Semiconductor Capacitance Diaphragm Gauge (CDG) Market Insights

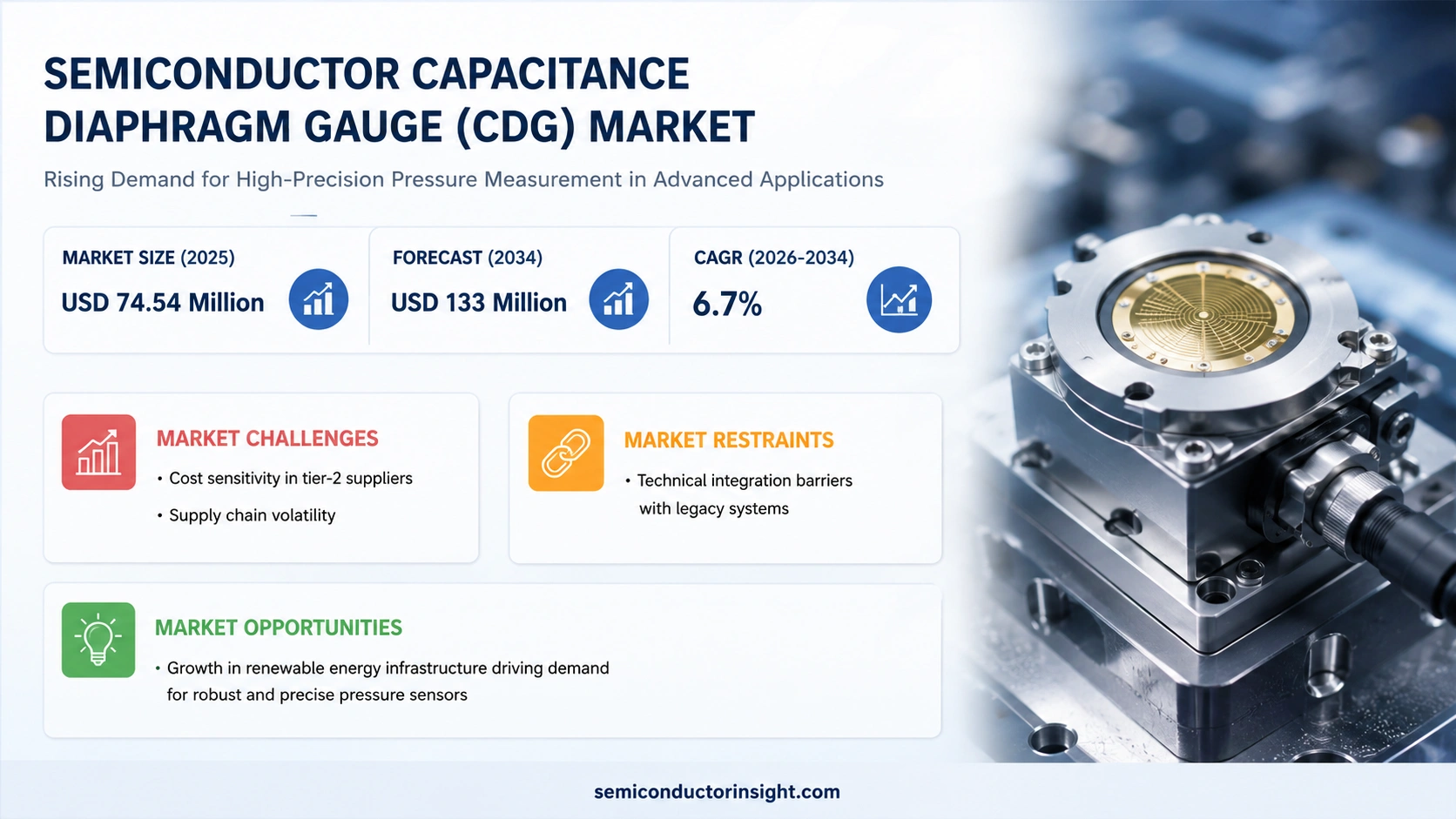

Global Semiconductor Capacitance Diaphragm Gauge (CDG) market size was valued at USD 74.54 million in 2025 and will reach USD 133 million by 2034, exhibiting a CAGR of approximately 6.7 % over the period.

A Semiconductor Capacitance Diaphragm Gauge (CDG) is a high‑accuracy vacuum pressure sensor widely used in semiconductor manufacturing and other precision industrial applications.

It measures pressure by detecting the deflection of a thin, corrosion‑resistant diaphragm,typically ceramic or metal,through changes in capacitance between the diaphragm and a fixed electrode.

As pressure varies, the diaphragm flexes, altering capacitance, which is converted into an electrical signal for precise readings.

CDGs provide excellent linearity, stability and gas‑independent performance across ranges from milliTorr to atmospheric pressure, making them valuable in processes such as etching, CVD and PVD.

Advanced models incorporate temperature control, digital interfaces such as EtherCAT or PROFIBUS and diagnostic capabilities that enhance reliability in critical vacuum systems.

MARKET DRIVERS

Automotive Emissions Regulations

Stringent emissions standards across Europe and North America have forced OEMs to adopt more precise pressure‑sensing solutions. Semiconductor Capacitance Diaphragm Gauge (CDG) Market benefits because CDG sensors deliver superior resolution and temperature stability, enabling tighter control of exhaust‑gas recirculation loops.

Miniaturization of Portable Devices

The push for thinner smartphones and wearables creates a demand for ultra‑compact pressure sensors. CDG technology, with its low profile and high accuracy, aligns with this trend, allowing manufacturers to integrate pressure monitoring without compromising device ergonomics.

➤ “Design engineers cite CDG’s low power draw as a decisive factor when targeting battery‑operated products.”

Overall, the convergence of regulatory pressure and consumer‑driven size constraints is reshaping procurement decisions, positioning Semiconductor Capacitance Diaphragm Gauge (CDG) Market as a preferred choice for next‑generation equipment.

MARKET CHALLENGES

Cost Sensitivity in Tier‑2 Suppliers

Smaller component distributors often prioritize unit cost over performance, limiting adoption of CDG sensors that carry a premium price relative to traditional piezoresistive devices. This price differential can deter bulk purchases in cost‑driven segments.

Other Challenges

Supply Chain Volatility

Recent disruptions in semiconductor wafer supplies have introduced lead‑time uncertainties, making it difficult for end‑users to plan inventory for CDG‑based solutions.

MARKET RESTRAINTS

Technical Integration Barriers

Many legacy systems rely on analog output formats, whereas CDG devices frequently require digital interfaces and calibration algorithms. Upgrading existing platforms to accommodate these requirements can entail significant engineering effort, slowing market penetration.

MARKET OPPORTUNITIES

Growth in Renewable Energy Infrastructure

Wind turbines and solar inverters increasingly need precise pressure monitoring for hydraulic and cooling systems. The robustness of CDG sensors in harsh environments makes them attractive for these applications, opening a pathway for new contracts and diversification beyond traditional automotive and consumer markets.

Semiconductor Capacitance Diaphragm Gauge (CDG) Market Trends

Supply‑Chain Consolidation and Margin Pressure

Semiconductor Capacitance Diaphragm Gauge (CDG) Market recorded revenue of roughly $74.5 million in 2025 and is slated to reach about $118 million by 2032. Unit shipments of 77,500 in 2025 translated into an average selling price near $1,053, indicating a modest premium for high‑precision variants. A tightening of the upstream component base,especially for high‑Ni alloys and ceramic seals,has forced the leading manufacturers to lock in long‑term contracts, thereby reducing procurement volatility but also limiting pricing flexibility. As major fab expansions under U.S. CHIPS and EU Chips Act incentives lift the overall demand for vacuum metrology, profit margins are increasingly dictated by the ability to control clean‑room labor and calibration overhead rather than raw material costs. Companies that preserve a tightly‑controlled core assembly while outsourcing only non‑critical housings are preserving gross margins in the 55‑70 % range for premium heated gauges.

Other Trends

Manufacturing Model and Cost Structure

The prevailing “in‑house core + selective outsourcing” approach reflects the high‑mix, low‑volume nature of CDG production. Core activities,diaphragm fabrication, capacitor electrode alignment, and thermal‑control integration,remain inside the OEM’s clean‑room environment to safeguard IP and traceability. Outsourced items, such as housing extrusion and standard connectors, are limited to components that do not affect sensor stability. This configuration yields a gross margin spread of roughly 40‑60 % for standard models, while premium heated or corrosion‑resistant versions benefit from additional value‑added services like remote diagnostics and bundled controller packages. The calibration step, which includes helium leak testing and multi‑point certification, is the decisive cost driver and a key differentiator for after‑sales revenue streams.

Demand Shift Toward Integrated Digital Controls

Downstream, fabs are moving from a purely installation‑focused mindset to a yield‑and‑uptime‑centric strategy. In etch and CVD chambers, the need for micro‑drift control and continuous remote monitoring has turned CDGs into networked process‑control nodes rather than isolated sensors. Digital interfaces such as EtherCAT and PROFIBUS, together with built‑in diagnostic alerts, enable predictive maintenance and reduce unplanned downtime. This evolution fuels growth in the MRO segment,refurbishment, recalibration, and spare parts now represent a larger share of the revenue mix. Moreover, the preference for heated and corrosion‑resistant designs is accelerating as newer fabs target tighter pressure tolerances across a broader temperature envelope. The cumulative effect is a more resilient demand base that balances original equipment purchases with recurring service contracts.

COMPETITIVE LANDSCAPE

Key Industry Players

Semiconductor Capacitance Diaphragm Gauge (CDG) Competitive Landscape

MKS Instruments and INFICON together command a sizable portion of CDG revenue, each leveraging a vertically integrated production model that keeps the sensing‑head core within proprietary facilities. Their ability to combine clean‑room assembly, in‑house burn‑in testing, and traceable calibration under a single roof translates into gross margins that routinely exceed 50 % for premium heated gauges. Both firms have expanded their service networks to include remote diagnostics and automated recalibration, turning spare‑parts sales into a recurring revenue stream. The strategic emphasis on digital interfaces such as EtherCAT and PROFIBUS has also positioned them as preferred suppliers for new‑fab installations where networked process control is mandatory.

Beyond the leaders, a cluster of specialized manufacturers sustains market depth. Atlas Copco (through Leybold and Edwards), Pfeiffer Vacuum, and Setra Systems focus on rugged, corrosion‑resistant designs for legacy equipment, while Canon Anelva and Brooks Instrument supply compact, low‑power units for niche sub‑fab applications. ULVAC and Azbil excel in heated‑type gauges that meet tight temperature‑drift specifications, and Agilent‑owned MKS‑Affiliated brands provide integrated metrology suites. Smaller players such as Kurt J. Lesker, EBARA, ASAIR, Atovac and SATO VAC capture niche segments including ultra‑low‑drift ceramic diaphragms and bespoke connector kits, often thriving on close OEM partnerships and localized after‑sales support.

List of Key Semiconductor Capacitance Diaphragm Gauge Companies Profiled

- MKS Instruments

- INFICON

- Atlas Copco (Leybold & Edwards)

- Pfeiffer Vacuum

- Setra Systems

- Canon Anelva

- Brooks Instrument

- ULVAC

- Azbil

- Agilent

- Kurt J. Lesker

- EBARA

- ASAIR

- Atovac

- SATO VAC

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Heated Type

|

| By Application |

|

Deposition

|

| By End User |

|

Semiconductor fabs

|

| By Technology Trend |

|

Digital Integration

|

| By Service Offering |

|

Calibration Services

|

Regional Analysis: Semiconductor Capacitance Diaphragm Gauge (CDG) Market

North America

Collaborative R&D hubs in Silicon Valley and the Midwest funnel cutting‑edge MEMS expertise into gauge designs, shortening the concept‑to‑prototype interval. Early adopters test integrated sensor platforms that embed CDG elements directly onto wafer carriers, expanding functional density without compromising accuracy.

Recent disruptions have prompted manufacturers to diversify component sourcing, establishing secondary silicon wafer suppliers in Canada and Mexico. This redundancy lessens exposure to single‑point failures and sustains production cadence for high‑volume customers.

Tightened emissions standards for cleanroom operations compel fabs to adopt more precise pressure‑control instruments. The resulting regulatory climate incentivizes the deployment of CDG technology as a compliance‑enabling tool.

Tier‑1 semiconductor makers prioritize gauges that integrate seamlessly with existing metrology software, driving demand for open‑API solutions. Vendors that deliver robust data interoperability see accelerated contract cycles.

Europe

European fabs benefit from a strong heritage in precision engineering, fostering a market where CDG units are valued for their reliability under stringent quality regimes. Collaborative standards bodies across Germany, France and the Netherlands harmonize calibration protocols, reducing variability between sites. Automotive and aerospace suppliers in the region are integrating gauges into supply‑chain quality checks, emphasizing traceability. The confluence of high‑skill labor and coordinated regulatory frameworks sustains a steady infusion of projects that explore ultra‑stable pressure monitoring for emerging quantum‑chip production lines.

Asia‑Pacific

The Asia‑Pacific region is characterized by rapid capacity expansion in semiconductor foundries, particularly in Taiwan, South Korea and Singapore. While the market remains price‑sensitive, manufacturers are shifting focus toward value‑added features such as on‑chip diagnostics that leverage CDG technology. Local government incentives for high‑technology clusters encourage joint ventures between gauge makers and equipment integrators, accelerating the rollout of hybrid metrology suites. Cultural emphasis on iterative engineering cycles means that feedback from pilot lines quickly informs product refinement, positioning the region as a testing ground for next‑generation sensor architectures.

South America

South American semiconductor activity, though modest in scale, is bolstered by niche applications in aerospace and defense that demand high‑precision pressure measurement. Brazil’s expanding research universities collaborate with multinational gauge suppliers to tailor CDG solutions for tropical climate testing chambers. The region’s growing focus on domestic component production aims to reduce reliance on imported metrology tools, spurring modest but steady adoption of locally supported gauge platforms.

Middle East & Africa

In the Middle East & Africa, emerging semiconductor initiatives are anchored by sovereign wealth funds channeling capital into advanced manufacturing parks. Early adopters in the United Arab Emirates and South Africa are seeking CDG technology to support high‑purity material handling for solar‑cell production. Partnerships with global gauge firms emphasize knowledge transfer, ensuring that local engineers acquire the expertise required to maintain ultra‑stable vacuum environments. The strategic intent is to build a self‑sustaining ecosystem that can eventually service neighboring markets.

Report Scope

This market research report provides a comprehensive analysis of the Semiconductor Capacitance Diaphragm Gauge (CDG) Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Semiconductor Capacitance Diaphragm Gauge (CDG) Market?

-> Semiconductor Capacitance Diaphragm Gauge (CDG) Market was valued at USD 74.54 million in 2025 and is expected to reach USD 118 million by 2032, at a CAGR of 6.7% during the forecast period.

Which key companies operate in Semiconductor Capacitance Diaphragm Gauge (CDG) Market?

-> Key players include MKS Instruments, INFICON, Atlas Copco (Leybold and Edwards), Pfeiffer Vacuum, Setra Systems, Canon Anelva, Brooks Instrument, ZHENTAI INSTRUMENT, ULVAC, Azbil, Agilent, Kurt J. Lesker, EBARA, ASAIR, Atovac, SATO VAC.

What are the key growth drivers?

-> Key growth drivers include advanced‑node and advanced‑packaging expansions, productivity upgrades in existing fabs, government incentives such as U.S. CHIPS and EU Chips Act, and rising demand for high‑accuracy vacuum pressure control in etching, CVD/ALD and PVD processes.

Which region dominates the market?

-> Asia‑Pacific leads the market, driven by extensive semiconductor fab activity in China, Japan and South Korea, while North America and Europe also hold significant shares.

What are the emerging trends?

-> Emerging trends include shift from installation‑led to yield‑and‑uptime‑led demand, increased digital connectivity and remote diagnostics, networked CDG nodes in process‑control loops, and growing adoption of premium heated and corrosion‑resistant designs.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...