EDSFF NVMe SSD Market Insights

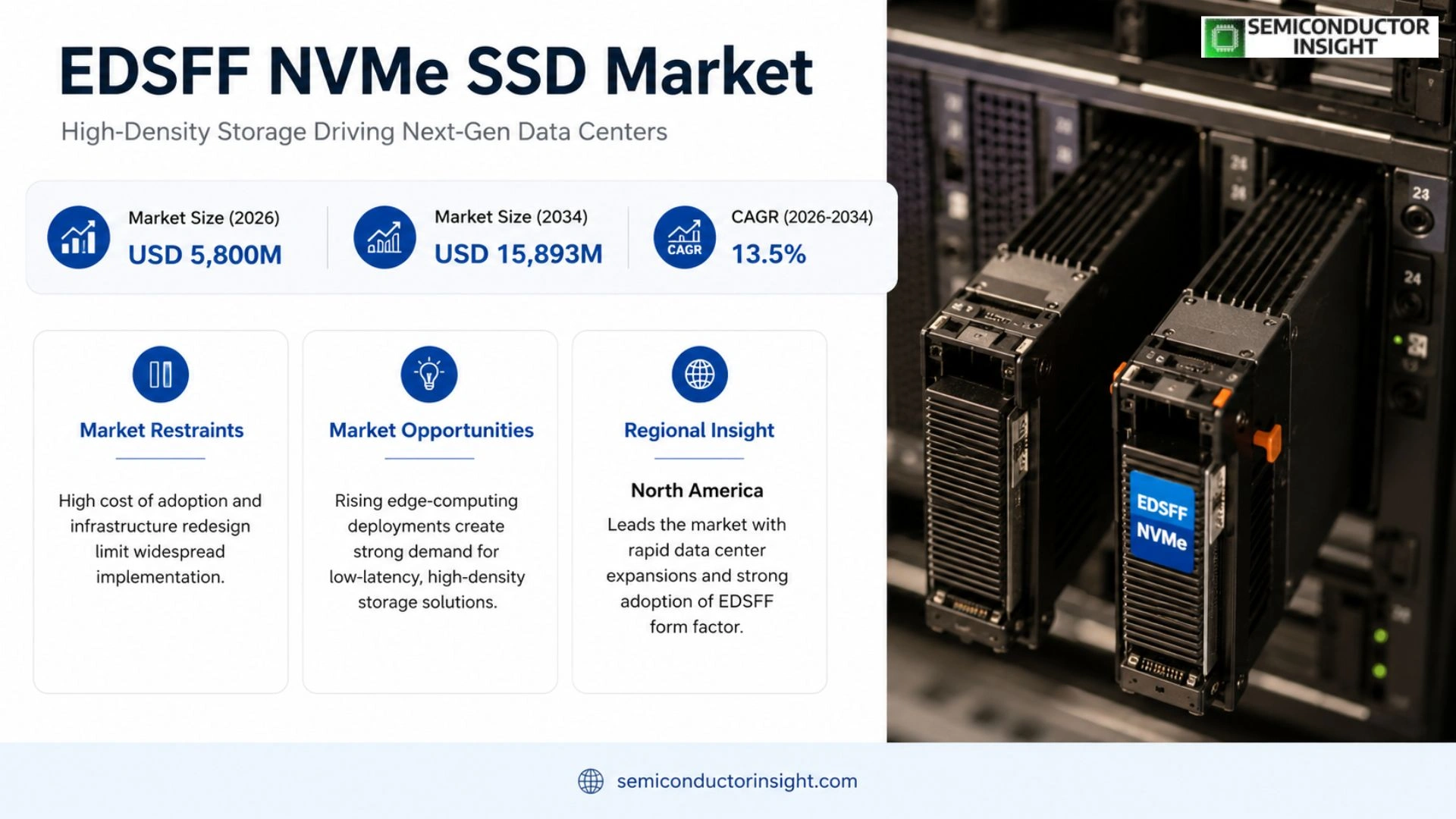

Global EDSFF NVMe SSD market size was valued at USD 5,675 million in 2025. The market will rise from USD 5,800 million in 2026 to USD 15,893 million by 2034, delivering a compound annual growth rate of approximately 13.5% during the forecast period.

EDSFF NVMe SSD (Enterprise & Datacenter Standard Form Factor NVMe Solid State Drive) is a standardized solid‑state drive designed for high‑performance enterprise and data‑center workloads. Built on the NVMe protocol and conforming to the EDSFF mechanical specification, it replaces legacy 2½‑inch U.2 drives while offering superior thermal management, higher storage density and easier serviceability.

The sector is expanding because hyperscale cloud operators and AI‑driven HPC clusters demand greater bandwidth and denser storage footprints; meanwhile advances in PCIe Gen4/Gen5 interfaces enable faster data paths that align with GPU‑intensive applications. However, early‑stage standardisation creates compatibility challenges that manufacturers are addressing through tighter ecosystem collaboration.

MARKET DRIVERS

Increasing Data‑Center Density Requirements

The acceleration of AI workloads and real‑time analytics forces operators to pack more compute power per rack. EDSFF NVMe SSDs satisfy this pressure by offering a compact form factor that maximizes usable board space while retaining high throughput. Facilities that adopt the standard can reduce floor‑space costs by up to 15 % compared with legacy U.2 solutions, a tangible advantage in hyperscale campuses where every square foot commands a premium.

Shift Towards Low‑Latency Storage Architectures

Enterprises are moving away from tiered storage hierarchies that rely on slower SAS drives. The direct‑attach nature of EDSFF modules eliminates interposer latency, delivering sub‑microsecond I/O response times that translate into faster model training cycles. Companies that have migrated to this architecture report a 20‑30 % reduction in job completion time, underpinning a strategic advantage in time‑sensitive markets such as financial services.

➤ “Adopting EDSFF has reshaped our rack design, allowing us to double the flash capacity without expanding the chassis footprint.” – Chief Infrastructure Officer, leading cloud provider

Beyond performance, the standard’s modularity simplifies maintenance. Hot‑swap capability means a failed drive can be replaced without interrupting power, reducing mean‑time‑to‑repair (MTTR) and supporting the high‑availability SLAs demanded by tier‑1 operators.

MARKET CHALLENGES

Thermal Management Constraints

While the dense packaging delivers space efficiency, it also concentrates heat sources. Without optimized cooling, device temperatures can climb beyond the safe operating envelope, throttling performance. Operators must invest in enhanced airflow designs or liquid‑cooling loops, which adds upfront capital and operational complexity.

Other Challenges

Supply Chain Volatility

Component shortages for high‑performance NAND and the specialized connectors required by EDSFF have introduced lead‑time variability. Procurement teams now negotiate longer safety stocks, increasing inventory holding costs and potentially limiting rapid scaling for new data‑center builds.

MARKET RESTRAINTS

High Cost of Adoption

The premium pricing of EDSFF NVMe SSDs relative to conventional 2.5‑inch drives remains a barrier for cost‑sensitive segments. Early‑stage deployments often require redesign of server backplanes and power distribution, inflating the total cost of ownership. Organizations weighing the trade‑off must justify the expense through measurable gains in performance or density.

MARKET OPPORTUNITIES

Emerging Edge‑Computing Deployments

Edge locations,ranging from autonomous‑vehicle fleets to remote telecom stations,are beginning to demand the same low‑latency storage that data centers have long required. The compact footprint of EDSFF aligns with the space‑constrained enclosures typical of edge nodes, while its high bandwidth supports AI inference at the source. Vendors that tailor reference designs for ruggedized edge hardware can capture a nascent segment forecasted to expand markedly over the next five years.

EDSFF NVMe SSD Market Trends

Thermal Efficiency and Density Gains Drive Adoption

The enterprise segment is rapidly swapping legacy 2.5‑inch U.2 drives for EDSFF NVMe SSDs because the new form factor delivers superior heat management while slashing the rack‑space required per terabyte. In 2025, global production reached roughly 9.56 million units at an average selling price of $650, a level that demonstrates both scale and price stability. Operators of hyperscale cloud platforms are especially attentive to the thermal headroom offered by the optimized airflow design; the extra margin enables higher core frequencies on AI accelerators without triggering throttling events. Consequently, total cost of ownership improves as power overhead falls and replacement cycles extend. The shift also aligns with the broader push toward denser compute nodes, where every millimeter of cabinet space translates into measurable revenue. However, the early‑stage standardization of the EDSFF ecosystem injects a degree of compatibility risk, prompting data‑center engineers to coordinate closely with OEMs during migration planning.

Other Trends

Supply‑Chain Consolidation Around NAND and Controllers

Upstream, the market is anchored by a tight group of NAND producers,Samsung, SK Hynix, Micron and Kioxia,which secures a reliable supply of high‑performance memory chips. Downstream, controller innovators such as Phison, Marvell and Silicon Motion shape firmware functionality and influence the timing of PCIe generation roll‑outs. This vertical integration has lifted gross profit margins to an average of 42 % and curbed the volatility that traditionally plagued SSD pricing. On the downside, the concentration raises entry barriers for niche manufacturers lacking strategic alliances, reinforcing the dominance of established players. For buyers, the concentrated supply base translates into predictable lead times but also diminishes bargaining leverage, a dynamic that will shape pricing negotiations over the next few years.

Form‑Factor Diversification Aligns With Workload Profiles

The EDSFF family’s triad,E1.S, E1.L and E3.S,offers a calibrated response to divergent workload requirements. AI‑heavy training clusters gravitate toward the high‑density E3.S modules, which accommodate capacities well beyond 30 TB and sustain the sustained throughput needed for large model parameter sets. Conversely, latency‑sensitive transactional databases prefer the compact, low‑power E1.S variant that slots neatly into blade servers and minimizes signal latency. This granular approach encourages data‑center owners to deploy a mix of form factors within a single facility, creating cross‑sell opportunities for SSD manufacturers. As the industry matures, the progressive displacement of U.2 drives becomes more pronounced, positioning EDSFF as the foundational storage architecture for next‑generation, AI‑driven infrastructure. The result is a reinforcing loop: broader adoption fuels higher production volumes, which in turn compresses unit costs and accelerates the transition of legacy systems.

COMPETITIVE LANDSCAPE

Key Industry Players

EDSFF NVMe SSD Competitive Overview – 2025‑2032

Samsung Electronics dominates the high‑density tier, leveraging its NAND lead‑time advantage and an integrated controller portfolio to supply both E1.S and E3.S modules to hyperscale operators. The company’s ability to match flash cost declines with aggressive volume‑scale production gives it a pricing edge that forces downstream integrators to align their road‑maps around Samsung‑qualified parts. Western Digital’s recent acquisition of Solidigm has broadened its firmware capabilities, allowing it to compete directly in the AI‑centric segment where thermal efficiency is critical. Both firms benefit from vertically integrated supply chains that reduce exposure to component shortages and enable rapid firmware iteration, a decisive factor for data‑center architects seeking predictable performance.

Beyond the giants, a constellation of specialist manufacturers is shaping niche corridors. Kioxia and SK Hynix supply memory‑centric solutions that prioritize power efficiency for edge‑cloud deployments, while Micron’s focus on multi‑dimensional stacking drives capacity gains in the 8‑30 TB bracket. Chinese players such as DapuStor and InnoGrit have secured contracts with regional cloud providers by offering cost‑effective E1.L variants tuned for PCIe Gen4. Companies like Innodisk and SMART Modular Technologies differentiate through ruggedized enclosures appealing to telecom and industrial customers, whereas Seagate and Kingston leverage brand recognition to capture mid‑range enterprise workloads.

List of Key EDSFF NVMe SSD Companies Profiled

- Samsung Electronics

- Western Digital

- Solidigm

- Kioxia

- SK Hynix

- Micron Technology

- Seagate Technology

- Kingston Technology

- Innodisk Corporation

- DapuStor

- InnoGrit

- SMART Modular Technologies

- Huawei Technologies

- Swissbit

- ATP Electronics

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Form‑Factor Diversity drives adoption because each size aligns with distinct server architectures; • Designers can match thermal envelope and space constraints precisely, reducing cooling overhead. • Modular approach simplifies upgrades and serviceability, encouraging long‑term platform commitment. • Early ecosystems favor E1.S for dense rack units while E3.S meets emerging AI workloads demanding ultra‑high capacity. |

| By Application |

|

AI‑Centric Workloads increasingly dictate storage choices; • HPC and AI clusters seek the superior thermal performance of EDSFF to sustain sustained throughput. • Cloud providers value the density and serviceability, enabling higher rack‑level capacity. • Edge deployments appreciate the robust airflow design that tolerates harsher operating environments. |

| By End User |

|

Strategic Adoption reflects long‑term infrastructure planning; • Cloud operators prioritize scalability and lower total cost of ownership, seeing EDSFF as a future‑proof investment. • Enterprises focused on latency‑sensitive workloads appreciate the improved airflow and reliability. • Research institutions value the ability to pack large capacity drives in limited space for data‑intensive experiments. |

| By Interface Generation |

|

Generational Leap influences architectural decisions; • Gen5 compatibility is a key differentiator for AI servers that demand extreme bandwidth. • Legacy Gen3 remains viable for cost‑sensitive workloads, ensuring a migration path. • The industry views the transition as a catalyst for broader adoption of EDSFF across server generations. |

| By Thermal Management |

|

Thermal Innovation underpins market momentum; • Passive airflow designs reduce mechanical complexity and improve reliability. • Active heat‑sink solutions cater to high‑density racks where heat buildup is a concern. • Emerging liquid‑cooling integrations position EDSFF as the preferred storage for next‑gen AI accelerators. |

Regional Analysis: EDSFF NVMe SSD Market

North America

Customers prioritize multi‑terabyte modules that fit within the same volumetric envelope, prompting manufacturers to double‑stack NAND layers and adopt advanced packaging. The result is a noticeable move toward 4 TB and 8 TB capacities per drive, making the platform attractive for dense compute clusters.

System integrators increasingly specify EDSFF in rack‑scale designs because the architecture aligns with high‑performance compute nodes. Integration of thermal‑aware backplanes has become a differentiator, reducing cooling overhead and extending device lifespan.

Component shortages that once hampered SSD rollouts are easing as semiconductor fabs re‑tool for EDSFF production. This shift improves lead times and enables vendors to fulfill larger orders without sacrificing inventory buffers.

Enterprises are demanding tighter SLAs on latency and endurance. Vendors that bundle predictive analytics for wear‑leveling and real‑time health monitoring are gaining preference among data‑center operators.

Europe

European cloud providers are aligning their roadmap with sustainability targets, and EDSFF NVMe SSD Market offers a pathway to lower energy consumption per petabyte. Countries such as Germany and the Netherlands are investing in hyperscale facilities that favor high‑density storage to reduce floor space. Meanwhile, the United Kingdom’s focus on data‑sovereignty encourages a preference for on‑prem procurement, reinforcing the appeal of locally sourced EDSFF solutions. OEMs are tailoring firmware to meet GDPR‑driven audit requirements, creating a niche for vendors that can certify compliance at the drive level. The competitive landscape is fragmenting, with niche players carving out segments in financial services and scientific research where latency‑critical workloads dominate.

Asia‑Pacific

The Asia‑Pacific region exhibits a heterogeneous mix of mature markets like Japan and emerging hubs such as Vietnam. Rapid digitization across manufacturing and telecom sectors drives a need for compact, high‑throughput storage. Enterprises are upgrading legacy infrastructure to accommodate AI inference at the edge, and EDSFF’s form factor matches these constraints. Local chip manufacturers are beginning to co‑invest in advanced packaging, which shortens the supply chain and reduces import dependence. Policy incentives aimed at building sovereign cloud capabilities in countries like India further stimulate adoption, particularly where data‑center operators seek to differentiate on performance per rack unit.

South America

In South America, the adoption curve is moderated by investment cycles, yet large mining and energy conglomerates are early adopters seeking to consolidate storage footprints. Brazil’s expanding data‑center market serves as a catalyst, with operators testing EDSFF in tier‑2 storage pools to balance cost and capacity. Local distributors are focusing on value‑added services, including on‑site integration and extended warranty programs, to overcome perceived risk. While price sensitivity remains high, the promise of reduced operational expenditure through lower cooling loads is compelling for cost‑conscious firms.

Middle East & Africa

The Middle East’s strategic positioning as a digital hub for the region fuels interest in high‑density storage architectures. Sovereign cloud initiatives in Saudi Arabia and the United Arab Emirates prioritize resilience and scalability, making EDSFF an attractive choice. African markets, though smaller, are witnessing pilot projects in financial services where data integrity and rapid access are paramount. Partnerships between global OEMs and regional system integrators are emerging, facilitating technology transfer and localized support, which in turn lowers barriers to entry for enterprises considering the transition.

Report Scope

This market research report provides a comprehensive analysis of the EDSFF NVMe SSD Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of EDSFF NVMe SSD Market?

-> EDSFF NVMe SSD market will rise from USD 5,800 million in 2026 to USD 15,893 million by 2034.

Which key companies operate in EDSFF NVMe SSD Market?

-> Key players include Samsung Electronics, SK Hynix, Solidigm, Kioxia, Micron Technology, Western Digital, Sandisk, Yangtze Memory Technologies Co, Seagate Technology, Kingston Technology.

What is the projected CAGR for the market?

-> The market is projected to grow at a CAGR of 16.0% during the forecast period.

What are the primary applications driving demand?

-> Demand is driven by high‑performance computing (HPC), cloud infrastructure, AI server systems, hyperscale cloud providers, enterprise data centers, and telecom infrastructure.

What advantages does EDSFF NVMe SSD offer over legacy formats?

-> It provides improved thermal performance, higher storage density, better airflow design, and easier serviceability compared with traditional 2.5‑inch U.2 SSDs.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...