

- TrioSecure

- Ismallcell Biz

- Avnon Group

- Jenovice Cyber Labs

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Active Interception Systems are emerging as the preferred solution for mission‑critical operations.

|

| By Application |

|

Military and Defense drives the most sophisticated requirement set.

|

| By End User |

|

Law Enforcement Agencies value tactical systems for urban and counter‑terrorism operations.

|

| By Deployment Mode |

|

Man‑portable Systems are gaining traction for their flexibility in field operations.

|

| By Product Type |

|

National Security‑tier Systems dominate strategic procurement programmes.

|

Regional Analysis: Tactical Wi-Fi Interception System Market

Europe

European directives on electronic surveillance impose layered approval processes, compelling suppliers to certify equipment against both NATO standards and national export controls. This dual compliance framework accelerates product hardening while limiting entry for non‑EU players lacking local partnerships.

Operators increasingly favour modular architectures that allow rapid integration of AI‑driven anomaly detection. The shift reflects a broader demand for systems that can distinguish benign traffic from covert threat vectors without extensive manual tuning.

Military special‑operations units and border‑control agencies constitute the bulk of procurement, driven by the need to monitor contested airspace and urban environments where conventional surveillance proves inadequate.

A handful of legacy defense contractors dominate the market, yet emerging startups are gaining traction by offering low‑cost, software‑defined interceptors that leverage cloud‑native analytics.

North America

In North America, the Tactical Wi‑Fi Interception System Market is shaped by a blend of extensive federal research budgets and a thriving commercial ecosystem. U.S. defense agencies prioritize interoperable solutions that can be fielded across multiple branches, encouraging vendors to adopt open‑architecture standards. At the same time, private security firms experiment with portable interceptors for critical‑infrastructure protection, blurring the line between governmental and civilian demand. The region’s investment in advanced signal‑processing chips ensures that home‑grown products retain a performance edge, while partnerships with academic labs accelerate algorithmic breakthroughs. This dual‑track approach yields a dynamic supply chain capable of swift adaptation to emerging wireless threats.

Asia‑Pacific

Asia‑Pacific presents a contrasting landscape where rapid urbanization and expanding broadband footprints create fertile ground for covert wireless monitoring. Nations with sizable border tensions are allocating resources to develop indigenous interception capabilities, often through joint ventures with European firms to acquire proven technology. Meanwhile, the proliferation of 5G networks introduces new frequency bands that local vendors are eager to exploit, prompting a shift toward multi‑band sensors. Cultural emphasis on self‑reliance drives considerable investment in domestic R&D, yet export‑control regimes occasionally curb cross‑border technology transfer, shaping a market that is both ambitious and highly segmented.

South America

In South America, budgetary constraints temper the pace of acquisition, but strategic considerations compel governments to modernise their wireless surveillance arsenals. Regional cooperation agreements, particularly within Mercosur, foster joint procurement initiatives that spread costs and standardise capabilities across member states. Suppliers that can demonstrate cost‑effective, ruggedised solutions often secure multi‑year contracts, especially where terrain challenges demand equipment with extended operational endurance. The market is further influenced by rising awareness of illicit spectrum use by non‑state actors, nudging policymakers toward more proactive interception strategies.

Middle East & Africa

The Middle East & Africa region experiences heightened demand for Tactical Wi‑Fi Interception System Market solutions due to geopolitical volatility and the need to safeguard critical oil and gas infrastructure. Nations with substantial sovereign wealth funds allocate capital to acquire sophisticated interception platforms that can operate in harsh desert environments. African states, meanwhile, focus on counter‑terrorism applications, often relying on donor‑funded programs to introduce baseline capabilities. The prevailing challenge lies in balancing advanced technology adoption with the limited local technical talent pool, prompting a reliance on foreign contractors for system integration and training.

Report Scope

This market research report provides a comprehensive analysis of the Tactical Wi-Fi Interception System Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Tactical Wi-Fi Interception System Market?

-> Tactical Wi-Fi Interception System market will increase to USD 2182 million by 2034, reflecting a CAGR of 9.4%

Which key companies operate in Tactical Wi-Fi Interception System Market?

-> Key players include TheSpyPhone, Elbit Systems, Netline Communications Technologies, NovoQuad Group, Sovereign Systems, NQ Defense, TAR, Shoghi, Stratign, Spectradome, Thespysolution, PKI-electronic, TrioSecure, Curtiss-Wright, Ismallcell Biz, Avnon Group, Jenovice Cyber Labs.

What are the key growth drivers?

-> Key growth drivers include increasing demand for covert intelligence gathering by military and law‑enforcement agencies, rapid evolution of Wi‑Fi standards that create new interception opportunities, heightened cyber‑security threats prompting advanced signal capture solutions, and sustained government investment in specialized cybersecurity and surveillance technologies.

Which region dominates the market?

-> North America and Europe currently hold the largest shares due to extensive defense budgets and established procurement processes, while the Asia‑Pacific region is emerging fast driven by modernization programs.

What are the emerging trends?

-> Emerging trends include AI‑enhanced signal analysis, miniaturized man‑portable and UAV‑mounted interception platforms, and advanced decryption techniques targeting newer Wi‑Fi security protocols.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...