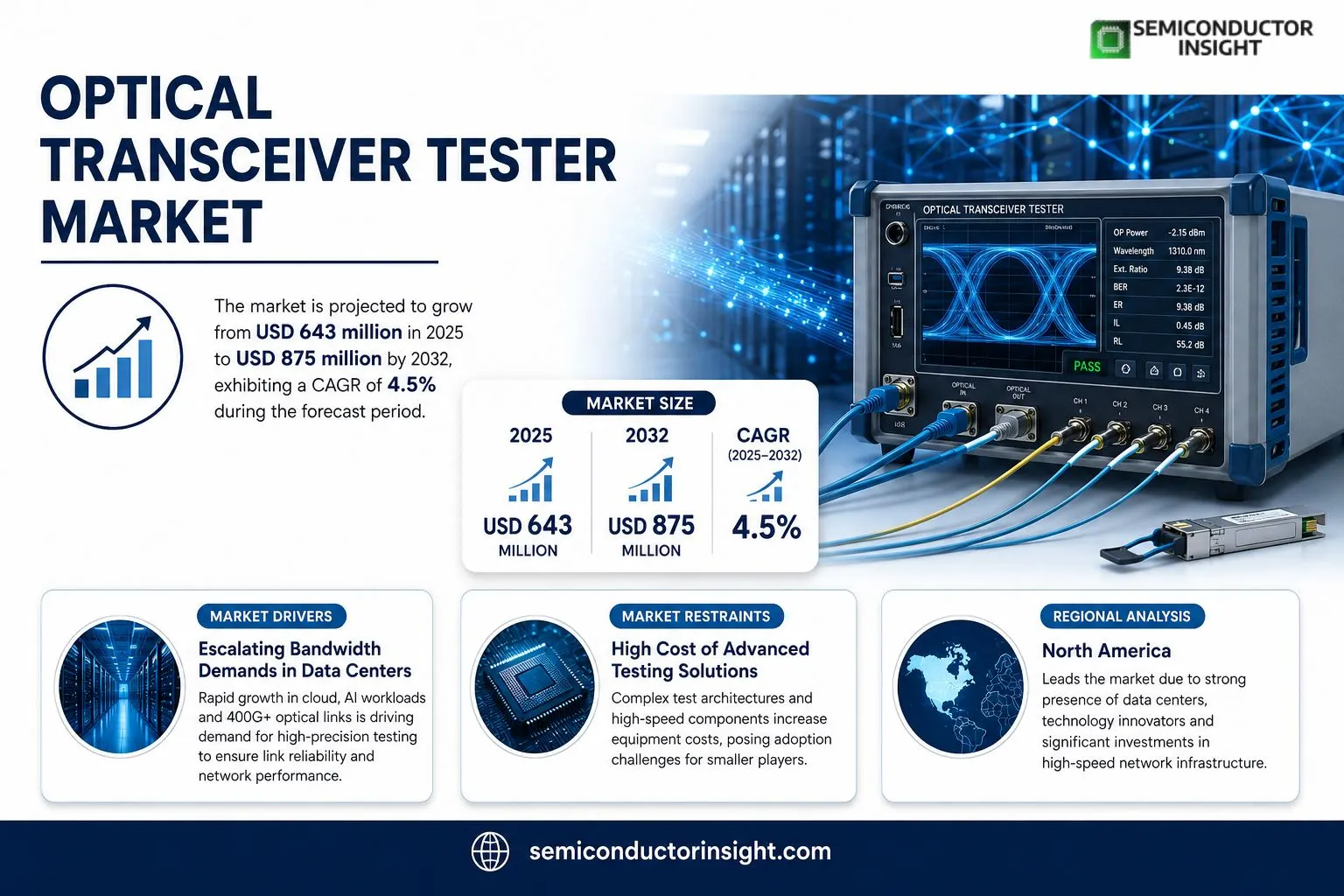

Optical Transceiver Tester Market Insights

Optical Transceiver Tester market was valued at USD 643 million in 2025 and will grow to USD 875 million by 2032, reflecting a compound annual growth rate of 4.5 percent over the period.

Optical transceiver testers are precision instruments that emulate real‑world communication environments while measuring optoelectronic parameters of transceivers. Core functions include assessment of optical power, wavelength, extinction ratio, bit error rate, eye‑diagram quality and insertion‑loss/back‑loss, enabling verification from chip level through full‑module integration.The expansion of high‑speed optical networks creates demand for reliable performance consistency and link stability; consequently manufacturers invest heavily in testing solutions. Upstream components such as ultra‑wideband photodetectors (sourced mainly from the United States and Japan) and high‑speed ASICs underpin device capability, while downstream usersoptical module makers (≈55 % of demand), communication equipment producers (≈20 %), data‑center operators (≈15 %) and certification labs (≈10 %)drive volume growth.

MARKET DRIVERS

Escalating Bandwidth Demands in Data Centers

The surge in cloud workloads and AI inference pushes data‑center operators to deploy 400 Gb/s and higher optical links. As line rates climb, the tolerance window for transceiver performance narrows, compelling network teams to rely on high‑precision testers. Consequently, Optical Transceiver Tester Market experiences amplified procurement cycles from Tier‑1 providers seeking to validate every serial interface before rack integration.

Shift Toward Multi‑Protocol Transport Networks

Enterprises are consolidating Ethernet, Fibre Channel, and Infiniband onto a common optical fabric to cut CAPEX. Multi‑protocol environments demand devices that can emulate diverse traffic patterns while preserving eye‑diagram fidelity. Test equipment able to switch between standards without hardware re‑configuration becomes a strategic asset, driving purchase intensity across Optical Transceiver Tester Market.

➤ Test accuracy above 99.5 % accelerates deployment cycles by reducing field re‑work.

Both trends converge on a single imperative: verify signal integrity at line‑rate speeds before production release. Vendors that embed AI‑assisted analysis into their tester platforms are seeing faster adoption, because customers value the ability to pinpoint marginal defects in minutes rather than hours.

MARKET CHALLENGES

Complexity of Test Algorithms

Modern transceivers incorporate adaptive equalization and digital signal processing that evolve in real time. Replicating these dynamics within a testbench requires sophisticated firmware and extensive calibration data sets. Development teams often confront steep learning curves, inflating time‑to‑market for new tester models.

Other Challenges

Cost Sensitivity

Although high‑performance testers deliver measurable ROI, mid‑size operators weigh capital outlay against incremental quality gains. Budget constraints can limit the frequency of upgrades, slowing overall market momentum.

MARKET RESTRAINTS

Regulatory Certification Hurdles

Global telecommunication standards mandate rigorous compliance testing for every optical module. Achieving certification often involves multiple laboratory passes and documentation cycles, which can delay product launch timelines. Test equipment that does not align with emerging IEC and IEC‑61755 revisions forces manufacturers to source additional validation tools, adding friction to adoption.Furthermore, regional security regulations sometimes restrict the export of advanced diagnostic firmware, limiting the ability of vendors to offer unified solutions across borders. These constraints temper the velocity of market penetration despite rising technical demand.

MARKET OPPORTUNITIES

Emergence of Integrated Photonics

Silicon‑photonic transceivers promise lower power consumption and smaller footprints, yet their novel material stacks introduce new failure modes. Test suites that incorporate on‑chip monitoring and wafer‑level probing can differentiate providers, opening a niche where early‑stage validation commands premium pricing.Additionally, service‑oriented testingwhere manufacturers lease test capacity on a subscription basisaddresses the cost sensitivity highlighted earlier. By converting a capital expense into an operational one, vendors can tap into operators seeking flexibility, thereby expanding the addressable base of Optical Transceiver Tester Market.

Optical Transceiver Tester Market Trends

Escalating Test Demands from AI‑Driven Optical Modules

The proliferation of AI accelerators and hyperscale cloud infrastructures is forcing module manufacturers to certify ever‑higher data‑rate transceivers. Over half of the downstream spend now originates from optical‑module factories, where test volumes have risen faster than 25% year‑on‑year. This surge reflects a shift from merely confirming compliance toward continuous performance monitoring, as operators seek to eliminate bit‑error spikes that can cripple latency‑sensitive workloads. Consequently, Optical Transceiver Tester Market is seeing a premium placed on instruments that can capture eye‑diagram fidelity, extinction‑ratio drift, and power‑budget variations in real time. Vendors that embed advanced DSP analytics into their test platforms are gaining traction because they enable rapid root‑cause isolation, shortening time‑to‑market for next‑generation 400G and 800G modules.

Other Trends

Supply‑Chain Concentration and Capacity Pressures

Key components such as ultra‑wideband photodetectors and high‑speed ASICs remain sourced predominantly from the United States, Japan, and Germany. A single production line delivers roughly 130 units annually, and the sector operates near an 88% utilization rate. This high utilization, combined with a gross profit margin of about 33%, underscores a market that rewards scale yet remains vulnerable to component shortages. Manufacturers are therefore investing in localized wafer‑fab partnerships and dual‑sourcing strategies to insulate against geopolitical volatility, while also exploring modular design approaches that can accommodate alternative detector technologies without sacrificing measurement precision.

Emergence of Portable Test Solutions and Regional Shifts

Portable testers, once niche, are now entering the mainstream as field engineers demand on‑site verification for rapidly deployed data‑center interconnects. Their lighter form factor, coupled with cloud‑based result aggregation, allows operators to monitor link health without returning to a central lab. Meanwhile, growth hotspots are migrating toward East Asia, where chip‑level testing capacity is expanding alongside silicon photonics initiatives. North America and Europe retain a brand‑lead advantage, but the influx of agile Asian players could erode that edge within the next five years, prompting incumbent firms to bolster service ecosystems and firmware upgrade pathways to preserve customer loyalty.

COMPETITIVE LANDSCAPE

Key Industry Players

Optical Transceiver Tester Market – Competitive Overview

The market is dominated by a handful of firms that command the bulk of revenue and capacity. Keysight Technologies, with a global footprint across North America, Europe and East Asia, leverages deep expertise in high‑speed electronic ASICs and precision optics to sustain a utilization rate near 90 % on its 120‑unit production lines. Its pricing power and brand equity translate into a gross margin well above 30 %, reinforcing the sector’s high entry barrier. VIAVI Solutions and EXFO occupy the second tier, each holding roughly 8‑10 % of total sales in 2025; both have diversified portfolios that span functional, performance and conformance testing, enabling them to serve module manufacturers and data‑center operators alike. Anritsu rounds out the top‑three, differentiating through advanced DSP algorithms for PAM4 and 800 G testing, a capability increasingly required as AI‑driven workloads push optical link speeds beyond 400 G.Beyond the leading triad, a constellation of niche players enriches the competitive fabric. Semight Instruments and Yokogawa Electric specialize in ultra‑wideband photodetectors sourced from InP and GaAs foundries in the United States and Japan, carving out market share in high‑precision laboratory environments. VeEX, Tektronix and Teradyne compete on portable test‑set ergonomics, targeting field engineers at telecom operators. Santec and Luna Innovations focus on German‑engineered optical components, while Chinese entrants such as Beijing Xinertel Technology, SHANGHAI HYWICOM TECHNOLOGY, Sinolink Technologies (Beijing) and APEX Technologies pursue cost‑efficient solutions for the rapidly expanding domestic module manufacturing base. Teledyne LeCroy rounds out the list, offering integrated software suites that streamline link‑level verification for system integrators. Collectively, these firms ensure that customers can select instruments aligned with specific performance thresholds, regional supply chains, and budgetary constraints.

List of Key Optical Transceiver Tester Companies Profiled

- Keysight Technologies

- VIAVI Solutions

- EXFO

- Anritsu

- Semight Instruments Co., Ltd

- Yokogawa Electric

- VeEX

- Tektronix

- Teradyne

- Santec

- Beijing Xinertel Technology

- SHANGHAI HYWICOM TECHNOLOGY

- Sinolink Technologies (Beijing)

- APEX Technologies

- Luna Innovations

- Teledyne LeCroy

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

400G Testers dominate the market driven by the rapid adoption of high‑speed optical modules in data‑center and telecom networks.

|

| By Application |

|

Optical Module Manufacturing is the primary driver of tester adoption because manufacturers require comprehensive verification from chip to module level.

|

| By End User |

|

Network Operators lead end‑user spending as they require continuous performance verification across expanding fiber‑optic backbones.

|

| By Test Function |

|

Performance Tester is the most sought‑after function because it validates signal integrity under real‑world traffic loads.

|

| By Form Factor |

|

Portable Testers are gaining traction as field engineers need agile solutions for rapid fault isolation.

|

Regional Analysis: Optical Transceiver Tester Market

North America

The surge in demand for 400 Gb/s and beyond interconnects forces data‑center operators to seek testers that can validate signal integrity at unprecedented rates. Providers that embed real‑time eye‑pattern analysis into their kits are gaining preference, as they enable faster qualification of new transceiver modules without extensive laboratory setups.

While performance expectations rise, budgetary pressures compel organizations to rationalize test‑equipment spend. Solutions that combine multiple test modalitiesloss, dispersion, and polarizationinto a single chassis are viewed as cost‑effective, reducing capital outlay and simplifying maintenance.

The rollout of 400G NRZ and PAM4 specifications opens a niche for testers that can emulate both electrical and optical characteristics of these standards. Early adopters expect verification tools that support simultaneous multi‑wavelength testing, a capability that few incumbents currently provide.

Vendors are bundling test software with cloud‑based analytics, allowing customers to track performance trends across geographically dispersed assets. This integration transforms raw data into actionable insights, fostering proactive network management.

Europe

European telecom operators are embracing Optical Transceiver Tester Market as regulators tighten specifications for cross‑border fiber links. National broadband initiatives, particularly in Germany and the Nordics, emphasize reliability, pushing service providers to adopt test platforms that can certify transceivers against stringent latency requirements. Meanwhile, a collaborative R&D environmentexemplified by EU‑funded projectsencourages equipment makers to co‑develop test modules tailored for emerging coherent optics. The result is a market where flexibility and multi‑standard support are prized, enabling firms to quickly adapt to shifting network architectures across the continent.

Asia‑Pacific

In Asia‑Pacific, rapid urbanization and the rollout of 5G backhaul are reshaping Optical Transceiver Tester Market. Countries such as Japan, South Korea, and China prioritize high‑capacity transport, driving operators to seek testers that can verify multicore and space‑division multiplexed solutions. Local manufacturers, keen to capture export opportunities, are investing in modular test platforms that can be customized for diverse carrier specifications. The competitive landscape is further intensified by aggressive pricing strategies, compelling vendors to demonstrate superior value through faster test cycles and reduced calibration overhead.

South America

South American markets are still consolidating their optical infrastructure, yet the push for broadband expansion is stimulating interest in reliable transceiver verification. Brazil’s recent spectrum allocation reforms have sparked a wave of network upgrades, prompting service providers to look for testers capable of handling both legacy 100 Gb/s equipment and emerging 200 Gb/s modules. Regional distributors favor partnerships with global OEMs that can deliver localized support, ensuring that test solutions align with local technical talent and maintenance practices.

Middle East & Africa

The Middle East & Africa region exhibits a blend of high‑growth projects in the Gulf and nascent deployments across Sub‑Saharan nations. Gulf Cooperation Council members invest heavily in submarine cable extensions, necessitating testers that can certify long‑haul transceivers under harsh environmental conditions. Conversely, African operators focus on cost‑efficient validation for mid‑range optical links, favoring compact, battery‑operated test units. The divergent needs create a market where versatility and ruggedness are equally critical, prompting vendors to tailor product portfolios to distinct climate and budgetary contexts.

Report Scope

This market research report provides a comprehensive analysis of the Optical Transceiver Tester Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Optical Transceiver Tester Market?

-> Optical Transceiver Tester Market was valued at USD 643 million in 2025 and is expected to reach USD 875 million by 2032 with a CAGR of 4.5% during the forecast period.

Which key companies operate in Optical Transceiver Tester Market?

-> Key players include Keysight Technologies, VIAVI Solutions, EXFO, Anritsu, Semight Instruments Co., Ltd, Yokogawa Electric, VeEX, Tektronix, Teradyne, Santec, Beijing Xinertel Technology, SHANGHAI HYWICOM TECHNOLOGY, Sinolink Technologies (Beijing), APEX Technologies, Luna Innovations, Teledyne LeCroy.

What are the key growth drivers?

-> Key growth drivers include the need for high‑performance consistency, mitigation of signal transmission errors, improving link stability in high‑speed optical networks, rapid AI‑driven data‑center expansion, and increasing demand for high‑speed optical module testing.

Which region dominates the market?

-> Asia dominates in terms of demand and production capacity, driven by extensive AI computing requirements, data‑center proliferation, and a concentrated manufacturing base in East Asia.

What are the emerging trends?

-> Emerging trends include advanced DSP algorithms for PAM4 and higher‑order modulation, integration of AI‑assisted test analytics, and development of portable yet high‑precision tester form factors.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...