Semiconductor Liquid Filter Market Insights

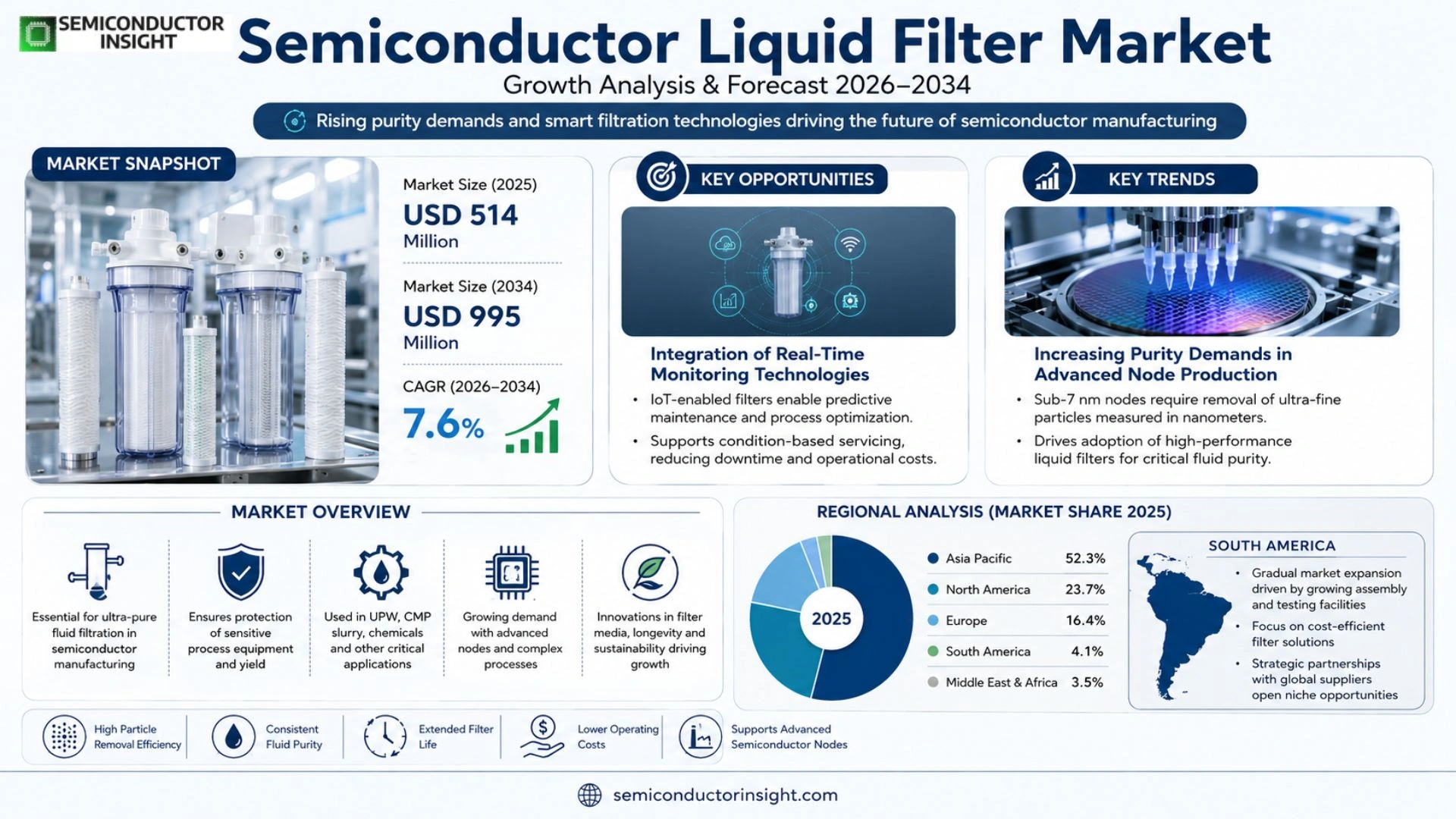

Global Semiconductor Liquid Filter market size was valued at USD 514 million in 2025. The market is projected to grow from USD 514 million in 2025 to USD 995 million by 2034, exhibiting a CAGR of 7.6 % during the forecast period.

Semiconductor liquid filters are specialised filtration devices that remove suspended solids, chemicals, solvents or phytochemicals from process liquids used in semiconductor manufacturing. They are essential for high‑cleanliness liquid treatment in chip fabrication, flat‑panel display production and photovoltaic module assembly because they protect sensitive equipment from particulate contamination.

The expansion of advanced‑node production together with rising investments in fabs across China, South Korea and the United States creates strong demand for ultra‑pure process water and chemicals. Environmental regulations that tighten waste‑water discharge limits also push manufacturers toward high‑efficiency filtration solutions. While technology upgrades raise performance standards for filter media, they simultaneously increase R&D costs for suppliers such as Pall, Entegris and Porvair. Moreover, fluctuations in raw‑material prices and supply‑chain disruptions add uncertainty to planning cycles.

MARKET DRIVERS

Rising Purity Requirements in Wafer Processing

Semiconductor Liquid Filter Market is gaining traction as manufacturers target sub‑micron defect levels in advanced node production. Continuous scaling of transistor geometries forces fabs to adopt filtration systems that can remove particles below 0.02 µm, compelling equipment vendors to upgrade their liquid‑handling units. This shift translates into higher specification filters and a willingness to pay premium prices for reliability.

Environmental Compliance and Re‑use Initiatives

Stringent wastewater regulations across North America and Asia are prompting fabs to recycle process chemicals rather than dispose of them. Re‑use cycles demand filtration media that retain catalytic efficiency over multiple passes, spurring demand for advanced polymer‑based filter cartridges. Companies that can demonstrate lower total‑cost‑of‑ownership through extended filter life gain a competitive edge.

➤ “Customers are increasingly evaluating filter performance against lifecycle cost, not just upfront price,”

At the strategic level, equipment integrators view filtration as a value‑added service, bundling filter monitoring sensors with their process tools. This creates recurring revenue streams and deepens supplier relationships, reinforcing the growth trajectory of Semiconductor Liquid Filter Market.

MARKET CHALLENGES

Capital Intensity and ROI Uncertainty

Investments in high‑precision filtration infrastructure often require multi‑year amortization schedules. Fab managers must justify expenditures against yield improvements that can be difficult to quantify, especially when yield gains are influenced by multiple concurrent process variables.

Other Challenges

Supply Chain Volatility

The reliance on specialty polymers and high‑purity reagents makes the filter supply chain vulnerable to raw‑material shortages. Recent geopolitical tensions have amplified lead‑time variability, forcing procurement teams to hold larger safety stocks, which in turn pressures working capital.

MARKET RESTRAINTS

High Initial Investment Thresholds

While performance gains are evident, the upfront cost of ultra‑fine filtration units remains a barrier for smaller fabs and emerging‑market players. This financial hurdle limits market penetration outside the largest integrated device manufacturers.

MARKET OPPORTUNITIES

Integration of Real‑Time Monitoring Technologies

The convergence of IoT sensors with filtration modules opens avenues for predictive maintenance and process optimization. Vendors that embed particle‑count telemetry into filter housings enable fabs to shift from scheduled replacements to condition‑based servicing, unlocking cost efficiencies and creating differentiated product offerings within Semiconductor Liquid Filter Market.

Semiconductor Liquid Filter Market Trends

Increasing Purity Demands in Advanced Node Production

The shift toward sub‑7 nm process nodes has intensified scrutiny of every fluid used on the fab floor. Minute contaminants that were once tolerable now threaten yield thresholds, prompting manufacturers to adopt filters capable of removing particles measured in nanometers. This heightened sensitivity is not merely a technical footnote; it reshapes procurement budgets, accelerates R&D pipelines, and forces equipment suppliers to revisit material compatibility. As a result, vendors that can demonstrate consistent performance at the extreme end of cleanliness are seeing their order books expand despite broader market headwinds.

Other Trends

Regional Investment Patterns

APAC continues to dominate Semiconductor Liquid Filter Market, contributing roughly 70 % of global sales. Government‑backed chip programs in China, South Korea, and Taiwan have spurred capital spending on ultra‑clean water and chemical recycling systems. Meanwhile, North America’s share, hovering near 13 %, is buoyed by defense‑related semiconductor projects and a resurgence of on‑shore fabrication. Europe, with about 9 % share, is leveraging strict environmental regulations to drive adoption of high‑efficiency filtration that reduces waste discharge. These geographic nuances create a tiered competitive landscape where regional players must tailor product portfolios to local policy and investment cycles.

Competitive Pressures and Innovation Cycles

Four firms,Pall, Entegris, Cobetter Filtration Group, and Porvair,command roughly 80 % of market volume, leaving limited room for newcomers. Their dominance stems from entrenched relationships with leading fabs and the ability to sustain long‑term R&D commitments. However, price compression in mature markets is eroding margins, compelling manufacturers to differentiate through advanced membrane materials and modular designs that simplify field servicing. Meanwhile, supply‑chain volatility, especially fluctuations in specialty polymer costs, forces players to adopt flexible sourcing strategies and to hedge raw‑material exposure wherever possible.

COMPETITIVE LANDSCAPE

Key Industry Players

Semiconductor Liquid Filter Market Competitive Overview

Pall Corporation continues to dominate the high‑purity filtration segment, leveraging its extensive portfolio of membrane technologies and a global service network that aligns with the stringent needs of 7‑nm and below process nodes. Entegris, with its focus on ceramic and polymeric filter media, has secured a leading position in lithography and CMP (chemical‑mechanical polishing) applications, where sub‑micron particle control is critical. Cobetter Filtration Group, operating primarily out of APAC, differentiates itself through an aggressive cost‑management strategy while maintaining compliance with evolving environmental regulations, helping it capture a sizable share of the fast‑growing Chinese fab sector. Porvair’s niche in ultra‑low‑particulate water filters has attracted major integrated‑circuit manufacturers seeking to reduce defectivity in wafer processing. 3M’s diversified filtration business, backed by strong R&D investment, enables cross‑selling of its anti‑static and chemical‑resistant filter media to both semiconductor and display fabs, reinforcing its foothold in North America and Europe. Collectively, these five firms account for roughly 80 % of global revenue, shaping a market structure where scale, technology breadth, and regional service capabilities dictate competitive advantage.

Beyond the top tier, a cadre of specialised firms fuels innovation in sub‑segments that larger players often overlook. Advantec Group supplies precision‑grade filter cartridges for semiconductor chemical cleaning, catering to boutique fabs that prioritize ultra‑clean water cycles. Critical Process Filtration focuses on high‑temperature polymer filters used in advanced deposition tools, positioning itself as a supplier of choice for emerging AI‑driven chip lines. Roki Techno has built a reputation for rapid‑prototype filter designs, enabling customers to experiment with new process chemistries without long lead times. Bright Sheland International, although smaller, leverages a vertically integrated supply chain to offer customized filtration solutions for photovoltaic module production, an area where demand is accelerating due to renewable‑energy incentives. These niche players add depth to the competitive landscape, compelling the market leaders to continuously refine product performance and pricing models while also opening collaborative opportunities for co‑development of next‑generation filtration technologies.

List of Key Semiconductor Liquid Filter Companies Profiled

- Pall Corporation

- Entegris

- Cobetter Filtration Group

- Porvair

- 3M

- Advantec Group

- Critical Process Filtration

- Roki Techno

- Bright Sheland International

- Mitre Filtration

- PureTech Solutions

- Filtracom Ltd.

- Nanofilter Systems

- DeepClean Filters

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Lithography Filter

|

| By Application |

|

Integrated Circuit

|

| By End User |

|

Chip Fabrication Plants

|

| By Technology |

|

Nanofiltration

|

| By Market Trend |

|

Sustainability Focus

|

Regional Analysis: Semiconductor Liquid Filter Market

Asia‑Pacific

Localized production clusters surround key semiconductor valleys, enabling filter makers to align capacity expansions with fab ramp‑ups. The close physical tie‑up trims lead times for custom filter designs and encourages joint engineering initiatives, fostering a feedback loop that sharpens product differentiation.

Recent disruptions have prompted a shift toward diversified sourcing of high‑purity solvents and membrane substrates. Regional players are investing in vertical integration, securing raw‑material pipelines and shielding downstream filter fabrication from external volatility.

Harmonised standards across major economies simplify compliance for filter producers targeting multi‑regional customers. Emerging safety guidelines on chemical handling encourage adoption of greener filtration media, prompting firms to redesign processes for environmental resilience.

Collaborative research consortia funded by both public and private sectors accelerate breakthroughs in nano‑porous membrane technologies. These advances translate into higher rejection rates for sub‑micron particles, a critical requirement for the most advanced node manufacturers.

North America

North America retains a strong foothold in Semiconductor Liquid Filter Market by leveraging deep pockets of venture capital and a robust IP framework. Filtration firms here focus on high‑value, low‑volume offerings tailored to specialty applications such as quantum‑computing chips. The presence of leading equipment OEMs creates a demand for bespoke filter solutions that can operate under the extreme temperatures of next‑gen lithography. Cross‑border collaborations with Asian partners enable a hybrid model of design innovation in the United States combined with cost‑effective manufacturing in the Pacific basin, offering customers flexibility in supply chain configuration.

Europe

European stakeholders emphasize precision engineering and compliance with stringent environmental directives. The region’s filter manufacturers differentiate themselves through ultra‑cleanroom certifications and the ability to process exotic fluids required by cutting‑edge photolithography. Strategic investment in digital twins of filtration lines enhances predictive maintenance, reducing downtime for high‑mix, low‑batch production schedules prevalent in the European fab landscape. Moreover, the EU’s emphasis on circular economy principles drives research into recyclable filter media, aligning product development with sustainability goals.

South America

South America’s participation in Semiconductor Liquid Filter Market is gradually expanding as regional governments prioritize semiconductor assembly and testing facilities. Local enterprises are building capabilities in bespoke filter fabrication to support a nascent assembly sector. While the market scale remains modest, the focus on cost‑efficient designs and partnerships with established Asian suppliers offers a pathway for South American firms to capture niche segments, particularly in low‑to‑mid‑range device manufacturing.

Middle East & Africa

The Middle East & Africa region is emerging as a strategic hub for downstream processing, leveraging its logistics infrastructure and growing investment in high‑tech parks. Companies are positioning themselves as service providers for filter validation and calibration, catering to multinational chipmakers establishing satellite facilities. In Africa, a handful of startups are exploring low‑cost filtration solutions aimed at supporting local electronics assembly, signaling the early stages of market diversification across the broader continent.

Report Scope

This market research report provides a comprehensive analysis of the Semiconductor Liquid Filter Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Semiconductor Liquid Filter Market?

-> Semiconductor Liquid Filter market is projected to grow from USD 514 million in 2025 to USD 995 million by 2034, exhibiting a CAGR of 7.6 %

Which key companies operate in Semiconductor Liquid Filter Market?

-> Key players include Pall, Entegris, Cobetter Filtration Group, Porvair, 3M, Advantec Group, Critical Process Filtration, Roki Techno, Bright Sheland International.

What are the key growth drivers?

-> Key growth drivers include the increasing complexity of semiconductor manufacturing (especially sub‑7 nm nodes), rising global semiconductor investments (China, South Korea, United States), and stricter environmental and safety standards driving demand for high‑efficiency filtration systems.

Which region dominates the market?

-> Asia‑Pacific is the largest market, accounting for approximately 70% of global share, followed by North America (13%) and Europe (9%).

What are the emerging trends?

-> Emerging trends include greater emphasis on ultra‑clean liquid environments for 5G, AI, and IoT applications, development of highly precise lithography filters (33% share), and integration of advanced materials to improve filtration accuracy for next‑generation integrated circuits.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...