Semiconductor Slurry Filters Market Insights

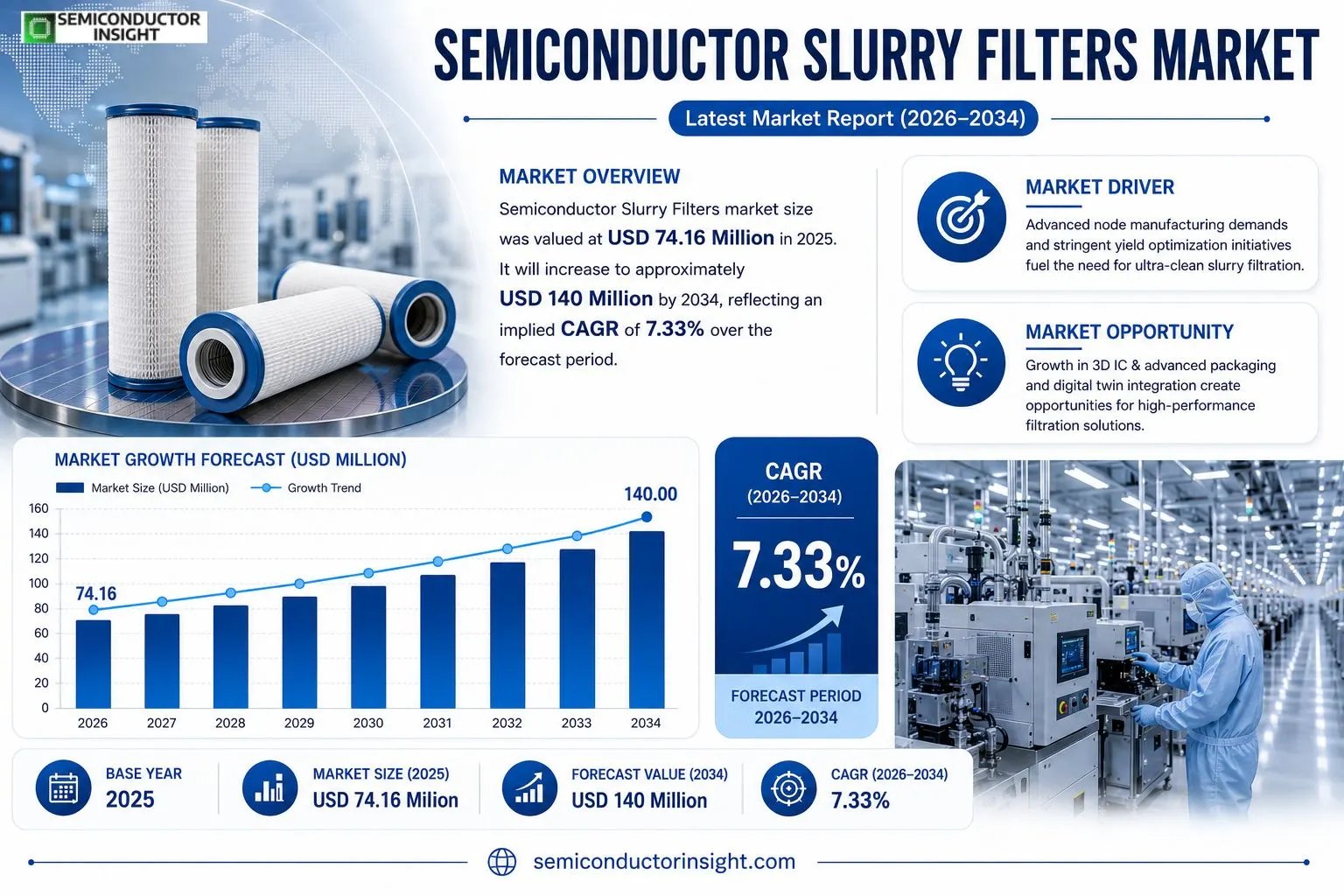

Semiconductor Slurry Filters market size was valued at USD 74.16 million in 2025. It will increase from USD 74.16 million in 2025 to roughly USD 140 million by 2034, reflecting an implied CAGR of about 7.33% over the nine‑year horizon.

Semiconductor slurry filters are high‑cleanliness liquid filtration elements used throughout wafer fabrication where polishing slurries are present. By controlling particle‑size distribution and limiting large‑particle counts, these filters help stabilize slurry chemistry, lower defect density and improve overall yield.Growth stems from tighter defect tolerances in advanced nodes, increasingly complex slurry chemistries and the need for reliable chemical delivery management across fab lines. Multi‑stage filtration configurations raise unit usage per production line, while barriers such as clean‑room manufacturing capability and qualification consistency limit new entrants, creating steady pricing rather than aggressive discounting.

MARKET DRIVERS

Advanced Node Manufacturing Demands

The push toward sub‑10 nm process nodes has forced wafer fabs to seek tighter particle control. Semiconductor Slurry Filters Market suppliers that can deliver sub‑micron filtration efficiency are witnessing stronger customer interest because yield loss from contaminant‑induced defects becomes increasingly costly at smaller geometries.

Stringent Yield Optimization Initiatives

Foundries are allocating larger portions of their CAPEX budgets to inline filtration systems that reduce slurry‑borne particulates before polishing. This trend translates into recurring revenue streams for filter manufacturers, as maintenance contracts and filter‑replacement programs become standard practice.

➤ “Every 0.1 µm reduction in particle size can lift overall yield by up to 2 % on high‑volume production lines,” a senior process engineer noted.

Consequently, vendors that combine high‑temperature resilience with low‑pressure drop designs are positioning themselves as essential partners in the fab’s quality‑control ecosystem, driving incremental adoption across multiple commodity and specialty semiconductor categories.

MARKET CHALLENGES

Cost Sensitivity of High‑Volume Production

While performance gains are clear, the price differential between conventional and premium filtration media remains a barrier for cost‑conscious fabs. Decision‑makers often weigh the immediate expense against projected yield improvements, leading to slower upgrade cycles for filter technology.

Other Challenges

Supply‑Chain Volatility

logistics disruptions and raw‑material availability fluctuations have introduced lead‑time uncertainties for filter components, compelling manufacturers to hold higher inventory levels and eroding margins.Furthermore, the need to certify new filter designs against each fab’s stringent qualification protocols adds another layer of time and expense, discouraging rapid adoption of innovative solutions.

MARKET RESTRAINTS

Regulatory and Environmental Compliance

Stringent environmental regulations governing waste disposal and chemical usage limit the types of slurry formulations that can be paired with certain filter media. Manufacturers must invest in R&D to develop compliant products, a cost that can be passed on to end users.

Technological Replacement Cycle

Rapid evolution of wafer‑processing equipment shortens the effective lifespan of existing filter solutions. Companies that cannot keep pace with new process chemistries risk losing relevance, thereby restraining market expansion.

MARKET OPPORTUNITIES

Emergence of 3D IC and Advanced Packaging

The rise of three‑dimensional integrated circuits and heterogeneous packaging introduces novel slurry chemistries that demand bespoke filtration characteristics. Suppliers that tailor pore‑size distribution and chemical resistance for these applications can capture a growing niche within Semiconductor Slurry Filters Market.

Digital Twin Integration

Adopting digital‑twin models to simulate slurry flow and particle capture enables manufacturers to offer performance‑guaranteed filters, reducing trial‑and‑error cycles for fabs and unlocking premium pricing opportunities.

Semiconductor Slurry Filters Market Trends

Yield Sensitivity and Advanced Node Demands

In 2025 Semiconductor Slurry Filters Market generated US$ 74.16 million from the sale of roughly 1.83 million units, each averaging $44.3. The price‑performance balance of these filters directly influences defect density on wafers, especially as manufacturers shift to sub‑10 nm nodes where a single particle can jeopardize entire lots. Consequently, tighter control of slurry particle size and Large Particle Counts (LPCs) has become a decisive factor for fab profitability. The market’s trajectory toward US$ 122 million by 2032 reflects how incremental yield improvementsoften measured in fractions of a percenttranslate into multi‑million‑dollar revenue gains for chipmakers, prompting them to treat slurry filtration as a core consumable rather than a peripheral cost.

Other Trends

Manufacturing Complexity and Supply Constraints

High‑cleanliness assembly, media qualification, and batch‑to‑batch consistency erect substantial entry barriers for new suppliers. Cost structure analysis shows that filtration media and auxiliary membranes consume 35‑45 % of production expense, while cleanroom testing and packaging account for another 20 % combined. Because the process tolerates little deviation, manufacturers favour established players capable of guaranteeing the 0.5‑1 µm retention rating required for both cartridge‑type and capsule‑type designs. This dynamic curtails price competition and reinforces a modest gross margin band of 30‑40 %, with premium margins reserved for filters that pass stringent qualification for tool‑inlet and loop applications.

Regional Concentration and Role of Asia‑Pacific

Asia‑Pacific supplies roughly 60‑70 % of Semiconductor Slurry Filters Market output, mirroring the region’s dominance in wafer‑fab capacity and its drive toward localized material sourcing. The concentration of both demand and production creates a feedback loop: fabs in China, Korea, and Taiwan require rapid delivery and low‑lead‑time inventory, which incentivizes regional manufacturers to scale single‑line capacities to 150,000‑300,000 units annually. Meanwhile, North America and Europe retain niche premium segments, focusing on high‑end applications that demand extended filter lifetimes and superior chemical compatibility. This geographic split shapes investment patterns, with capital allocated toward automation in Asia‑Pacific and toward advanced qualification services in Western markets.

COMPETITIVE LANDSCAPE

Key Industry Players

Semiconductor Slurry Filters Competitive Overview

Entegris, Pall and 3M dominate the high‑cleanliness segment, each commanding a sizable share of the filter supply chain. Their strength lies in vertically integrated production facilities that couple advanced polymer resin sourcing with rigorous qualification programs required by leading foundries. By leveraging economies of scale in cleanroom assembly and offering extensive service networks across Asia‑Pacific, North America and Europe, they set pricing benchmarks that smaller outfits must accommodate. The market’s structure therefore resembles a tiered hierarchy: a few multinational manufacturers supply cartridge‑type and capsule‑type filters for premium nodes, while a broader base of regional firms fills niche demand for legacy processes and volume‑driven fabs.Beyond the dominant trio, a constellation of specialized firms adds depth to the ecosystem. TAK Microfilter Inc. and Kan I International focus on ultra‑low retention ratings for 0.5 µm‑1 µm applications, often collaborating directly with equipment OEMs. Taiwan Grace International, JENG KANG International and Cobetter supply cost‑effective capsule filters to mid‑tier fabs in Southeast Asia. Membrane Solutions and Feature‑Tec carve out positions in custom‑membrane engineering, whereas Hangzhou Deefine, Hangzhou Darlly Filtration Equipment Co.,Ltd, Ever Pure Applied Materials Co., Ltd and other Chinese players capitalize on localized production to meet the region’s 60‑70 % demand share. Their agility in rapid delivery and ability to certify against regional standards make them indispensable partners for capacity expansion projects.

List of Key Semiconductor Slurry Filters Companies Profiled

- Entegris

- Pall Corporation

- 3M

- TAK Microfilter Inc.

- Kan I International

- Taiwan Grace International

- JENG KANG International

- Cobetter

- Membrane Solutions

- Hangzhou Deefine

- Hangzhou Darlly Filtration Equipment Co.,Ltd

- Ever Pure Applied Materials Co., Ltd

- Feature‑Tec

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Cartridge‑type Filters

|

| By Application |

|

Tool Inlet Filtration

|

| By End User |

|

Foundries

|

| By Retention Rating |

|

0.5‑1 µm Retention

|

| By Filter Form Factor |

|

Capsule Filters

|

Regional Analysis: Semiconductor Slurry Filters Market

Asia‑Pacific

The bulk of wafer production sits in East‑Asia, where fabs operate at capacity levels that leave little margin for slurry contamination. This concentration forces filter providers to maintain a local inventory and to adapt designs to the high‑throughput environments of twin‑track lines, ensuring that filter change‑over does not become a bottleneck.

Recent disruptions have accelerated the shift toward vertically integrated supply chains. Companies are now evaluating the trade‑off between purchasing standard filters and co‑developing proprietary media that align with their slurry formulations, a move that tightens control over defect sources.

Environmental regulations in the region increasingly target waste‑water discharge from polishing processes. Filter manufacturers respond by offering reusable cartridge systems and low‑particle‑release materials, helping fabs meet tighter compliance thresholds while preserving cost efficiency.

Research parks in Hsinchu and Shenzhen host collaborations between academia and industry, accelerating the introduction of nanofiber filter media. These hubs act as incubators for next‑generation solutions that can handle the increasingly aggressive chemically‑mechanical planarization chemistries used in leading‑edge nodes.

North America

In North America, Semiconductor Slurry Filters Market benefits from a mature ecosystem of equipment OEMs and a strong emphasis on reliability engineering. U.S. fabs prioritize filter solutions that integrate seamlessly with automated slurry‑recycling loops, a practice driven by the high cost of consumables and the need for consistent particle control. Canadian research institutions contribute by testing novel filter composites under extreme temperature cycles, influencing vendor roadmaps. The regional focus on lifecycle cost reduction steers buyers toward long‑life cartridge designs that can be regenerated on‑site, aligning with sustainability initiatives championed by major semiconductor producers.

Europe

European players approach slurry filtration with a pronounced attention to precision and standardization. The continent’s mixed landscape of legacy fabs and emerging specialty wafer lines creates demand for adaptable filter configurations that can be tuned for varying slurry chemistries. German and Dutch engineering firms often act as system integrators, embedding filter diagnostics within broader process‑control platforms. Compliance with stringent EU environmental directives pushes manufacturers to adopt low‑emission filter materials, prompting a modest shift toward biodegradable binders. Collaborative European projects also explore the use of AI‑based predictive maintenance for filter health, aiming to pre‑empt particle‑induced yield losses.

South America

South America’s semiconductor activities remain concentrated in Brazil and Chile, where emerging fabs are establishing pilot lines for display and sensor applications. These facilities favor flexible filter solutions that can be quickly reconfigured as production ramps up. Local distributors often act as technical consultants, bridging the knowledge gap between filter technology and process engineers. Market participants note that cost‑sensitivity drives interest in modular filter kits that allow incremental upgrades without full equipment replacement, a strategy that supports incremental capacity expansion while managing capital expenditure.

Middle East & Africa

The Middle East & Africa region is witnessing the early stages of semiconductor‑related investments, particularly in free‑zone manufacturing hubs. While overall volume is modest, the strategic intent to develop domestic supply‑chain capabilities elevates the importance of reliable slurry filtration. Companies entering the market are looking for turnkey filter packages that can be deployed with limited on‑site expertise. Partnerships with established Asian filter producers are emerging, providing technology transfer that helps local fabs meet the stringent cleanliness standards required for advanced packaging processes.

Report Scope

This market research report provides a comprehensive analysis of the Semiconductor Slurry Filters Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Semiconductor Slurry Filters Market?

-> Semiconductor Slurry Filters Market was valued at USD 74.16 million in 2025 and is expected to reach USD 122 million by 2032 with a CAGR of 7.1% during the forecast period.

Which key companies operate in Semiconductor Slurry Filters Market?

-> Key players include Entegris, Pall, Cobetter, 3M, TAK Microfilter Inc., ROKI TECHNO, Kan I International, Taiwan Grace International, JENG KANG International, Membrane Solutions, Hangzhou Deefine, Hangzhou Darlly Filtration Equipment Co.,Ltd, Ever Pure Applied Materials Co., Ltd, Feature-Tec.

What are the key growth drivers?

-> Key growth drivers include higher yield sensitivity in advanced nodes, increasingly complex slurry chemistries, process capacity expansion, and stringent particle control requirements.

Which region dominates the market?

-> Asia-Pacific is the primary hub, accounting for roughly 60%‑70% of demand and supply, driven by concentrated wafer‑fab capacity and material localization.

What are the emerging trends?

-> Emerging trends include finer filtration under tighter defect tolerances, simultaneous optimization of higher throughput and longer filter lifetime, integration of modular filtration with in‑line monitoring, and increased investment in localized manufacturing capacity.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...