RF Matching Unit Market Insights

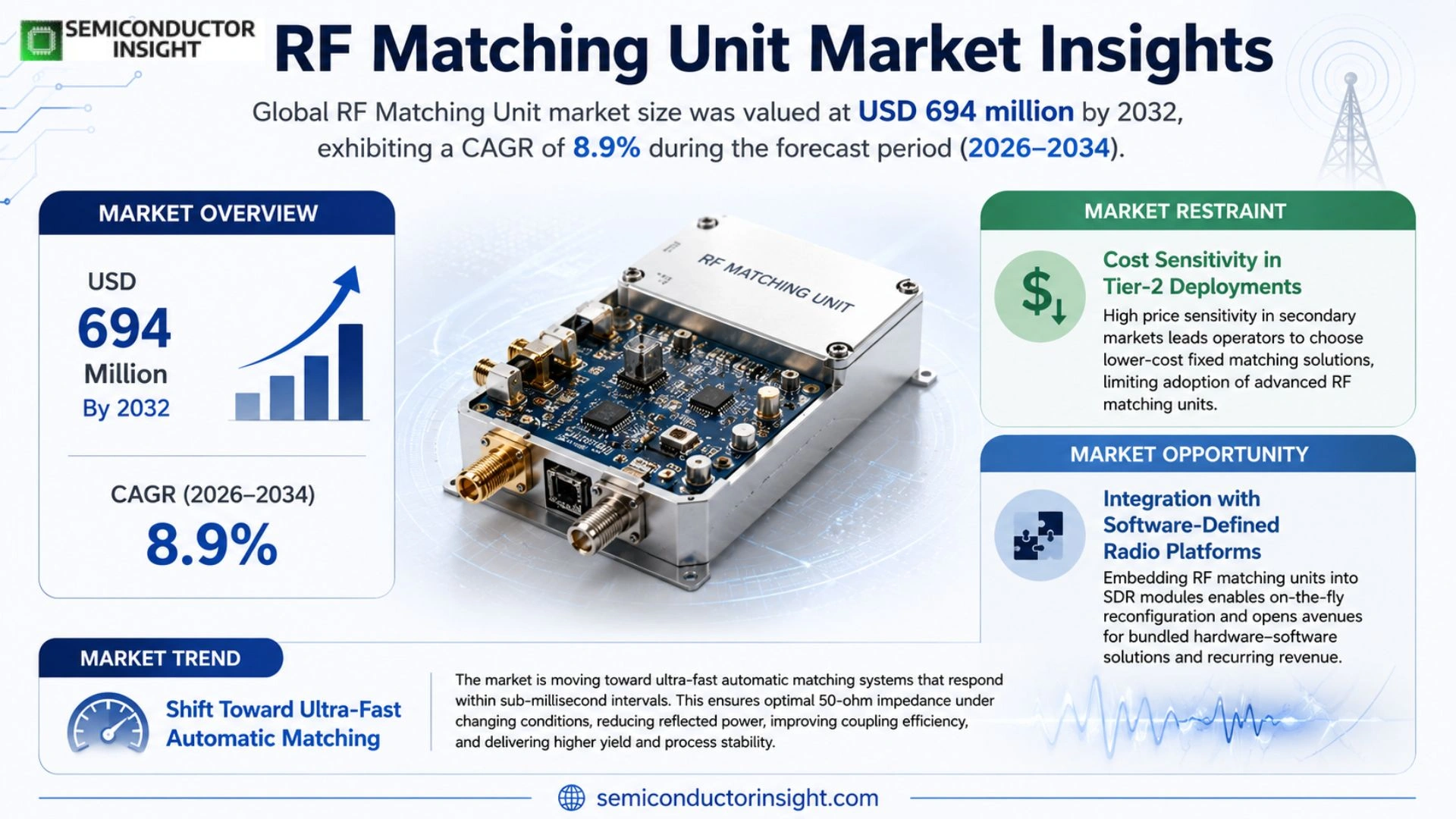

Global RF Matching Unit market size was valued at USD 385 million in 2025. The market is projected to grow from USD 385 million in 2025 to USD 694 million by 2032, exhibiting a CAGR of 8.9% during the forecast period.

RF Matching Unit is the core power‑delivery and impedance‑tuning component placed between an RF generator and a plasma load. It maintains a near‑50 Ω match despite dynamic changes in load impedance caused by plasma ignition or gas composition shifts.

Growth stems from rising fab‑equipment spend under policies such as the EU Chips Act and US CHIPS Act plus demand for high‑speed automatic matching with dual‑frequency control. Leading suppliers,including Advanced Energy Industries Inc., MKS Instruments Inc., Comet AG,are adding sub‑millisecond response algorithms and localized support.

MARKET DRIVERS

Rising Demand for 5G Infrastructure

The rollout of 5G networks requires precise impedance matching across a broad frequency spectrum. RF Matching Unit Market suppliers that can deliver compact, low‑loss solutions are seeing heightened interest from mobile operators seeking to reduce site‑level tuning time. This pressure incentivizes manufacturers to refine tuning algorithms and expand product families that address both sub‑6 GHz and millimeter‑wave bands.

IoT and Edge‑Computing Expansion

Proliferation of connected sensors and edge compute nodes creates a mosaic of antenna configurations. When each node must operate efficiently in congested spectrum, RF matching units become a cost‑effective way to ensure signal integrity without custom‑built matching networks. The trend encourages OEMs to adopt modular units that can be programmed post‑deployment, reducing engineering cycles.

➤ Key driver: Streamlined antenna tuning lowers total cost of ownership for telecom and industrial deployments

Regulatory emphasis on spectrum efficiency, especially in densely populated urban zones, forces network planners to adopt technologies that minimize return loss. Vendors that bundle real‑time monitoring with adaptive matching hardware are positioned to capture a larger share of RF Matching Unit Market, as operators look for solutions that can react to dynamic load conditions.

MARKET CHALLENGES

Technical Complexity of Multi‑Band Designs

Designers must accommodate divergent impedance requirements while preserving linearity and low noise. The engineering effort needed to develop a unit that spans from 300 MHz to 6 GHz often translates into higher upfront R&D spend, limiting the number of players able to compete effectively.

Other Challenges

Supply Chain Bottlenecks

Component shortages, particularly for high‑Q inductors and precision capacitors, have elongated lead times. This pressure forces system integrators to hold larger inventories, which can suppress demand for new matching solutions in the short term.

MARKET RESTRAINTS

Cost Sensitivity in Tier‑2 Deployments

Operators expanding coverage in secondary markets often prioritize absolute cost over performance nuance. When the price differential between a fixed matching network and an adaptive RF matching unit is perceived as excessive, procurement decisions tilt toward the cheaper, albeit less flexible, option, curbing broader adoption of advanced matching technology.

MARKET OPPORTUNITIES

Integration with Software‑Defined Radio Platforms

Emerging software‑defined radio (SDR) ecosystems rely on programmable front‑ends that can reconfigure on the fly. Embedding RF matching units directly into SDR modules opens a pathway for vendors to sell bundled hardware‑software kits, creating a recurring revenue stream as customers upgrade firmware to exploit new frequency bands.

RF Matching Unit Market Trends

Shift Toward Ultra‑Fast Automatic Matching

RF Matching Unit Market is moving from mechanically tuned devices to high‑speed automatic systems that respond within sub‑millisecond intervals. This evolution is driven by the need to keep plasma impedance close to the 50‑ohm optimum as load conditions change during ignition, gas flow shifts, and material transitions. Faster response times reduce reflected power, improve coupling efficiency, and tighten process repeatability, which directly translates into higher wafer yield for advanced logic and memory nodes. Vendors such as Advanced Energy, Comet, and TRUMPF have integrated dual‑frequency synchronous control, broadband sensing, and real‑time diagnostics into their platforms, turning the matching unit into an active process‑control node rather than a passive power accessory.

Other Trends

Supply‑Side Consolidation

European, U.S., and Japanese manufacturers continue to dominate the high‑end segment, leveraging decades of know‑how in ultrafast tuning algorithms and system‑level integration. At the same time, Korean and Chinese suppliers are gaining traction by offering localized engineering support, rapid customization, and cost‑effective options for mature‑node equipment. The result is a two‑tier market where global leaders serve advanced‑packaging and compound‑semiconductor applications, while regional players expand in broader plasma tool categories and retrofit projects. This structure discourages a monopoly and encourages competitive innovation across the value chain.

Demand‑Side Drivers

Investment cycles in wafer fabs, reinforced by policy initiatives such as the European Chips Act and the U.S. CHIPS Act, are inflating the demand for RF power delivery solutions. As 300‑mm fab equipment spending climbs, equipment makers are not only procuring new matching units for fresh tool builds but also retrofitting existing lines to achieve tighter process windows required by dual‑frequency and pulsed plasma techniques. The multiplier effect of a high‑performance matching unit,enhancing ignition success, reducing downtime, and enabling advanced data capture,creates a premium market segment where software upgrades and algorithmic licensing add recurring revenue streams. Consequently, RF Matching Unit Market will see growth sourced from both capital equipment purchases and value‑added service contracts.

COMPETITIVE LANDSCAPE

Key Industry Players

RF Matching Unit Market: Competitive Overview

The high‑end segment of RF Matching Unit market is anchored by a handful of global technology houses that combine deep RF generator expertise with sophisticated matching algorithms. Advanced Energy Industries, MKS Instruments, and TRUMPF dominate tool‑makers targeting advanced‑node etch and deposition platforms, where sub‑millisecond response, dual‑frequency coordination, and real‑time diagnostics are mandatory. These firms leverage extensive semiconductor OEM relationships to supply integrated power‑delivery suites, often bundling matching networks with proprietary control software. Their pricing reflects the added value of reduced reflected power, higher process yield, and faster cycle times, which makes the hardware an enabler of equipment differentiation rather than a cost‑center. The competitive pressure among these leaders centers on algorithmic refinement, V/I sensing accuracy, and the breadth of industrial communication standards supported.

Below the premium tier, a diverse set of regional manufacturers fills niche and cost‑sensitive opportunities. Companies such as Comet (Germany), DAIHEN (Japan), Kyosan (Japan), and TDK (Japan) offer robust platforms that emphasize reliability and ease of integration, catering to mid‑range fabs and specialty plasma tools. Asian players,including Asendia, RF Power Tech, Aurasky, AENI, and YOUNGSIN‑RF,capitalize on local engineering support, rapid customization, and competitive pricing to win contracts for mature‑node equipment, retrofit upgrades, and research‑lab installations. Korean firms like ADTEC Plasma Technology and Chinese enterprises such as SUNSAY GENERIC and Chengdu DSD extend the supply chain into emerging markets where localization requirements and service proximity are decisive factors. This two‑tier architecture creates a market where strategic partnerships and field service capabilities can be as influential as raw technical performance.

List of Key RF Matching Unit Companies Profiled

- Advanced Energy Industries, Inc.

- MKS Instruments, Inc.

- TRUMPF SE + Co. KG

- Comet AG

- TDK Corporation

- DAIHEN Corporation

- Kyosan Electric Manufacturing Co., Ltd.

- ADTEC Plasma Technology Co., Ltd.

- Asendia Co., Ltd.

- RF Power Tech

- AENI

- Beijing AURASKY Electronics Co., Ltd.

- YOUNGSIN‑RF Co., Ltd.

- Generator Research Limited

- Chengdu DSD Digital Technology Co., Ltd.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Automatic is emerging as the dominant choice because it delivers sub‑millisecond tuning, closed‑loop coordination with the RF generator, and advanced diagnostics that support real‑time process stability.

|

| By Application |

|

Etching and Removal leads the application landscape as manufacturers prioritize matching speed to sustain plasma ignition and uniform etch profiles.

|

| By End User |

|

Semiconductor fabs command the most sophisticated matching solutions because process yield hinges on precise energy coupling.

|

| By Frequency Architecture |

|

Dual Frequency is gaining traction as equipment migrates toward tighter process windows and higher throughput.

|

| By Integration Level |

|

Integrated matchbox + controller is perceived as the most value‑adding configuration because it blends rapid tuning with on‑board analytics.

|

Regional Analysis: RF Matching Unit Market

North America

Defense modernization programs and carrier‑grade 5G deployments create persistent demand for high‑efficiency matching networks. OEMs seek units that can compress insertion loss while accommodating tighter antenna tolerances, a requirement that accelerates product cycles and drives R&D spend in the region.

The FCC’s spectrum repurposing agenda and the Department of Defense’s stringent electromagnetic compatibility standards shape design parameters. Compliance pathways are well‑defined, enabling suppliers to certify matching units faster than in less regulated markets.

A handful of legacy players coexist with agile startups that specialize in miniaturized, broadband solutions. Strategic collaborations between chip designers and packaging firms are reshaping value chains, pushing incumbents to broaden their portfolio beyond traditional narrow‑band units.

The rise of satellite‑based broadband constellations introduces a new tier of high‑frequency matching requirements. Suppliers that can deliver low‑mass, thermally stable units stand to capture a growing slice of this nascent segment.

Europe

European activity in RF Matching Unit Market reflects a strategic pivot toward sustainability and spectrum efficiency. Operators are migrating to shared‑infrastructure models, compelling manufacturers to supply components that enable carrier aggregation across adjacent bands. Concurrently, the EU’s emphasis on reducing electromagnetic emissions forces designers to fine‑tune impedance matching, which in turn raises the bar for component quality. aerospace programs in France and the United Kingdom also sustain a steady demand for high‑reliability units that can survive harsh temperature cycles, reinforcing Europe’s role as a hub for precision engineering. The combined effect of policy‑driven efficiency targets and a strong legacy aerospace sector fuels a nuanced market where customization and compliance are paramount.

Asia‑Pacific

Asia‑Pacific’s ascent in RF Matching Unit Market is driven by aggressive mobile network expansion and a burgeoning consumer electronics segment. Nations such as China, India, and South Korea are deploying dense small‑cell networks to meet ever‑growing data consumption, a scenario that necessitates compact matching units capable of operating over wide frequency spans. In parallel, the region’s manufacturing ecosystem, characterized by high‑volume production capabilities, pressures suppliers to balance cost efficiency with performance. Emerging standards for private 5G and industrial IoT add another layer of demand, as factories seek bespoke matching solutions to reduce latency in mission‑critical communication links. This mix of scale, speed, and diversification renders the Asia‑Pacific market both opportunity‑rich and competitively intense.

South America

South America’s RF Matching Unit Market development is anchored in broadband penetration initiatives and localized defense procurement. Governments are investing in digital inclusion programs that extend mobile coverage into remote areas, a rollout that leans on rugged matching components capable of tolerating harsh environmental conditions. At the same time, defense modernization budgets in Brazil and Argentina stimulate demand for reliable RF front‑end modules used in radar and communication platforms. While overall market size remains modest relative to larger regions, the convergence of infrastructure projects and sovereign procurement creates a niche where suppliers with proven durability records can secure long‑term contracts.

Middle East & Africa

The Middle East & Africa exhibits a gradual but discernible rise in RF Matching Unit Market activity, largely spurred by oil‑rich economies investing in smart‑city and IoT infrastructure. Large‑scale petrochemical facilities are integrating wireless sensor networks that demand precise impedance matching to ensure signal fidelity in electrically noisy environments. In the Gulf, defense spending prioritizes advanced air‑defense systems, which require high‑power matching units to sustain radar performance under extreme temperatures. Africa’s nascent telecom expansion, driven by mobile‑first demographics, also pushes demand for cost‑effective yet reliable components. The region’s eclectic mix of high‑tech industrial applications and emerging consumer markets positions it as a frontier for tailored RF solutions.

Report Scope

This market research report provides a comprehensive analysis of the RF Matching Unit Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of RF Matching Unit Market?

-> RF Matching Unit Market was valued at USD 385 million in 2025 and is expected to reach USD 694 million by 2032, growing at a CAGR of 8.9% during the forecast period.

Which key companies operate in RF Matching Unit Market?

-> Key players include Advanced Energy Industries, Inc., MKS Instruments, Inc., Comet AG, TRUMPF SE + Co. KG, TDK Corporation, DAIHEN Corporation, Kyosan Electric Manufacturing Co., Ltd., Asendia Co., Ltd., RF Power Tech, Aurasky, among others.

What are the key growth drivers?

-> Key growth drivers include rising global wafer fab equipment investment, AI‑driven expansion of advanced logic and memory nodes, regional semiconductor localization policies (e.g., CHIPS Acts, European Chips Act), new equipment installations, process upgrades, and regional substitution of legacy tools.

Which region dominates the market?

-> Asia‑Pacific is the fastest‑growing and dominant region, driven by high concentration of semiconductor fabs in China, Japan, South Korea and Taiwan, while Europe and North America remain important secondary markets.

What are the emerging trends?

-> Emerging trends include ultrafast automatic matching with sub‑millisecond response, dual‑frequency synchronous control, broadband and multi‑frequency programmable architectures, AI/IoT‑enabled real‑time diagnostics, Smith‑chart visualization, and advanced V/I sensing integrated with industrial communication interfaces.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...