Alumina Coated Evaporation Sources Market Insights

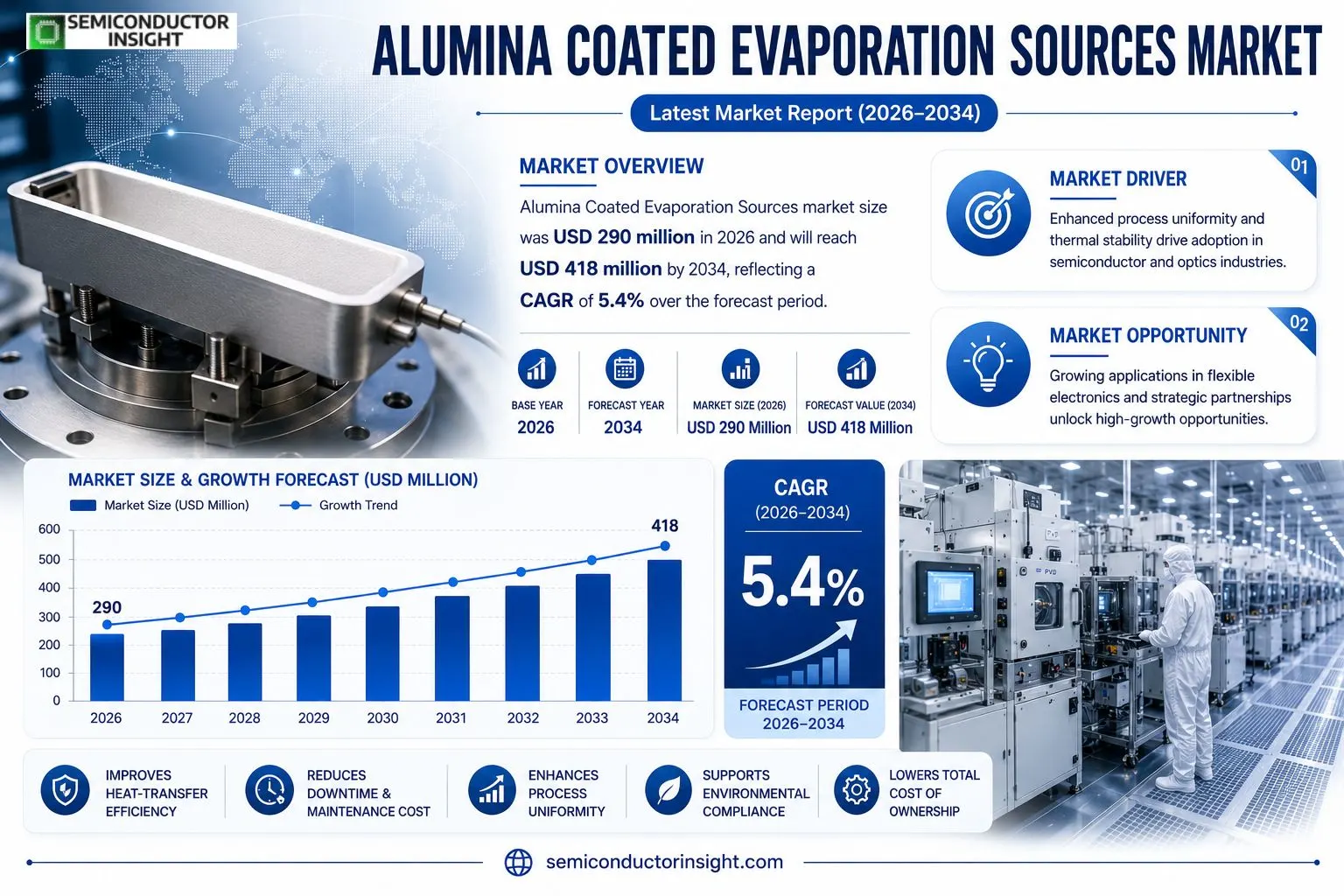

Alumina Coated Evaporation Sources market size was USD 290 million in 2026 and will reach USD 418 million by 2034, reflecting a CAGR of 5.4% over the forecast period.

The Alumina Coated Evaporation Sources are engineered to improve performance and lifespan of evaporation equipment through a thin, durable alumina layer applied on heat‑transfer surfaces. This coating curtails fouling and scaling, enhances heat‑transfer efficiency, and shields components from corrosion, thereby delivering reliable operation and lower total‑ownership cost.The expansion of this market stems from rising demand in semiconductor manufacturing, optics production, solar‑cell fabrication and medical‑equipment sectorsareas where precision thermal processing is essential. Manufacturers are investing in advanced coating technologies and eco‑friendly designs while adopting intelligent monitoring systems that streamline maintenance. As high‑tech industries scale up production volumes, opportunities emerge for suppliers that can offer customized solutions with consistent quality and compliance with emerging environmental standards.

MARKET DRIVERS

Enhanced Process Uniformity

Alumina Coated Evaporation Sources Market benefits from the material’s intrinsic ability to deliver highly uniform thin‑film deposition across large substrates. Manufacturers are capitalising on this attribute to reduce cycle‑time variability, which translates into tighter tolerance windows for advanced semiconductor and display applications. Consistent film thickness directly improves yield, positioning alumina‑coated sources as a preferred choice for high‑value product lines.

Thermal Stability Advantages

Alumina’s superior thermal conductivity allows evaporation sources to operate at elevated temperatures without rapid degradation. This stability enables process engineers to push power densities higher, unlocking new material combinations that were previously untenable. The resulting expanded design envelope is prompting OEMs to integrate these sources into next‑generation optical coating and solar‑cell production lines.

➤ Customers report up to a 15% reduction in downtime when transitioning from conventional quartz to alumina‑coated evaporation modules.

Overall, the convergence of uniformity and thermal resilience is reshaping procurement strategies, compelling end users to allocate a larger share of capital expenditure toward alumina‑based solutions.

MARKET CHALLENGES

Cost Sensitivity in High‑Volume Segments

While performance metrics are compelling, the initial acquisition price of alumina‑coated evaporation sources remains higher than that of traditional alternatives. Mid‑size fabs, which operate under tight margin constraints, often delay adoption until a clear return‑on‑investment justification emerges. This price‑performance calculus slows market penetration despite technical merits.

Other Challenges

Installation Complexity

Integrating alumina‑coated modules into legacy equipment frequently demands bespoke mounting hardware and recalibrated control loops. The engineering effort required can extend commissioning timelines, creating a secondary barrier for manufacturers seeking rapid roll‑out.

MARKET RESTRAINTS

Supply‑Chain Bottlenecks

production of high‑purity alumina relies on a limited number of specialized ceramic vendors. Recent disruptions in raw‑material logistics have led to elongated lead times, which in turn constrain the ability of equipment suppliers to meet surge demand. Supply‑chain volatility therefore acts as a practical ceiling on market expansion.

Regulatory Scrutiny

Stringent emissions and waste‑disposal regulations applicable to high‑temperature processes add compliance costs for end users. In regions where environmental oversight is intensifying, manufacturers must invest in additional monitoring infrastructure, thereby inflating total cost of ownership for alumina‑coated evaporation solutions.

MARKET OPPORTUNITIES

Emerging Applications in Flexible Electronics

Flexible display and wearable sensor manufacturers are exploring deposition techniques that accommodate low‑temperature substrates without sacrificing film quality. Alumina’s ability to maintain structural integrity at modest temperatures makes it a strong candidate for next‑generation roll‑to‑roll coating equipment, opening a niche yet high‑growth avenue for the market.

Strategic Partnerships and Licensing

Major equipment vendors are entering joint‑development agreements with ceramic specialists to co‑create proprietary alumina‑coated source lines. These collaborations aim to shorten development cycles and lock in exclusive supply arrangements, positioning participants to capture a larger slice of future demand.

Alumina Coated Evaporation Sources Market Trends

Increasing Penetration in Semiconductor Fabrication

The latest production data show that output of Alumina Coated Evaporation Sources reached roughly 10.26 million units in the most recent year, with an average transaction price near US$31 per unit. This price‑performance balance is sustaining a gross margin band of 28‑30 % for manufacturers that operate single‑line capacities around 200 k units. Semiconductor manufacturers now account for about half of total downstream demand, while the optics segment contributes roughly one‑fifth. The concentration of demand in high‑mix, high‑volume silicon processing drives suppliers to prioritize yield‑enhancing coating integrity and to streamline supply‑chain logistics. Companies that can keep unit costs low while delivering the thin, durable alumina barrierknown to curb fouling and improve heat transferare securing repeat business from fab lines that value predictable uptime and reduced cleaning cycles. Consequently, the competitive landscape is shifting toward firms that couple robust margin structures with responsive technical support.

Other Trends

Advancements in Coating Application Methods

Recent R&D initiatives focus on plasma‑enhanced deposition and atomic‑layer techniques that produce more uniform alumina films at lower temperatures. These methods address two long‑standing operational constraints: thermal stress on delicate substrates and variability in coating thickness that can affect heat‑exchange efficiency. By integrating in‑line monitoring sensors, manufacturers are able to adjust process parameters in real time, thereby reducing scrap rates and extending component lifespan. The move toward modular coating stations also aligns with the broader industry push for flexible production layouts, allowing equipment users to retrofit existing evaporation rigs without extensive downtime.

Emphasis on Environmental Compliance and Compact System Design

Regulatory scrutiny on energy consumption and hazardous waste is prompting vendors to package Alumina Coated Evaporation Sources in more compact, energy‑efficient chassis. Design teams are exploring lightweight alloys and optimized airflow paths that lower overall power draw while maintaining the protective benefits of the alumina layer. Simultaneously, service contracts are evolving to include predictive maintenance analytics, helping end‑users meet compliance targets without sacrificing throughput. This convergence of sustainability goals with operational efficiency is reshaping purchase criteria, encouraging buyers to evaluate total cost of ownership rather than initial capital outlay alone. Firms that can demonstrate measurable reductions in carbon footprint and operational expense are poised to capture a larger share of the emerging market landscape.

COMPETITIVE LANDSCAPE

Key Industry Players

Alumina Coated Evaporation Sources Market – Competitive Overview

The market is anchored by a handful of firms that have combined extensive coating know‑how with large‑scale production lines. Kurt J. Lesker Company commands the largest share, leveraging a single‑line capacity of roughly 200 k units and a gross margin near 29 %. Its vertically integrated supply chain, from high‑purity alumina powder to precision sputtering equipment, enables the firm to meet the heavy demand from semiconductor manufacturers, which represent about half of total consumption. Lesker’s strategy of bundling customized coating processes with predictive maintenance services creates a recurring revenue stream and raises barriers for new entrants attempting to duplicate its cost structure.Beyond the dominant player, a constellation of niche specialists enriches the competitive fabric. RD Mathis and Neyco focus on optical and medical‑equipment applications, where coating uniformity and low‑contamination thresholds are paramount. Angstrom and Advanced Engineering Materials have differentiated themselves through research‑driven development of hybrid alumina‑tungsten layers that improve heat‑transfer efficiency in solar‑cell production. Regional champions such as Shandong Pengcheng Advanced Ceramics and Suzhou Keyue Materials supply the Asian market, capitalizing on proximity to high‑tech fabs and benefiting from local material‑science clusters. These firms often pursue strategic collaborations with equipment OEMs to co‑develop compact source designs that address space constraints in next‑generation manufacturing lines.

List of Key Alumina Coated Evaporation Sources Companies Profiled

- Kurt J. Lesker Company

- RD Mathis

- Neyco

- Angstrom

- Advanced Engineering Materials

- Demaco Vacuum

- Kennametal (Sintec Group)

- Shandong Pengcheng Advanced Ceramics

- Suzhou Keyue Materials

- Ted Pella

- Kojundo

- Thermo Scientific

- Plasma Technology Ltd.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Boat Type is emerging as the preferred architecture because it provides superior thermal uniformity, reduces fouling risk, and enables easier integration with modular evaporation systems. – Engineers cite its flexibility for scaling production lines. – The design supports rapid maintenance cycles, enhancing overall equipment uptime. – Users appreciate the reduced cleaning frequency driven by the smooth alumina coating surface. |

| By Application |

|

Semiconductor drives the most vigorous adoption of alumina‑coated sources, largely due to its demand for ultra‑clean deposition environments and high‑temperature stability. – The coating mitigates particle contamination, supporting tighter process windows. – It extends source lifespan, which is critical for high‑volume chip fabs. – Manufacturers value the consistent heat‑transfer efficiency that improves yield consistency. |

| By End User |

|

Manufacturing Plants benefit from the robustness of alumina coated sources, which translates into higher production reliability and lower downtime. – Plant operators highlight the reduced scaling incidents that keep processes running continuously. – The coating aligns with sustainability goals by lowering cleaning chemical usage. – Service teams report that predictive maintenance tools integrate more smoothly with the stable performance profile of alumina sources. |

| By Coating Material |

|

Alumina‑Coated Molybdenum enjoys preference because of its balanced thermal conductivity and mechanical resilience. – It delivers stable heat flux across a wide temperature range. – The material tolerates repeated thermal cycling, supporting long‑term source stability. – Users note the ease of integrating molybdenum substrates with existing furnace designs. |

| By Size |

|

Large Size sources are gaining traction in high‑throughput production environments where greater evaporation capacity and longer service intervals are critical. – They support wider batch volumes, reducing change‑over times. – The larger thermal mass contributes to more uniform temperature distribution. – Operators appreciate the lower frequency of source replacement, which improves overall cost efficiency. |

Regional Analysis: Alumina Coated Evaporation Sources Market

Europe

High‑volume photonic devices and next‑generation display panels demand ultra‑clean deposition environments; alumina coatings suppress particle emission, aligning with manufacturers’ quality imperatives. Concurrently, stringent environmental regulations elevate the importance of materials that minimise waste and enable longer tool lifespans, reinforcing market traction.

A dense supplier base in Germany, France and the Nordics ensures rapid access to high‑purity alumina powders and precision machining services. This geographic concentration shortens order‑to‑delivery cycles and facilitates collaborative engineering, which is a decisive advantage over more fragmented markets.

EU directives on cleanroom standards and hazardous material handling indirectly favour alumina‑coated sources, as they reduce volatile compound emissions. Compliance audits often cite source material purity, prompting fab managers to prioritize equipment that demonstrably meets these thresholds.

Collaborative projects between equipment OEMs and university labs accelerate the rollout of next‑gen source geometries. The resulting design refinementssuch as optimized emissivity gradientsenhance deposition uniformity, positioning Europe at the forefront of technological progress in the market.

North America

In North America, Alumina Coated Evaporation Sources Market is shaped by a blend of high‑value defense contracts and a robust aerospace supply chain. U.S. fabs value the reliability offered by alumina coatings but temper adoption with cost‑conscious budgeting, especially in smaller facilities. Nevertheless, a wave of strategic partnerships between domestic OEMs and research institutions is catalysing incremental improvements in source durability. Regulatory scrutiny on chemical usage pushes firms toward materials that minimise hazardous by‑products, a niche where alumina‑coated sources excel. Market participants are therefore positioning themselves to capture projects that demand the highest cleanliness standards, even as they negotiate tighter cost structures.

Asia‑Pacific

The Asia‑Pacific region exhibits a contrasting dynamic, where rapid capacity expansion coexists with intense price competition. Nations such as China, South Korea, and Taiwan are scaling advanced display and semiconductor fabs, creating a sizable pipeline for deposition equipment. While budget constraints drive many manufacturers toward lower‑cost alternatives, the growing prevalence of premium‑grade productsparticularly in OLED and micro‑LED segmentscreates pockets of demand for alumina‑coated sources. Regional trade shows and government‑backed R&D incentives are fostering a collaborative climate that encourages local suppliers to enhance material purity, gradually narrowing the technology gap with Europe.

South America

South America remains an emerging frontier for Alumina Coated Evaporation Sources Market. Investment in high‑technology manufacturing is modest, yet academic laboratories and niche research facilities are increasingly experimenting with thin‑film deposition for medical imaging and scientific instrumentation. These early adopters value the low‑contamination profile of alumina coatings, as it directly impacts experimental fidelity. Although the commercial scale is limited, the region’s gradual shift toward advanced materials research signals a latent opportunity for equipment providers willing to tailor service models to smaller, knowledge‑driven customers.

Middle East & Africa

In the Middle East and Africa, market activity is anchored around nascent solar‑cell manufacturing and a handful of display assembly plants. Governments are launching diversification programmes that earmark funds for high‑tech manufacturing, subtly nudging local fabs toward process purity standards. Alumina‑coated evaporation sources are perceived as a strategic asset that can reduce contamination‑related yields loss, a critical consideration for cost‑sensitive ventures. While adoption remains at an exploratory stage, the combination of policy support and a growing appetite for advanced optics positions the region for incremental growth as expertise matures.

Report Scope

This market research report provides a comprehensive analysis of the Alumina Coated Evaporation Sources Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Alumina Coated Evaporation Sources Market?

-> Alumina Coated Evaporation Sources Market was valued at USD 290 million in 2026 and is expected to reach USD 418 million by 2034, registering a CAGR of 5.4% during the forecast period.

Which key companies operate in Alumina Coated Evaporation Sources Market?

-> Key players include Kurt J. Lesker Company, RD Mathis, Neyco, Ted Pella, Kojundo, Angstrom, Advanced Engineering Materials, Demaco Vacuum, Kennametal (Sintec Group), Shandong Pengcheng Advanced Ceramics, Suzhou Keyue Materials.

What are the key growth drivers?

-> Key growth drivers include rapid development of high‑tech industries, increasing demand for semiconductor and optics applications, technological innovation in coating processes, and expanding precision manufacturing requirements.

Which region dominates the market?

-> Regional dominance data is not disclosed in the available source.

What are the emerging trends?

-> Emerging trends include development of high‑performance and environmentally friendly coating technologies, intelligent monitoring systems, compact design solutions, and enhanced service and technical support to meet sustainability and efficiency goals.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...