D-Sub Micro Connectors Market Insights

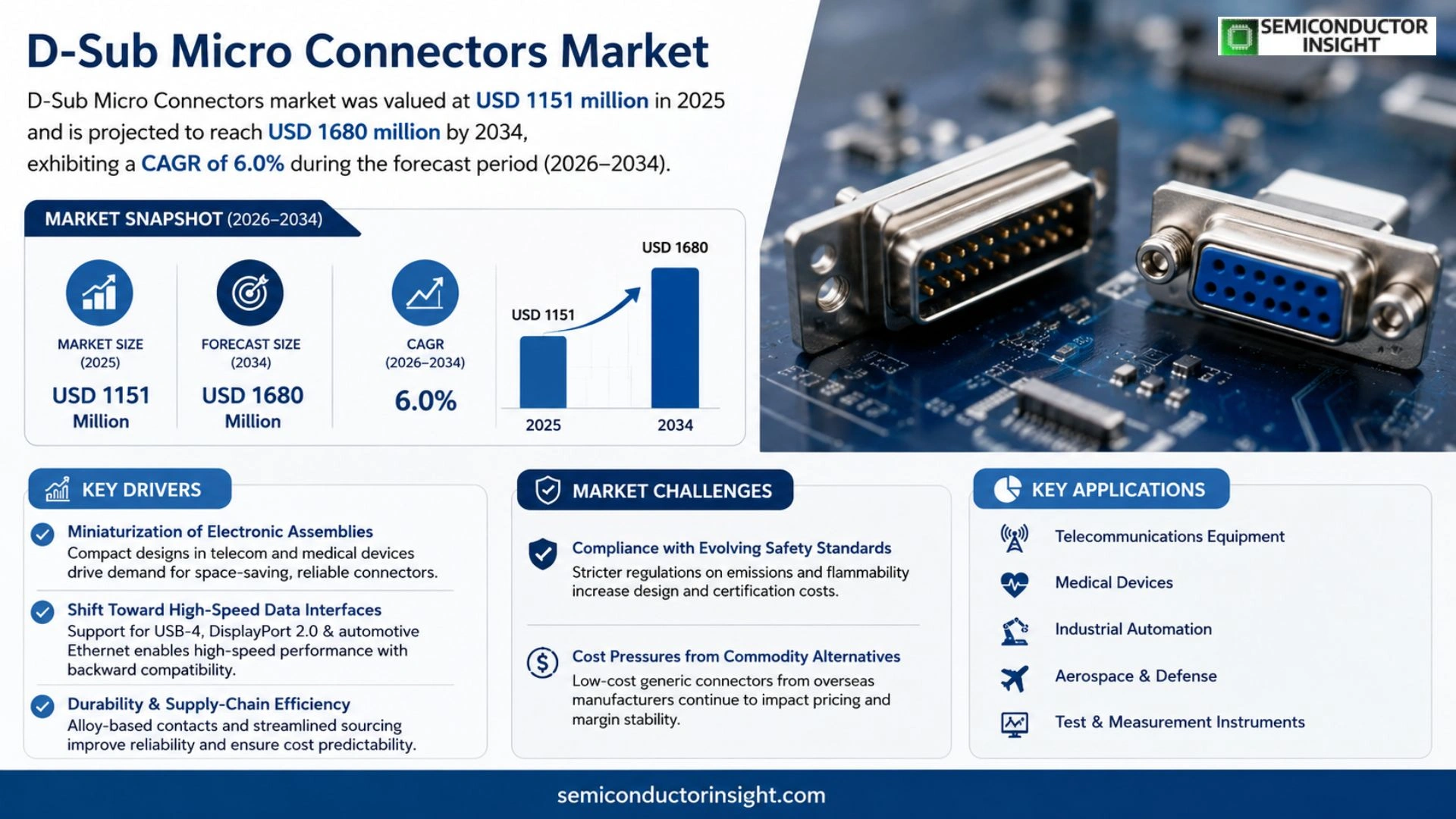

Global D-Sub Micro Connectors market was valued at USD 1151 million in 2025 and is projected to reach USD 1680 million by 2034, exhibiting a CAGR of 6.0% during the forecast period.

D-Sub Micro Connectors are a compact, high‑density variant of the classic D‑Subminiature connector family, designed with smaller geometry,roughly one‑third the size of a standard D‑Sub,and reduced contact spacing (typically 1.27 mm). They preserve the characteristic D‑shaped shell for secure mating while delivering space‑saving advantages for PCB‑constrained designs. Common configurations offer 9, 15 or 25 contacts and support through‑hole, panel or cable mounting; each contact handles about 1 A and metal shielding provides EMI resistance.

The market benefits from continued demand for reliable interconnects across aerospace, defense, industrial automation and telecommunications sectors, while ongoing miniaturisation pushes manufacturers toward tighter tolerances and higher‑precision contacts.

MARKET DRIVERS

Miniaturization of Electronic Assemblies

Customers in telecommunications and medical equipment are compressing board real‑estate to accommodate higher functionality. The trend toward smaller form factors forces designers to adopt D-Sub Micro Connectors that deliver reliable signal integrity within confined spaces. As a result, component suppliers are re‑engineering housings and contact materials to meet tighter pitch requirements while preserving durability.

Shift Toward High‑Speed Data Interfaces

Emerging protocols such as USB‑4, DisplayPort 2.0 and automotive Ethernet demand connectors capable of handling gigabit‑level throughput. D-Sub Micro Connectors, with their refined shielding and low‑loss geometry, have become a pragmatic bridge for legacy equipment needing an upgrade path without a full redesign. This convergence of performance and backward compatibility is prompting OEMs to specify micro‑scale D‑Sub parts across new product lines.

➤ Manufacturers that invest in alloy‑based contacts now command a pricing premium, reflecting the market’s willingness to pay for extended lifecycle reliability.

Supply‑chain rationalization also contributes to growth. Consolidated sourcing strategies enable buyers to secure inventory at predictable costs, while vendors benefit from economies of scale. The combined effect of design pressure, data‑rate acceleration, and procurement efficiency creates a solid foundation for D-Sub Micro Connectors Market to expand over the next several years.

MARKET CHALLENGES

Compliance with Evolving Safety Standards

Regulatory bodies across North America and Europe are tightening limits on electromagnetic emissions and material flammability. Manufacturers must redesign housings and certify each variant, which adds engineering cycles and testing expenses. Companies that cannot absorb these costs risk losing contracts with safety‑critical OEMs, especially in aerospace and rail sectors.

Other Challenges

Cost Pressures from Commodity Alternatives

Low‑cost generic connectors manufactured overseas continue to erode margin windows for premium D‑Sub Micro solutions. Customers often evaluate total cost of ownership, weighing the higher upfront price against projected downtime savings from a more robust connector. The balance between price competitiveness and performance assurance remains a delicate negotiation point.

MARKET RESTRAINTS

Limited Adoption in Ultra‑Low‑Power Devices

Battery‑operated wearables and IoT sensors prioritize ultra‑low‑power consumption and often bypass traditional D‑Sub form factors in favor of surface‑mount solutions. The intrinsic mechanical design of micro D‑Sub connectors, while robust, introduces a marginal parasitic loss that can be unacceptable for devices targeting multi‑year battery life. Consequently, this segment curtails broader market penetration.

MARKET OPPORTUNITIES

Customization for Industrial Automation

Industrial automation is transitioning toward modular, reconfigurable production lines. OEMs are seeking connectors that can be tailored to specific pin counts, plating options, and ruggedized shells. By offering a configurable platform, suppliers can capture incremental revenue from niche projects that require bespoke solutions, positioning themselves as strategic partners rather than mere component vendors.

Expansion into Emerging Automotive Segments

Electric‑vehicle platforms are integrating increasingly sophisticated driver‑assist modules and high‑resolution sensor arrays. D-Sub Micro Connectors Market can leverage this shift by developing hardened variants that meet automotive temperature cycles and vibration standards. Early entry into these sub‑segments promises a differentiated revenue stream as vehicle manufacturers lock in component suppliers for multiple model years.

D-Sub Micro Connectors Market Trends

Miniaturization Fuels Demand for Micro‑D Form Factors

Industrial designers are increasingly forced to squeeze functionality into ever smaller chassis, prompting a shift from traditional D‑Subminiature parts to the Micro‑D family. The reduced footprint,roughly one‑third the size of a standard D‑Sub,lets engineers meet board‑real‑estate constraints without sacrificing the robust shielding that legacy connectors provide. Because the shell retains the familiar D‑shape, system architects can reuse existing mating hardware while gaining up to 40 % more contacts per unit area. This convergence of size efficiency and mechanical reliability explains why the D‑Sub Micro Connectors Market is seeing a noticeable uptick in new product introductions across aerospace, automation and telecom equipment.

Other Trends

Manufacturing Precision and Material Costs

The production chain for micro connectors hinges on sub‑micron tolerance machining and strict plating protocols. Recent volatility in copper and nickel prices has squeezed margins, encouraging OEMs to consolidate purchases or explore alternative alloy treatments. Simultaneously, advances in CNC micro‑machining have lowered scrap rates, allowing manufacturers to sustain profitability even as order volumes fluctuate. Automation of stamping and injection processes is being introduced to improve repeatability, while tighter statistical process control reduces lead‑time variance. This balance between cost pressure and technological improvement shapes supplier strategies throughout the D‑Sub Micro Connectors Market supply chain, prompting many players to invest in hybrid‑metal‑plastic housings that retain EMI performance at lower material cost.

Application‑Specific Divergence

While high‑speed serial links erode D‑Sub usage in consumer devices, the connectors retain a niche where ruggedness, standardized pinouts and proven EMI performance outweigh bandwidth considerations. Aerospace platforms, military ground stations and oil‑field instrumentation continue to specify D‑Sub micro form factors because qualification cycles favour proven components. Manufacturers respond by expanding mixed‑layout families that embed power, signal and coaxial contacts within a single housing, effectively turning a legacy interface into a multifunctional hub. For end users, this translates into reduced bill‑of‑materials, simplified inventory management and higher overall system reliability, reinforcing the relevance of the D‑Sub Micro Connectors Market in sectors that prioritize durability over raw data rates.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive dynamics in the D‑Sub Micro Connectors market

TE Connectivity dominates the upper tier of the D‑Sub Micro Connectors segment, leveraging a portfolio that spans legacy MIL‑DTL series to recently introduced high‑density micro‑D families. Its extensive global manufacturing footprint and deep relationships with aerospace OEMs allow it to capture price‑sensitive contracts while maintaining stringent performance standards. The company’s ability to integrate precision metal stamping with advanced plating processes gives it a cost advantage that smaller rivals struggle to match. This scale translates into a market structure where a handful of tier‑one suppliers control the majority of revenue, while a robust second tier competes on niche specifications such as IP‑67 ratings or mixed‑layout configurations for industrial automation.

Beyond the tier‑one echelon, a diverse set of specialists enriches the competitive landscape. Amphenol and Molex have broadened their micro‑D lines with modular back‑shell options that appeal to system integrators seeking rapid customization. European player Harting focuses on rugged, panel‑mount variants tailored for railway and heavy‑industry deployments, whereas Glenair concentrates on hermetic solutions for defense and space programs. Smaller innovators such as NorComp, Kycon, and Nicomatic differentiate themselves through rapid prototyping services and localized supply chains that reduce lead times for emerging markets in Asia‑Pacific. This mix of global scale and targeted agility creates a competitive pressure that pushes all participants toward tighter tolerances, higher EMI shielding, and more sustainable material sourcing.

List of Key D‑Sub Micro Connectors Companies Profiled

- TE Connectivity

- Amphenol Corporation

- Molex, LLC

- NorComp, Inc.

- Glenair, Inc.

- Harting Technology Group

- Kycon, Inc.

- EDAC, Inc.

- Cinch Connectivity Solutions

- Positronic Industries, Inc.

- Nicomatic SA

- Adam Tech

- AVX Interconnect

- L‑com, Inc.

- Switchcraft Inc.

- Smiths Interconnect Ltd.

- ITT Cannon (ITT Interconnect Solutions)

- Omron Electronics

- Panduit Corp.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Straight Style is widely preferred because:

|

| By Application |

|

Aerospace drives demand through:

|

| By End User |

|

Communications Equipment remains a core end‑user because:

|

| By Mounting Style |

|

Through‑Hole Mount is favored for:

|

| By Connector Size |

|

Micro‑D Connectors dominate because:

|

Regional Analysis: D-Sub Micro Connectors Market

Europe

EU directives on electromagnetic compatibility and environmental stewardship shape connector specifications. Manufacturers align bill of materials with REACH‑compliant alloys, reducing the risk of supply interruptions while meeting client expectations for sustainable sourcing.

Engineers are exploring hybrid shell concepts that blend traditional D‑Sub geometry with nano‑coated contacts, extending lifecycle performance in harsh industrial climates without overhauling existing tooling.

Multi‑sourcing strategies across Germany, Italy and the Czech Republic mitigate geopolitical shocks, ensuring that critical micro‑connectors reach assembly lines on schedule even during pandemic‑related disruptions.

Long‑standing collaborations between connector specialists and automotive tier‑1 suppliers facilitate rapid qualification cycles, allowing legacy vehicle platforms to adopt newer micro‑form factors without re‑engineering harnesses.

North America

In North America, the D‑Sub Micro Connectors Market is shaped by a pragmatic approach to legacy system upgrades. Defense contractors and aerospace firms retain extensive inventories of older platforms, prompting vendors to offer refurbish‑ready parts that meet stringent MIL‑SPEC criteria. Parallelly, the surge in edge‑computing deployments across U.S. data centers drives interest in compact interconnects that fit within constrained chassis. Companies that can balance compliance with cost‑effectiveness are gaining the confidence of both government and commercial buyers, fostering a niche but steady growth trajectory.

Asia‑Pacific

The Asia‑Pacific region presents a paradox of rapid digital transformation alongside entrenched manufacturing practices. While Japanese and South Korean electronics firms are integrating D‑Sub Micro Connectors into high‑precision instrumentation, manufacturers in India and Vietnam prioritize low‑cost solutions for expanding telecom back‑haul. The strategic focus on localized production reduces lead times, yet variations in quality standards require suppliers to adapt process controls for each market. This duality creates opportunities for firms that can tier‑price offerings without compromising the core reliability associated with the connector family.

South America

South American demand is anchored in the refurbishment of legacy industrial equipment, especially within Brazil’s automotive assembly sector. Economic incentives aimed at modernizing manufacturing plants have spurred interest in micro‑scale connectors that enable tighter packaging while preserving established wiring architectures. However, import‑tariff volatility forces local distributors to maintain buffer stocks, influencing procurement cycles. Vendors that provide transparent logistics and after‑sales support are better positioned to capture this evolving segment.

Middle East & Africa

In the Middle East and Africa, infrastructure projects tied to oil‑and‑gas extraction and renewable‑energy installations drive intermittent spikes in connector requirements. Operators value the proven durability of D‑Sub Micro Connectors for rugged field equipment, yet they also seek modular solutions that simplify maintenance in remote locations. Limited local manufacturing capacity places emphasis on reliable import channels, making partnership models with global distributors a decisive factor for market entry and sustained relevance.

Report Scope

This market research report provides a comprehensive analysis of the D-Sub Micro Connectors Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of D-Sub Micro Connectors Market?

-> D-Sub Micro Connectors market is projected to reach USD 1680 million by 2034, exhibiting a CAGR of 6.0% during the forecast period.

Which key companies operate in D-Sub Micro Connectors Market?

-> Key players include TE Connectivity, NorComp, Amphenol, ITT Cannon, Harting, Molex, Glenair, and other leading manufacturers.

What are the key growth drivers?

-> Key growth drivers include demand for reliable standardized interconnect solutions, miniaturization and high‑density design trends, growth in aerospace & defense, and expanding industrial automation applications.

Which region dominates the market?

-> North America remains the dominant region due to strong aerospace, defense, and telecommunications sectors, while Asia‑Pacific is the fastest‑growing market.

What are the emerging trends?

-> Emerging trends include high‑density and IP67‑rated designs, hermetic MIL‑DTL solutions for aerospace, and increased adoption of mixed‑layout connectors that combine signal, power, and coaxial contacts.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...