DC Probe Station Market Insights

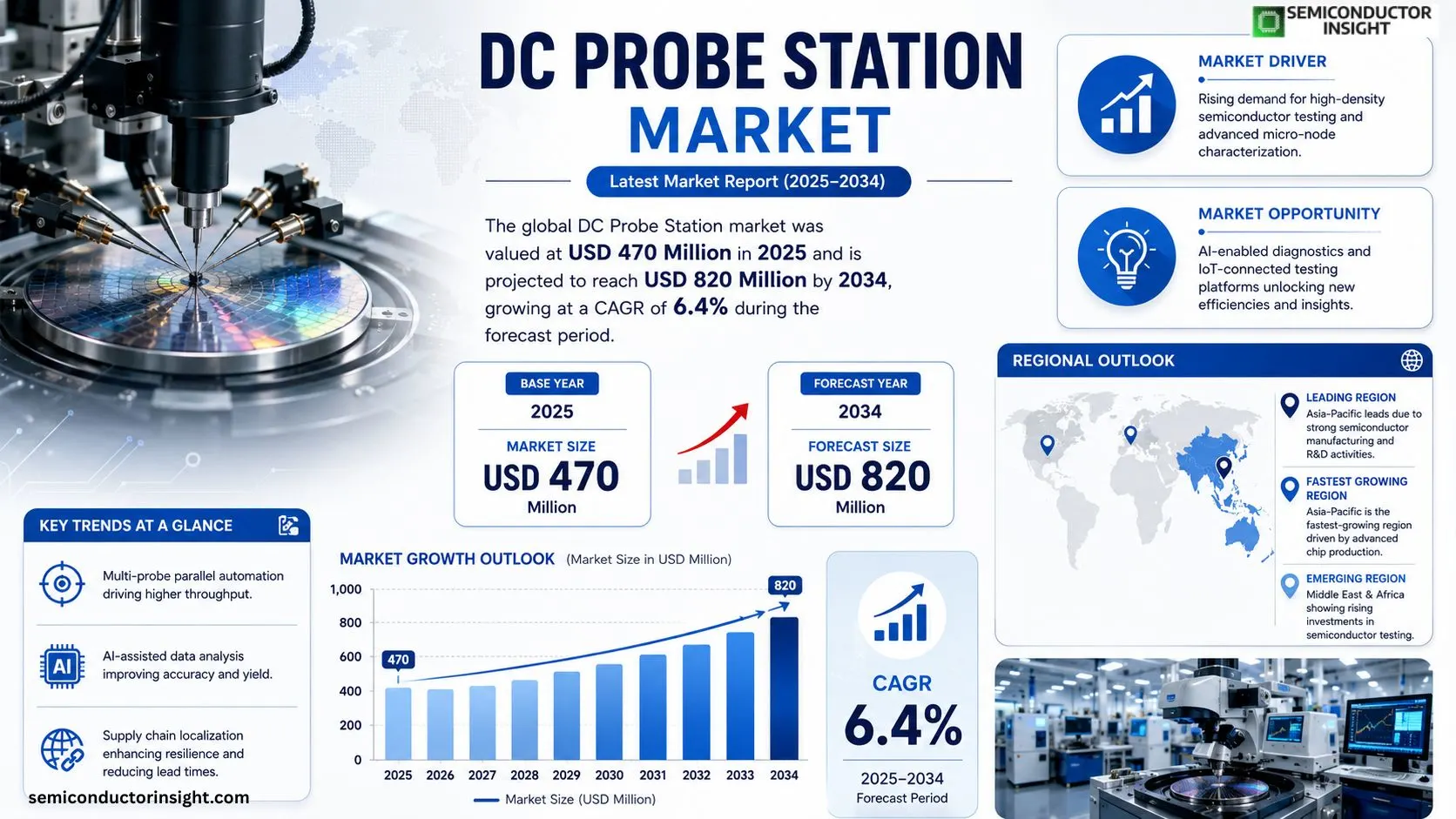

DC Probe Station market was valued at USD 470 million in 2025. It is forecasted to rise to USD 820 million by 2034, reflecting a compound annual growth rate of 6.4% over the period.

DC probe stations are precision testing platforms used for electrical characterization of semiconductor devices and wafers. They deliver accurate contact, biasing and measurement capabilities within controlled environments, enabling analysis of DC electrical properties such as current‑voltage (I‑V) curves and leakage behavior.The expansion stems from increasingly complex semiconductor architectures that require finer electrical diagnostics; manufacturers are therefore investing in high‑precision stages, automated multi‑probe heads and enhanced thermal stability features. Recent collaborations among leading suppliers aim to integrate AI‑assisted data processing with parallel probing solutions, addressing throughput demands while maintaining measurement reliability.

MARKET DRIVERS

Escalating demand for high‑density semiconductor testing

DC Probe Station Market benefits from manufacturers accelerating the rollout of advanced micro‑nodes. As chip geometries shrink, fault detection must occur at lower voltages and tighter tolerances, compelling test facilities to adopt precision probe stations that can sustain repeatable measurements on delicate dies.

Innovation in probe tip materials and automation

Recent breakthroughs in conductive alloys and MEMS‑based actuation have lowered contact resistance and reduced cycle times. Automation platforms now integrate vision‑guided alignment, enabling operators to achieve sub‑micron positioning without manual intervention, which translates into higher throughput for high‑mix production lines.

➤ Operators who pair AI‑assisted image recognition with next‑generation probe assemblies report a 12% reduction in test‑failure rates within six months.

These technical refinements are reshaping procurement strategies; OEMs are reallocating budget from legacy test rigs to modular stations that can be reconfigured for emerging device architectures, thereby extending asset lifecycles.

MARKET CHALLENGES

High upfront capital investment

Acquiring a fully featured DC probe station often requires a multi‑million‑dollar outlay, especially when configured for ultra‑low‑noise environments. Mid‑size firms face cash‑flow constraints that can delay adoption, forcing them to rely on shared facilities or older equipment with lower performance envelopes.

Other Challenges

Maintenance complexity

The precision mechanics and custom cabling demand specialized service contracts. Downtime for calibration or component replacement can erode the expected productivity gains, prompting some users to question the total cost of ownership.

MARKET RESTRAINTS

Scarcity of qualified technicians

The nuanced nature of DC measurements requires operators with deep knowledge of signal integrity and probe handling. Labor markets in key semiconductor hubs report a shortage of engineers who can both configure the stations and interpret the nuanced data outputs, limiting the speed of rollout.In addition, regulatory compliance for electromagnetic emissions imposes design constraints that some manufacturers find costly to meet, especially when retrofitting older facilities.

MARKET OPPORTUNITIES

Convergence with AI‑enabled diagnostics

Embedding machine‑learning algorithms within the measurement workflow allows real‑time anomaly detection and predictive maintenance. Vendors that bundle AI analytics with their probe stations can differentiate themselves, offering customers actionable insights that reduce scrap and accelerate yield improvement cycles.The expanding ecosystem of IoT‑connected testing rigs also opens subscription‑based service models. Clients can access software updates, remote troubleshooting, and performance dashboards on a recurring basis, turning a traditionally capital‑intensive purchase into a more flexible operational expense.

DC Probe Station Market Trends

Precision Requirements Accelerate Equipment Evolution

The relentless push toward sub‑10 nm features and three‑dimensional architectures is compelling semiconductor fabs to tighten tolerances on electrical measurements. Modern probe stations must deliver sub‑microamp resolution while preserving thermal stability across wafer sizes that range from 150 mm to 300 mm. This pressure translates into higher demand for ultra‑stable precision stages and multi‑probe automation that can keep pace with shortened test windows. For equipment vendors, the shift creates a premium pricing environment for modules that integrate real‑time drift compensation and AI‑assisted probe alignment, fostering a move away from legacy manual platforms toward fully automated solutions.

Other Trends

Supply‑Chain Localization Gains Traction

Recent disruptions in global logistics have prompted major manufacturers to re‑evaluate the geographic distribution of critical components such as micromanipulators, vacuum chucks and high‑precision power supplies. By sourcing more parts from domestic suppliers in Japan, the United States and China, companies reduce lead times and improve control over quality benchmarks that directly affect measurement repeatability. The strategic pivot not only cushions against future shortages but also adds a competitive edge for customers who value rapid equipment turn‑around for high‑volume production cycles.

Automation and Parallel Testing Expand Throughput

As wafer‑level testing becomes a bottleneck in advanced logic and power device lines, manufacturers are embedding parallel‑probe architectures into their stations. The ability to acquire simultaneous I‑V curves from multiple die sites shortens overall test time and raises throughput without sacrificing accuracy. This trend encourages fab operators to invest in platforms that combine high‑speed data acquisition with integrated analytics, enabling quicker decision‑making on yield and process adjustments. The ripple effect is a stronger emphasis on software ecosystems that can handle large data volumes while maintaining traceability, which in turn opens new revenue streams for vendors through subscription‑based analysis tools.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive Landscape of DC Probe Station Market

FormFactor, Inc. dominates the high‑end segment, leveraging a vertically integrated supply chain that couples precision stage engineering with proprietary automation software. This integration yields profit margins near the top of the industry range and enables the company to command premium pricing for fully automatic platforms aimed at 7‑nm and beyond wafer nodes. MPI Corporation follows closely, differentiating through a strong foothold in the Japanese market and a diversified portfolio that spans manual, semi‑automatic, and fully automatic stations. Both firms benefit from long‑term relationships with leading fabs, which translate into recurring service contracts and upgrade pathways. The market structure therefore reflects a dual‑track hierarchy: a handful of global OEMs that capture the bulk of revenue and a broader set of regional system integrators that address cost‑sensitive segments, particularly in emerging semiconductor clusters across Southeast Asia.Beyond the two giants, a constellation of niche players injects agility into the ecosystem. Micromanipulator and Instec Inc. specialize in custom micromanipulation solutions that appeal to research laboratories requiring sub‑micron repeatability. Ossila Probe Stations and EVERBING INT’L International have carved out a presence in university and prototype environments by offering modular, cost‑effective kits. Chinese manufacturers such as Shenzhen Sendonbao Technology and Silan Microelectronics Co., Ltd. are expanding rapidly, capitalizing on domestic fab growth and offering competitive pricing for ambient and vacuum‑based stations. EasyTest Technology and several Europe‑based integrators complete the landscape, providing application‑specific adaptations for power‑device testing and compound‑semiconductor characterization. Collectively, these firms sustain a vibrant competitive dynamic, forcing incumbents to accelerate innovation cycles while preserving margins through service‑oriented business models.

List of Key DC Probe Station Companies Profiled

- FormFactor, Inc.

- MPI Corporation

- Micromanipulator

- Instec Inc.

- Ossila Probe Stations

- EVERBING INT’L International

- Silan Microelectronics Co., Ltd.

- Shenzhen Sendonbao Technology Co., Ltd.

- EasyTest Technology Co., Ltd.

- Tektronix (DC Probe Station division)

- Microworld Ltd.

- Advantest Corporation

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Fully Automatic DC Probe Station is emerging as the leading segment because it aligns with the industry’s push toward higher throughput and tighter measurement tolerance.

|

| By Application |

|

Semiconductor Wafer Fab dominates this dimension as fabs require consistent, high‑precision electrical characterization across multiple process nodes.

|

| By End User |

|

Semiconductor Manufacturers are the primary end‑users, driven by the need for reliable, repeatable measurements at scale.

|

| By Test Environment |

|

Shielded DC Probe Station is gaining prominence because it isolates electromagnetic interference, which is critical for low‑current leakage measurements.

|

| By Technology Trend |

|

Multi‑probe Parallel Automation is emerging as the most impactful trend, driven by the need for higher throughput without sacrificing precision.

|

Regional Analysis: DC Probe Station Market

North America

Vendors are introducing probe heads with sub‑micron tip radii, enabling finer feature probing on emerging logic nodes. The emphasis on automated tip‑exchange mechanisms reflects a shift toward higher throughput in research labs that must keep pace with rapid design cycles.

To mitigate component shortages, manufacturers are diversifying sources for precision motion stages and high‑frequency cabling, a strategy that cushions the market against geopolitical fluctuations while preserving product reliability.

Early‑stage startups in quantum computing are allocating a larger share of capital to versatile probe stations, seeking equipment that can transition from wafer‑level testing to device‑level characterization without extensive retooling.

Emerging safety standards for high‑voltage probing are prompting manufacturers to embed additional isolation features, a move that reassures end‑users operating in aerospace and medical device sectors.

Europe

European semiconductor clusters in Germany, the Netherlands, and France are capitalising on robust public‑private partnerships that fund joint test‑equipment initiatives. The region’s emphasis on sustainability drives demand for energy‑efficient probe stations, prompting OEMs to highlight low‑power motor designs. Additionally, strict electromagnetic compatibility directives are influencing product specifications, nudging suppliers toward tighter shielding solutions. Customers in automotive electronics value modular platforms that can integrate seamlessly with existing test lines, a preference that fuels a modest but steady upgrade cycle across mid‑size firms.

Asia‑Pacific

The Asia‑Pacific landscape is distinguished by rapid scale‑up in contract manufacturing hubs, especially in Taiwan, South Korea, and China. These fabs require high‑volume probe stations that can tolerate continuous operation, leading vendors to stress durability and automated maintenance alerts. Local tech parks are fostering collaborations between equipment makers and chip designers, accelerating the diffusion of customized probe solutions for emerging memory technologies. Although cost sensitivity remains high, buyers are willing to invest in features that reduce downtime, such as predictive wear‑monitoring for probe tips.

South America

In South America, market activity revolves around a handful of research institutions and niche electronics firms focused on renewable‑energy applications. Limited local manufacturing capacity compels importers to prioritize versatile stations that support both legacy and cutting‑edge devices. Partnerships with North American distributors are common, enabling access to after‑sales service networks that mitigate concerns over spare‑part lead times. The region’s slower adoption pace is offset by growing interest in training programs that build local expertise in DC probing techniques.

Middle East & Africa

The Middle East & Africa segment is anchored by defense and aerospace projects that demand high‑precision testing capabilities. Investment in localized test labs is accelerating, driven by governmental initiatives to diversify economies away from hydrocarbons. Stakeholders are looking for probe stations that can integrate with existing radar and satellite testing infrastructures, emphasizing ruggedness and environmental tolerance. While overall market size remains modest, the strategic importance of reliable measurement equipment is prompting multinational vendors to establish dedicated support channels in the region.

Report Scope

This market research report provides a comprehensive analysis of the DC Probe Station Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of DC Probe Station Market?

-> DC Probe Station Market was valued at USD 466 million in 2025 and is expected to reach USD 710 million by 2032 with a CAGR of 6.3% during the forecast period.

Which key companies operate in DC Probe Station Market?

-> Key players include FormFactor, Inc.; MPI Corporation; Micromanipulator; Instec Inc.; Ossila Probe Stations; EVERBING INT’L International; Silan Microelectronics Co., Ltd.; Shenzhen Sendonbao Technology Co., Ltd.; EasyTest Technology Co., Ltd..

What are the key growth drivers?

-> Key growth drivers include the expansion of advanced logic, memory, power and compound semiconductor devices; the need for precise electrical characterization; investments in high‑precision stages, automated probing, thermal stability and integrated software; and supply‑chain localization together with multi‑probe parallel testing.

Which region dominates the market?

-> Asia dominates the market, driven by strong manufacturing and R&D activities in Japan, China and South Korea.

What are the emerging trends?

-> Emerging trends include localization of the supply chain, adoption of multi‑probe platforms for parallel testing, and integration of AI‑driven analytics with automated probing systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...