Touch Sensor Control Chip Market Insights

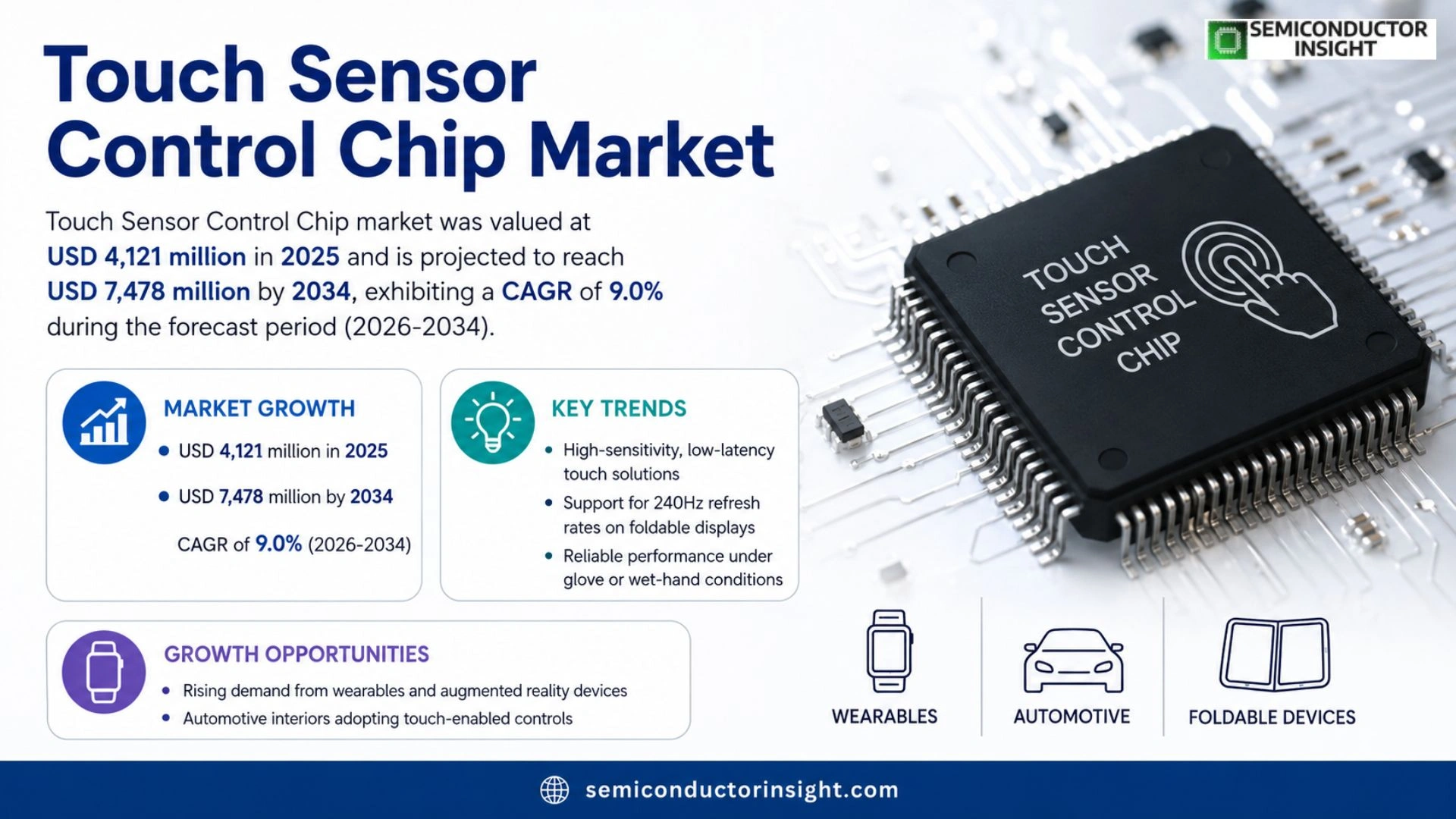

Global Touch Sensor Control Chip market was valued at USD 4,121 million in 2025 and is projected to reach USD 7,478 million by 2034, exhibiting a CAGR of 9.0% during the forecast period.

Touch sensor control chips are the core control ICs embedded in touchscreens, touch panels or touch buttons. They capture capacitance, resistance, voltage or pressure variations generated by a sensor surface and convert user actions,clicks, swipes, multi‑touch gestures or stylus input,into digital commands through signal amplification, filtering, analog‑to‑digital conversion, coordinate calculation and algorithmic recognition. These chips are integral to smartphones, tablets, wearables, automotive displays, home‑appliance panels and industrial terminals; their performance directly influences touch sensitivity, response latency, anti‑interference capability and power consumption.

MARKET DRIVERS

Consumer Demand for Seamless Interaction

Smartphones, tablets and home appliances are converging on touch‑first interfaces, pushing OEMs to source chips that deliver low latency and high precision. In Touch Sensor Control Chip Market, manufacturers that can guarantee sub‑millisecond response are seeing order volumes rise by double‑digit percentages, because end‑users now equate tactile fluidity with product quality.

Integration with Advanced IoT Devices

Edge‑connected devices require sensors that operate reliably under varying power budgets and temperature swings. Companies that fuse touch detection with on‑chip AI inference are gaining a competitive edge, as they enable features such as gesture‑based control without additional processors. This convergence is expanding the addressable market for control chips by roughly 8 % annually.

➤ “The ability to embed touch processing alongside security modules is reshaping OEM sourcing strategies, making integrated chips a decisive factor in product timelines.”

Regional adoption is accelerating in Asia‑Pacific, where consumer electronics firms are scaling production lines to meet local demand. The ripple effect is a modest uplift in component orders, reinforcing the overall bullish outlook for Touch Sensor Control Chip Market.

MARKET CHALLENGES

Technical Complexity in Miniaturization

Reducing die size while maintaining signal‑to‑noise ratios demands sophisticated lithography and advanced packaging. Many midsize suppliers lack the capital to invest in 7‑nm processes, resulting in a technology gap that slows product rollout and pressures profit margins.

Other Challenges

Supply Chain Volatility

Global semiconductor shortages have exposed the fragility of raw‑material pipelines. Lead times for high‑purity silicon wafers have stretched beyond 12 weeks, forcing manufacturers to hold higher inventory levels and eroding cash flow.

MARKET RESTRAINTS

High Component Costs

Advanced touch chips command premium pricing due to R&D intensity and low‑volume production runs. For price‑sensitive segments such as low‑cost wearables, the cost premium restricts wider adoption, curbing overall market expansion.

Additionally, compliance with electromagnetic compatibility (EMC) standards varies across jurisdictions, creating additional testing burdens that increase time‑to‑market for new designs.

MARKET OPPORTUNITIES

Emerging Wearables and Augmented Reality

Next‑generation smart glasses and fitness bands rely on ultra‑thin touch interfaces that blend with flexible substrates. Companies that can deliver chips compatible with bendable displays are positioned to capture a share of an estimated $2 billion niche within the next three years.

Automotive interiors are also embracing touch‑enabled climate and infotainment controls. The shift toward cabin digitization creates a distinct growth corridor, as automakers look for chips that meet automotive reliability grades while offering a premium user experience.

Touch Sensor Control Chip Market Trends

Convergence on High‑Sensitivity, Low‑Latency Solutions

Touch Sensor Control Chip Market is moving away from basic capacitance detection toward chips that combine ultra‑fast coordinate calculation, robust anti‑interference filtering, and integrated active‑pen support. 2025 saw an average selling price of $2.5 per chip while volume reached 1.805 billion units, indicating that manufacturers are able to command modest premiums for added functionality. End‑device designers are now specifying touch controllers that can sustain 240 Hz refresh rates on foldable displays and remain responsive under glove or wet‑hand conditions. This shift is driven by consumer expectations for seamless interaction across smartphones, wearables, and increasingly, vehicle infotainment screens. Companies that embed proprietary algorithms into a single TDDI (touch‑display‑driver‑integrated) block are able to reduce bill‑of‑materials, which translates into higher gross margins,often in the 50‑60 % range for premium segments.

Other Trends

Margin Compression in Volume‑Driven Consumer Segments

While high‑end devices reward sophisticated chip designs, the bulk of Touch Sensor Control Chip Market still serves low‑cost smartphones and household appliances. In these categories, competition squeezes gross profit margins to between 10 % and 25 %. Manufacturers rely on scale, aggressive wafer‑foundry pricing, and minimal packaging differentiation to stay viable. The 2.57 billion‑chip production capacity reported for 2025 illustrates that excess capacity exists, prompting players to seek cost‑saving partnerships and standardized testing processes. Without clear differentiation, price wars are likely to persist, pushing marginal producers toward consolidation or niche specialization.

Automotive and Industrial Adoption Elevates Profitability

Automotive infotainment systems and industrial control terminals are reshaping the revenue mix. These applications demand high anti‑interference capability, long‑term reliability, and compliance with automotive‑grade standards, which lifts average margins to the 40‑55 % band. The growing prevalence of large‑format vehicle dashboards and rugged factory interfaces forces OEMs to source chips that can operate across wide temperature ranges and with minimal latency. As a result, firms that have invested in hardened analog front‑ends and certified automotive modules are securing contracts that outpace the modest growth seen in the consumer arena. The strategic implication for suppliers is clear: deeper integration with system‑level partners and expanded algorithm portfolios will be essential to capture the premium pricing available in these high‑value markets.

COMPETITIVE LANDSCAPE

Key Industry Players

Touch Sensor Control Chip Market Competitive Overview

Synaptics remains the cornerstone of the high‑performance segment, leveraging its deep algorithmic expertise and integrated TDDI solutions to secure contracts with leading smartphone OEMs and premium automotive infotainment suppliers. The firm’s ability to deliver low‑latency, multi‑gesture processing while maintaining a gross margin above 50 % differentiates it from lower‑tier manufacturers that compete mainly on unit price. This strategic positioning forces rivals to either specialize in niche applications or invest heavily in analog front‑end innovation to close the technology gap.

The remainder of the landscape is populated by a mix of diversified semiconductor groups and specialist firms. Goodix and FocalTech dominate the mid‑range consumer electronics space, offering cost‑effective capacitive ICs that satisfy volume‑driven smartphone makers. Novatek and Himax have pivoted toward automotive and industrial panels, where their robust anti‑interference architectures command higher price points. Smaller entrants such as ELAN Microelectronics, Zinitix, and Luhua Group focus on emerging wearable and smart‑home interfaces, relying on tight integration with original equipment manufacturers to establish market footholds. The overall competitive tension is shifting from pure price rivalry to a battle over algorithmic differentiation, power‑efficiency metrics, and ecosystem‑level validation.

List of Key Touch Sensor Control Chip Companies Profiled

- Synaptics

- Goodix

- FocalTech

- Novatek

- Himax

- ELAN Microelectronics

- Zinitix

- Luhua Group

- STMicroelectronics

- Samsung Electronics

- LX Semicon

- Chipone

- Ilitek

- Raydium

- Solomon Systech

- Jadard Technology

- Omnivision

- Yitoa Micro Technology

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Capacitive Touch ICs are the dominant type because they provide the most responsive user experience across a wide range of devices.

|

| By Application |

|

Smartphones and Tablets drive the most demanding requirements for touch sensor control chips.

|

| By End User |

|

Consumer Electronics Manufacturers prioritize chips that balance cost efficiency with high‑quality touch experience.

|

| By Technology |

|

Integrated Algorithmic Solutions are gaining traction because they embed sophisticated noise‑cancellation and gesture logic directly in silicon.

|

| By Performance Capability |

|

Anti‑Interference Robust Chips are critical for automotive and industrial deployments where electromagnetic noise is pervasive.

|

Regional Analysis: Touch Sensor Control Chip Market

North America

Companies are re‑engineering their component sourcing by integrating silicon‑photonic interconnects, which shortens lead times for high‑frequency touch chips. Regional fabs are increasingly adopting modular production lines that can switch between legacy and emerging process nodes, giving manufacturers the agility to respond to shifting design specifications without costly re‑tooling.

The U.S. Federal Communications Commission and Canadian standards agencies have harmonised electromagnetic emission limits, simplifying cross‑border product launches. This alignment reduces time‑to‑market for multi‑regional devices, encouraging firms to consolidate development cycles and allocate resources toward functional enhancements.

There is a decisive shift toward ultra‑thin form factors, compelling chip designers to embed advanced signal‑conditioning blocks directly onto the sensor die. This integration eliminates external components, trims bill of materials, and improves tactile response consistency across temperature extremes common in automotive interiors.

Legacy silicon vendors are leveraging legacy process expertise to offer cost‑effective solutions for mass‑market devices, while emerging fabless firms target premium segments with customizable IP cores. The resulting dual‑track strategy forces incumbents to diversify portfolios, balancing volume‑driven profitability with high‑margin specialty offerings.

Europe

Europe’s touch sensor ecosystem is characterised by strong collaboration among automotive consortiums and consumer‑electronics clusters in Germany and France. Regional manufacturers are prioritising sustainability, embedding recyclable materials and low‑power architectures to meet EU directives on electronic waste. The prevalence of standards such as EN 61322 fosters interoperability, enabling smaller firms to participate in multinational projects without extensive re‑engineering. Consequently, the market sees a steady influx of niche players offering specialised interface solutions for smart appliances and industrial control panels.

Asia‑Pacific

In Asia‑Pacific, rapid adoption of touch‑enabled wearables and smart home devices drives demand for cost‑efficient control chips. Chinese manufacturers benefit from scale, frequently co‑developing chips with original equipment manufacturers to lock in volume contracts. Meanwhile, South Korean firms advance high‑frequency designs that support augmented‑reality headsets, positioning the region as a hub for next‑generation tactile experiences. The competitive pressure encourages continuous refinement of wafer yields and aggressive pricing strategies.

South America

South America exhibits a fragmented market where regional distributors play a pivotal role in bridging global chip suppliers with local appliance assemblers. Brazil’s growing automotive sector is experimenting with touch‑sensor‑based infotainment suites, prompting local design houses to adapt foreign IP for regional compliance. Market participants are also exploring low‑cost packaging techniques to address price sensitivity while maintaining functional integrity for everyday consumer products.

Middle East & Africa

The Middle East & Africa region is witnessing nascent interest in touch‑sensor technologies for public‑sector kiosks and fintech terminals. Investment in smart‑city infrastructure creates pockets of demand for ruggedized control chips capable of withstanding harsh climates. Local OEMs are forming joint ventures with established silicon providers to acquire design know‑how, accelerating the region’s transition from import‑reliant to modestly self‑sufficient production capabilities.

Report Scope

This market research report provides a comprehensive analysis of the Touch Sensor Control Chip Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Touch Sensor Control Chip Market?

-> Touch Sensor Control Chip Market was valued at USD 4,121 million in 2025 and is expected to reach USD 7,478 million by 2034, growing at a CAGR of 9.0% during the forecast period.

Which key companies operate in Touch Sensor Control Chip Market?

-> Key players include Synaptics, Goodix, FocalTech, Novatek, Himax, Parade, STMicroelectronics, Samsung Electronics, LX Semicon, ELAN Microelectronics, Melfas, Zinitix, Luhua Group, Ilitek, Chipone, Raydium, Solomon Systech, Jadard Technology, OMNIVISION, Yitoa Micro Technology.

What are the key growth drivers?

-> Growth is driven by the rapid adoption of touch‑enabled devices such as smartphones, tablets, smart wearables, automotive displays, and smart‑home appliances, as well as demand for higher sensitivity, lower latency, robust anti‑interference performance, and integration of active‑pen and TDDI solutions.

Which region dominates the market?

-> Asia‑Pacific holds the largest share, propelled by extensive manufacturing bases, high consumption of consumer electronics, and strong automotive and industrial automation growth.

What are the emerging trends?

-> Emerging trends include increased integration of TDDI (Touch‑Display‑Driver‑Integration) technologies, AI‑enhanced touch algorithms, waterproof/glove‑compatible sensors, active‑pen support, and ultra‑low‑power designs for IoT‑centric applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...