NVMe SSD Market Insights

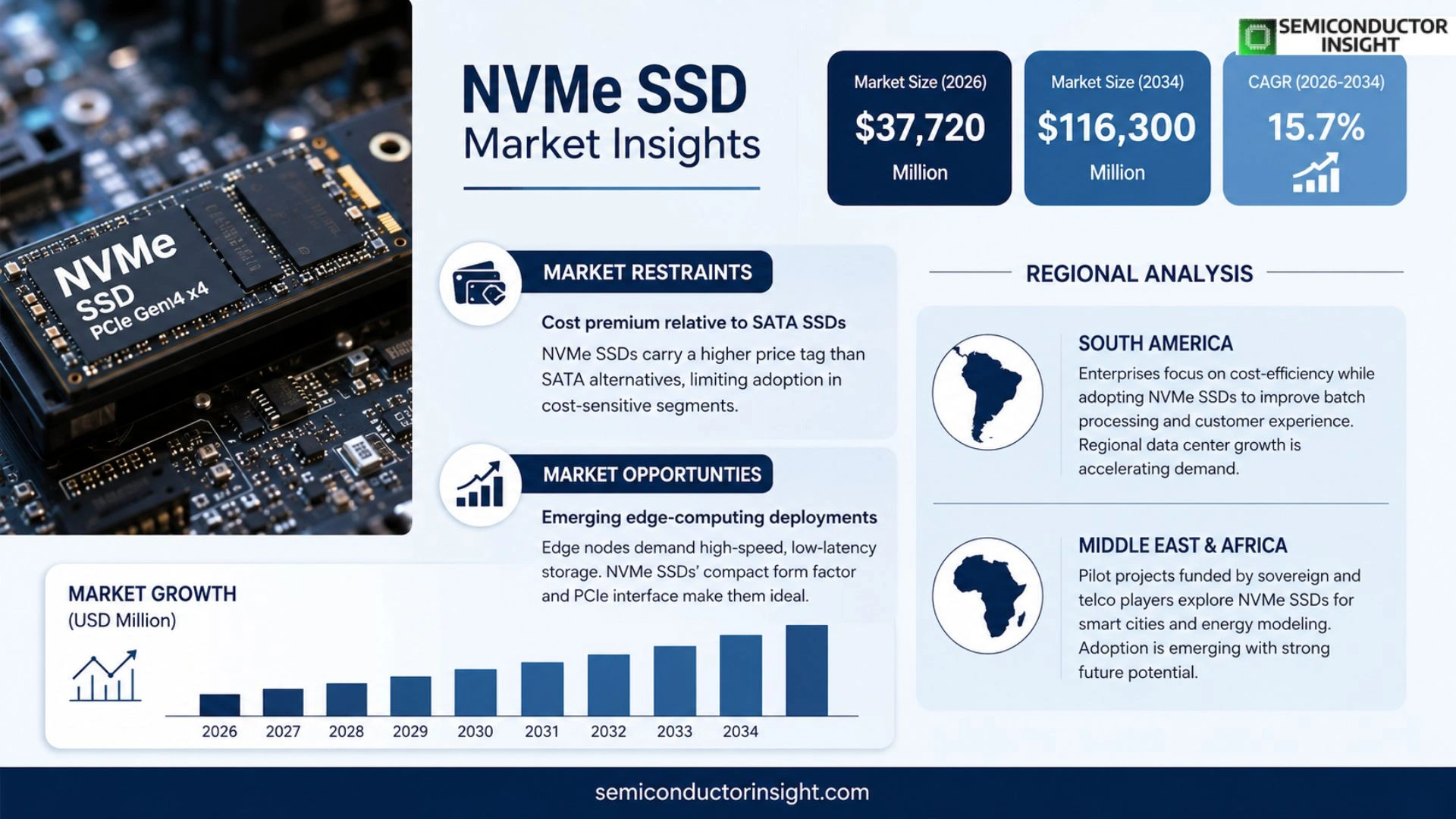

Global NVMe SSD market size was valued at USD 31,526 million in 2025 and is projected to reach USD 86,595 million by 2032 and approximately USD 116,300 million by 2034, exhibiting a CAGR of about 15·7% during the forecast period.

NVMe SSD (Non‑Volatile Memory Express Solid State Drive) is a type of solid‑state storage device that connects via the PCIe interface and uses the NVMe protocol. It is specifically optimized for non‑volatile memory such as NAND flash, delivering lower latency, higher parallelism and faster data transfer speeds compared with traditional SATA/AHCI‑based SSDs. NVMe SSDs are widely deployed in high‑performance computing, data centers and premium consumer devices.

MARKET DRIVERS

Performance Edge in Data‑Intensive Workloads

Enterprises are replacing legacy storage tiers with flash solutions that can sustain high I/O rates. The NVMe SSD Market benefits from this shift because NVMe protocols eliminate the bottleneck of traditional SATA interfaces, allowing workloads such as real‑time analytics and AI model training to run with markedly lower latency. Companies that adopt these devices report faster time‑to‑insight, which directly boosts competitive positioning.

Economies of Scale in Manufacturing

Foundries have refined 3D‑stacked NAND processes, reducing per‑gigabyte cost while preserving endurance. This cost curve creates a feedback loop: lower prices stimulate broader deployment, which in turn justifies larger production runs. The resulting price elasticity encourages even mid‑market segments to allocate budget toward NVMe‑based platforms rather than older HDD or SATA‑SSD options.

➤ Adoption of NVMe over PCIe Gen 4 is reshaping server chassis design, prompting OEMs to prioritize thermal management and slot density.

Cloud providers are re‑architecting their storage tiers to align with the performance envelope of NVMe drives. By consolidating workloads onto fewer, faster devices, they achieve higher server utilisation and lower power per transaction, translating into measurable operational savings.

MARKET CHALLENGES

Compatibility with Legacy Infrastructure

Many data centres still run on platforms that lack native PCIe 4.0 or U.2 connectors. Retrofitting such environments incurs both capital outlay and downtime, which can temper the pace of substitution despite clear performance incentives. Vendors must therefore supply bridge adapters or hybrid firmware, adding complexity to deployment plans.

Other Challenges

Supply‑Chain Volatility

Fluctuations in semiconductor fab capacity create periodic shortages of high‑density NAND chips. When inventory tightens, lead times extend, and pricing pressure rises, limiting the ability of end‑users to scale projects predictably.

Regulatory scrutiny over data sovereignty is also gaining traction. Organizations operating across multiple jurisdictions must verify that NVMe‑based storage solutions comply with regional encryption and audit requirements, adding a layer of compliance overhead.

MARKET RESTRAINTS

Cost Premium Relative to SATA SSDs

Although manufacturing efficiencies are improving, NVMe devices still command a price premium compared with SATA‑based alternatives. For organisations with modest performance needs, the additional expense can be hard to justify, especially when budget cycles are constrained. This price differential slows diffusion in cost‑sensitive segments such as small‑to‑medium enterprises.

MARKET OPPORTUNITIES

Emerging Edge‑Computing Deployments

Edge nodes processing video streams, autonomous‑vehicle telemetry, and IoT sensor fusion require storage that can keep pace with high‑throughput, low‑latency demands. NVMe SSDs, with their compact form factor and PCIe interface, are uniquely suited to these workloads. Companies that position their offerings around edge‑ready form factors can capture a growing slice of the NVMe SSD Market as the edge‑computing ecosystem matures.

NVMe SSD Market Trends

Enterprise Adoption Accelerates

Production data from 2025 shows roughly 557 million units leaving factories, with an average selling price near US$ 62. The surge in unit output reflects a decisive move by hyperscale operators to replace legacy storage stacks with PCIe‑based solutions that can sustain the bandwidth demands of AI inference and large‑scale cloud services. Because the latency advantage of NVMe over SATA‑based SSDs translates into measurable cost savings on power and cooling, data‑center operators are scaling deployments faster than the typical PC refresh cycle. This shift reshapes the revenue profile of the NVMe SSD Market, turning it into a core component of digital infrastructure rather than a peripheral performance add‑on.

Other Trends

Supply Chain Consolidation

The upstream segment remains tightly held by a handful of NAND manufacturers, which gives them leverage over pricing and volume allocation. Mid‑stream firms that can lock in long‑term NAND contracts are better positioned to balance inventory against the growing demand from both enterprise and premium consumer segments. The vertical integration of controller design with firmware optimization further differentiates players that control the full stack, allowing them to capture higher gross margins,illustrated by the industry‑wide 38.6 % average in 2025. Companies that fail to secure stable supply risk margin compression as they contend with periodic flash shortages.

Architectural Shift Toward AI Workloads

Beyond raw throughput, the next wave of adoption hinges on how well SSDs manage sustained mixed‑read/write patterns typical of training and inferencing tasks. Vendors are embedding power‑efficiency algorithms and endurance‑focused firmware to reduce wear‑leveling overhead while maintaining deterministic latency. These system‑level enhancements enable AI clusters to keep more data in‑place, shortening model iteration cycles. For OEMs, the implication is clear: investing in advanced controller‑firmware co‑design will secure a disproportionate share of the upcoming purchasing wave, as enterprises prioritize total‑cost‑of‑ownership over headline speed figures.

COMPETITIVE LANDSCAPE

Key Industry Players

NVMe SSD Market – Competitive Overview

Samsung Electronics remains the anchor of the NVMe SSD ecosystem. By owning NAND fab capacity, controller design teams, and high‑volume assembly lines, Samsung can synchronize product cycles with raw‑material availability, which translates into tighter pricing discipline and faster time‑to‑market for next‑generation PCIe 4.0/5.0 drives. Its portfolio spans consumer‑grade M.2 modules to enterprise‑grade EDSFF form factors, allowing the company to capture demand across data centers, AI accelerators, and high‑performance gaming rigs. The depth of its R&D pipeline, combined with a global sales network, has forced rivals to align their strategies around securing NAND supply and co‑developing firmware that optimizes power‑efficiency and endurance for AI workloads.

Beyond Samsung, the field is populated by a blend of legacy storage specialists and newer entrants that carve out value by focusing on niche segments or differentiated technology. SK Hynix and Kioxia leverage their NAND heritage to offer cost‑effective high‑capacity drives for hyperscale cloud operators. Western Digital and Micron push the envelope on controller‑firmware integration, targeting low‑latency enterprise servers. Solidigm, spun out of Intel, concentrates on PCIe 5.0 solutions for edge AI. Companies such as Seagate, Kingston, ADATA, Transcend, Silicon Power, TeamGroup, and PNY supplement the market with specialty form factors,U.2, Add‑in Card, and ruggedized models,catering to OEMs that require tailored thermal or mechanical designs. Their collective emphasis on firmware adaptability and supply‑chain agility creates a competitive environment where differentiation hinges more on system‑level optimization than raw throughput alone.

List of Key NVMe SSD Companies Profiled

- Samsung Electronics

- Micron Technology

- SK Hynix

- Western Digital

- Kioxia Holdings

- Solidigm

- Seagate Technology

- Kingston Technology

- ADATA Technology

- Transcend Information

- Silicon Power

- TeamGroup

- PNY Technologies

- Innodisk

- Yangtze Memory Technologies

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Enterprise SSDs dominate strategic importance.

|

| By Application |

|

AI/ML Workloads are the leading growth catalyst.

|

| By End User |

|

Cloud Service Providers lead adoption.

|

| By Interface Generation |

|

PCIe 4.0/5.0 drive future architecture.

|

| By Form Factor |

|

EDSFF Form Factor emerging in hyperscale.

|

Regional Analysis: NVMe SSD Market

North America

Large‑scale firms view NVMe SSDs as a catalyst for operational efficiency, replacing older storage tiers to streamline transaction processing and real‑time reporting. The shift is less about raw capacity and more about unlocking latency gains that translate into competitive advantage in time‑sensitive markets.

Data‑center architects are redesigning rack layouts to accommodate denser NVMe form factors, allowing higher compute density per square foot. This redesign reduces power overhead and simplifies cooling strategies, reinforcing the business case for further capital allocation.

High‑performance gaming and content‑creation ecosystems drive consumer willingness to pay a premium for NVMe SSDs. The perception of “instant‑load” experiences fuels iterative upgrades, encouraging manufacturers to embed the technology across product lines rather than confine it to niche models.

Data‑sovereignty statutes in the United States promote on‑premise storage solutions, prompting enterprises to favor locally managed NVMe arrays that satisfy compliance mandates while preserving performance.

Europe

European organizations are balancing stringent data‑privacy regulations with the desire to modernize infrastructure, positioning NVMe SSDs as a compliant pathway to faster processing. Automotive manufacturers, a notable sub‑segment, leverage the technology to support advanced driver‑assistance systems that require rapid sensor data fusion. Meanwhile, fintech firms integrate high‑throughput storage to meet transaction‑speed expectations set by regulators, reinforcing the market’s relevance across divergent industries throughout the continent.

Asia‑Pacific

In Asia‑Pacific, the market momentum stems from a blend of aggressive consumer electronics roll‑outs and burgeoning cloud services. Manufacturers in China and South Korea embed the drives into flagship smartphones and ultrabooks, signaling a shift toward portable high‑speed storage. Simultaneously, regional cloud providers expand hyperscale facilities, selecting NVMe SSDs for their ability to accelerate AI workloads without compromising power efficiency, thereby shaping competitive dynamics across the sub‑region.

South America

South American enterprises are navigating cost‑sensitivity while recognizing the operational upside of adopting next‑generation storage. Financial institutions, in particular, view NVMe SSDs as a lever to reduce batch‑processing times, which can improve customer experience without demanding extensive capital expenditure. The gradual rollout of regional data centers further amplifies demand, as providers seek to differentiate service tiers by leveraging the performance edge offered by the technology.

Middle East & Africa

The Middle East & Africa region exhibits a cautiously optimistic stance, with sovereign wealth funds and telco operators financing pilot projects that explore NVMe SSD integration within smart‑city frameworks. Energy firms, confronting data‑intensive geophysical modeling, are experimenting with high‑speed storage to shorten analysis cycles. Although adoption rates lag behind more mature markets, strategic investments hint at a trajectory that could reshape the regional storage ecosystem in the coming years.

Report Scope

This market research report provides a comprehensive analysis of the NVMe SSD Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of NVMe SSD Market?

-> Global NVMe SSD market size is projected to reach USD 86,595 million by 2032 and approximately USD 116,300 million by 2034.

Which key companies operate in NVMe SSD Market?

-> Key players include Samsung Electronics, SK Hynix, Solidigm, Kioxia Holdings, Western Digital, Micron Technology, Seagate Technology, Kingston Technology, ADATA Technology, Transcend Information, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for high‑performance computing, exponential growth of data centers and AI workloads, the need for lower latency and higher parallelism, and the transition of NVMe SSDs from consumer upgrades to core enterprise infrastructure.

Which region dominates the market?

-> Asia‑Pacific leads the market in terms of revenue share, driven by large‑scale data‑center deployments and rapid adoption of AI‑intensive applications, while North America remains a strong secondary market.

What are the emerging trends?

-> Emerging trends include system‑level optimization for power efficiency and endurance, AI‑aware firmware, tighter integration of NAND supply chains, and the development of advanced controllers that target enterprise AI and cloud workloads.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...