Semiconductor Tester Market Insights

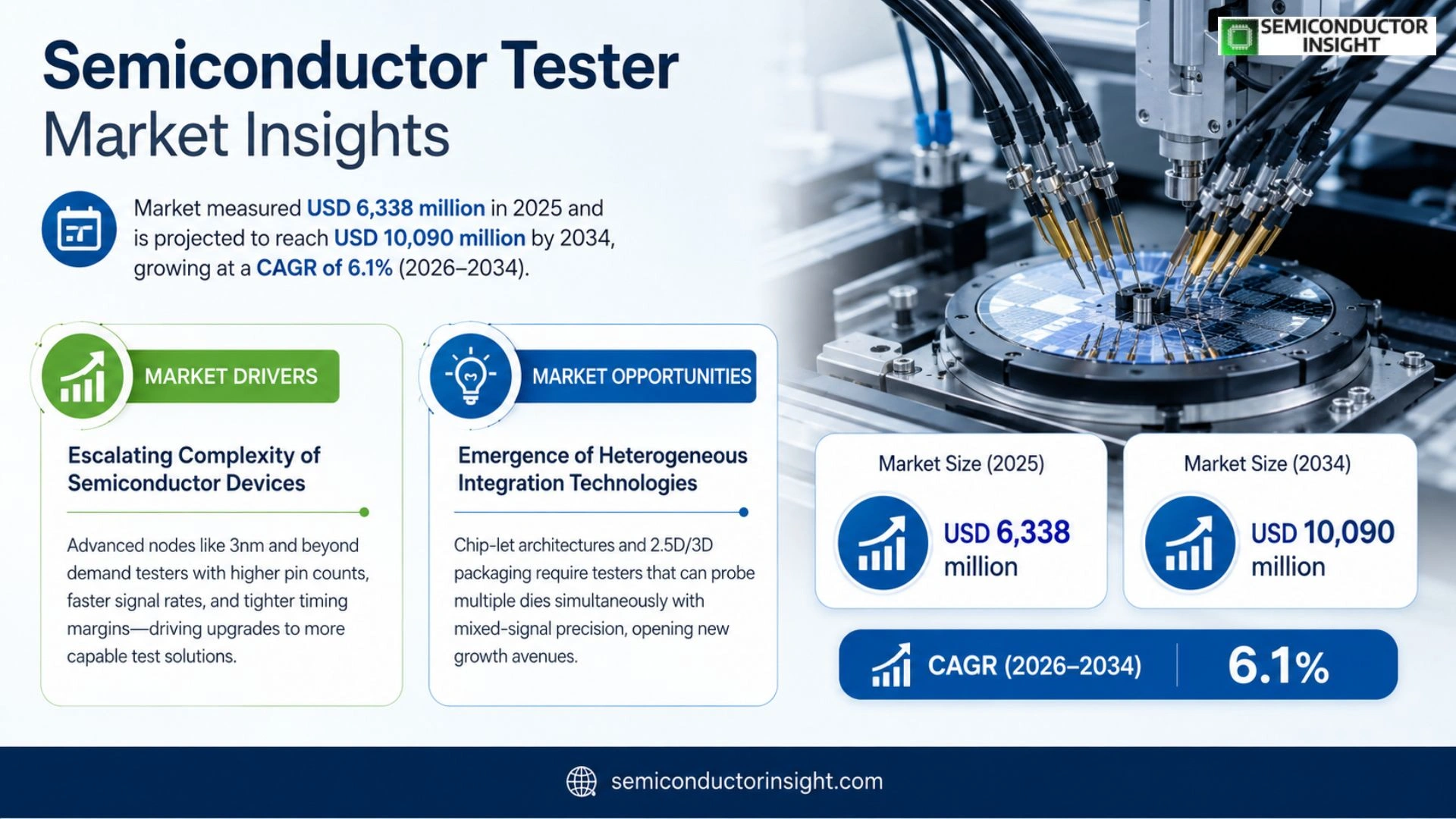

Semiconductor Tester market measured USD 6,338 million in 2025 and rose to USD 10,090 million by 2034, delivering an approximate CAGR of 6.1 % over the period.

Semiconductor testers are precision instruments engineered to verify functionality and performance of stand‑alone integrated circuits, system‑on‑chip (SoC) devices and system‑in‑package (SiP) solutions. The portfolio includes SoC testers, memory testers, RF testers, analog/hybrid testers, power device testers and CIS testers that support developers throughout design validation and volume production.

The expansion of this segment reflects heightened demand from smart terminals, autonomous‑driving platforms, AI computing workloads, next‑generation wireless (5G/6G) infrastructure and data‑center deployments. Because chip complexity continues to climb, manufacturers require faster, more accurate and increasingly automated test equipment. Companies such as Advantest, Teradyne, Hangzhou Changchuan and Cohu have introduced high‑throughput platforms that improve yield while trimming cycle time; their recent product launches underscore a shift toward AI‑assisted diagnostics and modular test architectures.

MARKET DRIVERS

Escalating Complexity of Semiconductor Devices

As the semiconductor industry adopts advanced nodes such as 3 nm and beyond, test equipment must handle higher pin counts, faster signal rates, and tighter timing margins. This technical escalation forces fab operators to upgrade to more capable testers, creating a direct pull for sophisticated Semiconductor Tester Market solutions.

Shift Toward Automation and Yield Optimization

Manufacturers are embedding AI‑enabled analytics into test flows to detect subtle defects early. By automating data collection and analysis, plants can reduce scrap rates and accelerate time‑to‑volume. The value of such capabilities spurs investment in next‑generation testing platforms, reinforcing growth for Semiconductor Tester Market.

➤ “Test throughput gains of 15‑20 % are routinely reported when integrating AI‑driven test‑data analytics.”

Regional expansion, especially in Southeast Asia where new fabs are breaking ground, adds further demand. Local firms are procuring modular test solutions that can be deployed rapidly, ensuring capacity keeps pace with production ramps.

MARKET CHALLENGES

High Capital Expenditure and Short Product Cycles

Investing in a state‑of‑the‑art tester often exceeds $10 million, yet the lifespan of a specific test configuration aligns with the rapid turnover of semiconductor products. Companies must balance the allure of cutting‑edge features against the risk of obsolescence, a tension that tempers purchase decisions.

Other Challenges

Skilled Workforce Shortage

The operation of high‑speed testers demands expertise in signal integrity, software scripting, and data analytics. Tight labor markets in key regions make it difficult for fabs to fully leverage sophisticated equipment, limiting the realized benefits of new test platforms.

Supply‑chain disruptions for precision components, such as high‑frequency probes, occasionally delay deliveries, forcing end‑users to defer upgrades despite clear performance advantages.

MARKET RESTRAINTS

Stringent Regulatory and Environmental Standards

Compliance with emerging e‑waste directives and energy‑efficiency mandates adds an extra layer of cost for equipment manufacturers. Certification processes extend time‑to‑market, discouraging some players from introducing innovative test solutions.

Moreover, the need to retrofit existing test lines to meet new standards can be prohibitively expensive, prompting some fabs to extend the use of legacy systems beyond their optimal performance window.

MARKET OPPORTUNITIES

Emergence of Heterogeneous Integration Technologies

Chip‑let architectures and 2.5 D/3 D packaging demand test equipment capable of probing multiple dies simultaneously with mixed‑signal precision. Vendors that can deliver modular, scalable testers tailored to these configurations stand to capture a sizable share of forthcoming spend.

Additionally, the rise of cloud‑based test‑as‑a‑service platforms offers a subscription model that reduces upfront capital barriers. This approach resonates with midsize fabs seeking flexibility, opening a new revenue stream for Semiconductor Tester Market.

Finally, collaborations between equipment makers and semiconductor OEMs on co‑development projects accelerate feature integration, shortening development cycles and fostering a more responsive ecosystem.

Semiconductor Tester Market Trends

Rising Demand for Advanced SoC Test Solutions

Semiconductor Tester Market recorded a valuation of $6,338 million in 2025, reflecting the intensifying need for high‑performance test equipment as semiconductor designs become increasingly complex. Sales of roughly 54,390 units at an average price of $127.6 per unit underline the volume‑driven nature of the sector, while a gross profit margin near 68 % signals strong pricing power for manufacturers. Drivers such as AI‑enabled computing, autonomous‑driving platforms, smart‑terminal proliferation, and the rollout of 5G/6G networks force chip makers to adopt test solutions capable of handling multi‑gigahertz signaling and dense integration. Consequently, SoC testers, high‑speed memory testers, and RF testers are experiencing heightened adoption, prompting equipment suppliers to prioritize yield‑enhancing features and rapid test‑cycle times.

Other Trends

Shift Toward Automated Test Platforms

Automation is reshaping Semiconductor Tester Market as manufacturers integrate machine‑learning algorithms and closed‑loop control into test stations. The push for faster, more precise, and smarter equipment reduces reliance on manual calibration, cutting cycle times and mitigating human error. Automated platforms enable simultaneous multi‑parameter measurements, which is essential for validating complex system‑in‑package (SiP) and heterogeneous integration designs. For end‑users, this translates into lower total cost of ownership, as higher throughput offsets capital expenditures while maintaining stringent quality standards required for data‑center and IoT semiconductor shipments.

Emergence of Domestic Test Equipment Players

Regional competitors are gaining ground, challenging the traditional dominance of established global vendors. Domestic manufacturers in key Asian markets have accelerated product development cycles, delivering cost‑competitive testers that meet local design specifications for advanced SoC and power devices. This shift introduces pricing pressure and diversifies the supply chain, compelling incumbents to enhance service offerings and invest in differentiated technologies such as inline analytics and predictive maintenance. For buyers, the expanding supplier base provides greater negotiation leverage and reduces exposure to geopolitical constraints, thereby influencing long‑term procurement strategies within Semiconductor Tester Market.

COMPETITIVE LANDSCAPE

Key Industry Players

Semiconductor Tester Market – Competitive Overview 2025‑2032

Advantest and Teradyne continue to dominate the global tester arena, jointly accounting for roughly half of total revenue. Their advantage stems from deep R&D pipelines that integrate high‑speed analog front‑ends with AI‑enhanced pattern generators, enabling them to service large‑volume SoC and memory customers. Both firms have leveraged strategic acquisitions in Europe and the United States to broaden portfolio breadth, reinforcing their position as the primary suppliers to IDMs and leading OSATs. Their pricing power, coupled with robust gross margins, allows sustained reinvestment in next‑generation test architectures that address the emerging 5G/6G and automotive‑grade chips.

The remainder of the landscape is fragmented among specialist and regional manufacturers that target niche segments or price‑sensitive customers. Companies such as Hangzhou Changchuan, Beijing Huafeng, PowerTECH and UNITEST focus on cost‑effective RF and analog testers for midsize fab operations in Asia, where domestic demand is accelerating. European outfits like SPEA S.p.A. and Chroma ATE excel in high‑precision measurement solutions for power‑device testing, while firms such as Cohu and Test Research, Inc. differentiate through modular test platforms that can be rapidly reconfigured for CIS and emerging sensor applications. This diversity of capabilities creates a competitive matrix where clients can mix‑and‑match suppliers based on technology fit, service depth, and total cost of ownership.

List of Key Semiconductor Tester Companies Profiled

- Advantest

- Teradyne

- Cohu

- Chroma ATE

- YC Corporation

- Hangzhou Changchuan

- Beijing Huafeng

- PowerTECH

- UNITEST

- TESEC Corporation

- SPEA S.p.A.

- Exicon

- Macrotest

- ShibaSoku

- Test Research, Inc.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

SoC Testers are viewed as the primary growth engine because they address the most complex integration challenges.

|

| By Application |

|

IDMs dominate the application landscape through deep integration of test flows within their own fabs.

|

| By End User |

|

Chip Designers increasingly influence tester specifications through early‑stage validation requirements.

|

| By Technology Trend |

|

AI‑Enabled Test Automation is reshaping verification workflows through predictive analytics and adaptive test sequencing.

|

| By Market Driver |

|

5G/6G Expansion drives demand for high‑frequency RF testers and ultra‑fast digital test solutions.

|

Regional Analysis: Semiconductor Tester Market

Asia‑Pacific

Designers in the region are integrating heterogeneous integration and chiplet architectures, which push test equipment to support mixed‑technology validation. Vendors respond by offering modular test heads that can be reconfigured on‑the‑fly, reducing capital outlay for test fabs that serve multiple product families.

The surge in fab capacity, especially in advanced nodes, creates a constant demand for higher‑speed test platforms. Test providers are therefore emphasizing ultra‑low latency measurement and parallel testing architectures to keep pace with the output of 3‑nm and sub‑3‑nm lines.

A deep bench of engineers skilled in both semiconductor physics and data science fuels innovation in test algorithms. Companies that embed machine‑learning models into test flow see quicker defect isolation, giving them a competitive advantage in high‑volume production.

Local policy frameworks that streamline component import and protect patents reduce time spent on compliance, enabling test equipment manufacturers to launch new solutions with minimal bureaucratic delay.

North America

North America retains a strong position in Semiconductor Tester Market due to its concentration of leading‑edge design firms and a robust ecosystem of research institutions. The United States, in particular, pushes test technology through collaborations between chip designers and equipment makers that focus on high‑frequency performance and security testing. Customer expectations for rapid scaling of test capacity drive vendors to offer cloud‑enabled test analytics, allowing fab operators to aggregate data across sites for better yield insight. While cost pressures persist, the region’s emphasis on intellectual property protection and a mature procurement process ensure that new test solutions are adopted with a clear ROI narrative.

Europe

European players contribute a sophisticated blend of precision engineering and standards‑driven testing approaches. Countries such as Germany and the Netherlands excel at developing metrology‑focused test instruments that meet stringent automotive and industrial safety requirements. The regional focus on sustainability has spurred interest in test equipment that reduces power consumption and extends hardware lifespan. Partnerships between equipment manufacturers and research consortia accelerate the incorporation of quantum‑ready testing capabilities, positioning Europe as a niche but influential market segment within the broader Semiconductor Tester landscape.

South America

South America’s semiconductor testing footprint is emerging, anchored by a handful of multinational fabs and an expanding domestic electronics sector. Regional distributors prioritize flexible test platforms that can handle a variety of product types, from consumer IoT devices to automotive modules. Investment in workforce upskilling and joint ventures with Asian OEMs is narrowing the technology gap, allowing local fabs to adopt more advanced test strategies without incurring prohibitive capital expense. Market participants view the region as a proving ground for modular test solutions that can be scaled as production volumes increase.

Middle East & Africa

The Middle East & Africa region is characterized by strategic investments in semiconductor testing as part of broader digital transformation agendas. Emerging test centers in the United Arab Emirates and South Africa focus on supporting regional chip packaging and assembly operations. Vendors are tailoring service models that include remote diagnostics and on‑site training, addressing the scarcity of local expertise. The growing emphasis on secure supply chains drives interest in test equipment capable of verifying authenticity and detecting counterfeit components, adding a layer of trust to the nascent market.

Report Scope

This market research report provides a comprehensive analysis of the Semiconductor Tester Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Semiconductor Tester Market?

-> Semiconductor Tester market measured USD 6,338 million in 2025 and rose to USD 10,090 million by 2034

Which key companies operate in Semiconductor Tester Market?

-> Key players include Advantest, Teradyne, Hangzhou Changchuan, Cohu, Chroma ATE, YC Corporation, Beijing Huafeng, PowerTECH, UNITEST, TESEC Corporation, SPEA S.p.A., Exicon, Macrotest, ShibaSoku, Test Research, Inc., Unisic Technology, NI (SET GmbH), AMIDA Technology, YTEC, STATEC, Hitachi Energy, ipTEST Ltd, Shandong Prime-rel, Shaoxing Hongbang, JUNO International, ITEC BV, Lorlin Test Systems, POWORLD Electronic, Tektronix, VX Instruments GmbH.

What are the key growth drivers?

-> Key growth drivers include increasing demand from smart terminals, autonomous driving, AI computing, 5G/6G communications, data centers, and IoT, which boost semiconductor chip demand and consequently tester market growth.

Which region dominates the market?

-> Asia is the dominant region, driven by extensive semiconductor manufacturing activities and rising demand for advanced testing solutions.

What are the emerging trends?

-> Emerging trends include movement towards faster, more accurate, smarter, and highly automated test equipment, with growth points in advanced SoC chips, high‑speed storage, 5G/6G RF chips, power semiconductors, and CIS sensors.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...