Automotive High-Side FET Drivers Market Insights

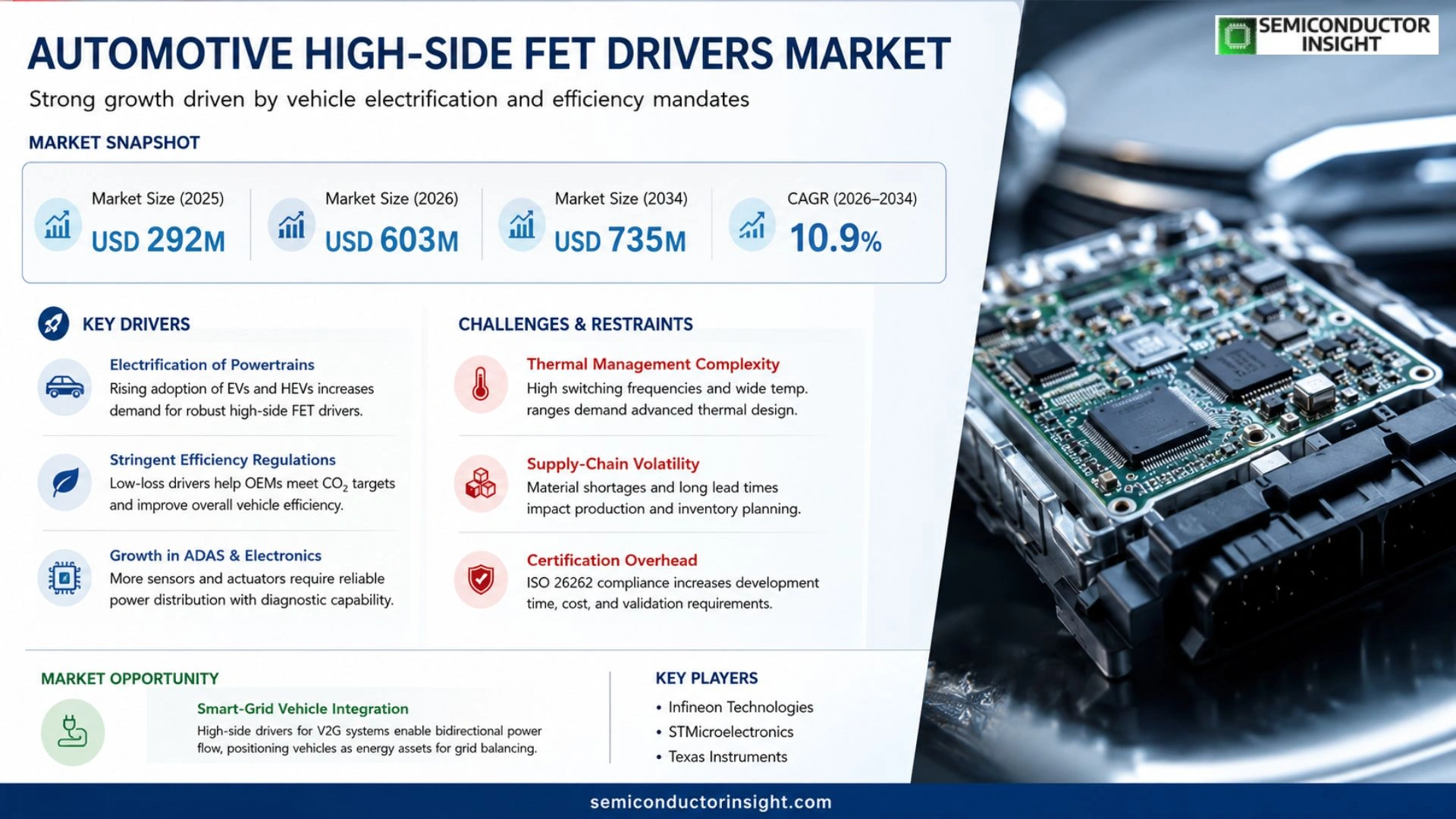

Global Automotive High-Side FET Drivers market size was valued at USD 292 million in 2025 and will increase from USD 603 million in 2026 to USD 735 million by 2034, exhibiting a CAGR of 10.9 % during the forecast period.

Automotive High‑Side FET Drivers are automotive‑grade integrated circuits that drive high‑side power transistors, converting control signals into stable gate‑drive waveforms while embedding protection and diagnostics to ensure efficient switching, functional safety, and long‑term reliability across vehicle power systems.

The market expands because vehicle electrical architectures are becoming more complex, safety standards such as ISO‑26262 demand higher integration of protection features, and OEMs seek reduced system losses through consolidated driver solutions; consequently suppliers that provide fast design‑in support and long‑life qualification tend to capture pricing discipline.

MARKET DRIVERS

Electrification of Powertrains

The shift toward electric and hybrid drivetrains compels OEMs to adopt robust high‑side FET drivers that can tolerate high voltage swings while maintaining tight switching control. Automotive High‑Side FET Drivers Market players are benefitting from design‑in opportunities as manufacturers re‑engineer inverter modules for battery‑electric vehicles (BEVs). This transition unlocks volume growth because each powertrain now relies on multiple driver ICs to manage motor phases and ancillary loads.

Stringent Efficiency Regulations

Regulatory frameworks that target lower CO₂ emissions force vehicle designers to optimise every watt of power loss. High‑side FET drivers with low on‑resistance and fast transition times directly reduce conduction and switching losses, helping power‑train packages meet mandated efficiency thresholds. Consequently, suppliers that can demonstrate measurable energy‑saving benefits are seeing accelerated qualification cycles.

➤ “Design engineers cite the ability to shrink inverter footprints by up to 15 % when using integrated high‑side drivers, a factor that directly influences vehicle packaging and cost.”

Beyond regulatory pressure, the rise of ADAS and autonomous functions is inflating demand for reliable power distribution to sensors and actuators. Integrated high‑side solutions simplify board layouts, cut BOM count, and improve diagnostic capability,attributes that are increasingly valued in safety‑critical subsystems.

MARKET CHALLENGES

Thermal Management Complexity

High‑side FET drivers operating in automotive environments must dissipate heat generated by frequent switching under wide temperature ranges. Integrators often face trade‑offs between driver performance and the need for auxiliary cooling, which can erode the cost advantage of integrated solutions. Engineers must therefore allocate additional silicon area for heat‑spreading structures, raising design overhead.

Other Challenges

Supply‑Chain Volatility

The semiconductor ecosystem continues to feel the impact of raw‑material shortages and geopolitical tensions. Lead times for silicon wafers and packaging substrates have stretched, prompting manufacturers to hold higher safety stocks. This volatility hampers just‑in‑time production models that many automotive firms rely upon.

MARKET RESTRAINTS

Certification Overhead

Achieving functional safety compliance (ISO 26262) for high‑side drivers adds a layer of engineering effort that can delay product launches. Each new driver family must undergo rigorous failure‑mode analysis and tool‑qualification, processes that increase development budgets and can deter smaller suppliers from entering the space.

MARKET OPPORTUNITIES

Smart‑Grid Vehicle Integration

The emerging concept of vehicles as mobile energy storage units creates a niche for high‑side drivers that can interface with vehicle‑to‑grid (V2G) systems. Drivers capable of handling bidirectional power flow while maintaining isolation requirements are positioned to capture contracts from utilities seeking to leverage fleets for grid balancing.

Automotive High-Side FET Drivers Market Trends

Integration of Protection and Diagnostics Fuels Design Consolidation

The latest vehicle architectures demand driver ICs that do more than toggle a transistor. Engineers increasingly select high-side FET drivers that embed over‑voltage shutdown, short‑circuit detection, and temperature monitoring within a single silicon block. This consolidation trims board‑level component counts, reduces wiring complexity, and shortens the validation loop for functional‑safety compliance. Suppliers that deliver a tightly integrated protection suite are gaining design‑in approvals faster, which in turn reinforces their pricing leverage on high‑volume platforms.

Other Trends

Capacity Utilization and Margin Dynamics

In 2025 the industry’s capacity utilization settled around 66 %, while gross margins hovered near 48 %. The margin profile reflects the premium that OEMs attach to reliability guarantees and the economies of scale achieved through platform reuse. As manufacturers refine tape‑out strategies and standardize verification flows, the utilization curve is expected to climb modestly, allowing margin expansion without sacrificing the cost discipline demanded by mass‑market vehicles.

Electrification Pressure Elevates Driver Criticality

Rising electrical loads in both passenger and commercial fleets are reshaping the role of high‑side drivers from peripheral support parts to central control nodes for body‑electronics, chassis systems, and power‑train modules. The shift forces OEMs to treat driver reliability as a system‑level determinant of vehicle uptime, prompting tighter collaboration with IC vendors during early development stages. Companies that align their qualification roadmaps with automotive program schedules are better positioned to lock in long‑term supply contracts, thereby insulating themselves from incremental price erosion on high‑volume programs.

COMPETITIVE LANDSCAPE

Key Industry Players

Automotive High‑Side FET Drivers: Competitive Overview

Infineon Technologies commands the top tier of the market, leveraging its extensive automotive‑grade silicon portfolio and a reputation for rigorous functional‑safety qualification. The company’s ability to integrate high‑voltage protection, diagnostics and charge‑pump architectures into a single die enables OEMs to reduce bill‑of‑materials while meeting tightening ISO‑26262 targets. Infineon’s deep foothold in European and Asian passenger‑car programs translates into stable pricing power, especially on high‑volume platforms where marginal cost improvements are critical. Its strategic collaborations with tier‑one suppliers further cement its position as the de‑facto reference source for multi‑channel high‑side drivers used in body‑control modules and chassis‑level power distribution.

Beyond the market leader, a cohort of mid‑size and niche specialists is reshaping the value chain. STMicroelectronics and Texas Instruments each offer differentiated analog‑front‑end expertise that appeals to manufacturers seeking higher integration of PWM control and fault‑logging. ROHM and Renesas focus on compact, single‑channel solutions optimized for electric‑vehicle gateway units, while Diodes Incorporated emphasizes cost‑effective single‑channel families for commercial‑vehicle lighting. Fuji Electric, onsemi and Microchip provide strong North‑American support networks, which is increasingly decisive as U.S. OEMs demand rapid design‑in cycles. Japanese heavyweight Toshiba and Korean champion Samsung Electro‑Mechanics add depth in high‑voltage packaging, whereas Chinese firms such as Shanghai Silicon Industry Group and Shennan Circuits compete on price for emerging market entrants. Collectively, these players intensify competition on feature sets, lead‑time and long‑term supply assurance.

List of Key Automotive High‑Side FET Drivers Companies Profiled

- Infineon Technologies

- STMicroelectronics

- Texas Instruments

- ROHM Semiconductor

- Renesas Electronics

- Diodes Incorporated

- Fuji Electric

- onsemi

- Microchip Technology

- Toshiba

- Shanghai Silicon Industry Group

- Shennan Circuits

- NXP Semiconductors

- Analog Devices (Maxim Integrated)

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Single‑Channel Drivers

|

| By Application |

|

Power‑distribution modules

|

| By End User |

|

OEMs

|

| By Voltage Level |

|

24 V Domain Drivers

|

| By Package Form |

|

Other Advanced Packages

|

Regional Analysis: Automotive High-Side FET Drivers Market

North America

Recent logistics disruptions have prompted North American manufacturers to diversify sourcing, favoring domestic fabs that can guarantee tighter lead times for high‑side drivers. This shift reduces exposure to geopolitical shocks and aligns inventory practices with just‑in‑time production philosophies.

Major OEMs are standardizing high‑side FET drivers across multiple vehicle families to streamline software validation. The resulting platform commonality accelerates rollout of hybrid and fully electric models while lowering unit costs.

Upcoming emissions standards in California and Quebec place explicit efficiency targets on power‑train components, driving engineers to select drivers with lower on‑resistance and faster switching capabilities.

The rise of 48‑volt mild‑hybrid architectures is creating a niche for compact, high‑current drivers that can be integrated without major redesign, expanding the addressable market beyond full‑electric platforms.

Europe

European manufacturers are responding to a tightly coordinated legislative agenda that couples CO₂ caps with mandatory fleet‑wide electrification milestones. The region’s strong emphasis on circular economy principles is prompting suppliers to develop recyclable driver modules, thereby differentiating premium brands. Collaborative research programs funded by the EU are accelerating the migration toward wide‑bandgap semiconductors, which promise higher thermal margins for demanding electric‑vehicle applications. As OEMs balance performance with cost, they are increasingly leveraging modular driver families that can be reused across multiple model lines, reinforcing Europe’s reputation for engineering efficiency.

Asia‑Pacific

Asia‑Pacific’s growth trajectory is anchored by rapid urbanization and government subsidies that favor electric mobility. The sheer volume of vehicle production in China, Japan, and South Korea translates into a sizable demand for high‑side drivers, yet the market is fragmented by diverse design standards. Domestic chipmakers are investing heavily in process innovation to achieve parity with Western fabs, aiming to capture a larger share of the automotive supply chain. Meanwhile, tier‑2 OEMs are experimenting with cost‑optimized driver topologies to serve price‑sensitive segments, creating a dual‑track market where premium and budget solutions coexist.

South America

In South America, market momentum is guided by emerging electric‑bus programs and nascent passenger‑car electrification policies. While total vehicle volumes remain modest, the focus on public‑transport electrification offers a gateway for the Automotive High‑Side FET Drivers Market to demonstrate value in high‑durability, temperature‑tolerant designs. Local assemblers are forming joint ventures with North American suppliers to gain access to advanced driver IP, a strategy that mitigates technology gaps while fostering regional expertise.

Middle East & Africa

The Middle East & Africa region is characterized by a strategic pivot toward renewable‑energy‑powered transportation, driven by ambitious national visions for carbon neutrality. Investment in charging infrastructure is prompting fleet operators to adopt electric trucks that rely on robust high‑side drivers capable of withstanding harsh climatic conditions. African markets, still in early adoption phases, are attracting pilot projects funded by multilateral institutions, which test driver reliability in rugged operating environments and lay the groundwork for broader market entry.

Report Scope

This market research report provides a comprehensive analysis of the Automotive High-Side FET Drivers Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Automotive High-Side FET Drivers Market?

-> Automotive High-Side FET Drivers market will increase from USD 603 million in 2026 to USD 735 million by 2034

Which key companies operate in Automotive High-Side FET Drivers Market?

-> Key players include STMicroelectronics, Infineon, Diodes Incorporated, ROHM, Renesas, Fuji Electric, Texas Instruments, Microchip, onsemi, and Toshiba.

What are the key growth drivers?

-> Key growth drivers include rising electrical content in vehicles, stricter functional‑safety and efficiency requirements, increasing complexity of power distribution architectures, and the need for integrated protection and diagnostics that reduce system losses and validation risk.

Which region dominates the market?

-> Asia‑Pacific dominates Automotive High-Side FET Drivers market, driven by large OEM volumes, extensive supplier ecosystems, and rapid electrification programs across China, Japan, and South Korea.

What are the emerging trends?

-> Emerging trends include higher integration of protection/diagnostic functions, shift toward multi‑channel high‑voltage solutions, platform‑level adoption across multiple vehicle generations, and longer program lifecycles that emphasize gross‑margin stability.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...