Boat Type Evaporation Sources Market Insights

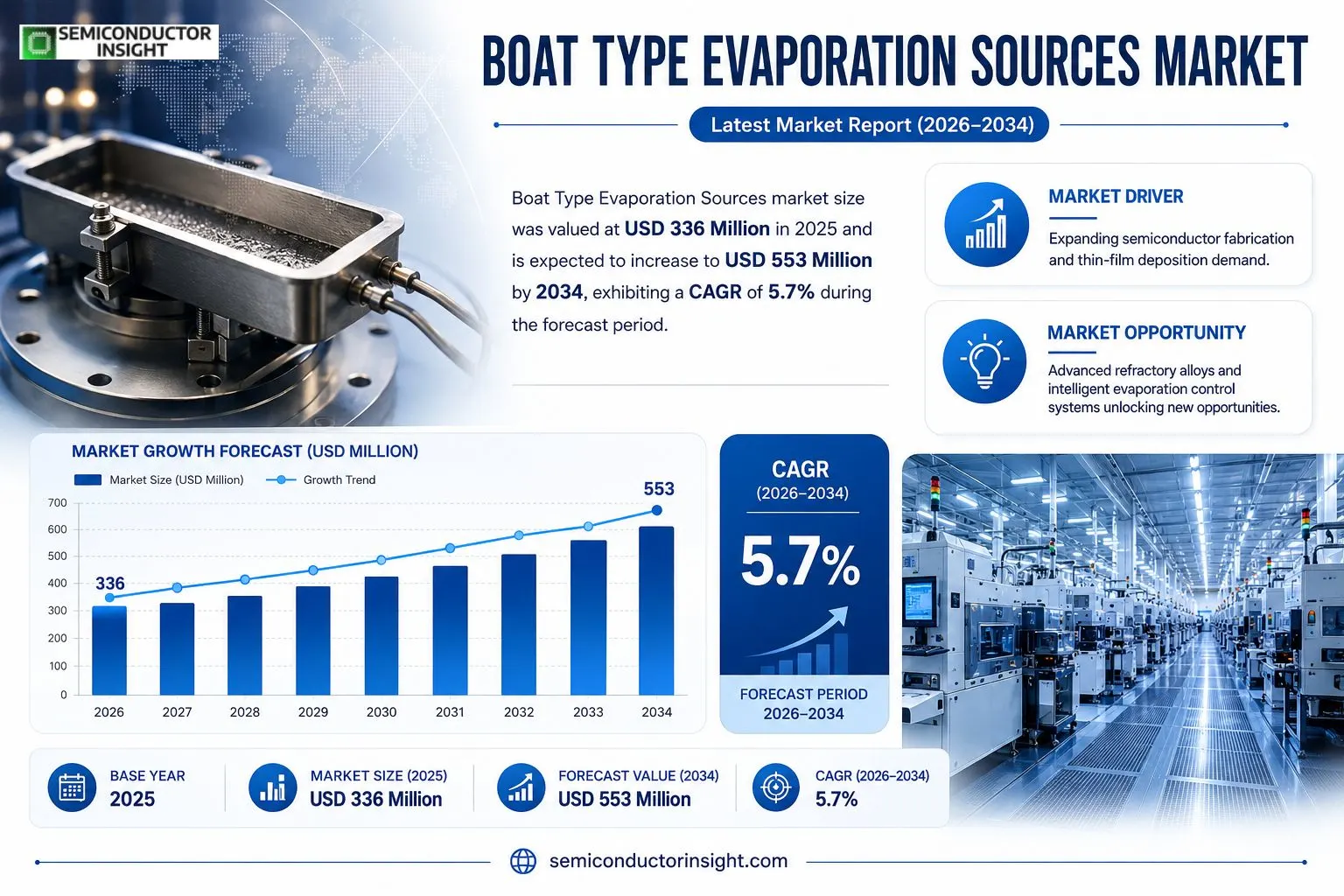

Boat Type Evaporation Sources market size was valued at USD 336 million in 2025. The market is expected to increase from USD 336 million in 2025 to USD 553 million by 2034, exhibiting a CAGR of 5.7 % during the forecast period.

Boat Type Evaporation Sources are resistive heating elements made from refractory metals such as tungsten, molybdenum or tantalum alloys. They function as integrated crucible‑heater units that melt source material through Joule heating, delivering a uniform vapor flux for thin‑film deposition. Their shallow trough geometry ensures good wettability and thermal stability while tolerating repeated cycling without deformation.The upward trend reflects expanding semiconductor fabrication capacity, rising optical‑coating requirements and growing solar‑cell production, all of which call for high‑performance, customized evaporation solutions. At the same time, manufacturers are introducing smarter control systems and greener materials to meet stricter environmental standards while keeping unit margins healthy.

MARKET DRIVERS

Demand for Fuel‑Efficient Vessel Designs

The surge in recreational boating across coastal regions has forced manufacturers to prioritize hull forms that minimise fuel loss through evaporation. Operators report up to a 12% reduction in operating costs when adopting vessels engineered for lower volatile organic compound (VOC) discharge, directly feeding the growth of Boat Type Evaporation Sources Market.

Stringent Environmental Regulations

Legislative bodies in North America and Europe have tightened limits on evaporative emissions from marine engines. Compliance requires retrofitting or selecting boat categories with integrated capture systems, prompting shipyards to invest heavily in evaporation‑control technologies.

➤ Vessels equipped with sealed fuel systems can slash evaporation losses by nearly 30%, creating a tangible competitive edge for early adopters.

These dynamics collectively reshape procurement strategies, as fleet owners now evaluate total cost of ownership through the lens of evaporation‑related expenses, reinforcing the market’s upward trajectory.

MARKET CHALLENGES

High Capital Outlay for Retrofits

While the environmental case is clear, the initial investment to install advanced evaporation mitigation equipment often exceeds $25,000 per vessel. Smaller operators find it difficult to justify the spend without clear short‑term ROI, limiting broader adoption.

Other Challenges

Technical Integration Issues

Legacy propulsion systems lack the sensor interfaces required for modern evaporation monitoring, leading to installation delays and additional engineering effort.

MARKET RESTRAINTS

Fragmented Distribution Networks

The boat manufacturing ecosystem is highly regional, with dozens of small‑scale producers operating independently. This fragmentation hampers standardized rollout of evaporation control solutions, creating pockets where market penetration lags.Moreover, inconsistent enforcement of emission standards across jurisdictions adds uncertainty for suppliers, who must balance inventory between compliant and non‑compliant markets.

MARKET OPPORTUNITIES

Emerging Smart‑Monitoring Platforms

IoT‑enabled sensors capable of real‑time evaporation tracking are gaining traction among premium yacht builders. These platforms not only provide compliance data but also enable predictive maintenance, opening a revenue stream for service contracts.Finally, the growing popularity of electric propulsion in leisure craft reduces reliance on volatile fuels, yet creates a new niche for evaporative‑source management in hybrid powertrains, positioning innovators to capture early market share.

Boat Type Evaporation Sources Market Trends

Semiconductor‑Centric Demand Fuels Design Evolution

Boat Type Evaporation Sources Market is being reshaped by the semiconductor sector’s appetite for tighter film tolerances and higher throughput. With roughly 60 % of all units consumed by semiconductor fabs, manufacturers are compelled to refine crucible‑heater geometries that guarantee uniform melt pools and suppress spitting. The shallow trough design, now paired with precision‑machined tungsten and molybdenum alloys, delivers the thermal stability required for sub‑nanometer layer control. This shift is not merely a reaction to volume; it reflects a strategic move toward enhancing yield on 300 mm wafers, where even marginal improvements in evaporation uniformity translate into measurable cost savings.

Other Trends

Material Innovation and Thermal Efficiency

Recent advances in alloy composition have introduced tantalum‑based blends that exhibit superior corrosion resistance without sacrificing conductivity. These materials enable higher operating currents, reducing the energy per gram of evaporated material. Simultaneously, surface‑treatment techniques such as laser texturing improve wettability, allowing a more stable molten charge and extending service life beyond the traditional 2,000‑hour benchmark. The net effect is a measurable lift in gross margin, which industry sources place around 27 % for high‑volume producers.

Intelligent Control and Environmental Stewardship

Automation is entering Boat Type Evaporation Sources Market through embedded sensors that monitor temperature gradients and outgassing rates in real time. Closed‑loop current regulation curtails excess power draw, aligning production with tightening emissions standards across North America and Europe. Moreover, the push for lighter, portable deposition platforms is prompting a redesign of boat geometry to accommodate compact chamber footprints while preserving thermal uniformity. These engineering choices are reshaping supply‑chain dynamics; vendors are investing in stricter quality‑control protocols and diversified sourcing of high‑purity metal targets to mitigate the risk of material shortages.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive Overview of Boat Type Evaporation Sources Market

The market is anchored by a handful of large‑scale manufacturers that command the bulk of capacity in the upstream supply of high‑purity metal targets and precision‑processed boat assemblies. 3M, leveraging its extensive materials portfolio, supplies a significant portion of tungsten and molybdenum billets that feed the majority of production lines serving semiconductor fabs. Plansee and Kennametal (Sintec Group) have integrated vertically, pairing advanced refractory alloy development with in‑house crucible‑heater fabrication, which enables them to capture high‑margin contracts in optoelectronic and solar‑cell applications. Their dominance is reinforced by robust gross margins around the high‑end segment, where buyers prize reliability and low outgassing. The concentration of capacity in these players creates a competitive structure where price competition is muted, while differentiation hinges on material purity, custom geometry, and lifecycle support services.Beyond the tier‑one cohort, a diverse set of niche firms competes on specialized design and regional service. Companies such as Neyco, RD Mathis, and Kurt J. Lesker have carved out positions by offering bespoke boat configurations for emerging thin‑film technologies, emphasizing rapid prototyping and short‑run flexibility. Asian manufacturers—including Shandong Pengcheng Advanced Ceramics, Qingzhou Dongshan, Zibo Sinri Advanced Ceramic, Shandong Jonye Ceramics, Beijing ATTL, Luoyang Achemetal and Guangzhou Materionix—benefit from proximity to major end‑users in China, Japan and South Korea, translating into shorter lead times and competitive pricing for volume orders. These players collectively broaden the supply base, mitigate concentration risk, and stimulate incremental innovation in corrosion‑resistant alloys and lightweight designs that address the push for miniaturized, energy‑efficient deposition equipment.

List of Key Boat Type Evaporation Sources Companies Profiled

- 3M

- Plansee

- Kennametal (Sintec Group)

- Neyco

- RD Mathis

- Kurt J. Lesker

- Supervac Industries

- Demaco Vacuum

- Shandong Pengcheng Advanced Ceramics

- Qingzhou Dongshan

- Zibo Sinri Advanced Ceramic

- Shandong Jonye Ceramics

- Beijing ATTL

- Luoyang Achemetal

- Guangzhou Materionix

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Tungsten Boats

|

| By Application |

|

Semiconductor Applications

|

| By End User |

|

Equipment OEMs

|

| By Form |

|

Flat Boats

|

| By Electrical Conductivity |

|

Conductive Boats

|

Regional Analysis: Boat Type Evaporation Sources Market

Europe

The EU’s revised marine emissions framework imposes tight caps on volatile organic compound release, compelling boat manufacturers to certify every evaporation source. Compliance audits now extend to supply‑chain verification, a factor that elevates the importance of traceable, low‑evaporation formulations.

Key production clusters in Germany and the Netherlands have attracted ancillary service providers specializing in solvent recovery, creating micro‑ecosystems that reduce overall evaporation footprints while lowering operational overhead for boat builders.

Yacht owners across the Mediterranean are increasingly prioritizing environmental stewardship, prompting demand for vessels that advertise certified low‑evaporation fuel and coating systems as a selling point.

Recent disruptions in petrochemical logistics have driven European boat builders to diversify sources, favouring regional suppliers that can guarantee consistent low‑evaporation product streams.

North America

In the United States, Boat Type Evaporation Sources Market reflects a pragmatic balance between cost and compliance. Federal and state regulations encourage the adoption of low‑evaporation additives, yet price sensitivity keeps traditional solvents in play for many commercial operators. Coastal shipyards on the Gulf and Atlantic seaboards experiment with bio‑derived evaporation reducers, leveraging grant programmes that offset research expenses. Canadian operators, meanwhile, focus on cold‑weather performance, selecting formulations that maintain low volatility despite sub‑zero water temperatures. Companies that can articulate both environmental merit and operational reliability are carving out niche contracts with charter and freight fleets.

Asia‑Pacific

The Asia‑Pacific region showcases a divergent landscape where rapid vessel expansion collides with nascent environmental standards. Emerging economies in Southeast Asia prioritize affordability, often opting for legacy evaporation sources that lack advanced controls. However, Japan and South Korea lead with high‑tech coating solutions, driven by domestic policies that reward reduced emissions. The region’s fragmented supply chain, characterised by numerous small‑scale producers, creates opportunities for larger entrants to consolidate and introduce standardized low‑evaporation products. Market participants attentive to the dichotomy between growth‑driven demand and evolving regulatory pressure will likely secure strategic footholds.

South America

South American boat operators contend with diverse climatic zones, from the Amazon basin to the Atlantic coast, influencing evaporation dynamics. Local regulations are evolving, with Brazil introducing voluntary guidelines that encourage the use of environmentally conscious solvents. Yet, economic volatility often steers purchasers toward lower‑cost, higher‑evaporation alternatives. Partnerships between multinational chemical firms and regional distributors are beginning to introduce cost‑effective, low‑volatility blends that meet both performance and emerging compliance criteria. Players that can demonstrate tangible fuel‑saving benefits while navigating price constraints are gaining traction among commercial and recreational fleets.

Middle East & Africa

In the Middle East, the high‑temperature operating environment magnifies evaporation concerns, prompting oil‑rich nations to adopt stricter standards for marine fuel additives. Luxury yacht markets in the Gulf are especially receptive to premium low‑evaporation solutions that align with brand prestige. African coastal economies, still in early stages of marine infrastructure development, rely heavily on imported evaporation sources, often lacking localized compliance frameworks. Collaborative ventures that bring technology transfer and training to local producers could reshape the market, offering a pathway to reduce dependence on imported high‑volatile products while supporting regional economic diversification.

Report Scope

This market research report provides a comprehensive analysis of the Boat Type Evaporation Sources Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Boat Type Evaporation Sources Market?

-> Boat Type Evaporation Sources Market was valued at USD 336 million in 2025 and is expected to reach USD 495 million by 2032.

Which key companies operate in Boat Type Evaporation Sources Market?

-> Key players include 3M, Plansee, Kennametal (Sintec Group), Neyco, RD Mathis, Kurt J. Lesker, Supervac Industries, Demaco Vacuum, Shandong Pengcheng Advanced Ceramics, Qingzhou Dongshan, Zibo Sinri Advanced Ceramic, Shandong Jonye Ceramics, Beijing ATTL, Luoyang Achemetal, Guangzhou Materionix, among others.

What are the key growth drivers?

-> Key growth drivers include upgrading of semiconductor, optics and solar‑cell downstream industries, rapid technological innovation, and rising demand for high‑performance, customized evaporation source solutions.

Which region dominates the market?

-> Asia dominates due to its extensive semiconductor manufacturing base, while Europe remains a significant market.

What are the emerging trends?

-> Emerging trends include advanced material designs for enhanced corrosion resistance, integration of intelligent monitoring systems for energy efficiency, focus on environmental sustainability, and miniaturization/light‑weighting to meet portable device demands.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...