Electronics Industry X-ray Inspection Equipment Market Insights

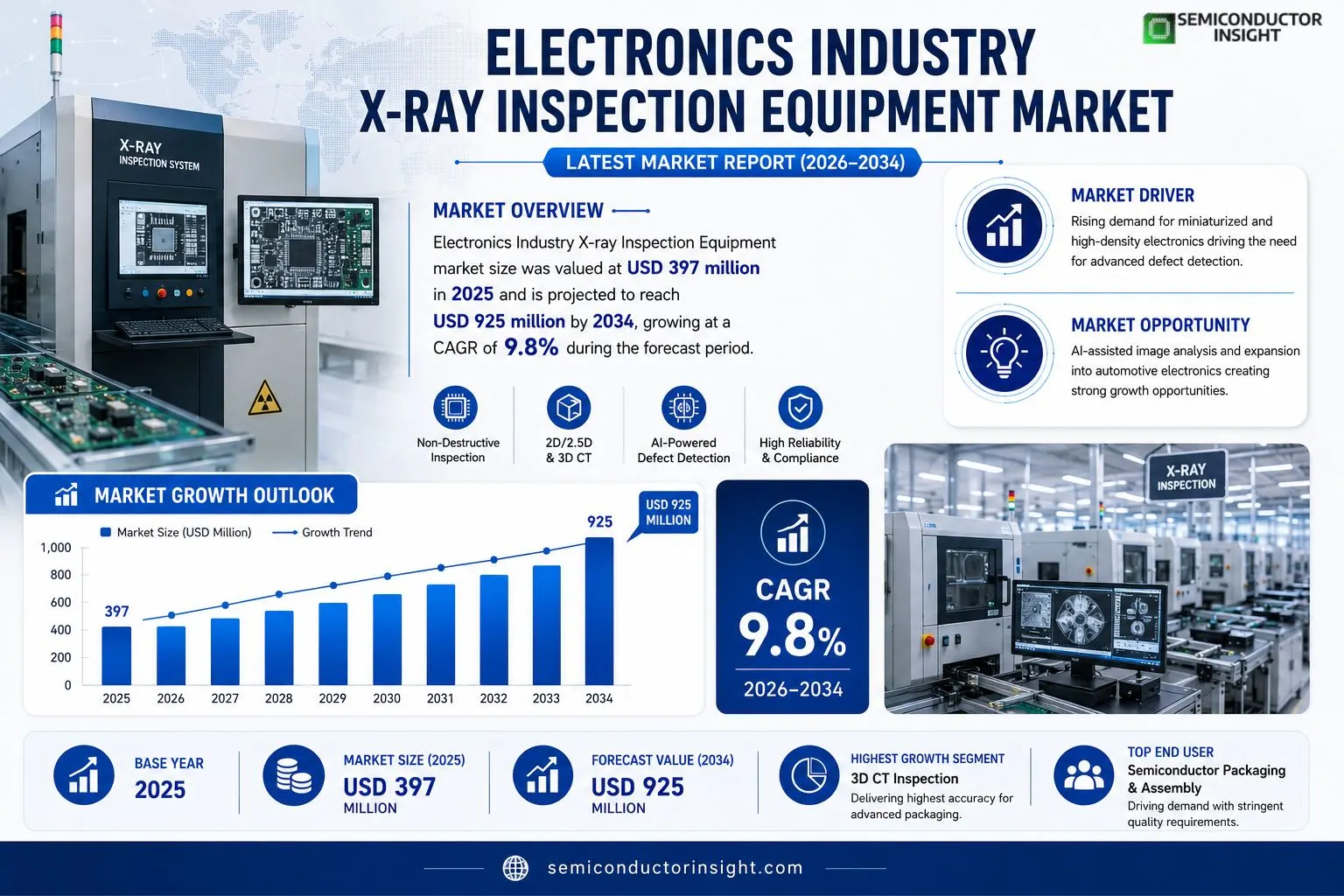

Electronics Industry X-ray Inspection Equipment market size was valued at USD 397 million in 2025. The market is projected to grow from USD 397 million in 2025 to USD 925 million by 2034, exhibiting a CAGR of approximately 9.8% during the forecast period.

Electronics Industry X‑ray Inspection Equipment comprises non‑destructive inspection and quality‑data systems used across PCB/PCBA production, semiconductor packaging, power modules and precision devices. It integrates a micro‑focus or high‑power X‑ray source, high‑resolution detectors, precision motion stages and shielding with capabilities such as 2D radiography, 2½D tomosynthesis/laminography and full‑3D CT reconstruction together with automated defect recognition and quantitative analytics.The market is gaining traction because hidden internal defectssolder voids, bridging, cracks or foreign material in BGA/QFN/Flip‑Chip jointscannot be reliably detected by optical methods alone. Drivers include rising demand for high‑density interconnects, increased adoption of advanced packaging formats and government programmes accelerating digital transformation in electronics manufacturing. Leading suppliers such as ViTrox, Viscom, Nordson, Omron and NIKON differentiate through modular platform designs, AI‑assisted decisioning and richer software licensing models; recent announcements highlight expanded CT capabilities and tighter integration with MES/QMS traceability solutions.

MARKET DRIVERS

Increasing Demand for Miniaturized Electronics

The relentless push toward smaller, more densely populated circuitry has heightened the need for precise defect detection. Electronics Industry X-ray Inspection Equipment Market providers are benefiting from manufacturers’ willingness to invest in technologies that can resolve sub‑micron anomalies without halting production lines.

Regulatory Pressure for Defect Detection

Stringent safety and reliability standards, especially in aerospace and medical device sectors, compel OEMs to adopt certified inspection solutions. Companies that can demonstrate compliance through rapid X‑ray imaging gain a decisive advantage in winning high‑value contracts.

➤ Real‑time X‑ray imaging accelerates yield improvements and reduces costly re‑work cycles.

Overall, the convergence of component miniaturization and tighter regulatory oversight is creating a fertile environment for equipment vendors, encouraging both product innovation and price‑premium positioning.

MARKET CHALLENGES

Complexity of Multi‑Layered PCBs

Modern printed‑circuit boards now feature upwards of ten active layers, each with different material compositions. This architectural depth complicates X‑ray penetration, forcing operators to balance resolution against throughput, which can erode productivity gains.

Other Challenges

High Capital Expenditure

The upfront cost of high‑resolution X‑ray systems remains a barrier for small‑to‑mid‑size manufacturers, limiting market diffusion despite clear long‑term ROI.Furthermore, the need for periodic calibration and specialized maintenance contracts adds recurring expense, prompting some players to defer upgrades in favor of legacy equipment.

MARKET RESTRAINTS

Limited Skilled Workforce

Operating advanced X‑ray inspection tools requires technicians with expertise in radiation safety, image interpretation, and equipment troubleshooting. The scarcity of such talent hampers rapid adoption across Electronics Industry X-ray Inspection Equipment Market.

Integration with Existing Production Lines

Manufacturers often run tightly scheduled assembly lines; inserting an X‑ray station can disrupt flow if not seamlessly integrated. The engineering effort needed to harmonize inspection cycles with upstream and downstream processes deters some firms from immediate deployment.

Supply Chain Volatility

Component shortages and fluctuating raw‑material costs propagate through the equipment supply chain, leading to lead‑time extensions that make budgeting for new inspection assets unpredictable.

MARKET OPPORTUNITIES

Adoption of AI‑Assisted Image Analysis

The integration of machine‑learning algorithms into X‑ray systems enables automated defect classification, reducing reliance on human interpretation. Early adopters report faster decision cycles and higher detection confidence, positioning this capability as a strong growth lever for Electronics Industry X-ray Inspection Equipment Market.

Expansion into Automotive Electronics

Electrified power‑train components and advanced driver‑assistance systems demand rigorous quality control. Suppliers that tailor X‑ray solutions to the automotive supply chain can capture market share as vehicle electronics become increasingly sophisticated.

Modular System Design for Flexible Production

Modularity allows manufacturers to scale inspection capacity in line with volume fluctuations. Vendors offering plug‑and‑play modules are well‑positioned to attract customers seeking agile, cost‑effective upgrades without complete system overhauls.

Electronics Industry X-ray Inspection Equipment Market Trends

Shift Toward In‑Line 3D CT Inspection

The latest production data shows that manufacturers are moving from isolated defect spotting to comprehensive internal‑structure analysis on the shop floor. With unit prices hovering around US$147 and annual output close to 3,000 systems, suppliers have enough scale to embed 3‑dimensional computed‑tomography (CT) modules directly into high‑volume lines. This evolution is driven by the rise of stacked‑die and high‑density interconnect (HDI) packages, where solder voids, micro‑cracks, and foreign particles lie beyond the reach of conventional 2D radiography. By integrating CT inline, fabs can capture quantitative defect metrics in real time, link them to statistical process control (SPC) logs, and trigger corrective actions without stopping the line. The approach reduces yield loss on advanced semiconductor and PCB assemblies, converting what was formerly a sampling expense into a cost‑avoidance engine for Electronics Industry X-ray Inspection Equipment Market.

Other Trends

Software and AI Integration

Beyond hardware upgrades, the competitive edge now rests on analytics platforms that translate raw radiographic data into actionable intelligence. Vendors are bundling AI‑powered defect classifiers, automated root‑cause libraries, and closed‑loop traceability dashboards with their imaging suites. These tools draw on labeled image repositories amassed over several generations of equipment, enabling near‑zero false‑call rates for complex geometries such as BGA, QFN and flip‑chip joints. As a result, service contracts and software licensing have become a larger share of total revenue, pushing gross margins toward the upper end of the historical 35‑55 % band. Early adopters report faster new‑product introductions because design‑for‑inspectability checks can be simulated digitally, shortening the NPI cycle and improving time‑to‑market for high‑performance electronics.

Margin Pressure and Service‑Driven Revenue

While equipment pricing remains relatively stable, manufacturers face tight cost structures in tube and detector supply chains, prompting a shift toward recurring‑revenue models. Companies that have modularized the tube‑detector‑motion platform can offer upgrade pathways, allowing customers to add CT capability or AI modules without a full system replacement. This strategy not only cushions margin erosion from raw‑material volatility but also deepens customer lock‑in through integrated maintenance and calibration services. In the broader Electronics Industry X-ray Inspection Equipment Market, the blend of hardware, software, and aftermarket support is becoming the hallmark of market leaders, aligning profitability with the growing demand for traceable, data‑rich inspection solutions.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive Dynamics of Electronics X‑ray Inspection Equipment Market

ViTrox continues to dominate the segment through a modular platform that couples high‑power microfocus tubes with AI‑enhanced defect analytics. Its ability to ship fully calibrated systems rapidly has translated into a de‑facto standard for inline PCB inspection, especially where 3‑D CT and quantitative defect mapping are required. The company’s margin profile benefits from recurring software licences and service contracts, which lock in revenue beyond the initial hardware sale. By continuously upgrading detector arrays and integrating advanced motion control, ViTrox not only sustains its lead in imaging clarity but also shapes customers’ expectations around traceability and closed‑loop quality assurance.Beyond the market leader, a cohort of specialised firms fuels the ecosystem. Viscom leverages heritage in high‑resolution detectors to serve niche aerospace and defense assemblers, while Nordson’s strong service network accelerates adoption in high‑volume automotive lines. Omron and Unicomp Technology differentiate through lean integration packages that target small‑batch and prototype fabs. Nikon’s optical pedigree informs its hybrid X‑ray/optical solutions, and Waygate Technologies (Baker Hughes) focuses on rugged, oil‑field‑ready platforms for power‑module inspection. Companies such as Comet Yxlon, Test Research Inc. (TRI), and Seamark ZM capture regional demand by offering cost‑effective 2‑D systems, whereas ZEISS and Saki Corporation push the envelope with ultra‑high‑resolution CT for advanced packaging. This diversified landscape creates ample room for partnership, technology licensing, and incremental market capture.

List of Key Electronics Industry X-ray Inspection Equipment Companies Profiled

- ViTrox

- Viscom

- Nordson

- Omron

- Unicomp Technology

- Nikon

- Waygate Technologies (Baker Hughes)

- Comet Yxlon

- Test Research Inc. (TRI)

- Seamark ZM

- Zhengye Technology

- ZEISS

- Saki Corporation

- XAVIS Co., Ltd.

- SEC

- Techvalley

- Goepel Electronic

- Scienscope

- SXRAY

- Creative Electron

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Inline X‑ray Inspection

|

| By Application |

|

PCB Industry

|

| By End User |

|

Semiconductor Packaging

|

| By [Segment Category 3]] |

|

3D CT Technology

|

| By [Segment Category 4]] |

|

Inline Deployment

|

Regional Analysis: Electronics Industry X-ray Inspection Equipment Market

Asia‑Pacific

Foundries in Taiwan, South Korea, and China are scaling line‑up capabilities, creating a ripple effect that intensifies demand for inspection tools capable of handling larger wafer volumes while maintaining defect detection fidelity.

Regional standards bodies are tightening defect‑rate thresholds for high‑density interconnects, compelling vendors to embed advanced image‑processing algorithms that meet the stricter compliance criteria.

Recent disruptions have motivated manufacturers to source X‑ray modules from multiple Asian suppliers, reducing lead times and insulating production schedules from geopolitical shocks.

Growth in wearables and IoT devices is widening the inspection footprint, as even low‑cost electronics now require reliable non‑destructive testing to assure reliability in harsh environments.

North America

North America remains a mature market where legacy equipment providers retain strong relationships with aerospace and defense contractors. Yet, the sector is undergoing a subtle shift as newer entrants, backed by venture capital, introduce AI‑enhanced X‑ray platforms that promise faster defect classification. This technology infusion forces incumbents to reconsider pricing structures and service contracts. Meanwhile, trade policies encouraging domestic production of advanced semiconductors are re‑energising local fabs, which are beginning to source inspection systems internally rather than relying on long‑standing overseas vendors. The strategic implication for players is clear: integration of predictive maintenance analytics will become a decisive differentiator in a market where cost‑plus‑service models are losing relevance.

Europe

European manufacturers are navigating a landscape shaped by stringent environmental directives and a strong commitment to circular economy principles. These factors translate into a preference for inspection equipment that minimises energy consumption while delivering high‑resolution imaging. In addition, the region’s fragmented industrial basespanning Germany’s automotive hubs to the electronics clusters in the Beneluxcreates varied specifications for X‑ray systems, compelling vendors to develop modular product families. The emerging focus on collaborative inspection stations, where multiple stakeholders can jointly analyse data, suggests that future business models will lean heavily on subscription‑based analytics services.

South America

South America’s electronics assembly sector is still consolidating, but recent public‑private partnerships aimed at boosting local component manufacturing are generating modest demand for inspection technologies. Operators are keen on solutions that can be deployed rapidly and require limited on‑site expertise, given the relative scarcity of specialised technicians. As a result, turnkey X‑ray inspection kits with remote diagnostics are gaining traction. Companies that can pair hardware with robust training programs stand to capture market share as the region gradually shifts from import‑reliant to more self‑sufficient production models.

Middle East & Africa

The Middle East & Africa region is witnessing early‑stage adoption of X‑ray inspection equipment, driven largely by aerospace maintenance, repair and overhaul (MRO) activities in the Gulf and emerging consumer electronics assembly in North Africa. Investment cycles are cautious, with buyers prioritising equipment that offers scalability and low total cost of ownership. Partnerships with European distributors are common, providing a conduit for technology transfer and after‑sales support. For market entrants, establishing local service hubs will be essential to overcome perceived reliability concerns and to nurture long‑term relationships in a market that values on‑ground presence.

Report Scope

This market research report provides a comprehensive analysis of the Electronics Industry X-ray Inspection Equipment Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Electronics Industry X-ray Inspection Equipment Market?

-> Electronics Industry X-ray Inspection Equipment Market was valued at USD 397 million in 2025 and is expected to reach USD 776 million by 2032, growing at a CAGR of 9.2% during the forecast period.

Which key companies operate in Electronics Industry X-ray Inspection Equipment Market?

-> Key players include ViTrox, Viscom, Nordson, Omron, Unicomp Technology, NIKON, Waygate Technologies (Baker Hughes), Comet Yxlon, Test Research Inc. (TRI), Seamark ZM, Zhengye Technology, ZEISS, Saki Corporation, XAVIS Co., Ltd., SEC, Techvalley, Goepel Electronic, Scienscope, SXRAY, Creative Electron, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for high‑density interconnects, advanced packaging formats (BGA, CSP, Flip‑Chip, QFN), increasing cost of hidden defects, AI‑driven server workloads driving higher PCB layer counts, and government programmes accelerating digital transformation and in‑line inspection adoption.

Which region dominates the market?

-> Asia‑Pacific dominates the market, benefitting from a large electronics manufacturing base, strong semiconductor packaging activity, and significant investments in advanced inspection technologies.

What are the emerging trends?

-> Emerging trends include AI‑assisted automated defect recognition, increased adoption of 2.5D/3D CT for quantitative defect analysis, modular platform plus application‑engineering delivery models, and tighter closed‑loop traceability integrated with SPC and quality management systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...