Super Junction MOSFET for Charging Pile Market Insights

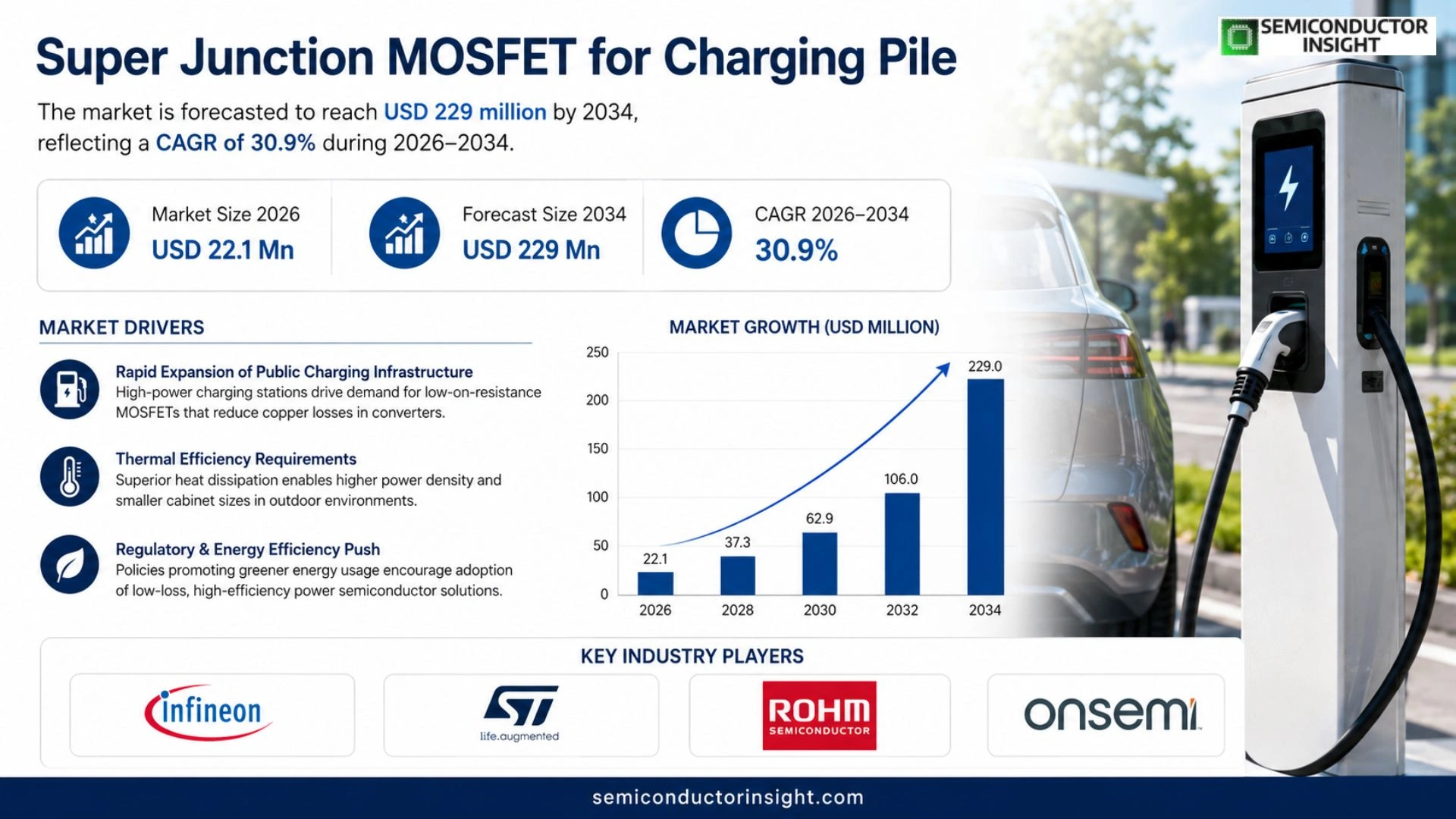

Global Super Junction MOSFET for Charging Pile market size was valued at USD 34.57 million in 2025. The market is forecasted to reach USD 229 million by 2034, reflecting a compound annual growth rate of 30.9 % over the period.

Super Junction MOSFET for Charging Pile refers to a high‑voltage silicon power device built on a charge‑balanced drift‑region architecture. Alternating N‑type and P‑type pillars within the drift zone equalize charge, allowing substantially lower specific on‑resistance (RDS(on)) compared with conventional planar devices at identical breakdown voltages. This structure enables fast, voltage‑driven switching ideal for EV charging converters.

The devices are typically fabricated from silicon wafers through epitaxial growth followed by trench or pillar formation, gate oxidation, ion implantation, metallization and passivation steps. Because the blocking capability depends primarily on epitaxial thickness while maintaining low resistance, precise control of pillar charge balance and oxide quality drives both performance and reliability.

In downstream applications these MOSFETs are commonly employed in front‑end AC‑DC stages, isolated DC‑DC converters and auxiliary rails of charging piles where cost sensitivity and mature silicon supply chains remain advantageous.

MARKET DRIVERS

Rapid Expansion of Public Charging Infrastructure

The rollout of high‑power charging stations across major urban corridors has created a pressing need for power‑semiconductor solutions that can handle elevated voltage and current levels. Super Junction MOSFET for Charging Pile Market players that can offer low‑on‑resistance devices are seeing a surge in OEM specifications, because the technology directly reduces copper losses in converters.

Thermal Efficiency Requirements

Charging piles operate in outdoor enclosures where temperature spikes are common. The superior heat‑dissipation profile of super‑junction structures translates into higher power density, allowing manufacturers to shrink cabinet dimensions while maintaining safety margins. This trend encourages adoption of advanced MOSFET designs over legacy silicon alternatives.

➤ Design engineers report up to a 30% reduction in cooling system size when replacing conventional MOSFETs with super‑junction variants.

Regulatory pushes toward greener energy consumption have also nudged operators to select components that lower overall system loss. The cumulative effect is a tighter alignment between policy incentives and the technical advantages of super‑junction devices, accelerating market momentum.

MARKET CHALLENGES

Cost Sensitivity Among Infrastructure Investors

While performance metrics are compelling, the initial price premium of super‑junction MOSFETs remains a barrier for capital‑constrained projects. Investment committees often prioritize total‑cost‑of‑ownership calculations that discount upfront savings, leading to cautious procurement cycles.

Other Challenges

Supply‑Chain Volatility

Limited wafer capacity and concentrated fab locations mean that sudden demand spikes can outpace production, creating lead‑time extensions that ripple through project schedules.

MARKET RESTRAINTS

Stringent Reliability Standards

Charging pile manufacturers must satisfy automotive‑grade reliability tests, including high‑temperature operating life (HTOL) and electrical overstress (EOS) assessments. Super‑junction MOSFETs, being relatively newer, sometimes lack the extensive field‑history that legacy devices possess, prompting conservative qualification approaches.

Furthermore, certifications such as IEC 61851 impose strict leakage current limits. Meeting these thresholds often requires additional circuit protection, which can erode some of the efficiency gains that the technology promises.

Finally, the niche nature of the market means that end‑users have limited experience in integrating super‑junction architectures, resulting in longer engineering validation periods and higher design‑iteration costs.

MARKET OPPORTUNITIES

Integration with Wide‑Bandgap Power Electronics

Hybrid topologies that pair silicon‑based super‑junction MOSFETs with silicon‑carbide (SiC) or gallium‑nitride (GaN) devices are gaining attention. Such configurations can push efficiency beyond 98% for DC‑DC converters, opening premium‑segment opportunities for suppliers that provide mixed‑technology design services.

In parallel, the emergence of smart‑grid‑enabled charging stations creates a demand for devices capable of rapid switching and bidirectional power flow. Companies that position their super‑junction MOSFETs within a broader ecosystem,offering firmware support and predictive‑maintenance analytics,stand to capture a larger share of future deployments.

Lastly, strategic collaborations between semiconductor fabs and EV charging OEMs are expected to streamline development cycles. Joint‑venture projects that co‑develop application‑specific MOSFET libraries could reduce time‑to‑market, giving early movers a decisive advantage in the evolving Super Junction MOSFET for Charging Pile Market.

Super Junction MOSFET for Charging Pile Market Trends

Escalating Demand for Higher‑Power EV Chargers

The market recorded a value of US$ 34.57 million in 2025 and is forecasted to rise to roughly US$ 229 million by 2032, reflecting an annual growth rate of about 30.9 percent. This trajectory is rooted in the push for charging stations that deliver greater power density while keeping system cost under control. Operators are favouring silicon‑based Super Junction MOSFETs because they combine low on‑resistance with mature, cost‑effective manufacturing, a balance that is difficult for emerging wide‑bandgap options to match at mid‑tier voltage classes (600‑650 V). The result is a steady influx of new designs that integrate these devices into front‑end AC‑DC converters and auxiliary DC‑DC rails, where efficiency gains translate directly into lower electricity bills for end users.

Other Trends

Manufacturing Economics and Margin Pressure

Upstream, the process chain relies on precise trench‑or‑pillar formation, followed by cell structuring, gate oxidation, and metallisation. Control of pillar charge balance and oxide quality determines blocking capability and resistance, making yield a key lever for profitability. In 2025, global sales reached approximately 17 million pieces at an average price of US$ 2.2 per unit, delivering gross margins that vary from 30 percent to 50 percent across manufacturers. Capacity is unevenly distributed, with a handful of vendors commanding the bulk of volume, which intensifies price competition and forces smaller players to specialise in niche voltage or qualification grades.

System‑Level Integration and Competitive Positioning

On the downstream side, charging‑pile architectures are increasingly partitioned into modular stages where silicon Super Junction MOSFETs occupy mid‑power blocks, secondary supplies, and hybrid configurations. While wide‑bandgap devices are gaining foothold in ultra‑high‑efficiency front‑ends, the silicon offering retains relevance because of its established supply chain and familiar design‑in ecosystem. Vendors are differentiating through device‑package co‑optimisation that reduces parasitics, improves thermal extraction, and tightens EMI performance. The principal headwinds include relentless pricing pressure from commoditised platforms and the stringent reliability validation required for outdoor deployment, which raises total cost of ownership considerations for OEMs.

COMPETITIVE LANDSCAPE

Key Industry Players

Super Junction MOSFETs for EV Charging Piles – Competitive Overview

The market is anchored by a handful of Tier‑1 silicon specialists that command the bulk of volume and pricing power. Infineon, with its dedicated SuperJunction family, leverages deep wafer‑fab capacity and a mature supply chain to secure design‑in relationships across OEM charging‑station platforms. Its ability to co‑optimize device layout and thermal package translates into lower on‑resistance and tighter switching margins, which in turn drives a premium margin profile of 40‑50 %. STMicroelectronics follows a similar trajectory, offering a broad portfolio that spans the 500 V to 800 V classes and integrates seamlessly with its automotive power‑module ecosystem. The duopoly imposes a price‑discipline on the remainder of the field, while still leaving room for differentiated product‑gate strategies such as hardened automotive‑grade silicon that tolerates harsh outdoor cycles.

Beyond the dominant duopolists, a constellation of niche innovators enriches the competitive set. ROHM and onsemi supply cost‑competitive SJ devices that excel in soft‑switching topologies, with ROHM emphasizing low‑gate‑charge variants for auxiliary rails and onsemi focusing on high‑current modules for DC‑DC conversion. Toshiba, Vishay, and Taiwan Semiconductor maintain strong regional footprints, especially in Asia‑Pacific, by coupling foundry scale with targeted application engineering. Smaller entrants,including Magnachip, IceMOS Technology, PANJIT, Marching Power, CoolSemi, Oriental Semiconductor, Lonten Semiconductor, and Jiangsu JieJie Microelectronics,differentiate through aggressive pricing, specialty package formats, or bespoke reliability programs that appeal to system integrators seeking supply‑chain resilience. Their collective presence ensures that while the market gravitates toward a few large players, diversification of risk and innovation persists across the value chain.

List of Key Super Junction MOSFET for Charging Pile Companies Profiled

- Infineon Technologies AG

- STMicroelectronics

- ROHM Co., Ltd.

- onsemi

- Toshiba Electronic Devices & Storage Corporation

- Vishay Intertechnology, Inc.

- Taiwan Semiconductor Manufacturing Co.

- Microchip Technology Inc.

- Magnachip Semiconductor Corp.

- IceMOS Technology Ltd.

- PANJIT Electronics Co., Ltd.

- Marching Power (Shenzhen) Co., Ltd.

- CoolSemi Ltd.

- Oriental Semiconductor Co., Ltd.

- Lonten Semiconductor Co., Ltd.

- Jiangsu JieJie Microelectronics Co., Ltd.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

High‑Voltage Core dominates the market as designers prioritize low on‑resistance for efficiency. ‑ Mature silicon process ensures cost‑effective production while delivering reliable blocking capability. ‑ Designers favor the 600/650V tier for most EV charging piles, balancing voltage margin and thermal performance. ‑ Emerging interest in 800‑950V devices supports next‑generation ultra‑fast chargers where silicon still offers a pragmatic trade‑off. |

| By Application |

|

Versatile Converter Role enables broad adoption across charging architectures. ‑ In front‑end stages, low RDS(on) reduces conduction loss, directly improving overall charger efficiency. ‑ Isolated DC‑DC modules benefit from the robust voltage blocking of SJ structures, simplifying isolation design. ‑ Auxiliary rails rely on the fast switching capability to manage control logic without adding bulk. ‑ Soft‑switching bridges exploit the reduced reverse recovery charge of SJ MOSFETs, mitigating EMI and easing thermal design. |

| By End User |

|

Cost‑Sensitive Deployments drive preference for silicon SJ MOSFETs. ‑ Residential units value the lower component cost and proven reliability, favoring mid‑range voltage families. ‑ Commercial fleets seek durability under higher duty cycles; SJ devices provide a balance of robustness and thermal handling. ‑ Public fast‑charging operators prioritize efficiency gains to reduce operational electricity expense, making low‑loss SJ MOSFETs attractive despite emerging wide‑bandgap competition. |

| By Voltage Class |

|

Strategic Voltage Positioning informs system topology choices. ‑ Low‑voltage devices are increasingly relegated to auxiliary functions where ultra‑low loss is less critical. ‑ Mid‑voltage SJ MOSFETs remain the workhorse for most AC‑DC converters, offering an optimal trade‑off between breakdown capability and on‑resistance. ‑ High‑voltage offerings enable compact designs for emerging ultra‑fast chargers, preserving silicon’s cost advantage while extending voltage headroom. |

| By Switching Optimization |

|

Design‑Centric Differentiation guides product selection for charger architects. ‑ Hard‑switching families emphasize ruggedness, suited for cost‑driven installations where EMI control is manageable. ‑ Soft‑switching optimized devices reduce voltage spikes and ringing, crucial for high‑power fast chargers seeking low acoustic noise and extended component life. ‑ PFC‑optimized MOSFETs integrate well into front‑end power factor correction stages, enhancing overall system power quality without additional circuitry. |

Regional Analysis: Super Junction MOSFET for Charging Pile Market

Europe

The EU’s revised Low‑Emission Vehicle Standards mandate higher conversion efficiencies for charging hardware, prompting many European firms to prioritize Super Junction MOSFETs that deliver lower on‑resistance. Compliance timelines are clear, enabling component suppliers to synchronize product launches with vehicle roll‑outs, thereby reducing time‑to‑market for charging solutions.

A well‑established silicon wafer ecosystem exists across the continent, supported by a network of specialty fabs that can handle the high‑voltage, high‑temperature requirements of Super Junction technology. This reduces reliance on distant manufacturers and shortens lead times for charging‑pile builders.

Leading European power‑semiconductor firms have leveraged their proximity to automotive OEMs to negotiate long‑term supply agreements. Their ability to offer custom device footprints gives them an edge over generic global players who lack localized engineering support.

Research clusters in Munich, Eindhoven and Paris host joint ventures between universities and industry, accelerating prototype validation for next‑generation MOSFETs that can handle higher charging currents without compromising thermal performance.

North America

In North America, Super Junction MOSFET for Charging Pile Market is shaped by a patchwork of state‑level incentives and a strong emphasis on fast‑charging networks along highway corridors. While federal policy remains less prescriptive than Europe’s, leading car manufacturers are already embedding high‑efficiency devices to meet corporate carbon‑reduction pledges. The region benefits from abundant silicon production capacity, yet the reliance on a few large foundries can introduce bottlenecks when demand spikes. Companies that establish close collaborations with utility firms are better positioned to integrate MOSFETs into grid‑interactive charging stations, creating a differentiated value proposition for commercial fleets.

Asia‑Pacific

Asia‑Pacific presents a divergent picture; rapid urbanization drives massive deployment of public chargers, yet the market is fragmented across economies with varying technical standards. China’s aggressive rollout of ultra‑fast chargers forces local suppliers to adopt Super Junction MOSFETs that can sustain high current densities while maintaining compact form factors. Japan and South Korea, with their mature semiconductor sectors, focus on integrating these devices into smart‑charging architectures that communicate with vehicle‑to‑grid systems. The region’s sheer scale offers growth potential, but firms must navigate intellectual‑property concerns and divergent certification regimes.

South America

South America is transitioning from a nascent to a more established market for electric‑vehicle charging infrastructure. Governments in Brazil and Chile have introduced fiscal measures to encourage the adoption of efficient power electronics, making Super Junction MOSFETs an attractive choice for cost‑sensitive projects. However, limited local manufacturing means most components are imported, inflating project budgets. Partnerships between multinational semiconductor firms and regional integrators are emerging as a solution, providing technology transfer while mitigating supply‑chain constraints.

Middle East & Africa

The Middle East & Africa region is characterised by a focus on high‑temperature reliability, given the extreme climatic conditions that charging stations must endure. Operators in the Gulf Cooperation Council states are piloting ultra‑fast chargers capable of delivering large power bursts; this pushes the demand for MOSFETs with superior thermal tolerance. In Africa, early‑stage deployments are concentrated in commuter hubs where grid stability is variable, prompting designers to select devices that can operate efficiently across a wide voltage range. Collaborative projects between local utilities and global component makers are beginning to address these unique challenges.

Report Scope

This market research report provides a comprehensive analysis of the Super Junction MOSFET for Charging Pile Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Super Junction MOSFET for Charging Pile Market?

-> Super Junction MOSFET for Charging Pile market is forecasted to reach USD 229 million by 2034, reflecting a compound annual growth rate of 30.9 %

Which key companies operate in Super Junction MOSFET for Charging Pile Market?

-> Key players include Infineon, STMicroelectronics, ROHM, onsemi, Toshiba, Vishay, Taiwan Semiconductor, Microchip, Magnachip, IceMOS Technology, PANJIT, Marching Power, CoolSemi, Oriental Semiconductor, Lonten Semiconductor, Jiangsu JieJie Microelectronics.

What are the key growth drivers?

-> Key growth drivers include rising EV charging infrastructure, demand for higher power density and efficiency, cost‑effective silicon solutions, and the need for reliable low‑loss power conversion in charging‑pile applications.

Which region dominates the market?

-> Asia leads the market due to extensive EV adoption, large‑scale charging‑station deployments, and mature silicon manufacturing ecosystems, while North America and Europe also show strong growth.

What are the emerging trends?

-> Emerging trends include integration of wide‑bandgap devices alongside silicon SJ MOSFETs, device‑package co‑optimization for lower parasitics, improved thermal management, and hybrid architectures that combine SJ MOSFETs with SiC/GaN for optimal performance.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...