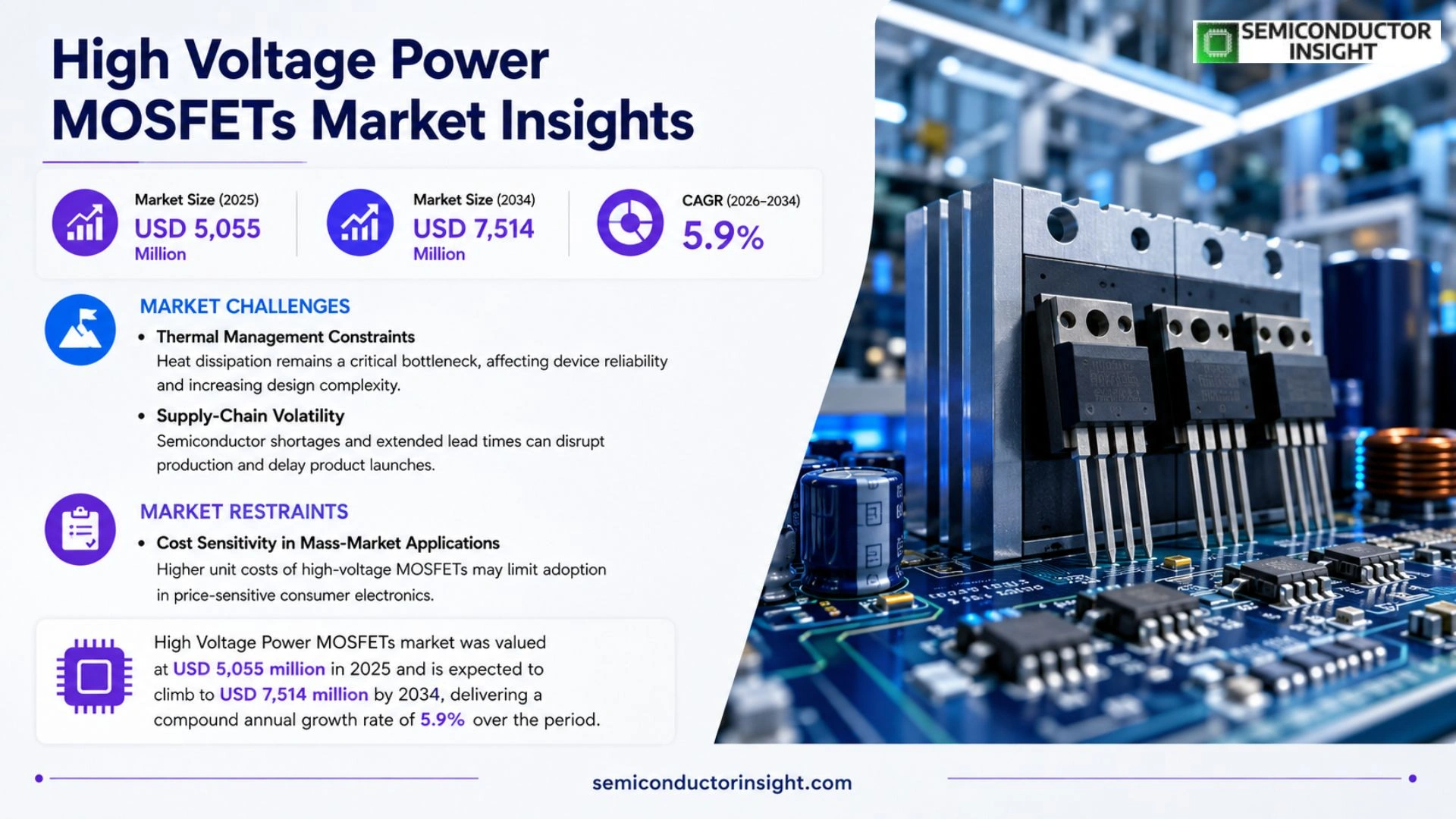

High Voltage Power MOSFETs Market Insights

High Voltage Power MOSFETs market was valued at USD 5,055 million in 2025 and is expected to climb to USD 7,514 million by 2032, delivering a compound annual growth rate of 5.9 % over the period.

High Voltage Power MOSFETs are discrete power‑switching devices placed on high‑voltage DC or rectified buses to enable high‑frequency switching, improve energy transfer efficiency and reduce thermal loss. Typical silicon devices cover a voltage span from 400 V up to 1 700 V, with Super‑Junction architecture now dominant alongside Planar and Quasi‑Plane‑Junction variants.

The expansion is anchored in simultaneous efficiency pushes across SMPS, PFC, server power supplies and emerging renewable‑energy converters; regulatory programs such as the U.S. DOE power‑supply standards and the EU’s updated ecodesign rules reinforce demand. Leading suppliers,including Infineon, onsemi and ROHM,continue to broaden voltage coverage and package options to meet these system‑level requirements.

MARKET DRIVERS

Electrification of Transportation

Automakers are redesigning power‑train architectures to accommodate higher system voltages, which pushes the demand for robust high‑voltage switching devices. The shift toward 400‑V and 800‑V platforms reduces conductor losses and shortens charging times, making High Voltage Power MOSFETs Market a pivotal component in next‑generation electric vehicles. OEMs are therefore prioritising suppliers that can deliver devices with low on‑resistance and fast recovery characteristics.

Growth of Renewable Energy Inverters

Grid‑scale solar and wind installations increasingly rely on multi‑megawatt inverters that operate at elevated voltages to improve efficiency. The higher voltage architecture permits smaller transformer sizes and lower overall system weight, directly benefiting the deployment of High Voltage Power MOSFETs Market solutions. Manufacturers that offer silicon‑carbide (SiC) MOSFETs with superior thermal performance are gaining traction among inverter producers seeking to meet tighter efficiency standards.

➤ “Design engineers are now optimizing for voltage‑tier consolidation, which elevates the strategic importance of high‑voltage MOSFETs across automotive and renewable sectors.”

Concurrently, data‑center power supplies are embracing 400‑V and 800‑V rail designs to accommodate higher density computing loads. This evolution reduces the number of series‑connected devices, simplifying board layouts and cutting BOM costs. Companies that can guarantee reliability at these stress levels stand to capture a growing slice of High Voltage Power MOSFETs Market.

MARKET CHALLENGES

Thermal Management Constraints

Despite advances in device architecture, dissipating heat from high‑voltage MOSFETs remains a critical bottleneck. Excessive thermal rise can erode lifetime and trigger premature failure, especially in compact automotive modules. Designers are forced to allocate additional copper area or implement advanced cooling techniques, which offsets some of the cost advantages of higher voltage operation.

Other Challenges

Supply‑Chain Volatility

Global semiconductor shortages have heightened lead times for silicon and SiC wafers. Manufacturers that lack diversified sourcing strategies may experience production delays, hampering their ability to meet the rising demand in automotive and renewable segments.

In addition, regulatory compliance for automotive safety standards imposes rigorous qualification cycles. The time‑intensive certification process can deter fast‑moving entrants and limit the speed at which new high‑voltage MOSFET designs reach the market.

MARKET RESTRAINTS

Cost Sensitivity in Mass‑Market Applications

While high‑voltage devices deliver efficiency gains, their unit price remains higher than traditional low‑voltage counterparts. For consumer‑grade electronics that prioritize cost over marginal performance uplift, manufacturers may opt for cheaper alternatives, constraining the overall penetration rate of High Voltage Power MOSFETs Market.

Reliability Concerns in Harsh Environments

Industrial equipment operating in extreme temperatures or high‑radiation zones demands devices with proven robustness. The current generation of high‑voltage MOSFETs, while efficient, still faces reliability scrutiny in such demanding settings, prompting some OEMs to retain legacy technologies until long‑term field data becomes more conclusive.

These cost and reliability considerations collectively temper the enthusiasm for immediate widescale adoption, especially in sectors where price elasticity is pronounced.

MARKET OPPORTUNITIES

Integration of SiC and GaN Platforms

The convergence of silicon‑carbide and gallium‑nitride technologies with traditional MOSFET designs opens pathways for devices that combine high voltage tolerance with ultra‑fast switching. Early adopters in aerospace and high‑performance computing are experimenting with hybrid solutions, suggesting a niche where High Voltage Power MOSFETs Market can expand beyond conventional automotive and renewable domains.

Emerging 48‑V Architecture in Commercial Vehicles

Commercial fleets are transitioning from 12‑V to 48‑V electrical systems to support higher‑power auxiliary functions such as electric power‑assist steering and advanced driver‑assist systems. This voltage shift creates a fresh demand tier for MOSFETs that can operate efficiently at mid‑range voltages, offering manufacturers a new revenue corridor within the broader High Voltage Power MOSFETs Market.

Finally, the proliferation of AI‑enabled edge devices requires power supplies that can maintain high efficiency under variable load conditions. Designing converters around high‑voltage MOSFETs reduces conversion stages, thereby simplifying power‑management architectures,a trend that could drive incremental market growth over the next five years.

High Voltage Power MOSFETs Market Trends

Shift Toward Super‑Junction Architectures

The dominant technology trajectory now centers on Super‑Junction devices, which combine low on‑resistance with compact silicon area. This balance reduces conduction loss while keeping gate charge modest, enabling designers to push switching frequencies higher without incurring prohibitive thermal penalties. As power converters migrate from planar to Super‑Junction structures, bill‑of‑materials costs fall because fewer devices are needed to meet the same power density targets. The move also eases thermal management in high‑frequency SMPS and PFC stages, a factor that directly influences enclosure size and cooling‑system design.

Other Trends

Application‑Driven Efficiency Push

Regulatory programs across the United States, Europe and emerging markets tighten permissible standby loss and raise minimum efficiency thresholds for external power supplies. Manufacturers of servers, telecom infrastructure, and industrial adapters are therefore compelled to select high‑voltage MOSFETs that can sustain low loss at elevated voltages. The combined effect is a broader adoption of 600‑800 V families in data‑center adapters and a noticeable uptick in 950‑V selections for motor‑drive inverters. Companies that can demonstrate a clear advantage in avalanche robustness and low reverse recovery charge will capture design wins where reliability margins are scrutinized.

Regional Portfolio Diversification

While legacy players from Europe, the United States and Japan continue to dominate premium‑segment platforms, Asian manufacturers are expanding their offerings into the mainstream 400‑1000 V range with localized packaging options. This shift blurs traditional supply‑chain boundaries, as system integrators increasingly source MOSFET families that align with regional cost structures and manufacturing footprints. The emerging pattern suggests a dual‑track market: high‑end Super‑Junction devices for server and telecom power modules, and a parallel stream of cost‑optimized parts serving consumer electronics and emerging renewable‑energy converters. For incumbent vendors, the strategic implication is clear – reinforcing global platform consistency while tailoring package selections to regional preferences will be essential to retain market share.

COMPETITIVE LANDSCAPE

Key Industry Players

High‑Voltage Power MOSFETs: Competitive Dynamics and Market Structure

Infineon dominates the upper‑end segment by leveraging its broad Super‑Junction portfolio that spans 400 V to 950 V with a rich selection of packages. The company’s emphasis on low RDS(on) and robust avalanche capability has entrenched its position in server‑grade power supplies and industrial converters, where reliability tolerances are stringent. Geographic analysis shows a tri‑regional balance: European and U.S. firms command premium‑price niches, while Japanese players retain a strong foothold in automotive and telecom equipment. This distribution forces newcomers to specialize either in cost‑effective 600 V‑800 V devices or in niche features such as ultra‑low gate charge for high‑frequency SMPS topologies.

Beyond the headline leaders, a constellation of specialized manufacturers fuels product diversity. onsemi stresses its SupreMOS line, targeting PFC stages with exceptionally low gate charge, whereas ROHM’s PrestoMOS family balances conduction loss against fast recovery for lighting and motor‑drive applications. Fuji Electric persists with a Quasi‑Plane‑Junction approach that delivers low noise and strong dv/dt control, appealing to inverter markets. STMicroelectronics, Vishay, and Toshiba each operate multi‑voltage families that serve both consumer adapters and data‑center modules. Smaller Asian firms,including PANJIT, LRC, JSCJ, Yangjie, Leshan Radio, and Jiangsu Changjing,are expanding their Super‑Junction portfolios to capture the 600 V‑800 V mainstream, often coupling product launches with regional distribution agreements. Their rapid productization signals a shift from pure fab‑only operations toward full‑scale platform strategies.

List of Key High Voltage Power MOSFETs Companies Profiled

- Infineon Technologies AG

- onsemi

- ROHM Semiconductor

- Fuji Electric

- STMicroelectronics

- Vishay Intertechnology

- Toshiba

- Renesas Electronics Corp.

- Alpha and Omega Semiconductor Limited

- Diodes Incorporated

- Shindengen Electric Manufacturing Co., Ltd.

- KEC Corporation

- Magnachip Semiconductor Corporation

- PANJIT International Inc.

- Yangzhou Yangjie Electronic Technology Co., Ltd.

- Leshan Radio Company, Ltd.

- Jiangsu Changjing Electronics Technology Co., Ltd.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Super Junction MOSFET dominates the technology landscape because it delivers:

|

| By Application |

|

Primary‑side conversion (SMPS & PFC) is the leading application segment because it:

|

| By End User |

|

Server & Telecom Power Supplies emerge as the strongest end‑user because they:

|

| By Technology Trend |

|

Thermal‑optimized packaging is gaining prominence as it:

|

| By Market Driver |

|

Energy‑efficiency regulations are the primary catalyst because they:

|

Regional Analysis: High Voltage Power MOSFETs Market

North America

The automotive sector in North America has accelerated its shift toward electric drivetrains, demanding MOSFETs capable of handling 600 V and above. OEMs prioritize devices with low switching loss to extend vehicle range, prompting suppliers to tailor wafer‑scale processes for higher voltage ratings. This pressure expands design windows for power‑train engineers, fostering a cascade of ancillary component innovation.

Industrial manufacturers across the United States and Canada are retrofitting high‑capacity motor drives with high‑voltage MOSFETs to meet efficiency mandates. The transition from insulated‑gate bipolar transistors to MOSFETs reduces thermal footprints and simplifies gate drive circuitry. As a consequence, equipment vendors can offer modular solutions that shorten time‑to‑market, sharpening competitive advantage.

Silicon‑carbide research initiatives, backed by federal grants and private venture capital, have lowered the cost barrier for wide‑bandgap devices. North American fabs are integrating SiC layers onto conventional MOSFET platforms, delivering superior breakdown voltage and thermal conductivity. Early adopters in aerospace and renewable‑energy sectors report measurable gains in power density, prompting broader market curiosity.

Recent disruptions in trans‑Pacific logistics have motivated North American manufacturers to diversify sourcing and invest in domestic wafer fab extensions. Partnerships between semiconductor firms and regional utilities secure stable power for cleanroom environments, while government incentives encourage on‑shoring of critical components. This strategic reshoring reduces lead times and insulates the region from geopolitical volatility.

Europe

European manufacturers are navigating a regulatory landscape that emphasizes EU Green Deal objectives, driving demand for high‑efficiency power conversion. Automotive allies in Germany and France adopt high‑voltage MOSFETs to satisfy stringent emission standards, while the Nordic region leverages the technology in offshore wind inverters. However, fragmented supply chains across the continent create pressure to harmonize standards, prompting consortia to develop common design libraries. The net effect is a cautious yet steady uptake, with OEMs balancing performance gains against the cost premium of advanced devices. High Voltage Power MOSFETs Market thus reflects Europe’s blend of ambition and pragmatic execution.

Asia‑Pacific

Asia‑Pacific presents a contrasting pace, with China’s aggressive electrification roadmap and India’s emerging renewable‑energy capacity fueling a surge in MOSFET demand. Local fabs are scaling production to meet volume requirements for consumer electronics and electric‑two‑wheelers, yet quality concerns persist, prompting manufacturers to source mature devices from established suppliers. Japan’s automotive giants continue to refine high‑voltage architectures for next‑generation EVs, reinforcing a premium market segment. High Voltage Power MOSFETs Market in this region is defined by divergent growth pathways that reward flexible product portfolios capable of addressing both high‑volume, cost‑sensitive applications and high‑performance niches.

South America

In South America, Brazil’s expanding renewable‑energy projects and Mexico’s growing automotive assembly lines create pockets of opportunity for high‑voltage MOSFETs. Infrastructure constraints and intermittent power grids motivate utility operators to adopt efficient conversion solutions, where MOSFETs improve reliability under fluctuating voltage conditions. Nevertheless, limited local semiconductor manufacturing capacity forces reliance on imports, exposing the market to currency volatility. Stakeholders are therefore focusing on strategic partnerships with North American distributors to secure supply while advocating for regional fab incentives. These dynamics shape High Voltage Power MOSFETs Market across the continent.

Middle East & Africa

The Middle East & Africa region leverages abundant solar‑energy installations, where high‑voltage MOSFETs are integral to inverter designs that interface with large‑scale photovoltaic farms. United Arab Emirates and Saudi Arabia spearhead projects that demand robust devices capable of withstanding harsh temperatures. At the same time, emerging industrial zones in South Africa seek efficient motor‑drive solutions for mining operations. The market’s growth is tempered by a modest domestic semiconductor ecosystem, leading to a reliance on OEMs from Europe and North America. Consequently, regional players are negotiating long‑term supply agreements to mitigate lead‑time risks and align with sustainability commitments within High Voltage Power MOSFETs Market.

Report Scope

This market research report provides a comprehensive analysis of the High Voltage Power MOSFETs Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of High Voltage Power MOSFETs Market?

-> High Voltage Power MOSFETs Market was valued at USD 5,055 million in 2025 and is expected to reach USD 7,514 million by 2032 with a CAGR of 5.9% during the forecast period.

Which key companies operate in High Voltage Power MOSFETs Market?

-> Key players include STMicroelectronics, Vishay, Littelfuse, Toshiba, Fuji Electric, Infineon, onsemi, ROHM, Renesas Electronics, Alpha and Omega Semiconductor Limited, Diodes Incorporated, Shindengen Electric Manufacturing Co., Ltd., KEC Corporation, Magnachip Semiconductor Corporation, PANJIT International Inc., Yangzhou Yangjie Electronic Technology Co., Ltd., Leshan Radio Company, Ltd., Jiangsu Changjing Electronics Technology Co., Ltd..

What are the key growth drivers?

-> Key growth drivers include rising efficiency standards for external power supplies (U.S. DOE, EU ecodesign), increasing demand for high‑efficiency adapters, chargers, server and telecom power supplies, expansion of industrial and new‑energy power applications, and the broader push for higher power density and lower standby loss across multiple end‑markets.

Which region dominates the market?

-> Asia-Pacific holds the largest market share, driven by strong manufacturing capabilities and rapid adoption of high‑voltage MOSFETs in consumer electronics, data‑center, and emerging new‑energy applications, while North America and Europe remain important competitive hubs.

What are the emerging trends?

-> Emerging trends include the shift toward Super Junction architectures for lower RDS(on) and higher switching speed, integration of low‑Qg and low‑Qrr designs, focus on avalanche ruggedness and EMI control, and the growing importance of AI‑driven power‑supply solutions and renewable‑energy power conversion systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...