Automotive Charging High-side Switch Controller Market Insights

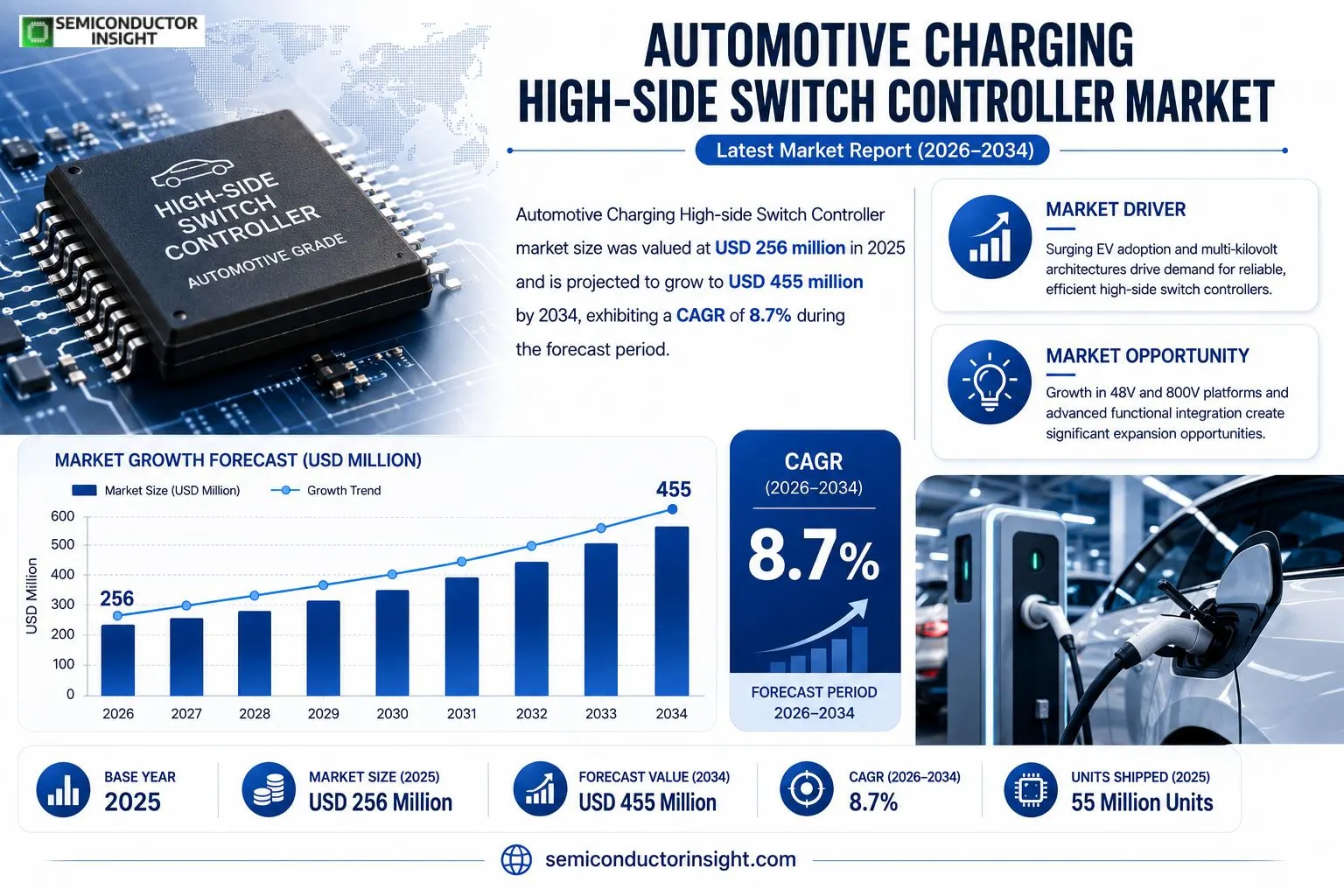

Automotive Charging High-side Switch Controller market size was valued at USD 256 million in 2025. The market is projected to grow from USD 256 million in 2025 to USD 455 million by 2034, exhibiting a CAGR of 8.7% during the forecast period.

Automotive Charging High-side Switch Controller is an automotive‑grade control IC dedicated to managing high‑side power paths in vehicle charging systems, integrating switching control, protection and diagnostics to ensure safe power distribution, fault isolation and stable operation under harsh electrical and thermal conditions. In 2025 production reached roughly 55 million units with an average price of USD 5.1 per unit; capacity utilization stood at about 70% and gross margin near 40%. Upstream inputs such as silicon wafers, photoresists, leadframes and epoxy molding compounds are supplied by firms including Shin‑Etsu Chemical, JSR, Sumitomo Bakelite and Amkor Technology. Midstream activities cover architecture definition, switching logic design, current sensing, thermal engineering and automotive qualification planning. Downstream customers span passenger‑car OEMs (BYD, Toyota, Volkswagen) and commercial‑vehicle makers (FAW Group, Ford), who value controllers that reduce validation effort while improving charging safety and uptime.

MARKET DRIVERS

Electrification Momentum Fuels Demand

sales of electric passenger vehicles surpassed 10 million units in 2023, a rise of roughly 14 % year‑over‑year. That surge forces automakers to adopt multi‑kilovolt battery architectures, which in turn lift the importance of reliable high‑side switch controllers. In Automotive Charging High-side Switch Controller Market, manufacturers are racing to qualify silicon‑based devices that can tolerate the 800‑V corridors now common in fast‑charging modules.

Stringent Efficiency Regulations

Europe’s WLTP revision and the U.S. Tier 3 emissions framework impose tighter limits on auxiliary power draw. Engineers therefore prioritize switch topologies that cut conduction loss to under 10 mΩ. The Automotive Charging High‑side Switch Controller Market benefits as OEMs replace legacy MOSFET solutions with low‑RDS(on) devices that shave a few percentage points off overall vehicle energy consumption.

➤ “Every percent of reduced loss translates directly into an additional 3‑5 km of range for a typical EV.”

Beyond efficiency, high‑side switches now serve as gatekeepers for safety‑critical isolations, complying with ISO 26262 functional‑safety standards. This dual roleperformance and safetycreates a compelling value proposition for suppliers that can certify their silicon for automotive‑grade reliability.

Integration with emerging silicon‑carbide (SiC) power stages is unlocking new design margins. SiC modules generate less heat, allowing the Automotive Charging High‑side Switch Controller Market to offer compact, lighter solutions that meet both cost targets and the aggressive packaging constraints of next‑generation vehicle platforms.

MARKET CHALLENGES

Thermal Management Constraints

High‑current charge paths produce significant junction temperatures, especially under fast‑charge scenarios exceeding 350 kW. If the switch controller cannot dissipate heat efficiently, failure rates climb, prompting costly warranty claims. Designers are forced to allocate precious board real‑estate to heat sinks or liquid‑cooling loops, which erodes the cost advantage of newer silicon.

Other Challenges

Cost Sensitivity

Automakers negotiate component prices at scale, targeting sub‑$2 per‑unit targets for high‑side switches. Suppliers that rely on low‑volume, specialty processes struggle to meet these pressure points, limiting their participation in mass‑market EV programs.Supply‑chain volatility adds another layer of risk. Recent semiconductor shortages have elongated lead times for silicon wafers, prompting OEMs to qualify multiple vendorsa strategy that dilutes volume discounts and complicates qualification pathways.

MARKET RESTRAINTS

Complexity of Integrated Power Architectures

Modern EV platforms embed the high‑side switch within a dense power‑electronics module that also houses DC‑DC converters, gate drivers and diagnostic circuitry. This integration raises the bar for electromagnetic‑compatibility (EMC) compliance and board‑level layout precision, discouraging smaller tier‑1 suppliers from entering the Automotive Charging High‑side Switch Controller Market.Limited availability of engineers experienced in both high‑voltage design and functional‑safety qualification further restrains market expansion. Companies that cannot staff projects with dual‑skill talent face longer development cycles and higher R&D expenditures.

MARKET OPPORTUNITIES

Emerging 48V and 800V Vehicle Platforms

While 400 V systems dominate today’s passenger‑car segment, the industry is pivoting toward 48 V mild‑hybrid architectures for cost‑effective electrification and 800 V platforms for ultra‑fast charging. Both trajectories demand switch controllers with wider voltage ratings and faster turn‑on/off capabilities, opening a niche that experienced silicon vendors can capture.Growth of aftermarket retrofit solutions presents a parallel avenue. Independent service providers are beginning to offer high‑voltage charging upgrades for legacy internal‑combustion vehicles, requiring plug‑and‑play high‑side switch modules that meet automotive safety standards. This segment, though modest in size, offers a steady revenue stream that can offset the volatility of original‑equipment demand.

Automotive Charging High-side Switch Controller Market Trends

Higher On‑board Charging Power Elevates Controller Criticality

Automotive Charging High-side Switch Controller Market is being reshaped as vehicle architectures accommodate charging currents that exceed legacy limits. In 2025 the market value stood at US$256 million, and the demand for unitsapproximately 55 millionreflected a shift toward controllers that do more than simple switching. OEMs such as Toyota, Volkswagen and BYD now regard these ICs as gatekeepers of charging safety, because they combine precise over‑current protection, fault isolation and diagnostic feedback in a single silicon die. This functional density reduces the part count in the power path, a benefit that directly translates into lower board‑level complexity and higher system reliability under the harsh thermal cycles typical of fast‑charging events.

Other Trends

Supply Chain Consolidation

Upstream inputs for the controller ecosystem remain dominated by a handful of silicon wafer and packaging suppliers, including Shin‑Etsu Chemical, JSR and Amkor Technology. Their stable process capabilities enable manufacturers to maintain a 70 % capacity utilization rate while delivering consistent quality. As the market expands, these suppliers are negotiating longer‑term agreements with controller fabless firms to lock in epoxy molding compounds and lead‑frame inventories, mitigating the risk of material shortages that could otherwise force price concessions.

Margin Preservation Through Functional Integration

Profitability in Automotive Charging High-side Switch Controller Market hinges less on unit‑price battles and more on the ability to embed additional safety and diagnostic features without inflating cost. The 2025 average gross margin of 40 % illustrates how manufacturers capture value by reducing external component counts and by offering platforms that can be reused across multiple vehicle programs. OEMs reward such solutions with reduced validation cycles, a factor that becomes increasingly important as charging architectures evolve toward dual‑channel designs and smarter PWM or SPI interfaces. Companies that can demonstrate measurable uptime improvements and lower field‑failure rates are better positioned to negotiate premium pricing while sustaining healthy margins even as volume pressures intensify.

COMPETITIVE LANDSCAPE

Key Industry Players

Automotive Charging High‑Side Switch Controller – Competitive Overview

The high‑side switch controller segment is anchored by a handful of silicon specialists that have locked in long‑term supply agreements with the world’s largest OEMs. Infineon and STMicroelectronics dominate the top tier, each leveraging mature 28 nm automotive‑grade processes to deliver integrated protection, diagnostic and current‑sensing functions that meet the stringent SAE‑J3105 safety standards. Their portfolios are bundled into platform‑wide power‑train families, allowing vehicle programs such as BYD, Toyota and Volkswagen to reduce validation effort and achieve consistent gross margins despite price pressure. The market’s capacity utilization of roughly 70 % in 2025 reflects a balance between high‑volume passenger‑car demand and the need for flexible design windows that accommodate emerging 800 V fast‑charging architectures.Beyond the front‑runners, a cluster of niche but technically aggressive firms is reshaping the competitive map. Diodes Incorporated and ROHM focus on compact 12 V and 24 V modules that excel in commercial‑vehicle fleets, while Renesas and Fuji Electric exploit their legacy automotive safety IP to embed functional‑safety monitors directly into the switch controller. Texas Instruments, Microchip and onsemi are differentiating through mixed‑signal solutions that combine SPI diagnostics with ultra‑low‑quiescent current, targeting electric‑bus applications where thermal headroom is limited. Toshiba, NXP Semiconductors and Analog Devices round out the field by pursuing silicon‑photonic integration or adding integrated DC‑DC stages, positioning themselves as one‑stop suppliers for next‑generation charging racks. These players collectively command a modest share of the market but exert outsized influence on price‑performance trade‑offs, especially as OEMs seek to minimise BOM count while tightening reliability KPIs.

List of Key Automotive Charging High‑Side Switch Controller Companies Profiled

- Infineon

- STMicroelectronics

- Diodes Incorporated

- ROHM Semiconductor

- Renesas Electronics

- Fuji Electric

- Texas Instruments

- Microchip Technology

- onsemi

- Toshiba

- NXP Semiconductors

- Analog Devices

- Maxim Integrated

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

12V Controller is the prevailing type because:

|

| By Application |

|

Passenger Cars dominate the application landscape because:

|

| By End User |

|

OEMs are the leading end‑user segment because:

|

| By Interface |

|

PWM Interface is favored due to:

|

| By Voltage Level |

|

48V Systems are emerging as a strategic focus because:

|

Regional Analysis: Automotive Charging High-side Switch Controller Market

Europe

The EU’s revised CO₂ framework mandates lower fleet‑average emissions, prompting manufacturers to prioritize electric power‑train components. As a result, high‑side switch controllers receive heightened attention in vehicle‑architecture roadmaps, with funding streams earmarked for qualifying technologies.

Recent mergers among European OEMs have streamlined platform strategies, creating larger volumes for standardized high‑side switch modules. Suppliers that can offer plug‑and‑play compatibility across multiple brands stand to capture a disproportionate share of orders.

Universities in the Netherlands and Sweden are pioneering wide‑bandgap semiconductor designs that cut losses and improve thermal performance. Early adopters among tier‑one firms translate these advances into compact controller packages, reinforcing Europe’s reputation for technical leadership.

Coordinated rollout of ultra‑fast chargers across major highways aligns with OEM plans to integrate high‑side switch controllers capable of handling higher charging currents, ensuring that vehicle and charger development progress in lockstep.

North America

In North America, Automotive Charging High-side Switch Controller Market reflects the continent’s focus on high‑performance EVs aimed at long‑range applications. U.S. federal tax credits and state‑level zero‑emission vehicle mandates have spurred OEMs to adopt advanced power‑train architectures, where the high‑side switch serves as a linchpin for safety and efficiency. Canadian manufacturers, while smaller in scale, emphasize cold‑climate resilience, prompting suppliers to engineer controllers with robust thermal‑management features. The region’s supply chain benefits from proximity to major silicon‑carbide fabs, enabling rapid prototyping cycles and fostering collaborations between automotive engineers and semiconductor vendors. Overall, market participants prioritize reliability under high‑current charging scenarios, translating regulatory incentives into tangible design imperatives.

Asia-Pacific

Asia‑Pacific remains a hotbed of activity for Automotive Charging High-side Switch Controller Market, driven largely by China’s aggressive push toward electrified mobility and Japan’s longstanding expertise in automotive electronics. Chinese OEMs are integrating high‑side switches into a broad spectrum of vehicle classes, from compact city cars to premium sedans, as part of national targets to curtail urban pollution. Japanese firms, on the other hand, leverage decades of experience with high‑voltage systems to refine controller architectures for optimal space utilization, a critical factor in densely packed vehicle designs. Korean manufacturers contribute by championing cost‑effective wafer‑scale integration, allowing volume production without sacrificing performance. The regional ecosystem is further reinforced by a dense network of component distributors that facilitate swift market penetration across diverse regulatory environments.

South America

South America’s Automotive Charging High-side Switch Controller Market is shaped by emerging EV adoption in Brazil and Argentina, where government incentives focus on reducing import tariffs for electric vehicles. Local manufacturers, seeking to differentiate their offerings, are beginning to source high‑side switch solutions that can operate reliably under the continent’s varied climate conditions, from tropical heat to high‑altitude environments. Supply‑chain constraints have encouraged partnerships with European tier‑ones, creating a channel for technology transfer and capacity building within the region. While overall vehicle volumes remain modest compared to other territories, the willingness of regional players to experiment with advanced controller topologies signals a nascent but growing demand base.

Middle East & Africa

The Middle East & Africa region presents a distinct set of opportunities for Automotive Charging High-side Switch Controller Market, largely linked to the Gulf Cooperation Council’s investment in renewable‑energy‑powered charging stations. Harsh desert temperatures have compelled OEMs and suppliers to prioritize thermal‑resilient controller designs, ensuring consistent performance during rapid charging cycles. South Africa’s automotive sector, with its mix of domestic assembly and export activity, is exploring high‑side switch integrations to comply with emerging safety standards for electric vehicles. Cross‑border trade agreements are facilitating the flow of components from Europe and Asia, allowing regional integrators to assemble bespoke solutions for niche markets such as luxury EVs and commercial fleets. Collectively, these dynamics illustrate a market that, while still maturing, is laying the groundwork for broader adoption of sophisticated charging architectures.

Report Scope

This market research report provides a comprehensive analysis of the Automotive Charging High-side Switch Controller Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Automotive Charging High-side Switch Controller Market?

-> Automotive Charging High-side Switch Controller Market was valued at USD 256 million in 2025 and is expected to reach USD 455 million by 2034, at a CAGR of 8.7% during the forecast period.

Which key companies operate in Automotive Charging High-side Switch Controller Market?

-> Key players include STMicroelectronics, Infineon, Diodes Incorporated, ROHM, Renesas, Fuji Electric, Texas Instruments, Microchip, onsemi, and Toshiba.

What are the key growth drivers?

-> Key growth drivers include the rapid increase in onboard charging power, tightening safety and reliability requirements, integration of precise protection and diagnostics, and the shift toward platform‑level adoption across vehicle programs.

Which region dominates the market?

-> Asia leads the market in terms of volume and revenue, driven by high production volumes in China, Japan, and South Korea, while Europe remains a strong secondary market.

What are the emerging trends?

-> Emerging trends include higher‑current architectures, smarter power‑path control, increased functional integration to reduce external components, and a focus on long‑term platform stability and fault‑isolation capabilities.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...