Laser Chip COS (Chip on Submount) Equipment Market Insights

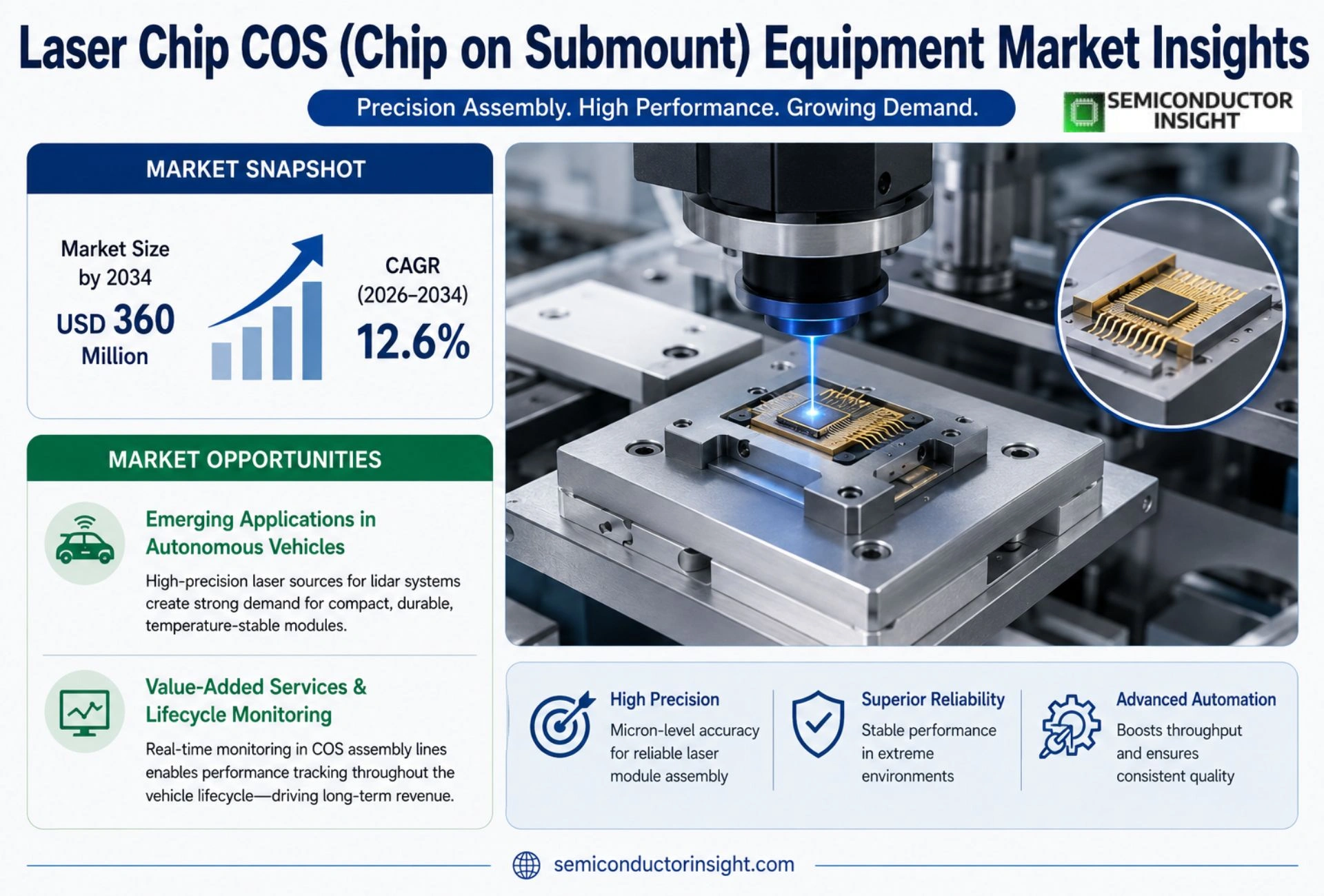

Global Laser Chip COS (Chip on Submount) Equipment market size was valued at USD 121 million in 2025 it is expected to reach approximately USD 360 million by 2034, reflecting an implied CAGR of about 12.6% over the forecast horizon.

Laser chip COS equipment comprises high‑precision back‑end assembly systems used for attaching laser diodes, VCSELs, photodiodes, silicon‑photonics chips and high‑power laser chips onto submounts, carriers or heat sinks. The core function is to secure accurate optical‑axis placement while controlling thermal resistance and eliminating bonding voids. Typical toolsets integrate sub‑micron motion stages, dynamic vision inspection, die pick‑up mechanisms, flip‑chip or face‑up placement modules, force control loops, pulse or localized laser heating sources, eutectic soldering stations, epoxy dispensing units and post‑bond inspection cameras. Applications span optical communication device packaging, data‑center interconnect modules, LiDAR transceivers and high‑power industrial laser assemblies, serving manufacturers of lasers, photonic modules and advanced packaging houses.

MARKET DRIVERS

Rising Demand for High‑Performance Photonic Modules

The surge in data‑center capacity and telecom operators’ shift toward wavelength‑division multiplexing have created a palpable need for compact, high‑power laser sources. Laser Chip COS (Chip on Submount) Equipment Market suppliers that can deliver tighter tolerances and higher reliability are seeing orders accelerate, because operators are unwilling to compromise on signal integrity.

Advancements in Integration and Packaging Techniques

Recent breakthroughs in adhesive‑free bonding and sub‑mount materials enable chip‑on‑submount configurations that surpass traditional flip‑chip solutions in thermal management. This technical edge translates into lower failure rates, prompting OEMs to allocate larger portions of their capex to next‑generation assembly lines.

➤ “Customers are rewarding manufacturers that can shrink footprint while preserving output power, turning integration capability into a decisive competitive advantage.”

When the cost of a missed launch far outweighs the incremental expense of adopting newer laser chip equipment, firms accelerate procurement cycles, reinforcing the upward momentum of the sector.

MARKET CHALLENGES

Cost Sensitivity and Capital Intensity

Deploying Laser Chip COS equipment entails significant upfront investment in precision optics, clean‑room environments, and skilled technicians. For midsize manufacturers, the payback horizon can be limiting, especially when budget cycles are constrained by broader economic uncertainty.

Other Challenges

Supply Chain Constraints

The scarcity of high‑purity sub‑mount wafers and specialty laser diodes creates bottlenecks that ripple through production schedules. Even minor delays in component delivery can force manufacturers to idle expensive equipment, eroding margin potential.

MARKET RESTRAINTS

Regulatory Compliance and Safety Standards

Stringent laser safety classifications and export‑control regimes impose additional testing and certification steps. Companies that lack a dedicated compliance team face longer time‑to‑market, which diminishes the attractiveness of scaling production quickly.

Compliance documentation also increases overhead for smaller players, limiting the pool of viable entrants and reinforcing the dominance of established firms with dedicated regulatory affairs groups.

MARKET OPPORTUNITIES

Emerging Applications in Autonomous Vehicles

Autonomous driving systems rely on lidar arrays that demand high‑precision laser sources in a compact form factor. The need for durable, temperature‑stable modules opens a niche where Laser Chip COS equipment can deliver custom‑engineered solutions that differentiate vehicle manufacturers.

Suppliers that integrate real‑time monitoring sensors into the COS assembly line can offer value‑added services, allowing automotive OEMs to track performance metrics throughout the vehicle’s lifecycle, thereby creating a new revenue stream beyond the initial sale.

Laser Chip COS (Chip on Submount) Equipment Market Trends

Shift Toward Integrated Photonic Packaging Solutions

Manufacturers are increasingly consolidating back‑end functions into single, high‑precision platforms that can handle everything from die pick‑up to post‑bond inspection. The move is prompted by the need to keep optical‑axis alignment within sub‑micron tolerances while also limiting thermal resistance for high‑power laser chips. Equipment that couples pulse‑laser heating with dynamic vision recognition now delivers placement accuracy of ±1.5 µm and cycle times that hover between six and ten seconds, a performance envelope that directly translates into higher line yields. Customers such as silicon‑photonics foundries and data‑center optoelectronic module assemblers are demanding this level of integration because it reduces hand‑offs, simplifies statistical process control, and shortens time‑to‑volume for emerging VCSEL and LiDAR modules. Consequently, vendors that can bundle eutectic bonding, epoxy stamping, and automated loading into a unified chassis are securing the most compelling contracts.

Other Trends

Emergence of Domestic Equipment Suppliers in Asia

Chinese firms are transitioning from generic die‑attach solutions to platforms explicitly engineered for laser‑chip packaging. Companies such as Bozhon, Microview, and Lieqi list COS‑specific capabilities on their product pages, indicating a strategic pivot toward optical‑communication‑grade performance. Their offerings often prioritize modular fixture design, allowing rapid switch‑over between P‑side‑down laser diodes and VCSEL arrays without extensive re‑calibration. While absolute market share data remain undisclosed, anecdotal reports suggest that regional OEMs are beginning to source these domestically produced systems to lower total ownership cost and to align with national policies favoring local technology adoption. This trend introduces a new competitive dynamic that pressures established European and Japanese players to differentiate on advanced motion control, active alignment, and integrated test‑and‑sort modules rather than solely on price.

Increasing Emphasis on Process Traceability and Automation

The downstream value chain now expects full‑traceable data streams that capture temperature profiles, bond‑force curves, and inspection imagery for each individual die. Vendors that embed secure logging and analytics within their control software are enabling customers to meet stringent quality‑assurance requirements for high‑volume data‑center interconnects and automotive LiDAR systems. This shift toward data‑driven manufacturing not only improves defect detection but also creates opportunities for service revenue through predictive maintenance and remote process optimisation. In practice, the ability to deliver a turnkey line—combining placement, heating, testing, and sorting—has become a decisive factor when enterprises evaluate capital investment in Laser Chip COS (Chip on Submount) Equipment market.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive Overview of the Global Laser Chip COS Equipment Market

The market is anchored by a small cadre of manufacturers that combine ultrahigh‑precision motion control with integrated thermal‑management modules. ASMPT Ltd. (through its AMICRA line) sets the benchmark with ±1.5 µm placement accuracy, sub‑10 second cycle times, and a suite of post‑bond inspection tools that enable high‑volume silicon‑photonics and VCSEL packaging. Its platform’s ability to switch seamlessly between eutectic soldering, epoxy stamping, and localized laser heating gives it a decisive edge in serving both data‑center transceiver makers and automotive LiDAR suppliers. Mycronic AB complements the tier‑one segment by offering parallel‑processing die bonders that accelerate tool changeover and support multi‑die sequencing, a capability increasingly demanded by contract manufacturers that juggle heterogeneous optical‑module portfolios.

Beyond the two leaders, a constellation of niche players is expanding the functional envelope of COS equipment. Palomar Technologies supplies a dedicated P‑side‑down laser‑diode attachment system that excels in high‑power fiber‑laser pump modules, while ficonTEC Service GmbH focuses on active‑alignment optics and integrated electro‑optical testing, positioning it well for research‑driven pilot lines. European specialists such as Dr. Tresky AG and Finetech GmbH & Co. KG deliver highly configurable platforms for custom bonding recipes, and SET Corporation adds automated loading/unloading solutions that improve overall line uptime. Asian entrants—including Shibuya Corporation, Toray Engineering, Bozhon Precision, Microview Intelligent Packaging, Suzhou Lieqi Intelligent Equipment, and FitTech—are leveraging cost‑effective engineering to capture domestic optical‑module contracts, gradually narrowing the technology gap with their Western counterparts.

List of Key Laser Chip COS Equipment Companies Profiled

- ASMPT Ltd.

- Mycronic AB

- Palomar Technologies, Inc.

- ficonTEC Service GmbH

- Dr. Tresky AG

- Finetech GmbH & Co. KG

- SET Corporation SA

- Shibuya Corporation

- Toray Engineering Co., Ltd.

- Bozhon Precision Industry Technology Co., Ltd.

- Microview Intelligent Packaging Technology (Shenzhen) Co., Ltd.

- Suzhou Lieqi Intelligent Equipment Co., Ltd.

- FitTech Co., Ltd.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Fully Automatic

|

| By Application |

|

Optical Communication Module Packaging

|

| By End User |

|

Optical‑Module Assemblers

|

| By Bonding Process |

|

Eutectic (AuSn) Bonding

|

| By Heating Method |

|

Localized Laser Heating

|

Regional Analysis: Laser Chip COS (Chip on Submount) Equipment Market

Asia‑Pacific

Fab operators are prioritising equipment that supports sub‑10 µm alignment tolerances, allowing laser sources to be positioned with unprecedented precision. Vendors offering real‑time interferometric feedback are seeing higher uptake, as manufacturers seek to lock in repeatability across high‑volume runs.

The region’s dense network of component vendors enables just‑in‑time delivery of specialty optics and bonding agents. This logistical advantage has encouraged equipment makers to adopt modular designs that can be reconfigured swiftly in response to customer specifications.

Government programmes in Japan and Singapore that earmark funds for advanced photonics manufacturing are fostering collaborative R&D. These initiatives lower entry barriers for smaller players aiming to commercialise niche laser‑on‑submount solutions.

Established equipment giants are encountering nimble startups that leverage AI‑driven process control. The resulting rivalry is accelerating feature releases, particularly in automated defect detection and adaptive laser power modulation.

North America

In North America, Laser Chip COS (Chip on Submount) Equipment segment is anchored by a cluster of R&D centers focused on high‑power laser integration for defense and data‑center applications. OEMs are seeking platforms that can accommodate both silicon‑photonic and compound‑semiconductor substrates, reflecting a diversification of end‑use cases. While the market size lags the Asia‑Pacific zone, the willingness to invest in proprietary tooling and long‑term service contracts creates a premium environment for suppliers that can prove reliability under stringent qualification regimes.

Europe

European manufacturers are channeling resources into laser‑chip‑on‑submount solutions that align with strict environmental standards. The emphasis on energy‑efficient processes has spurred demand for equipment that minimizes waste heat and leverages recyclable bonding materials. Collaborative projects funded by the EU’s Horizon initiatives are also encouraging cross‑border technology transfer, allowing firms to pool expertise in precision optics and advanced metrology.

South America

South American markets are in an early adoption phase, with a handful of regional foundries experimenting with laser‑based bonding to improve device miniaturisation. Industry observers note that the primary barrier remains limited access to high‑precision alignment tools, prompting local players to partner with overseas equipment providers for technology licensing. As the automotive sector expands its reliance on Lidar and optical sensing, demand for reliable COS equipment is expected to grow steadily.

Middle East & Africa

The Middle East & Africa region is witnessing nascent interest driven by telecom infrastructure upgrades and emerging smart‑city projects. Investors are attracted to the prospect of integrating laser‑chip assemblies into high‑capacity fiber‑optic backbones. However, the scarcity of skilled technicians and the need for localized after‑sales support pose challenges that equipment manufacturers must address through training programmes and remote diagnostics.

Report Scope

This market research report provides a comprehensive analysis of the Laser Chip COS (Chip on Submount) Equipment Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Laser Chip COS (Chip on Submount) Equipment Market?

-> Laser Chip COS (Chip on Submount) Equipment Market was valued at USD 121 million in 2025 and is expected to reach USD 284 million by 2032, representing a CAGR of 12.6% during the forecast period.

Which key companies operate in Laser Chip COS (Chip on Submount) Equipment Market?

-> Key players include ASMPT Ltd, Mycronic AB, Palomar Technologies, Inc., ficonTEC Service GmbH, Finetech GmbH & Co. KG, SET Corporation SA, Shibuya Corporation, Bozhon Precision Industry Technology Co., Ltd., Microview Intelligent Packaging Technology (Shenzhen) Co., Ltd., Suzhou Lieqi Intelligent Equipment Co., Ltd.

What are the key growth drivers?

-> Key growth drivers include upgrades in optical‑communication speeds, expansion of data‑center optical interconnects, increasing complexity of silicon‑photonics packaging, rising demand for VCSEL and LiDAR sensing devices, and continuous iteration of high‑power industrial laser modules.

Which region dominates the market?

-> Asia‑Pacific leads the market, driven by strong manufacturing bases in China, Japan, and South Korea, while Europe remains a significant but slower‑growing region.

What are the emerging trends?

-> Emerging trends include high‑precision eutectic bonding, active optical alignment, silicon‑photonics volume packaging, turnkey line‑delivery solutions, and increasing domestic substitution in key regions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...