Micro Electronics Evaporation Sources Market Insights

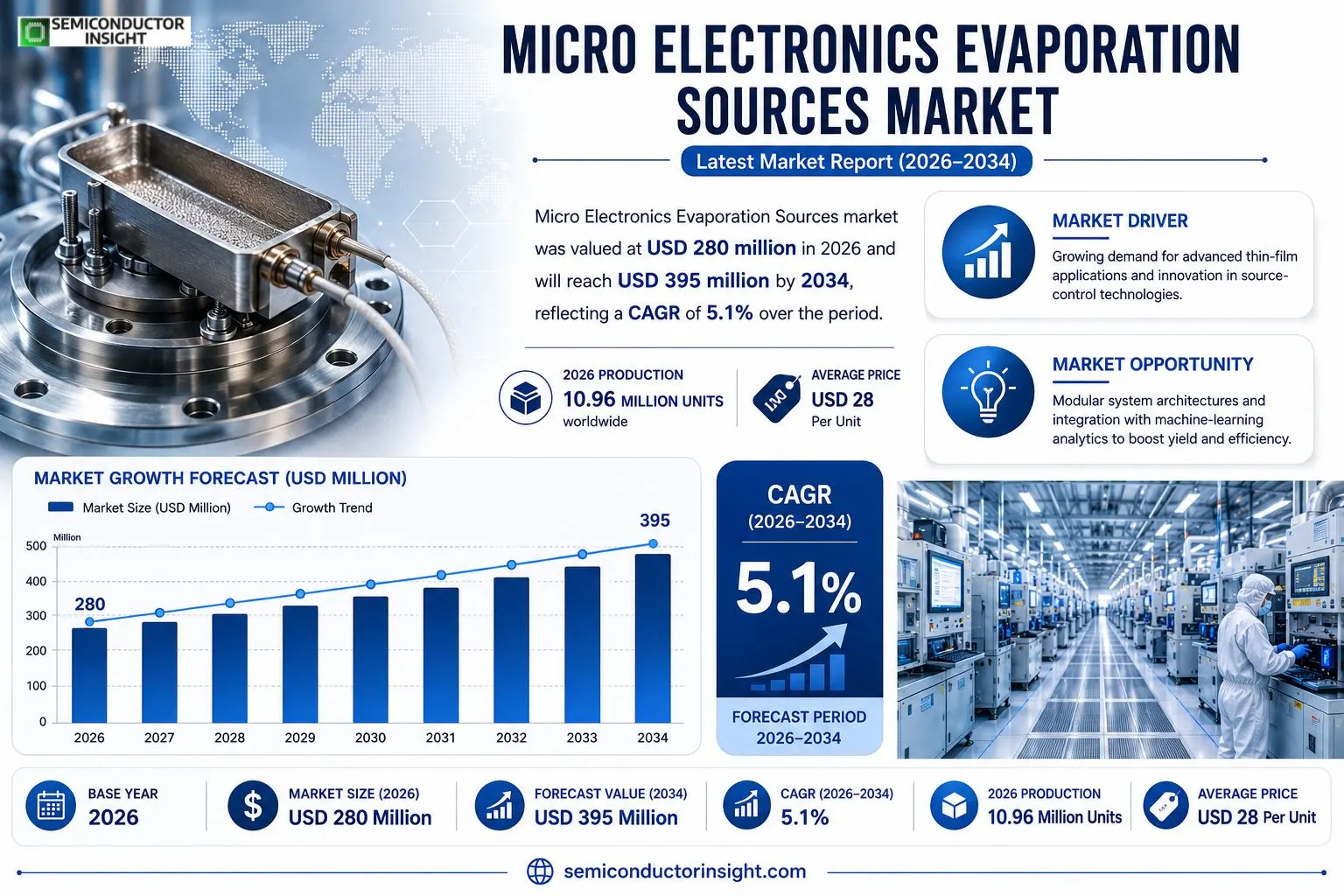

Micro Electronics Evaporation Sources market was valued at USD 280 million in 2026 and will reach USD 395 million by 2034, reflecting a CAGR of 5.1 % over the period

Micro Electronics Evaporation Sources are precision deposition tools that vaporise high‑purity materialssuch as tungsten, molybdenum or tantalumand condense them onto substrates as ultra‑thin films. Their tight control of evaporation rate and film uniformity enables critical components for semiconductors, optics, solar cells and medical equipment. In 2026 worldwide production amounted to roughly 10.96 million units at an average price of USD 28 per unit, underscoring their role as essential enablers of next‑generation micro‑fabrication technologies.

MARKET DRIVERS

Growing Demand for Advanced Thin‑Film Applications

The rise of flexible displays, wearable sensors and next‑generation photovoltaics is pushing manufacturers to seek deposition tools that can deliver uniform films at sub‑micron thicknesses. Micro Electronics Evaporation Sources Market participants that can guarantee repeatable layer quality are becoming preferred suppliers because product performance now hinges on film uniformity as much as on material composition.

Innovation in Source‑Control Technologies

Recent breakthroughs in real‑time flux monitoring and closed‑loop temperature regulation are reducing scrap rates and shortening cycle times. Companies that integrate these controls into evaporation modules are able to offer higher throughput without sacrificing precision, a combination that directly improves customers’ bottom lines.

➤ “Customers now prioritize systems that combine rapid ramp‑up with sub‑nanometer stability; the ability to meet both criteria defines market leadership.”

These technology shifts are also encouraging OEMs to redesign product road‑maps toward thinner, lighter, and more energy‑efficient devices. The resulting design pressure fuels a virtuous cycle: higher specification demands drive source upgrades, which in turn expand the addressable market for specialized evaporation equipment.

MARKET CHALLENGES

Process Complexity and Yield Variability

Achieving the required film characteristics often involves tightly controlled vacuum environments and precise material handling. Small deviations in chamber pressure or crucible purity can lead to thickness non‑uniformity, forcing manufacturers to rework or discard batches, thereby inflating production costs.

Other Challenges

Cost Pressures

The capital expense of high‑precision evaporation units remains a barrier for emerging manufacturers. When coupled with the need for skilled technicians to operate and maintain the equipment, total cost of ownership can outweigh short‑term performance gains, especially for low‑volume producers.Supply‑chain volatility for high‑purity source materials further compounds the issue. Fluctuating raw‑material prices force end‑users to reassess procurement strategies, often leading to longer lead times and reduced flexibility in scaling production volumes.Regulatory scrutiny around emissions from evaporation processes adds another layer of complexity. Companies must invest in filtration and monitoring solutions to meet increasingly strict environmental standards, which can erode profit margins if not managed efficiently.

MARKET RESTRAINTS

High Initial Investment Requirements

The upfront cost for ultra‑high‑vacuum chambers, precision temperature controllers, and advanced metrology tools often exceeds the budget thresholds of small‑to‑mid‑size producers. This capital intensity discourages entry and limits market expansion to firms with deep pockets.The need for ongoing calibration and preventive maintenance adds operating expense that many organizations view as a long‑term financial commitment. When depreciation schedules are aligned with product lifecycles, the financial payoff period can extend beyond typical planning horizons.Furthermore, the niche expertise required to troubleshoot deposition anomalies creates a talent bottleneck. Companies unable to attract or retain qualified engineers face longer downtimes, which directly hampers throughput and profitability.

MARKET OPPORTUNITIES

Modular System Architectures

Designing evaporation sources as interchangeable modules enables manufacturers to upgrade specific componentssuch as crucibles or power supplieswithout replacing the entire system. This approach reduces capital outlay and extends equipment lifespan, making the technology more attractive to cost‑conscious firms.

Integration with Machine‑Learning Analytics

Embedding AI‑driven process optimization tools can predict drift in deposition rates and suggest real‑time adjustments. Early adopters of such analytics report up to a 15% improvement in yield, positioning data‑centric solutions as a compelling differentiator.Geographic expansion into fast‑growing semiconductor hubs in Southeast Asia presents a sizable upside. Local manufacturers are seeking turnkey evaporation platforms that align with regional quality standards, creating a clear pathway for market entrants to capture share through tailored service packages.

Micro Electronics Evaporation Sources Market Trends

High‑Generation AMOLED Linearity Gains Momentum

The push for finer patterning in advanced semiconductor fabs and the scaling of OLED panel sizes are forcing equipment makers to tighten thickness tolerances to within one percent. Manufacturers are therefore redesigning linear evaporation heads to deliver steadier flux while curbing material waste. This shift reshapes supplier negotiations: buyers now prioritize source stability and in‑process monitoring over raw cost, while vendors that can certify sub‑micron uniformity secure longer contract cycles. For end‑users, the payoff appears as higher yield on 8.6‑generation AMOLED lines and a reduction in re‑work penalties, translating into measurable profitability gains across the supply chain.

Other Trends

Localization of Evaporation Source Production

Geopolitical uncertainty and recent disruptions in trans‑Pacific logistics have motivated major OEMs to source critical components closer to their fabs. Domestic fabs in East Asia are establishing dedicated lines for evaporation sources, leveraging existing semiconductor material expertise to cut lead times. This trend creates a dual‑track market: established multinationals retain niche high‑precision segments, while emerging regional players capture volume‑driven orders by offering competitive pricing and faster delivery. Companies that can bundle source hardware with localized service packages are positioning themselves as indispensable partners for next‑generation display manufacturers.

Environmental Efficiency and Intelligent Upgrades

Regulatory pressure on energy consumption combined with corporate sustainability mandates is prompting a redesign of evaporation chambers. Modern control algorithms now modulate valve timing in real time, shaving kilowatts per hour without compromising deposition rate. Concurrently, manufacturers are integrating diagnostic sensors that predict wear before failure, extending equipment life cycles and reducing scrap. These advances unlock new business models such as pay‑per‑performance leasing, where equipment cost is amortized against verified efficiency metrics. Customers adopting these greener solutions report lower operating expenses and a stronger ESG profile, strengthening their market positioning.

COMPETITIVE LANDSCAPE

Key Industry Players

Micro Electronics Evaporation Sources – Competitive Overview

The market is dominated by a handful of firms that command the bulk of high‑volume production for semiconductor and advanced display customers. Kurt J. Lesker leverages a legacy of ultra‑high‑vacuum expertise to supply linear evaporation sources that meet the sub‑percent thickness uniformity demanded by 8.6‑generation AMOLED lines. ULVAC, with its extensive service network, differentiates through integrated pump‑valve‑control suites that reduce downtime on 110 k‑unit lines, a factor that translates into the sector’s roughly 25 % gross margin benchmark. MKS Instruments rounds out the core triad by offering modular systems geared toward research‑driven optics and solar‑cell producers, allowing rapid re‑configuration of deposition rates. Together, these three players shape pricing dynamics, dictate technology road‑maps, and exert considerable influence over the upstream component supply chain, especially for evaporation‑material feedstock and precision metrology equipment.Beyond the top tier, a diverse set of specialists addresses niche requirements and regional demand spikes. RD Mathis and Neyco focus on custom‑shaped boat and basket sources that serve low‑volume, high‑precision optics labs in Europe. MetalsTek supplies high‑purity refractory‑metal evaporation modules critical for emerging thin‑film solar technologies in the United States. Angstrom’s strength lies in portable, mask‑less deposition units that enable printed‑OLED pilots in Southeast Asia. Demaco Vacuum, Shandong Pengcheng Advanced Ceramics, and Suzhou Keyue Materials each provide domestically sourced ceramic crucibles and valve assemblies that appeal to cost‑sensitive Asian manufacturers seeking supply‑chain resilience. Veeco Instruments and PVD Products round out the ecosystem with advanced process‑control software and hybrid source designs that bridge the gap between traditional evaporation and sputtering techniques. This layered supplier base injects competitive pressure, fosters incremental innovation, and cushions the market against single‑source disruptions.

List of Key Micro Electronics Evaporation Sources Companies Profiled

- Kurt J. Lesker

- ULVAC

- MKS Instruments

- RD Mathis

- Neyco

- MetalsTek

- Angstrom

- Demaco Vacuum

- Shandong Pengcheng Advanced Ceramics

- Suzhou Keyue Materials

- Veeco Instruments

- PVD Products

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Boat Type

|

| By Application |

|

Semiconductor

|

| By End User |

|

Chip Manufacturers

|

| By Material |

|

Tungsten Evaporation Source

|

| By Size |

|

Large Size

|

Regional Analysis: Micro Electronics Evaporation Sources Market

German and French fabs host a disproportionate share of high‑volume deposition lines, giving local source providers privileged access to feedback loops that accelerate product refinement. This proximity shortens the engineering turnaround that competitors in other continents must endure.

Stringent EU directives on hazardous emissions compel manufacturers to adopt evaporation sources with tighter material containment, prompting vendors to embed advanced monitoring features as a de‑facto requirement.

Recent geopolitical strains have encouraged European buyers to diversify component sourcing, favoring local suppliers that can guarantee on‑time delivery of crucibles, filaments and calibration services.

Research clusters in the Benelux region and Scandinavia foster rapid prototyping of novel source architectures, allowing early adopters to trial higher‑throughput configurations before broader market rollout.

North America

In North America, the fragmentation of the semiconductor ecosystem yields a competitive marketplace where multiple equipment manufacturers vie for niche contracts. The United States’ emphasis on defense‑related micro‑electronics drives a parallel demand for highly reliable evaporation sources that can meet exacting qualification standards. Simultaneously, the prevailing venture‑capital climate fuels start‑ups that experiment with hybrid deposition techniques, creating a feedback loop that pressures incumbent suppliers to broaden their service portfolios. The result is a market where agility, technical support depth, and the ability to integrate with diverse fab automation stacks determine success.

Asia‑Pacific

Asia‑Pacific’s rapid scaling of display and IoT production lines translates into a steady appetite for cost‑effective evaporation solutions. Countries such as South Korea, Taiwan and Singapore house vertically integrated players that prefer end‑to‑end control over source procurement, reducing reliance on external distributors. Nevertheless, the region grapples with variable environmental standards, prompting manufacturers to tailor source designs to local compliance regimes. The competitive pressure forces vendors to optimise tooling for both throughput and material efficiency, a balance that directly influences profitability for fab operators.

South America

South American fabs remain comparatively modest in volume, yet they prioritize flexibility because they serve a mix of automotive, medical and consumer‑electronics customers. Operators often select evaporation sources that can be re‑configured for multiple material families, reducing capital outlay. Local policy incentives aimed at boosting high‑tech manufacturing have sparked modest upgrades of legacy equipment, creating opportunities for suppliers that can offer retrofit kits and on‑site training. The prevailing market sentiment values long‑term service agreements that hedge against limited local technical talent.

Middle East & Africa

The Middle East & Africa region is characterized by nascent semiconductor initiatives paired with strong governmental pushes toward technology diversification. Investment funds are channelled into establishing pilot lines that require turnkey evaporation source packages, favoring vendors capable of delivering comprehensive installation and qualification services. At the same time, logistical constraints across vast distances underline the importance of robust after‑sales logistics networks. Companies that can demonstrate a resilient spares‑distribution model are better positioned to capture the emerging demand in this geography.

Report Scope

This market research report provides a comprehensive analysis of the Micro Electronics Evaporation Sources Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Micro Electronics Evaporation Sources Market?

-> Micro Electronics Evaporation Sources Market was valued at USD 280 million in 2026 and is expected to reach USD 395 million by 2034, growing at a CAGR of 5.1% during the forecast period.

Which key companies operate in Micro Electronics Evaporation Sources Market?

-> Key players include Kurt J. Lesker, RD Mathis, Neyco, MetalsTek, Angstrom, Demaco Vacuum, Shandong Pengcheng Advanced Ceramics, Suzhou Keyue Materials, among others.

What are the key growth drivers?

-> Key growth drivers include advancements in semiconductor manufacturing processes, expansion of OLED display panel capacities, stringent requirements for thin‑film uniformity, higher deposition rates, and improved material utilization.

Which region dominates the market?

-> Asia-Pacific leads the market, driven by the concentration of semiconductor fabs, optics manufacturers, and solar cell production facilities.

What are the emerging trends?

-> Emerging trends include technological innovation with intelligent upgrades, focus on energy‑efficient and environmentally friendly evaporation sources, localization of high‑generation AMOLED equipment, and diversification into printed OLED and maskless (ViP) technologies.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...