Seismic Accelerometers in Structural Health Monitoring (SHM) Market Insights

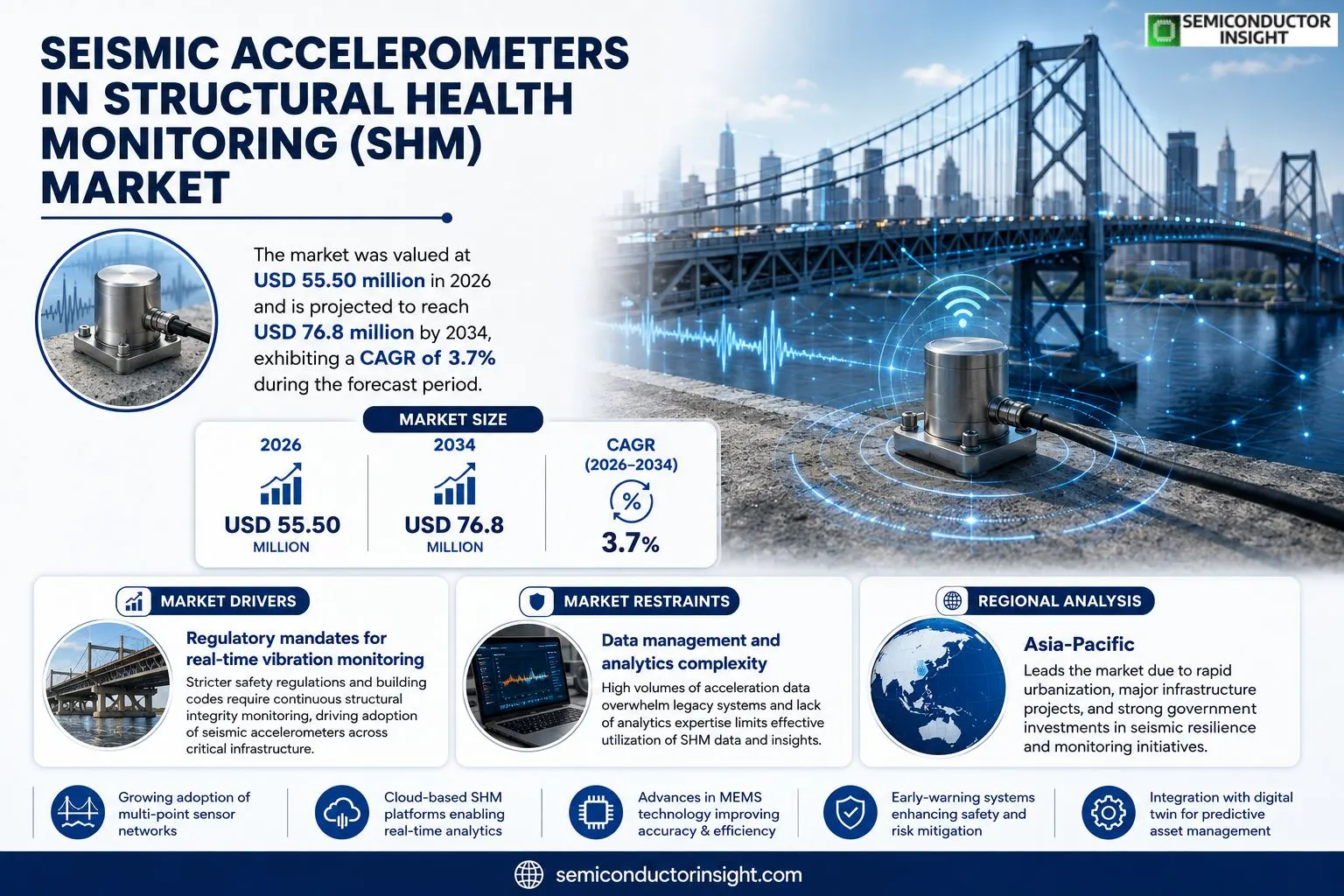

Seismic Accelerometers in Structural Health Monitoring (SHM) market was valued at USD 55.50 million in 2026 and is projected to reach approximately USD 76.8 million by 2034, exhibiting a CAGR of about 3.7 % during forecast period.

Seismic accelerometers used in SHM are engineering‑grade acceleration measurement instruments designed to capture dynamic response of civil structuressuch as bridges, high‑rise buildings, dams and tunnelsunder earthquake events and operational vibrations. Based on sensing principles including piezoelectric effects, capacitive variation or electromagnetic induction, se devices convert ground or structural acceleration into electrical signals and are offered in single‑axis or multi‑axis configurations to enable detailed vibration characterization.expanding need for resilient infrastructure monitoring, stricter safety regulations and growing investment in digital‑twin technologies are encouraging utilities and owners to deploy multi‑point sensor networks that provide continuous data for condition assessment, maintenance planning and early‑warning systems.

MARKET DRIVERS

Regulatory mandates for real‑time vibration monitoring

Governments and safety agencies across North America, Europe and parts of Asia have tightened building codes to require continuous structural integrity checks. This regulatory pressure pushes owners of bridges, high‑rise complexes and critical infrastructure toward deploying seismic accelerometers that can capture minute ground motions and structural responses. shift reduces risk of catastrophic failure and aligns with liability mitigation strategies.

Advances in sensor miniaturization and wireless networking

Recent breakthroughs in MEMS technology have cut size and power consumption of seismic accelerometers by more than 40 % while maintaining laboratory‑grade accuracy. Coupled with robust low‑power mesh protocols, installers can now field dense sensor arrays without extensive cabling, lowering installation costs and shortening project timelines. This technical evolution makes SHM solutions attractive to owners of older structures seeking cost‑effective retrofits.

➤ “Clients are willing to allocate up to 15 % of capital budgets for sensor networks that demonstrably extend asset life by 5‑7 years.”

When decision‑makers quantify financial upsidereduced downtime, lower maintenance spend and extended service life economic case for integrating seismic accelerometers becomes compelling. Moreover, ability to feed real‑time data into predictive algorithms creates a new revenue stream for service providers offering condition‑based maintenance contracts.

MARKET CHALLENGES

High upfront costs for comprehensive sensor deployments

Although unit pricing has fallen, a full‑scale implementation for a large bridge can still require a six‑figure investment in hardware, software licences and integration services. For owners operating under tight budget cycles, justifying this outlay against routine inspection budgets remains difficult, especially when tangible benefits are realized over a multi‑year horizon.

Or Challenges

Data management and analytics complexity

volume of high‑resolution acceleration data generated by modern networks can overwhelm legacy IT infrastructures. Organizations often lack expertise to cleanse, store and analyze se streams, leading to under‑utilisation of sensor investment. gap between data collection and actionable insight is a persistent obstacle.

MARKET RESTRAINTS

Limited skilled workforce for system integration

Deploying seismic accelerometers within existing structures demands a blend of civil engineering, instrumentation and wireless networking expertise. scarcity of professionals who can bridge se domains slows project rollout and raises labour costs, especially in emerging markets where training pipelines are still developing.

MARKET OPPORTUNITIES

Growth of cloud‑based SHM platforms

Software vendors are rolling out subscription models that ingest accelerometer data directly into cloud dashboards, offering scalable analytics without on‑premise hardware. This shift lowers barrier to entry for smaller municipalities and private owners, creating a sizable untapped demand segment for Seismic Accelerometers in Structural Health Monitoring (SHM) market.

Seismic Accelerometers in Structural Health Monitoring (SHM) Market Trends

Shift Toward Integrated Calibration Services

Project owners and owners of critical infrastructure are increasingly treating seismic accelerometers as components of a service ecosystem rar than isolated hardware items. 2026 production figure of 28,074 units, combined with an average selling price of USD 2,165, illustrates a market that already extracts significant value from each sensor. Yet tender documents now demand traceable calibration records, periodic re‑validation, and remote diagnostics. This creates a revenue stream that is less sensitive to unit‑price pressure and more aligned with long‑term maintenance contracts. Suppliers that embed calibration, data‑quality monitoring, and field‑support into sales proposition can command higher gross margins, often in 30 %‑45 % range, while differentiating mselves from cost‑driven entrants.

Or Trends

Performance Differentiation Driven by Noise and Low‑Frequency Capability

Engineering‑grade specifications such as noise density and low‑frequency response now dominate purchasing decisions. Clients monitoring bridges, high‑rise buildings, or dams require ability to detect subtle stiffness changes, which only sensors with ultra‑low noise floors can reveal. Consequently, manufacturers emphasizing stringent end‑of‑line testing and batch‑to‑batch consistency are securing premium pricing, particularly for multi‑axis units that maintain linearity across axes. competitive advantage is no longer breadth of SKU catalogues but demonstrable stability of measurement signal over months and years, a factor that directly influences post‑event assessment reliability.

Supply‑Chain Bottlenecks Center on Calibration Capacity

While component availability remains adequate, true throughput limitation resides in calibration and quality‑assurance operations. A single production line typically delivers between 500 and 5,000 calibrated units annually, depending on rigor of testing protocols. Scaling up refore requires parallel calibration stations and disciplined workflow planning rar than simply increasing component inventories. Companies that have invested in modular test rigs and automated drift‑correction procedures can align delivery schedules with fragmented, project‑driven demand pattern observed across SHM landscape, reby preserving margin integrity and reducing lead‑time variance.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive Positioning of Seismic Accelerometer Suppliers in SHM

Kinemetrics continues to dominate high‑performance segment, leveraging its long‑standing reputation for field‑validated force‑balance sensors. Its portfolio blends tri‑axial designs with robust temperature compensation, allowing customers to deploy units on bridges and high‑rise structures with minimal recalibration cycles. company’s vertically integrated calibration laboratory and documented traceability chain have become a decisive factor in public‑sector tenders, where data fidelity is scrutinized by engineering review boards. Guralp Systems Ltd, anor heavyweight, differentiates through an aggressive focus on low‑noise piezoelectric accelerometers that excel in capturing subtle modal shifts in masonry dams. By pairing its sensors with proprietary acquisition software, Guralp offers a turnkey monitoring solution that reduces integration risk for owners managing large‑scale infrastructure portfolios. Nanometrics rounds out upper tier by pushing MEMS technology into seismic domain, delivering compact units with an expanded dynamic range that can handle both ambient vibration monitoring and strong‑motion events without sacrificing linearity.Beyond marquee names, several specialized firms contribute depth to market. PCB Piezotronics has built a niche around high‑frequency capacitive sensors suited for vibration‑critical industrial facilities, while its broad distribution network ensures rapid replacement parts for legacy installations. R‑Sensors and Solgeo focus on cost‑effective piezoresistive models that appeal to emerging markets where budget constraints drive procurement decisions. Companies such as REF TEK and HBK Dytran emphasize rugged packaging for tunnel and underground applications, where moisture ingress and mechanical shock are persistent challenges. European players like Bruel & Kjaer and Metrix Instrument provide calibrated bundles that integrate seamlessly with regional data‑management platforms, reinforcing ir standing in EU public‑works arena. overall competitive picture is refore characterized by a blend of premium, engineering‑centric providers and value‑oriented manufacturers, each targeting distinct procurement philosophies across SHM ecosystem.

List of Key Seismic Accelerometers in Structural Health Monitoring Companies Profiled

- Kinemetrics

- Guralp Systems Ltd

- Nanometrics

- GeoSIG

- REF TEK

- Safran

- Tokyo Sokushin Co., Ltd

- R‑Sensors

- Solgeo

- GEObit Instruments

- PCB Piezotronics

- Wilcoxon

- HBK Dytran

- Bruel and Kjaer

- Meggitt Sensing Systems

- Metrix Instrument

- DJB Instruments

- Columbia Research Laboratories, Inc.

- IMV Corporation

- Honeywell

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Piezoelectric Accelerometer Sensors

|

| By Application |

|

Bridges

|

| By End User |

|

Government Agencies

|

| By Technology |

|

Force‑Balance Technology

|

| By Performance |

|

Low Noise

|

Regional Analysis: Seismic Accelerometers in Structural Health Monitoring (SHM) Market

North America

Federal safety codes in United States now require continuous vibration monitoring for structures exceeding certain height thresholds, prompting owners to install dense arrays of seismic accelerometers. Parallelly, Canadian provinces have introduced performance‑based design guidelines that reward proactive monitoring with reduced inspection fees, creating a fiscal incentive for adoption.

region benefits from early‑stage integration of edge‑computing chips within accelerometers, allowing real‑time anomaly detection without reliance on central servers. This capability is especially valued in remote oil‑field platforms where cellular connectivity is intermittent.

Transportation authorities, utility operators, and commercial real‑estate owners constitute primary user base. Each segment leverages accelerometer data differentlytransport agencies to verify bridge fatigue limits, utilities to detect pipeline vibration signatures, and property owners to certify building resilience for insurance underwriting.

Market incumbents are defending territory through extensive service contracts, while newcomers focus on modular sensor kits that can be retrofitted onto legacy structures, intensifying pressure on price points and accelerating innovation cycles.

Europe

European nations exhibit a fragmented yet technically sophisticated market for seismic accelerometers in SHM. Germany’s engineering consortiums prioritize sensor standardisation across rail networks, while United Kingdom leverages post‑Brexit regulatory flexibility to trial novel data‑fusion platforms. Funding from European Union’s Horizon programmes fuels cross‑border research, encouraging manufacturers to align hardware specifications with pan‑EU data‑exchange frameworks. result is a market where interoperability eclipses sheer scale, prompting vendors to adopt open APIs to remain competitive across continent.

Asia‑Pacific

Rapid urbanisation in Asia‑Pacific reshapes demand dynamics for structural health monitoring. Governments in China, Japan, and India channel substantial public‑investment into seismic resilience, yet region’s procurement culture favours cost‑effective, high‑volume solutions. Local OEMs respond with ruggedized, low‑maintenance accelerometer designs that tolerate extreme wear and logistical constraints. Meanwhile, megacities experiment with crowd‑sourced vibration data, blending low‑cost citizen sensors with professional arrays, a hybrid approach that could redefine scaling strategies for broader market.

South America

In South America, seismic risk awareness is heightened by Andean tectonic belt, prompting Brazil and Chile to embed accelerometer networks in key infrastructural assets. Budgetary constraints drive a preference for turnkey monitoring services, where sensor hardware and analytics are bundled under long‑term contracts. This model reduces upfront capital outlays and aligns vendor incentives with sustained performance, encouraging a shift toward outcome‑based pricing structures.

Middle East & Africa

Middle East & Africa region presents a juxtaposition of high‑profile mega‑projects and emerging markets with limited monitoring experience. In Gulf, ultra‑tall skyscrapers incorporate accelerometers as part of integrated building‑management systems to satisfy investor‑driven performance criteria. Conversely, sub‑Saharan nations are beginning to recognise value of monitoring for water‑infrastructure resilience, spurring pilot deployments funded by international development agencies. Vendor strategies refore balance high‑margin, bespoke solutions for affluent clients with scalable, low‑cost kits for nascent markets.

Report Scope

This market research report provides a comprehensive analysis of Seismic Accelerometers in Structural Health Monitoring (SHM) Market , covering forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping industry.

Key focus areas of report include:

- Market Overview: report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including ir product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure accuracy and reliability of insights presented.

FREQUENTLY ASKED QUESTIONS:

What is current market size of Seismic Accelerometers in Structural Health Monitoring (SHM) Market?

-> Seismic Accelerometers in Structural Health Monitoring (SHM) Market was valued at USD 55.50 million in 2026 and is expected to reach USD 71.43 million by 2032, at a CAGR of 3.7% during forecast period.

Which key companies operate in Seismic Accelerometers in Structural Health Monitoring (SHM) Market?

-> Key players include Kinemetrics, Guralp Systems Ltd, Nanometrics, GeoSIG, REF TEK, Safran, Tokyo Sokushin Co., Ltd, R‑Sensors, Solgeo, GEObit Instruments, PCB Piezotronics, Wilcoxon, HBK Dytran, Brüel & Kjær, Meggitt Sensing Systems, Metrix Instrument, DJB Instruments, Columbia Research Laboratories Inc., IMV Corporation, and Honeywell.

What are main growth drivers for this market?

-> Growth is driven by increasing demand for real‑time structural safety monitoring, stricter seismic‑resilience regulations, expanding infrastructure projects in emerging economies, rising awareness of asset‑performance management, and advances in low‑noise, multi‑axis sensor technologies.

Which region holds largest market share?

-> Asia-Pacific currently holds largest share, propelled by rapid urbanization, extensive bridge and high‑rise construction, and heightened earthquake‑risk mitigation programs across China, Japan, and India.

What emerging trends are shaping market?

-> Emerging trends include integration of IoT connectivity for remote calibration, adoption of MEMS‑based miniaturized accelerometers, AI‑enabled data analytics for early damage detection, and development of standardized modular SHM platforms that combine sensor, edge‑processing, and cloud services.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...