Vacuum Gate Valve for Semiconductor Market Insights

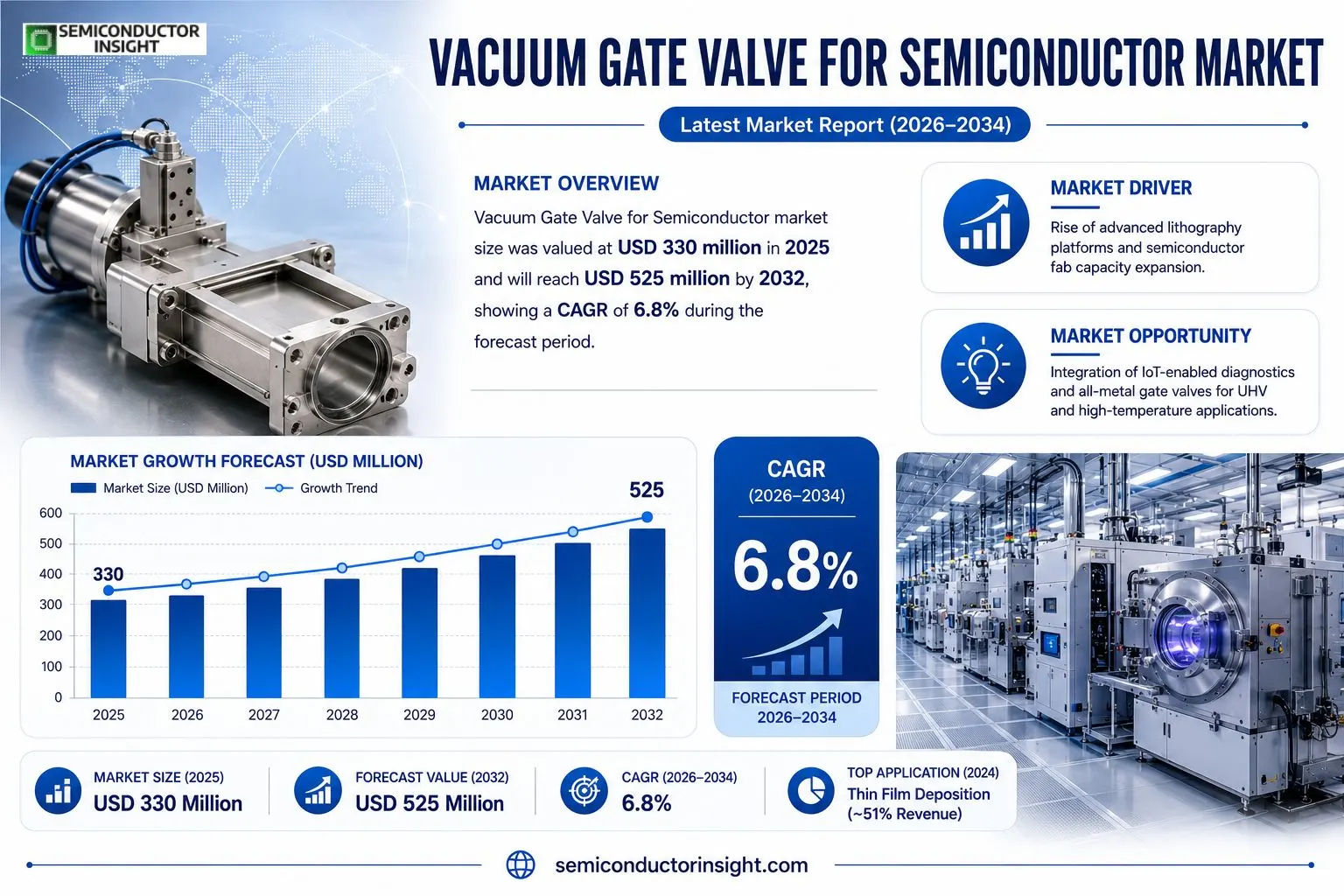

Vacuum Gate Valve for Semiconductor market size was valued at USD 330 million in 2025 and will reach USD 525 million by 2032, showing a CAGR of 6.8% during the forecast period.

In this report, “Vacuum Gate Valve for Semiconductor” refers to a vacuum isolation valve assembly used in semiconductor manufacturing equipment that opens and closes a flow path by a linear “gate” (plate) motion, providing fast, low‑leak, low‑particle isolation between vacuum volumes. The scope covers chamber/load‑lock gate valves, slit/transfer gate valves and all‑metal gate valves designed for UHV or high‑cycle operation, while excluding non‑gate vacuum valves and spare components.The market expands because semiconductor fabs continue investing in advanced process tools that require reliable vacuum isolation. Faster cycle times and stricter particle‑control standards push manufacturers toward pneumatic gate designs, which now account for over 98% of sales revenue. Emerging applications such as EUV lithography and high‑aspect‑ratio etching create additional demand for all‑metal gate solutions capable of withstanding bake‑out temperatures.

MARKET DRIVERS

Rise of Advanced Lithography Platforms

The adoption of extreme ultraviolet (EUV) lithography has created a demand for ultra‑clean vacuum environments. Vacuum Gate Valve for Semiconductor Market suppliers that can guarantee sub‑ppm particle release are seeing orders expand as fabs upgrade to 7 nm and beyond nodes.

Energy‑Efficiency Mandates

Utilities and corporate sustainability goals are pressuring chip manufacturers to cut process‑related power draw. Modern gate valves that incorporate low‑friction seals and smart actuation reduce cycle energy by up to 12 %, making them attractive investments for cost‑conscious fabs.

➤ Customers are prioritising valves that combine leak‑tight performance with predictive maintenance analytics, a shift that elevates total‑ownership value over upfront price.

Meanwhile, regional semiconductor expansion in Asia‑Pacific is fueling capacity additions at a pace that outstrips legacy valve inventories. Companies that can scale production while maintaining stringent contamination control are positioning themselves as preferred partners.

MARKET CHALLENGES

Stringent Contamination Controls

Fabrication lines operate under particle‑count thresholds that are often one order of magnitude lower than in traditional vacuum applications. Even minor outgassing from valve materials can trigger yield losses, prompting fabs to enforce rigorous qualification protocols that extend lead times.

Other Challenges

Supply‑Chain Volatility

The semiconductor supply chain remains sensitive to geopolitics and raw‑material shortages. Limited availability of high‑purity alloys for valve bodies can delay projects, especially when manufacturers rely on a narrow set of certified suppliers.

MARKET RESTRAINTS

Capital‑Intensive Retrofit Requirements

Upgrading existing vacuum infrastructure to accommodate next‑generation gate valves often entails costly pipe‑line modifications and system re‑validation. Many mid‑size fabs defer such investments until a clear ROI can be quantified, tempering short‑term market acceleration.

MARKET OPPORTUNITIES

Integration of IoT‑Enabled Diagnostics

Embedding sensors that monitor valve position, pressure differentials, and seal health opens a pathway for predictive maintenance services. Vendors that bundle these capabilities with the Vacuum Gate Valve for Semiconductor Market product line can unlock recurring revenue streams while helping fabs reduce unexpected downtime.

Vacuum Gate Valve for Semiconductor Market Trends

Pneumatic Dominance and Concentrated Supplier Landscape

The Vacuum Gate Valve for Semiconductor Market recorded revenue of roughly US$330 million in 2025 and is forecast to climb to about US$525 million by 2032. Unit pricing settled near US$2,828, supporting sales of 127,600 valves that year. Pneumatic devices accounted for 98.75 % of revenue and 98.14 % of volume in 2024, a share that is expected to edge upward toward 99 % by the early 2030s. This concentration reflects manufacturers’ preference for high‑speed, low‑leak actuation suited to high‑throughput fab lines. Meanwhile, the top five firmsVAT Group AG, V‑TEX Corporation, PRESYS, HVA, and Pfeiffer Vacuumcombined for 80.07 % of sales, with VAT alone holding 38.24 % and V‑TEX 29.24 %. The competitive environment therefore centers on a few large players dictating technology road‑maps and pricing structures.

Other Trends

Application Concentration in Deposition and Etching

Thin‑film deposition equipment captured just under 51 % of 2024 revenue, while etching tools contributed roughly 31 %. Together they drive more than 80 % of demand for gate valves, underscoring the importance of chamber‑door and load‑lock isolation in processes where particle contamination must be minimized. The remaining nicheion implantation, electron‑beam metrology, photolithography, and cleaning stationsexhibits annual growth rates north of 5 % from 2025 onward. This modest but steady expansion signals that equipment vendors are broadening process capabilities, prompting valve manufacturers to fine‑tune sealing performance for both high‑vacuum (HV) and ultra‑high‑vacuum (UHV) regimes.

Emerging Niche and All‑Metal Valve Opportunities

All‑metal gate valves, designed for bake‑out and high‑temperature cycles, are gaining relevance in advanced nodes that require UHV conditions. Although they represent a small fraction of current shipments, their adoption is accelerating as fab operators pursue tighter process windows and longer equipment lifespans. Vendors that can integrate robust metal sealing with the prevailing pneumatic actuation platform are positioned to capture incremental revenue from specialty applications such as electron‑beam inspection and next‑generation lithography. The broader implication for the Vacuum Gate Valve for Semiconductor Market is a shift from volume‑driven sales toward value‑added solutions that address specific performance criteria, encouraging strategic investments in material science and precision machining.

COMPETITIVE LANDSCAPE

Key Industry Players

Vacuum Gate Valve for Semiconductor – Competitive Overview

The market remains tightly concentrated around a handful of manufacturers that dominate revenue streams and set technical benchmarks. VAT Group AG, headquartered in Switzerland, accounts for roughly 38 % of sales, leveraging its extensive UHV‑grade product line and deep integration with major equipment OEMs. V‑TEX Corporation follows with a 29 % share, distinguishing itself through a broad portfolio of pneumatic gate valves and aggressive pricing in high‑volume wafer‑fab segments. Together, these two firms capture more than two‑thirds of total market value, creating a barrier to entry for newcomers. The remaining top‑five cohortPRESYS Co., Ltd, HVA, and Pfeiffer Vacuumsplits the balance of roughly 42 % and sustains a competitive dynamic where scale, reliability, and after‑sales service dictate client loyalty. This concentration reflects the capital‑intensive nature of valve development, the criticality of particle‑free operation, and the limited differentiation possible within the core pneumatic architecture.Beyond the dominant tier, several niche players address specialized applications or price‑sensitive segments. SMC Corporation and MKS Instruments supply cost‑effective pneumatic solutions that appeal to R&D labs and mid‑range production lines, while HTC Vacuum focuses on customized all‑metal designs for UHV environments where bake‑out cycles are routine. Science Probe Co., Ltd and i‑San Inc have carved out market share in transfer‑slit and wafer‑door valves, leveraging unique geometries to meet tight alignment tolerances. Companies such as Kunshan Kinglai Hygienic Materials, Sino Multi‑Micro Technology, and Trust Clean Tech serve the growing demand in mainland China and Taiwan, often competing on localized support and rapid delivery. Their collective presence ensures a diversified supply base, mitigating risk for fab operators and fostering incremental innovation in sealing materials and actuation mechanisms.

List of Key Vacuum Gate Valve for Semiconductor Companies Profiled

- VAT Group AG

- VAT Group AG

- V‑TEX Corporation

- V‑TEX Corporation

- PRESYS Co., Ltd

- HVA

- Pfeiffer Vacuum

- SMC Corporation

- MKS Instruments

- HTC Vacuum

- Science Probe Co., Ltd

- Kunshan Kinglai Hygienic Materials

- i‑San Inc

- Sino Multi‑Micro Technology Co., Ltd

- Trust Clean Tech

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Pneumatic Gate Valves dominate the semiconductor valve portfolio because they deliver rapid actuation, repeatable positioning, and reliable sealing under high‑vacuum conditions.

|

| By Application |

|

Thin Film Deposition represents the core application driver because gate valves enable rapid isolation of deposition chambers, preserving ultra‑high vacuum integrity required for uniform thin‑film growth.

|

| By End User |

|

Equipment Manufacturers drive the specification of gate valves, prioritizing reliability, integration simplicity, and compliance with ultra‑high vacuum standards.

|

Regional Analysis: Vacuum Gate Valve for Semiconductor Market

Asia‑Pacific

Taiwan’s fab clusters and South Korea’s integrated circuit parks serve as magnets for vacuum valve suppliers seeking proximity to high‑volume fabs. The concentration of design houses and equipment integrators creates a virtuous loop where design‑for‑manufacturability feedback shortens development cycles, allowing valve makers to iterate on sealing materials and actuation speed tailored to regional process windows.

Recent disruptions highlighted the need for diversified component sourcing. Vendors are establishing secondary production lines in Singapore and Malaysia, reducing dependency on a single node and ensuring that critical vacuum gate valve assemblies remain available even amid logistical bottlenecks.

Several economies have introduced subsidies for equipment that lowers wafer contamination rates. By aligning valve performance metrics with these incentive structures, manufacturers can present a compelling value proposition that resonates with fabs pursuing cost‑per‑die efficiency gains.

The shift toward heterogeneous integration and 3‑D stacking in the region amplifies demand for vacuum gate valves capable of rapid cycling and extreme vacuum levels, prompting R&D teams to explore ceramic‑based sealing faces that tolerate frequent pressure differentials without performance loss.

North America

North America remains a strong secondary market, anchored by the United States’ mature fab ecosystem and a steady pipeline of specialty foundries focused on advanced packaging. Here, the Vacuum Gate Valve for Semiconductor Market benefits from a technology‑centric purchasing culture, where buyers evaluate valve performance against stringent reliability standards set by industry consortia. Domestic suppliers leverage proximity to R&D labs in California and Texas to co‑develop customized actuation mechanisms that meet the exacting vacuum thresholds demanded by next‑generation lithography. While growth rates lag behind Asia‑Pacific, the region’s emphasis on high‑value, low‑volume production ensures that premium‑priced valve solutions continue to find a receptive audience.

Europe

Europe’s semiconductor footprint, concentrated in Germany, the Netherlands, and France, exhibits a measured yet sophisticated demand for vacuum gate valves. The market is shaped by the EU’s strategic emphasis on supply‑chain sovereignty, prompting local fabs to source components that comply with stringent environmental and safety regulations. German valve manufacturers, in particular, are capitalising on this climate by offering modular designs that can be retrofitted into existing equipment, extending asset life while adhering to the region’s circular‑economy goals. Collaborative research projects funded by the European Commission further embed valve innovation within the continent’s broader push toward photonics‑enabled chips.

South America

South America’s semiconductor activity is nascent, yet Brazil’s emerging microelectronics clusters signal a growing appetite for dependable vacuum gate valve technology. Local fab initiatives, often supported by government‑backed technology parks, are prioritising equipment that reduces contamination risk, a critical factor for yield improvement in a market still establishing its quality standards. Suppliers see an opportunity to introduce entry‑level valve platforms that balance performance with cost, facilitating technology transfer and encouraging domestic talent development within the Vacuum Gate Valve for Semiconductor Market.

Middle East & Africa

The Middle East & Africa region, while still peripheral to wafer production, is witnessing a gradual infusion of semiconductor assembly lines, especially in Israel’s innovation hubs and the United Arab Emirates’ smart‑manufacturing initiatives. In these environments, the Vacuum Gate Valve for Semiconductor Market is valued for its adaptability to modular clean‑room configurations and its ability to meet the rigorous vacuum specifications demanded by precision sensor fabrication. Early‑stage collaborations between regional equipment integrators and multinational valve providers are laying the groundwork for a supply chain that could support future expansion as local demand for advanced electronics rises.

Report Scope

This market research report provides a comprehensive analysis of the Vacuum Gate Valve for Semiconductor Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Vacuum Gate Valve for Semiconductor Market?

-> Vacuum Gate Valve for Semiconductor Market was valued at USD 330 million in 2025 and is expected to reach USD 525 million by 2032, at a CAGR of 6.8% during the forecast period.

Which key companies operate in Vacuum Gate Valve for Semiconductor Market?

-> Key players include VAT Group AG, V‑TEX Corporation, PRESYS Co., Ltd, HVA, and Pfeiffer Vacuum, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for advanced semiconductor manufacturing equipment, expanding thin‑film deposition and etching applications, and increasing adoption of all‑metal gate valves for UHV and high‑temperature processes.

Which region dominates the market?

-> Asia-Pacific leads the market due to the concentration of semiconductor fabs and the rapid growth of related equipment manufacturers, while Europe maintains a strong presence in high‑precision tooling.

What are the emerging trends?

-> Emerging trends include the shift toward pneumatic valve dominance (>98% of revenue), the development of all‑metal gate valves for ultra‑high vacuum (UHV) applications, and integration of smart monitoring for predictive maintenance.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...