High-speed Quantum Entropy Source Chip Market Insights

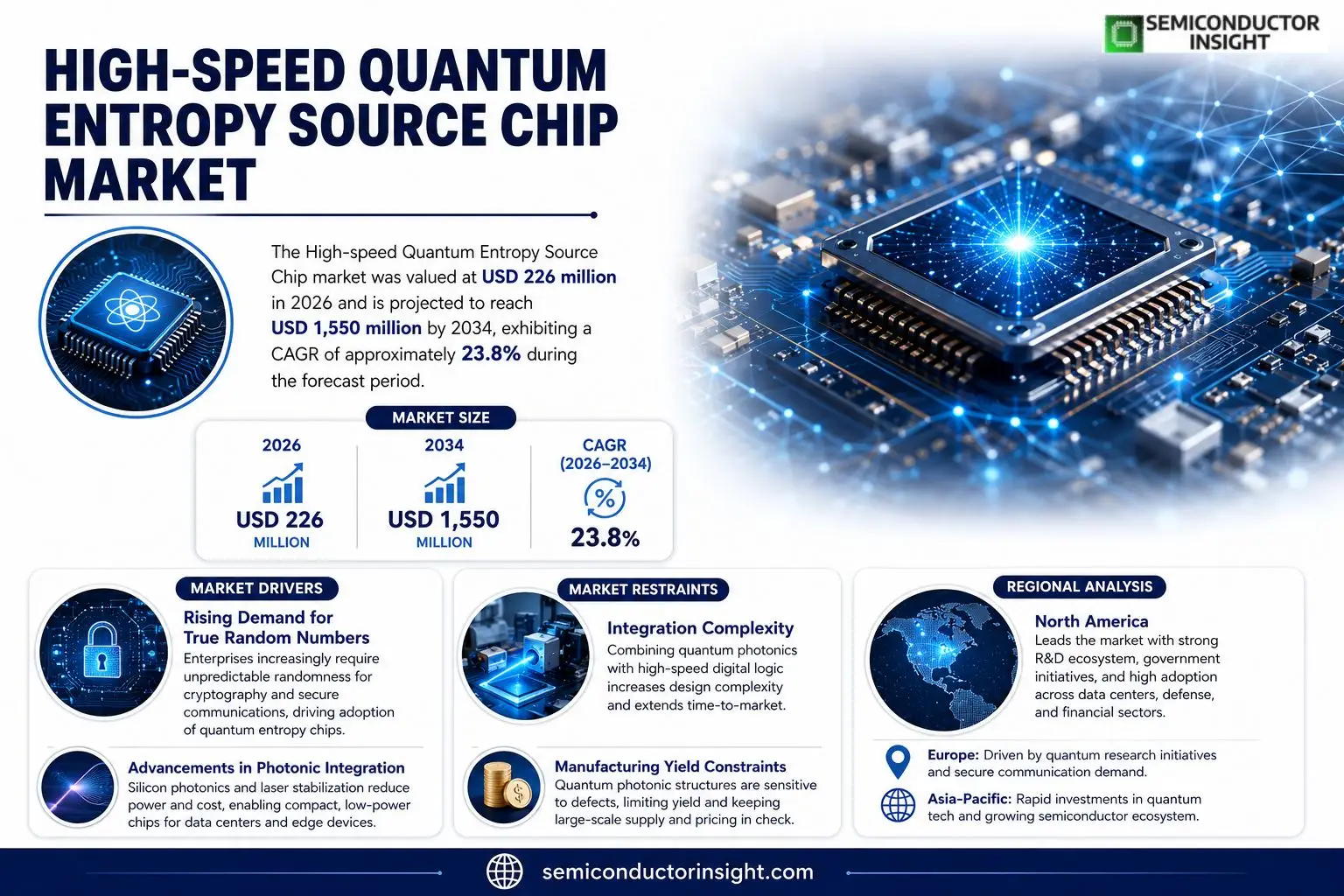

High-speed Quantum Entropy Source Chip market size was valued at USD 226 million in 2026 and is projected to reach USD 1,550 million by 2034, exhibiting a CAGR of approximately 23.8 % during the forecast period.

High‑speed quantum entropy source chips are core devices that exploit intrinsic quantum randomnesssuch as photon fluctuations, vacuum noise or tunnelingto generate true random numbers at chip level. By converting rapid quantum events into high‑entropy bit streams through detection, conversion and post‑processing circuits, these chips provide provable randomness, non‑replicability and integration ease for cryptographic systems.The market expands because enterprises increasingly adopt quantum‑secure encryption for data‑center workloads, financial transactions and defense communications, while advances in photonic integration lower production costs and improve yield rates. Recent collaborations among leading foundries and quantum‑software firms further accelerate adoption, positioning the technology as a strategic asset for post‑quantum security architectures.

MARKET DRIVERS

Rising Demand for True Random Numbers

High-speed Quantum Entropy Source Chip Market is buoyed by enterprises that cannot tolerate deterministic pseudo‑random generators. Cryptographic protocols, especially those underpinning financial ledgers and national‑security communications, now require entropy that cannot be reproduced through algorithmic attacks. This shift compels system designers to embed dedicated quantum entropy generators directly on silicon, creating a clear pull on chip suppliers.

Advancements in Photonic Integration

Recent breakthroughs in silicon‑photonic waveguides and on‑chip laser stabilization have lowered the power envelope of quantum entropy sources. Where early versions needed milliwatts of optical pump power, the latest designs operate at a fraction of that, unlocking form‑factor possibilities for data‑center cards and edge routers. Companies that can translate these photonic gains into volume‑ready CMOS processes are positioning themselves as preferred partners for security‑critical OEMs.

➤ Clients are willing to pay a premium for chips that guarantee non‑repeatable randomness, turning what was once a niche component into a strategic differentiator.

The convergence of tighter security regulations and the commercial availability of low‑latency quantum entropy cores means that procurement cycles are shortening. Vendors that can certify compliance while delivering sub‑nanosecond entropy extraction are likely to capture a disproportionate share of upcoming contracts.

MARKET CHALLENGES

Integration Complexity

Embedding a quantum entropy source alongside high‑speed digital logic demands precise thermal management and optical alignment. Design teams often confront a learning curve when reconciling photonic layout rules with traditional ASIC floor‑planning. The result is longer time‑to‑market for first‑generation products and higher engineering overhead for customers.

Other Challenges

Bullet Point Title

Cost Sensitivity – While premium security budgets exist, many end‑users still evaluate total cost of ownership. The added material cost of specialty waveguides and the need for calibrated testing suites can deter adoption in price‑conscious segments such as consumer IoT.

MARKET RESTRAINTS

Manufacturing Yield Constraints

Quantum entropy chips rely on defect‑free photonic structures; even a single scattering site can degrade entropy quality. Current fab lines report yields that lag behind conventional CMOS baselines, which translates into limited supply for large‑scale deployments. Until process engineers achieve wafer‑level consistency, volume pricing will remain modest.

Regulatory Uncertainty

International standards for quantum‑derived randomness are still evolving. Some jurisdictions treat quantum entropy sources as regulated cryptographic components, imposing certification timelines that can stall product launches. Companies must monitor legislative drafts to avoid surprise compliance costs.

MARKET OPPORTUNITIES

Emerging Applications in Secure Communications

Telecom operators upgrading to 6G‑grade encryption are scouting for chips that can generate entropy at line‑rate speeds. The ability to embed a quantum source directly into base‑station ASICs eliminates the need for external RNG modules, reducing both latency and attack surface. This creates a sizable niche for suppliers that can certify end‑to‑end security chains.

Edge AI and Quantum‑Ready Devices

Edge AI accelerators are beginning to incorporate secure boot and model‑obfuscation techniques that require high‑entropy seeds. As manufacturers push AI workloads to the periphery, the demand for compact, low‑power quantum entropy chips that can be co‑fabricated with AI ASICs is set to rise. Early entrants that align their roadmaps with AI silicon partners will capture this cross‑segment growth.

High-speed Quantum Entropy Source Chip Market Trends

Escalating Adoption in Data‑Center Security

High-speed Quantum Entropy Source Chip Market has moved from a niche segment to a core component of modern data‑center architectures. Revenue climbed from $226 million in 2026 to an estimated $1,001 million by 2032, implying an average yearly increase near 24 percent. This ascent is anchored in the chips’ ability to deliver provable randomness at gigabit‑per‑second rates, a prerequisite for encrypting the massive traffic flowing through hyperscale facilities. In 2026, the sector shipped roughly 29,000 units at an average price of $8,560, while maintaining a 95 percent capacity utilisation and a gross margin exceeding 50 percent. Customers such as cloud providers and financial exchanges are favouring these devices because they eliminate the uncertainty associated with traditional pseudo‑random generators, thereby tightening compliance with emerging cyber‑security standards.

Other Trends

Quantum‑Enhanced Encryption Gains Traction

The push toward post‑quantum cryptography has turned High-speed Quantum Entropy Source Chip Market into a strategic frontier for firms seeking future‑proof protection. By exploiting photon‑level fluctuations and vacuum noise, the chips generate entropy that cannot be reproduced by any classical algorithm, a characteristic that aligns with upcoming regulatory frameworks on data sovereignty. Enterprises are integrating these chips directly into hardware security modules, reducing the latency introduced by off‑chip randomness sources. As a result, the adoption curve is steepening in sectors where latency penalties translate into tangible revenue loss, such as high‑frequency trading and real‑time analytics. The operational advantagelowered error rates in key‑distribution protocolscreates a compelling business case for replacing legacy RNGs with quantum‑grade alternatives.

Competitive Landscape Consolidates Around Specialized Players

Concentration among manufacturers is sharpening, with a handful of firmsXanadu, PsiQuantum, TuringQ Co., and several leading Chinese entrantscapturing the majority of 2026 sales. These companies differentiate themselves through proprietary photonic integration processes that shrink chip footprints while preserving terabit‑scale output. The high margin environment (over 50 percent) affords sustained investment in R&D, which fuels incremental performance gains and expands the addressable address space for security‑critical applications. Smaller players find it increasingly difficult to achieve the scale needed for 95 percent capacity utilisation, prompting a wave of strategic alliances and joint‑development agreements. For investors, the evolving competitive matrix signals a shift from pure technology licensing toward end‑to‑end solution provisioning, a transition that reshapes revenue models across High-speed Quantum Entropy Source Chip Market.

COMPETITIVE LANDSCAPE

Key Industry Players

High‑speed Quantum Entropy Source Chip Market – Competitive Overview

Among the segment’s incumbents, Xanadu commands the largest share, leveraging its vertically integrated photonic platform to deliver entropy chips that combine vacuum‑fluctuation detection with on‑chip post‑processing. The company’s ability to scale manufacturing through partnerships with major foundries has translated into a capacity utilization rate north of 95 % and a gross margin that comfortably exceeds 50 %. This financial strength allows Xanadu to invest heavily in ASIC‑level integration, shortening time‑to‑market for customers in data‑center encryption and post‑quantum key distribution. The broader market structure is oligopolistic: a handful of well‑capitalized firms dominate high‑volume orders, while a second tier of specialist suppliers targets niche applications such as quantum‑secure financial systems or defense‑grade communications. The concentration of revenue in the top five creates high barriers to entry, yet the rapid evolution of photonic foundry services continues to open modest pockets for new entrants that can demonstrate a differentiated entropy‑generation mechanism.Beyond the lead, a constellation of niche innovators enriches the competitive fabric. PsiQuantum’s focus on quantum‑tunneling entropy sources differentiates its product line by delivering sub‑nanosecond latency, a trait prized by ultra‑low‑latency trading platforms. TuringQ Co.,Ltd. and Hefei Guizhen Chip Technology Co.,Ltd. specialize in photon‑shot‑noise chips optimized for integration with existing silicon‑photonic processors, enabling seamless adoption by semiconductor OEMs. Beijing QBoson Quantum Technology Co.,Ltd. and QuiX Quantum have secured strategic alliances with academic consortia, feeding a pipeline of custom‑design services for research‑intensive customers. Smaller firms such as Quandela, Photonic, C*Core Technology Co.,Ltd., Anhui Qasky Quantum Technology Co.,Ltd., and QuantumCTek Co.,Ltd. occupy distinct market nichesranging from hyperspectral entropy extraction to ruggedized chips for field‑deployed encryption hardware. Their collective activity fuels incremental innovation, pressuring incumbents to broaden portfolio breadth and accelerate roadmap execution.

List of Key High‑speed Quantum Entropy Source Chip Companies Profiled

- Xanadu

- PsiQuantum

- TuringQ Co.,Ltd.

- Hefei Guizhen Chip Technology Co., Ltd.

- Beijing QBoson Quantum Technology Co.,Ltd.

- QuiX Quantum

- Quandela

- Photonic

- C*Core Technology Co., Ltd.

- Anhui Qasky Quantum Technology Co., Ltd.

- QuantumCTek Co., Ltd.

- ID Quantique

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Vacuum‑fluctuation source is frequently highlighted as the leading type because it delivers the most intrinsic randomness and aligns well with high‑speed detection architectures.

|

| By Application |

|

Quantum key distribution emerges as the dominant application due to its reliance on truly random numbers for secure key generation.

|

| By End User |

|

Data center operators lead this segment as they seek scalable security primitives for massive compute workloads.

|

| By Integration Level |

|

System‑on‑chip solution is viewed as the leading integration approach because it consolidates entropy generation with processing logic.

|

| By Value Chain Position |

|

Photonic system providers dominate this dimension as they control the upstream technology that enables high‑quality entropy extraction.

|

Regional Analysis: High-speed Quantum Entropy Source Chip Market

North America

The United States combines federal research grants with private venture capital, nurturing a pipeline that moves from academic proof‑of‑concept to commercial silicon chips. Defense‑related procurement channels encourage rigorous testing, while the burgeoning fintech sector pressures vendors to deliver latency‑critical entropy solutions. This dual‑track funding sustains a steady flow of product iterations and fosters cross‑industry collaborations.

Canada’s quantum thrust benefits from coordinated provincial incentives, especially in Ontario and Quebec, where research parks host joint ventures between chip manufacturers and cryptographic start‑ups. The emphasis on low‑temperature silicon photonics aligns with a national strategy to position Canada as a supplier of secure hardware for North‑American data centers.

Financial services, cloud providers, and defense contractors dominate demand, each requiring entropy sources that can sustain gigahertz‑scale data streams without sacrificing statistical quality. The market’s architecture trends toward integrating entropy modules directly onto ASICs, a shift accelerated by the need for hardware‑based randomness in secure enclave designs.

NIST’s forthcoming randomness‑generation guidelines and the U.S. Department of Energy’s roadmap for quantum‑ready hardware are shaping product specifications. Early alignment with these standards affords manufacturers a competitive moat, as certification becomes a prerequisite for government and high‑value commercial contracts.

Europe

Europe’s approach to the High‑speed Quantum Entropy Source Chip Market is defined by collaborative frameworks such as the Quantum Flagship, which pools resources across multiple nations to de‑risk large‑scale research. German and Dutch wafer fabs excel at precision optics, offering a complementary route to silicon‑photonics integration. However, fragmented funding mechanisms and stricter data‑privacy regulations temper the speed of commercial rollout. Companies that can navigate GDPR‑compliant data handling while delivering quantum‑grade entropy find niche opportunities in sectors like secure voting and automotive cybersecurity, where European standards remain particularly exacting.

Asia‑Pacific

Asia‑Pacific displays a paradox of rapid capability growth tempered by nascent design ecosystems. China’s investment in quantum‑grade silicon processes rivals that of its Western counterparts, yet domestic market adoption lags due to limited awareness of hardware‑rooted entropy benefits. Japan and South Korea, leveraging mature semiconductor supply chains, focus on embedding entropy sources within consumer electronics, a strategy that could unlock mass‑market demand. The region’s competitive advantage lies in scale; once product‑market fit is achieved, volume‑driven cost reductions could reshape pricing dynamics.

South America

South America remains an emerging frontier, with Brazil spearheading academic collaborations that explore low‑cost quantum randomness generators. The market is constrained by relatively modest venture capital availability and a lag in high‑volume fab infrastructure. Nevertheless, niche applicationsparticularly in fintech solutions serving under‑banked populationscreate modest but tangible demand for secure entropy. Export‑oriented manufacturers that can partner with North American firms may use the region as a low‑cost development hub, gradually building competency for broader market entry.

Middle East & Africa

The Middle East & Africa region presents a mixed picture of strategic intent and infrastructural limitation. United Arab Emirates’ sovereign wealth funds have earmarked capital for quantum‑technology incubators, signaling a long‑term vision for cryptographic hardware. Meanwhile, African markets exhibit high mobile‑penetration rates but lack the semiconductor ecosystems needed for on‑chip entropy production. Partnerships that enable technology transferespecially through university‑linked research in South Africacould seed a modest domestic market while providing a testing ground for climate‑resilient chip designs.

Report Scope

This market research report provides a comprehensive analysis of the High-speed Quantum Entropy Source Chip Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of High-speed Quantum Entropy Source Chip Market?

-> High-speed Quantum Entropy Source Chip Market was valued at USD 226 million in 2026 and is expected to reach USD 1001 million by 2032, growing at a CAGR of 23.8% during the forecast period.

Which key companies operate in High-speed Quantum Entropy Source Chip Market?

-> Key players include Xanadu, PsiQuantum, TuringQ Co., Ltd., Hefei Guizhen Chip Technology Co., Ltd., Beijing QBoson Quantum Technology Co., Ltd., QuiX Quantum, Quandela, Photonic, C*Core Technology Co., Ltd., Anhui Qasky Quantum Technology Co., Ltd., QuantumCTek Co., Ltd.

What are the key growth drivers?

-> Key growth drivers include rising demand for quantum‑grade random numbers in cryptographic systems, expansion of data‑center encryption, growth of post‑quantum security solutions, and increasing adoption in financial and defense information systems.

Which region dominates the market?

-> North America, particularly the United States, currently holds the largest market share, driven by strong investments in quantum computing and cybersecurity.

What are the emerging trends?

-> Emerging trends include integration of quantum entropy chips into quantum communication networks, miniaturization for on‑chip security modules, and convergence with AI‑enabled security platforms.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...