Test Probe Pins Market Insights

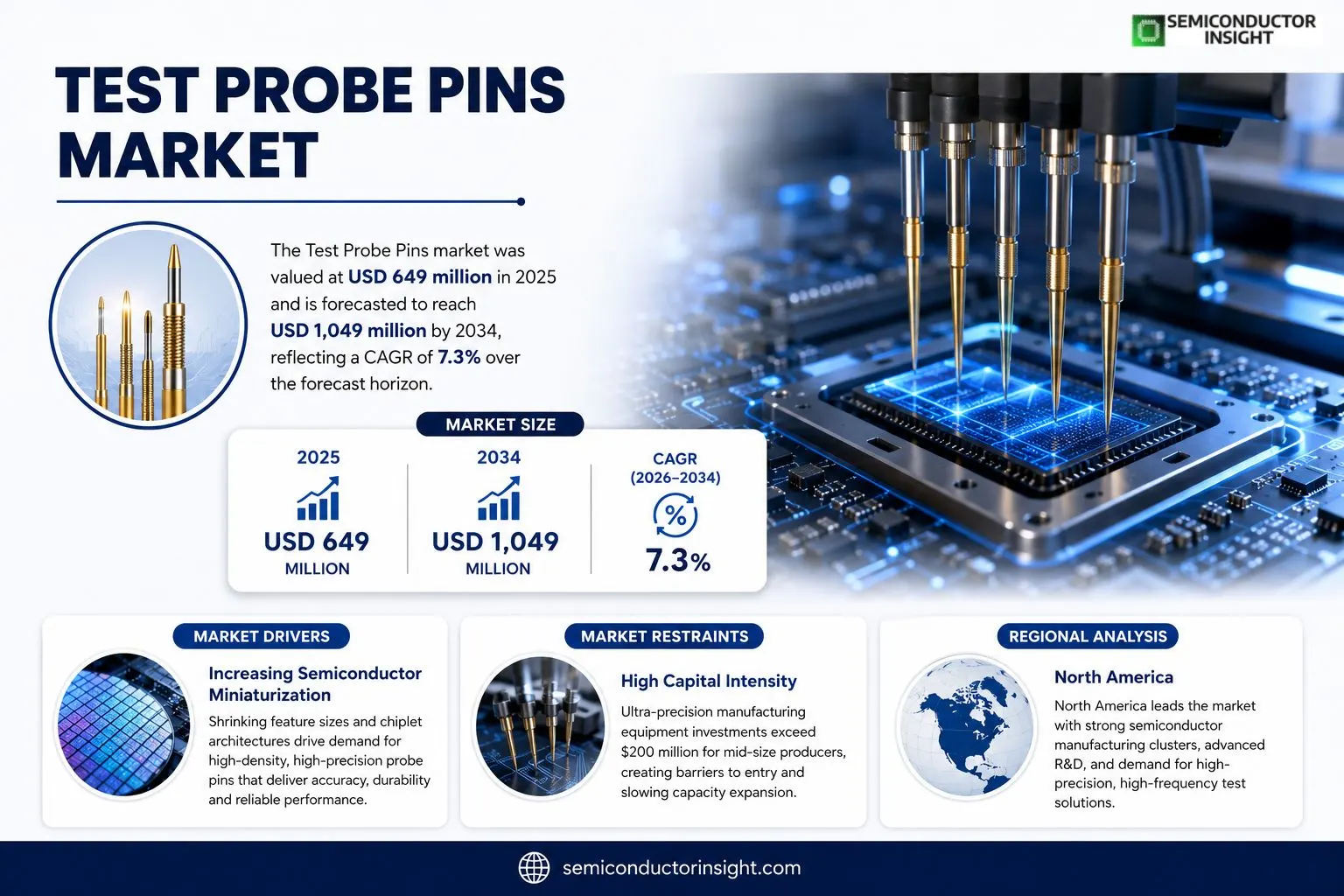

Test Probe Pins market was valued at USD 649 million in 2025 and is forecasted to reach USD 1,049 million by 2034, reflecting a CAGR of 7.3% over the forecast horizon.

Test Probe Pins are precision contact pins employed in electronic testing to temporarily connect device terminals or test points for measurement, verification, or programming of components and assemblies. In 2025 global production approximated 592 million units with an average price of about USD 1.2 per unit; manufacturing capacity stood near 600 million units and typical gross margins ranged from 20 % to 40 %.The increasing adoption of advanced packaging formats such as chiplet architectures, high‑density interconnects and higher‑frequency operation has raised requirements for pin durability and accuracy. Consequently, wafer fabs, OSAT firms, semiconductor equipment makers and EMS providers are sourcing larger volumes of probe pins for wafer probers, test sockets, automated test equipment and ICT/FCT systems. Emerging trends in semiconductor miniaturization therefore translate into steady demand for higher‑performance probe pins.

MARKET DRIVERS

Increasing Semiconductor Miniaturization

The relentless push toward smaller, faster chips has forced test equipment manufacturers to adopt finer probe solutions. As feature sizes shrink below 10 nm, Test Probe Pins Market participants are compelled to redesign pin geometry, delivering higher pin density without sacrificing mechanical stability. This trend fuels incremental revenue streams as OEMs seek qualified suppliers capable of meeting tighter tolerances.

Growth of High‑Volume Test Automation

Automated test systems now handle millions of devices per day, demanding probes that can endure prolonged cycling. Manufacturers that embed wear‑resistant coatings into probe pins gain a competitive edge, translating durability improvements into cost‑per‑test reductions for end users. The resulting efficiency pressure lifts overall spend on advanced probe assemblies.

➤ “The shift to sub‑micron probe pins has trimmed test cycle times by up to 15 % across leading wafer‑fab lines.”

Combined, these forces generate a steady uplift in capital expenditures for probe‑pin suppliers, positioning Test Probe Pins Market for a multi‑year expansion that outpaces the broader test equipment segment.

MARKET CHALLENGES

Stringent Quality Regulations

Regulatory bodies in key regions have tightened acceptance criteria for probe‑pin contamination and material composition. Compliance audits now require detailed traceability, inflating validation costs for smaller vendors and narrowing the competitive field.

Other Challenges

Supply‑Chain Volatility

The reliance on specialty alloys and precision‑machined ceramics creates exposure to raw‑material price swings. Recent geopolitical tensions have intermittently disrupted shipments, forcing manufacturers to hold higher safety stocks, which erodes margins.

MARKET RESTRAINTS

High Capital Intensity

Investment in ultra‑precision manufacturing equipment exceeds $200 million for a mid‑size producer, creating a barrier for new entrants and limiting the pace of capacity expansion in Test Probe Pins Market.Furthermore, the long lead times associated with custom tooling mean that order fulfillment can extend beyond six months, discouraging customers seeking rapid design‑to‑production cycles.

MARKET OPPORTUNITIES

Emergence of 3D‑Stacked Architectures

Three‑dimensional integrated circuits require probe pins capable of accessing multiple layers through micro‑vias. Companies that develop pins with adjustable compliance and integrated sensing electronics can capture a niche that is currently underserved, offering premium pricing potential.In addition, the rise of flexible printed circuit testing opens a parallel avenue. Tailoring probe‑pin tip geometry for bendable substrates allows suppliers to diversify beyond rigid wafer environments, expanding the addressable market base.

Test Probe Pins Market Trends

Rising Need for High‑Frequency, High‑Precision Probes

Test Probe Pins Market is feeling the impact of next‑generation semiconductor designs that push signal frequencies above 10 GHz and pack interconnects ever tighter. As chiplet architectures and advanced packaging become mainstream, test engineers require pins that can sustain low insertion loss while preserving dimensional accuracy. The 2025 production figure of roughly 592 million units, coupled with an average price of US$1.2 per pin, reflects a baseline that is now being stretched by specifications that demand tighter tolerances and superior surface finishes. Suppliers that have invested in diamond‑coated or gold‑plated alloys are seeing incrementally higher unit revenues, while customersespecially wafer fab and OSAT facilitiesare willing to absorb modest price premiums to avoid test failures that can erode yield. This shift is less about volume growth and more about the value extracted from each test cycle, reshaping the profit landscape for manufacturers.

Other Trends

Margin Pressures and Capacity Utilization

Gross profit margins in the sector historically range between 20 % and 40 %. In 2025, capacity stood at about 600 million units, a figure that marginally exceeds actual output. The narrow gap between capacity and production signals that firms are operating near full utilization, a position that can sustain current margins but leaves little room for error. Any disruptionwhether in raw material availability or in the supply chain for specialty coatingshas the potential to compress spreads. Companies that have diversified their sourcing or that have adopted lean inventory practices are better positioned to protect profitability as test volumes respond to the ebb and flow of semiconductor fab activity.

Geographic Shifts in Production and Consumption

While the United States and China remain the largest end‑users of test equipment, the production footprint for probe pins is increasingly global. The 2025 valuation of US$649 million reflects a market that is still concentrated in a handful of specialized manufacturers, yet emerging fab clusters in Southeast Asia are prompting strategic joint ventures. These partnerships aim to shorten lead times for high‑mix, low‑volume orders that are typical of advanced packaging pilots. The geographic rebalancing reduces dependence on any single region and creates new opportunities for local suppliers to capture a share of the projected US$1.049 billion market size anticipated for 2034.

COMPETITIVE LANDSCAPE

Key Industry Players

Test Probe Pins Market: Competitive Overview

The market continues to be anchored by a handful of vertically integrated manufacturers that control both design IP and high‑volume production. FormFactor, Inc. dominates the premium segment by leveraging its deep wafer‑probing heritage and a robust portfolio of high‑frequency pins that meet the tolerances demanded by advanced node fabs. Its ability to double‑line capacity in response to chiplet‑driven testing requirements has created a de‑facto price ceiling that pressures midsize rivals. Meanwhile, ITM Test Solutions has carved a niche in specialized ATE fixtures, pairing bespoke pin geometries with on‑site engineering support that locks in long‑term service contracts. The concentration of capacity around these two firms forces smaller entrants to differentiate through cost‑effective alloys or rapid prototype turn‑around, which is evident in the growing presence of Asian manufacturers that focus on bulk supply for EMS customers.Beyond the dominant players, a diverse set of regional companies contributes to a fragmented supply base. Shinko Electric Industries (Japan) and Shenzhen Hengxing (China) supply high‑volume, mid‑range pins that are popular in PCB‑level testing where ultra‑low inductance is less critical. Companies such as LFC Precision (South Korea) and Asian Test Solutions (Taiwan) have invested in laser‑cutting technology to offer tighter pitch offerings for emerging interposer testing. Additionally, Advantest and Teradyne, traditionally known for test equipment, have entered the consumables arena by acquiring niche pin makers, thereby extending their value chain and providing bundled solutions to semiconductor fabs. This mosaic of capabilities creates competitive pressure on pricing, accelerates innovation in coating materials, and compels original equipment manufacturers to re‑evaluate supply‑risk strategies.

List of Key Test Probe Pins Companies Profiled

- FormFactor, Inc.

- ITM Test Solutions

- Shinko Electric Industries Ltd.

- Shenzhen Hengxing Electronics

- LFC Precision Co., Ltd.

- Asian Test Solutions

- Advantest Corporation

- Teradyne, Inc.

- Kimball Electronics

- ProbeNet Technologies

- Amkor Technology, Inc.

- Keysight Technologies (formerly Agilent)

- Goede Technologies GmbH

- Jabil Circuit (EMS division)

- Micron Test Systems

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Tungsten pins are regarded as the premier choice for high‑precision testing environments.

|

| By Application |

|

Wafer testing remains the dominant application for probe pins.

|

| By End User |

|

Wafer fabs drive the most stringent specifications for probe pins.

|

| By Technology |

|

High‑frequency pins are increasingly pivotal as device architectures migrate to higher data rates.

|

| By Performance |

|

Low‑contact resistance is a critical performance driver for modern test environments.

|

Regional Analysis: Test Probe Pins Market

North America

The Silicon Valley corridor and the Boston‑Cambridge corridor host a concentration of startups focusing on micro‑fabricated probe designs, pushing the limits of miniaturization and material fatigue resistance.

Robust domestic sourcing of high‑purity copper and tungsten alloys mitigates exposure to geopolitical disruptions, ensuring consistent availability for high‑volume customers.

A handful of leading wafer‑fab operators account for a sizable share of demand, prompting suppliers to adopt tiered service agreements that balance volume discounts with rapid engineering support.

Harmonized testing standards across the US and Canada streamline certification pathways, allowing vendors to launch new pin families with reduced compliance overhead.

Europe

European manufacturers are emphasizing sustainability within Test Probe Pins Market, integrating recycled alloys and low‑impact manufacturing techniques. The presence of several automotive semiconductor hubs encourages design strategies that prioritize durability under thermal cycling. Collaborative programs between industry groups and standards bodies are shaping specifications that address both performance and environmental criteria, nudging suppliers toward greener product roadmaps.

Asia‑Pacific

Asia‑Pacific’s rapid expansion of advanced packaging facilities fuels demand for high‑precision probe pins. Local suppliers are capitalizing on lower labor costs to offer cost‑effective solutions, yet they face pressure to match the engineering depth of North American rivals. Partnerships with global OEMs are becoming a conduit for technology transfer, enabling regional firms to upscale capabilities while catering to burgeoning consumer‑electronics manufacturers.

South America

In South America, emerging test services are aligning with regional semiconductor fabs that focus on niche analog and power devices. Market participants are differentiating through localized support, offering rapid prototyping to address the fragmented client base. Although volume remains modest, the strategic emphasis on customized pin geometries positions the region as a niche supplier for specialty applications.

Middle East & Africa

The Middle East & Africa region is still nascent in Test Probe Pins Market, but recent government‑backed initiatives to develop semiconductor ecosystems are attracting foreign expertise. Early‑stage investments are concentrated on establishing precision machining facilities and training programs, laying groundwork for future participation in global supply chains once local fab capacity expands.

Report Scope

This market research report provides a comprehensive analysis of the Test Probe Pins Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: ✅ The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- ✅ Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- ✅ Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- ✅ Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- ✅ Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- ✅ Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- ✅ Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- ✅ Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Test Probe Pins Market?

-> Test Probe Pins Market was valued at USD 649 million in 2025 and is expected to reach USD 1049 million by 2034, growing at a CAGR of 7.3%.

What were the production volume and average price in 2025?

-> In 2025, global production reached approximately 592 million units with an average market price of around USD 1.2 per unit.

What is the typical gross profit margin for Test Probe Pins?

-> The typical gross profit margin ranges between 20 % and 40 % for manufacturers.

Which downstream customers and applications use Test Probe Pins?

-> Test probe pins are essential consumables in wafer testing, package testing, and finished PCB testing. Primary customers include wafer fabs, OSAT companies, semiconductor equipment manufacturers, and electronics manufacturing services (EMS) providers. They are deployed in wafer probers, test sockets, fixtures, automated test equipment (ATE) and ICT/FCT testing systems.

What trends are driving higher precision and performance requirements?

-> Advancements such as leading‑edge process nodes, chiplet architectures, advanced packaging, and high‑density interconnect technologies are increasing demand for higher‑precision, more durable, and high‑frequency capable test probe pins.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...