980nm SM Pump Laser Diode Market Insights

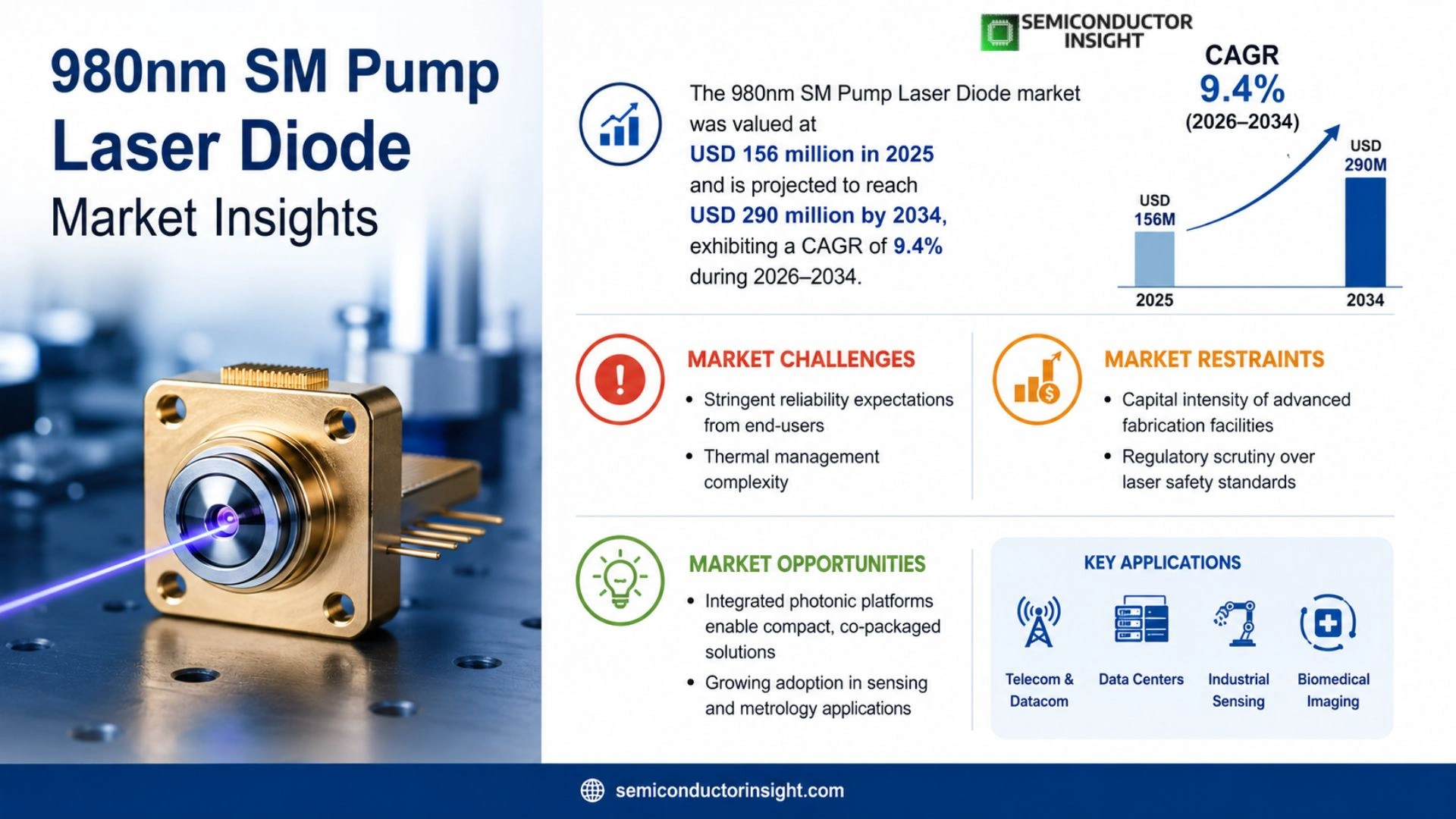

Global 980nm SM Pump Laser Diode market was valued at USD 156 million in 2025 and is projected to reach USD 290 million by 2034, exhibiting a CAGR of 9.4% during the forecast period.

The 980nm single‑mode pump laser diode is a semiconductor laser operating at a wavelength of 980 nm, emitting a single‑mode beam that pumps erbium‑doped fiber amplifiers (EDFA) or fiber lasers; its high beam quality, narrow divergence angle, low noise and stable high power improve gain efficiency in optical communication systems, industrial lasers and precision material processing.

MARKET DRIVERS

Rising Demand for High‑Efficiency Telecom Infrastructure

980nm SM Pump Laser Diode Market is gaining traction as telecom operators upgrade to dense‑wave‑division multiplexing (DWDM) platforms that require precise pump sources. Operators value the narrow linewidth and low noise of single‑mode devices, which translate into more reliable long‑haul transmission and reduced operational expenditures.

Growth of Data‑Center Interconnect (DCI) Links

Enterprises are extending their data‑center footprints across regions, creating a need for compact, energy‑saving amplification solutions. Single‑mode pump lasers at 980 nm fit seamlessly into silicon‑photonic modules, offering a path to higher bandwidth without a proportional rise in power draw.

➤ Manufacturers that integrate advanced epitaxial growth techniques are positioned to capture premium pricing because their devices sustain higher output powers while maintaining spectral purity.

Furthermore, the convergence of optical‑wireless (LiFi) research with traditional fiber networks is nudging system designers toward components that can serve dual roles, reinforcing the strategic importance of 980 nm pump technology.

MARKET CHALLENGES

Stringent Reliability Expectations from End‑Users

Telecom carriers and cloud providers demand mean time between failures (MTBF) figures that exceed historical benchmarks. Any deviation in diode lifetime can trigger costly network outages, prompting purchasers to favor proven suppliers over emerging entrants.

Other Challenges

Thermal Management Complexity

The high output levels required for modern amplification stages generate heat densities that challenge conventional packaging. Designers must balance compactness with sophisticated cooling solutions, adding to bill‑of‑materials and development timelines.

MARKET RESTRAINTS

Capital Intensity of Advanced Fabrication Facilities

Establishing or retrofitting fabs to support the precise wavelength control demanded by 980nm single‑mode pump diodes requires multibillion‑dollar investments. Smaller players often lack access to such capital, limiting competitive diversity.

Regulatory Scrutiny Over Laser Safety Standards

International laser safety directives impose rigorous testing regimes. Compliance costs rise sharply for manufacturers seeking certification across multiple jurisdictions, which can delay market entry for novel designs.

MARKET OPPORTUNITIES

Emergence of Integrated Photonic Platforms

Silicon‑photonic foundries are beginning to offer co‑packaged solutions that embed 980nm pump lasers directly onto waveguide chips. This integration reduces interconnect losses and opens pathways for mass‑production of compact transceiver modules, creating a sizable growth niche for component suppliers.

Expansion into Sensing and Metrology Applications

Beyond telecom, precision sensing systems,such as those used in biomedical imaging and industrial inspection,are adopting 980nm single‑mode sources for their stability and spectral consistency. Early entrants that tailor their product lines to these verticals can diversify revenue streams and mitigate dependence on traditional telecom cycles.

980nm SM Pump Laser Diode Market Trends

Rising Demand from Fiber‑Optic Amplification

The deployment of erbium‑doped fiber amplifiers in long‑haul communication links has accelerated the need for stable, high‑power pump sources. The 980nm single‑mode diode, with its narrow divergence and low‑noise output, matches the gain profile of modern EDFAs, allowing operators to push capacity without incurring excessive penalties on signal‑to‑noise ratio. As service providers upgrade to 400G and beyond, the unit price of $1,320 remains attractive relative to the performance lift, prompting procurement managers to lock in multi‑year supply contracts. This shift translates into higher order volumes for mid‑stream manufacturers, who must balance inventory positioning against the risk of overcapacity.

Other Trends

Supply‑Chain Pressures on Epitaxial Materials

High‑purity InP and GaAs substrates form the backbone of the 980nm pump diode, yet recent fluctuations in semiconductor wafer availability have introduced lead times that extend beyond six months. Manufacturers are responding by diversifying sources and investing in in‑house epitaxial reactors to tighten control over layer uniformity. The quality of the quantum‑well structure directly influences beam‑mode stability, so any compromise in material consistency can erode the gains achieved in downstream optical systems. Companies that secure reliable wafer contracts or develop proprietary growth recipes gain a competitive edge, as they can promise tighter performance tolerances and higher yields.

Competitive Landscape Consolidates Around Packaging Innovations

Packaging reliability has emerged as the decisive factor differentiating leading vendors. The transition from traditional butterfly enclosures to fiber‑optic coupling modules reduces insertion loss and simplifies system integration for telecom equipment makers. Players such as Lumentum and Coherent have announced new hermetic sealing techniques that extend mean‑time‑between‑failures, a metric increasingly scrutinized by OEMs focused on network uptime. This emphasis on robust packaging forces smaller entrants to either form strategic alliances or accelerate R&D spend, reshaping the supplier ecosystem and concentrating market share among firms capable of delivering proof‑point reliability in high‑volume production.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive Dynamics in 980nm SM Pump Laser Diode Market

Lumentum remains the de‑facto leader, leveraging its extensive photonics portfolio and deep relationships with telecom equipment manufacturers. The company’s ability to control both epitaxial growth and fiber‑coupling packaging grants it a cost advantage that translates into tighter margins and a more predictable supply chain for OEMs. Recent investments in high‑purity InP substrate processing have sharpened its performance edge, especially in the high‑power segment where beam quality and temperature stability are decisive. By aligning its product roadmap with the rollout of next‑generation erbium‑doped fiber amplifiers, Lumentum is shaping pricing pressure across the value chain while preserving a premium for its single‑mode modules.

Beyond the dominant player, a cluster of specialized firms is carving out defensible niches. Coherent and Innolume focus on ultra‑narrow‑band variants that serve precision material‑processing lasers, while Toptica Eagleyard supplies low‑power diodes prized by laboratory‑scale fiber‑laser research groups. Japanese and Korean manufacturers such as Furukawa Electric and YOFC capitalize on domestic telecom roll‑outs, offering vertically integrated solutions that reduce lead times. Smaller entities,including LD‑PD PTE, Sheaumann Laser, Focuslight, nLIGHT, Jenoptik, LUMICS, QPhotonics, AeroDIODE, Agiltron, Box Optronics, HJ Optronics and QPC Lasers,differentiate through bespoke packaging formats, regional service networks, or targeted applications in medical imaging and industrial inspection. Collectively, these firms sustain competitive pressure by advancing epitaxial uniformity, improving fiber‑coupling efficiency, and extending warranty periods, which forces the market leader to continuously innovate.

List of Key 980nm SM Pump Laser Diode Companies Profiled

- Lumentum

- Coherent

- Innolume

- Toptica Eagleyard

- Furukawa Electric

- YOFC

- LD‑PD PTE

- Sheaumann Laser

- Focuslight

- nLIGHT

- Jenoptik

- LUMICS

- QPhotonics

- AeroDIODE

- Agiltron

- Box Optronics

- HJ Optronics

- QPC Lasers

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

High-Power Type

|

| By Application |

|

Optical Communication

|

| By End User |

|

Telecom Service Providers

|

| By Technology |

|

Packaging Reliability

|

| By Integration |

|

Integrated Photonic Platforms

|

Regional Analysis: 980nm SM Pump Laser Diode Market

North America

OEMs in the region are integrating quantum‑dot gain media with 980nm pump diodes to boost wall‑plug efficiency, a move that reflects a shift toward energy‑conscious designs in data‑center optics.

Federal agencies maintain a transparent certification pathway for laser safety classification, allowing manufacturers to forecast compliance expenditures with confidence.

Proximity to silicon wafer producers and advanced MOCVD facilities grants North American suppliers a logistical edge, shortening the turnaround from prototype to pilot production.

The most active buyers are telecom operators and LIDAR developers, both of which value the 980nm wavelength for its compatibility with existing fiber‑optic infrastructure.

Europe

European manufacturers are capitalising on an established standards ecosystem that encourages interoperability across borders. The region’s emphasis on environmentally sustainable production has spurred collaborations between diode makers and optical‑design houses to reduce waste heat in pump modules. Meanwhile, the EU’s investment in photonics research clusters, especially in Germany and the Netherlands, nurtures a pipeline of talent adept at tailoring 980nm devices for high‑precision medical imaging. These dynamics create a market where quality assurance and eco‑efficiency are as decisive as price competitiveness.

Asia‑Pacific

Asia‑Pacific exhibits a rapid scale‑up of fabrication capacity, largely fueled by governmental incentives in China, Japan, and South Korea. Domestic demand is amplified by aggressive rollout of 5G backhaul networks, which rely on compact pump diodes to meet bandwidth targets. Although cost pressures remain intense, the region’s ability to mass‑produce epitaxial wafers at volume keeps 980nm SM Pump Laser Diode Market accessible to a broad tier of system integrators, fostering a competitive landscape that encourages incremental performance improvements.

South America

In South America, market momentum stems from growing telecommunications infrastructure projects in Brazil and Argentina. Operators are increasingly adopting hybrid fiber‑wireless solutions where 980nm pump diodes serve as the optical backbone for last‑mile connectivity. Local assemblers benefit from modest labor costs and emerging trade agreements that facilitate component importation, allowing them to offer cost‑effective transceiver solutions to regional carriers.

Middle East & Africa

The Middle East & Africa region is characterised by targeted deployments in oil‑field monitoring and defense surveillance, where the robustness of 980nm pump diodes aligns with harsh environmental requirements. Strategic partnerships between Western equipment vendors and regional integrators help bridge the technology gap, while sovereign wealth funds are allocating capital toward offshore photonics research labs, signalling a long‑term commitment to establishing a foothold in this niche market.

Report Scope

This market research report provides a comprehensive analysis of the 980nm SM Pump Laser Diode Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of 980nm SM Pump Laser Diode Market?

-> 980nm SM Pump Laser Diode Market was valued at USD 156 million in 2025 and is expected to reach USD 290 million by 2032, growing at a CAGR of 9.4% during the forecast period.

Which key companies operate in 980nm SM Pump Laser Diode Market?

-> Key players include Lumentum, Coherent, Innolume, Toptica Eagleyard, Furukawa Electric, YOFC, LD-PD PTE, Sheaumann Laser, Focuslight, nLIGHT, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for high‑performance fiber optic communication networks, expansion of erbium‑doped fiber amplifiers (EDFA) and fiber lasers, and increasing adoption in precision material processing and medical optical equipment.

Which region dominates the market?

-> Asia‑Pacific is the predominant region, driven by strong telecom infrastructure investments and growing demand for fiber‑laser applications, while North America and Europe also show significant activity.

What are the emerging trends?

-> Emerging trends include advancements in epitaxial growth and single‑mode beam control, higher‑efficiency fiber coupling techniques, and development of reliable packaging solutions such as butterfly and fiber‑optic modules.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...