Compute-in-Memory AI Accelerator Chips Market Insights

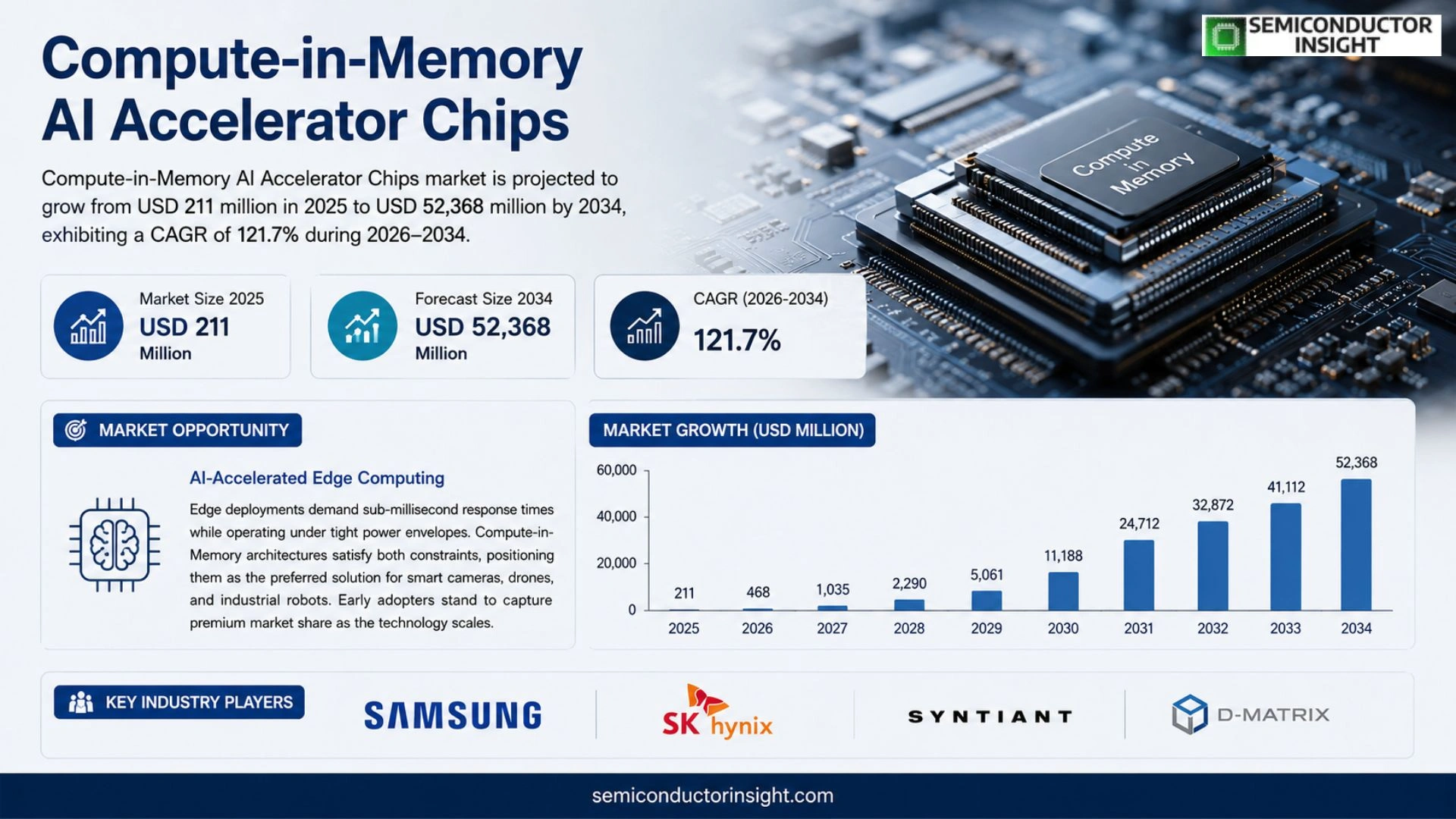

Global Compute-in-Memory AI Accelerator Chips market size was valued at USD 211 million in 2025. The market is projected to grow from USD 211 million in 2025 to USD 52,368 million by 2034, exhibiting a CAGR of 121.7% during the forecast period.

Compute-in-Memory (CIM) AI Accelerator Chips are specialized hardware accelerators that perform AI computations directly within or adjacent to memory arrays. By executing multiply‑accumulate (MAC) operations where data resides, these chips drastically cut data movement, lower power consumption, reduce latency, and ease memory‑bandwidth constraints typical of von Neumann architectures. Implementations leverage SRAM, DRAM or emerging non‑volatile memories such as ReRAM and MRAM, positioning them as a cornerstone for energy‑efficient edge AI and next‑generation computing platforms.

The market is gaining momentum because semiconductor manufacturers are prioritizing on‑chip intelligence for IoT devices, autonomous systems and data‑center inference workloads. Moreover, rising demand for low‑power AI inference drives adoption across automotive and consumer electronics sectors. Leading firms,including Samsung, SK Hynix, Syntiant, D‑Matrix, Mythic, Graphcore, EnCharge AI and Axelera AI,are expanding product portfolios and announcing joint development programs aimed at scaling CIM technologies for both edge and cloud environments.

MARKET DRIVERS

Rising Edge AI Workloads

The proliferation of transformer‑based models and real‑time inference at the network edge has forced chip designers to rethink the memory‑compute boundary. By embedding arithmetic units directly within SRAM or emerging non‑volatile arrays, Compute-in-Memory AI Accelerator Chips shave off latency that traditional von Neumann pipelines cannot eliminate. This architectural shift is turning latency‑sensitive services,such as autonomous navigation and video analytics,into prime adopters.

Energy‑Efficiency Imperative

Data‑center operators are grappling with power caps that limit expansion despite soaring demand. In‑memory acceleration reduces data movement by up to 70 %, translating into measurable reductions in PUE (Power Usage Effectiveness). Customers are therefore willing to pay a premium for chips that deliver comparable throughput with a fraction of the energy budget, accelerating commercial rollout.

➤ “Integrating compute and storage at the silicon level is no longer an academic exercise; it is the primary lever for cost‑controlled AI scaling.”

Beyond pure performance, the technology stack is maturing,design tools, verification suites, and fabrication processes now support large‑scale integration of analog and digital compute elements. This ecosystem readiness lowers entry barriers for system integrators, prompting a wave of product announcements across the Compute-in-Memory AI Accelerator Chips Market.

MARKET CHALLENGES

Design Complexity and Validation

Embedding arithmetic logic inside memory cells multiplies the verification matrix. Designers must balance analog noise, retention characteristics, and timing closure simultaneously, a task that stretches traditional EDA workflows. The longer validation cycles raise upfront costs, deterring smaller fabless players from entering the space.

Other Challenges

Manufacturing Yield Sensitivity

Process variations that are acceptable for conventional DRAM become critical when compute functions share the same substrate. Yield loss translates directly into higher per‑chip pricing, which can stall adoption in price‑sensitive segments such as consumer IoT.

MARKET RESTRAINTS

Standardization Gaps

Unlike mature CPU or GPU ecosystems, the Compute-in-Memory AI Accelerator Chips arena lacks universally accepted interconnect and programming standards. Integrators must navigate a fragmented set of APIs, which slows system‑level integration and raises total cost of ownership.

The absence of clear benchmark suites hampers objective performance comparison. Vendors frequently publish proprietary metrics that make side‑by‑side evaluation difficult for end‑users, reinforcing a cautious purchasing posture.

Regulatory scrutiny over emerging memory technologies,particularly those leveraging novel materials,adds another layer of uncertainty. Certification timelines can extend product launch windows, further constraining market momentum.

MARKET OPPORTUNITIES

AI‑Accelerated Edge Computing

Edge deployments demand sub‑millisecond response times while operating under tight power envelopes. Compute‑in‑Memory architectures satisfy both constraints, positioning them as the preferred solution for smart cameras, drones, and industrial robots. Early adopters stand to capture premium market share as the technology scales.

Another fertile avenue lies in hybrid cloud‑edge orchestration. Service providers can offload inference bursts to in‑memory accelerators located at regional edge nodes, reducing backbone traffic and improving user experience. This model opens recurring revenue streams for chip manufacturers through licensing of runtime libraries and support services.

Finally, collaboration between memory manufacturers and AI chip designers is spawning turnkey modules that bundle memory‑compute blocks with standardized interfaces. Such co‑engineered solutions lower integration risk for OEMs, accelerating the diffusion of Compute-in-Memory AI Accelerator Chips across verticals ranging from healthcare imaging to autonomous logistics.

Compute-in-Memory AI Accelerator Chips Market Trends

Emergence of Edge AI Drives the Compute-in-Memory AI Accelerator Chips Market

Integrating arithmetic operations directly into memory arrays eliminates the costly shuttling of tensors between separate processor cores and DRAM banks. This architectural shift translates into markedly lower power draw and sub‑microsecond inference latency, attributes that are increasingly decisive for battery‑constrained devices such as smart cameras, wearables, and autonomous drones. Vendors are leveraging the reduction in bandwidth pressure to differentiate edge products that can run complex neural nets without overheating. At the same time, hyperscale data‑center operators are piloting in‑memory acceleration to cut the total cost of ownership for inference workloads that dominate served‑model traffic. The convergence of these forces is reshaping buying patterns: system integrators are requesting silicon that offers a balanced trade‑off between memory density and compute intensity, while firmware teams are revising software stacks to exploit near‑memory MAC primitives.

Other Trends

Architectural Diversification and Memory Technology Choices

Designers are no longer confined to a single memory class. SRAM‑based compute cells deliver deterministic timing and are favored for low‑latency edge modules, whereas DRAM‑centric approaches provide higher capacity for data‑intensive analytics at the cloud edge. Emerging non‑volatile memories such as ReRAM and MRAM add the possibility of retaining learned weights across power cycles, opening new business models around on‑device model updates. Companies are building modular IP blocks that can be tiled across these substrates, allowing OEMs to target a broader price spectrum without redesigning the entire accelerator. This flexibility reduces entry barriers for niche applications,industrial IoT sensors, for example,while still satisfying the performance envelope demanded by large‑scale AI service providers.

Competitive Landscape Consolidates Around Foundry Partnerships

Leading silicon producers,including Samsung, SK Hynix, and Graphcore,are deepening collaborations with advanced foundries to secure access to sub‑10‑nm process nodes that can host dense compute‑in‑memory arrays. These alliances accelerate time‑to‑market for custom AI accelerators and enable shared risk in the development of next‑generation memory materials. Smaller innovators such as Mythic and Syntiant are licensing these advanced nodes to differentiate their product portfolios, while also pursuing ecosystem lock‑in through proprietary development kits. The net effect is a market where scale, process technology, and ecosystem readiness converge to determine which designs achieve broad adoption, prompting investors to prioritize firms that can demonstrate both technological depth and strategic foundry alignment.

COMPETITIVE LANDSCAPE

Key Industry Players

Compute-in-Memory AI Accelerator Chips: Competitive Overview

The market is anchored by memory giants whose extensive wafer capacity and deep IP portfolios enable them to embed compute blocks directly into DRAM, SRAM, or emerging NVM arrays. Samsung leverages its front‑end process leadership to ship CIM‑enabled HBM modules that address data‑center inference at scale, while SK Hynix has accelerated its PIM roadmap through a series of joint ventures with AI chipset designers. Their ability to amortize R&D spend across consumer, automotive, and edge segments creates a high barrier to entry for newcomers. Consequently, the competitive hierarchy resembles a tiered structure: a small apex of integrated memory manufacturers, a middle tier of fabless AI specialists that partner with these fabs, and a broad base of niche innovators that focus on specific form factors or application niches.

Beyond the tiered leaders, a vibrant set of specialists is reshaping the value chain. Mythic and D‑Matrix have pursued analog‑in‑memory approaches that sidestep traditional digital pipelines, delivering ultra‑low‑power inference for battery‑constrained devices. Graphcore’s IPU platform, now extended with CIM extensions, competes on flexibility for research‑heavy workloads. EnCharge AI and Axelera AI differentiate through silicon that co‑optimizes neural‑network compilers with memory‑centric execution, targeting autonomous‑driving and robotics. Chinese innovators such as Hangzhou Zhicun (Witmem) Technology, Suzhou Yizhu Intelligent Technology, Shenzhen Reexen Technology, Beijing Houmo Technology, AistarTek, and Beijing Pingxin Technology are rapidly scaling production of SRAM‑based and NVM‑based CIM chips for domestic AI cloud services. Syntiant, meanwhile, remains focused on ultra‑compact edge processors that embed inference kernels inside micro‑memory blocks, a strategy that aligns with the explosion of IoT sensing nodes. Collectively these firms inject diversity into product form factors, pricing strategies, and ecosystem partnerships, forcing the incumbents to accelerate integration cycles and broaden software support.

List of Key Compute-in-Memory AI Accelerator Chips Companies Profiled

- Samsung

- SK Hynix

- Syntiant

- D‑Matrix

- Mythic

- Graphcore

- EnCharge AI

- Axelera AI

- Hangzhou Zhicun (Witmem) Technology

- Shenzhen Reexen Technology

- Beijing Houmo Technology

- AistarTek

- Beijing Pingxin Technology

- Suzhou Yizhu Intelligent Technology

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Near‑in‑memory Computation (PNM) is emerging as the most compelling type because it blends the immediacy of processing with minimal data movement, delivering:

|

| By Application |

|

Edge AI Devices dominate application focus due to the rising demand for on‑device intelligence, offering:

|

| By End User |

|

Consumer Electronics are the primary end‑user segment, driven by:

|

| By Memory Technology |

|

SRAM‑based CIM leads this category because it provides:

|

| By Performance Tier |

|

Low‑power Edge is the dominant tier, offering:

|

Regional Analysis: Compute-in-Memory AI Accelerator Chips Market

North America

Early engagements with edge‑compute platforms have highlighted the tangible latency improvements afforded by on‑chip memory compute. OEMs are experimenting with heterogeneous designs that embed AI accelerator cores directly within DRAM stacks, a move that reshapes board‑level architecture choices.

Strategic alliances between memory manufacturers and fab facilities are reducing time‑to‑market for custom compute‑in‑memory modules. These collaborations also mitigate the risk of component shortages that have previously hampered scaling efforts.

Private equity funds are allocating capital to niche players that demonstrate a clear path from prototype to volume production. The influx of financing accelerates design iterations and fosters a competitive ecosystem.

Government initiatives that reward energy‑efficient AI workloads are encouraging adoption in data‑center environments. Policy incentives are shaping procurement criteria, prompting vendors to showcase compute‑in‑memory capabilities.

Europe

European chip designers are leveraging strong research consortia to embed AI acceleration logic within high‑bandwidth memory modules. The region’s emphasis on sustainability fuels interest in architectures that lower power draw per inference, making compute‑in‑memory solutions attractive for smart‑grid and industrial IoT deployments. Collaborative standards bodies are also aligning on interface specifications, which eases integration for system integrators across the continent.

Asia‑Pacific

In the Asia‑Pacific, rapid growth of mobile AI applications and expansive manufacturing capabilities create a fertile ground for Compute-in-Memory AI Accelerator Chips Market expansion. Companies are capitalising on cost‑effective fabs to produce large‑volume memory‑centric chips, while local cloud providers experiment with edge nodes that process data directly within storage devices. The competitive pressure drives continuous iteration on chip density and thermal management techniques.

South America

South American markets are beginning to explore compute‑in‑memory technologies as part of broader digital transformation agendas. Telecom operators are piloting low‑latency AI inference at the network edge to support emerging 5G services, while academic partnerships generate localized design expertise. The region’s emerging ecosystems benefit from technology transfer programs that lower entry barriers for domestic manufacturers.

Middle East & Africa

The Middle East & Africa region is witnessing nascent interest driven by sovereign wealth funds that seek to diversify into high‑tech hardware. Early deployments focus on data‑center efficiency improvements for oil‑and‑gas analytics and climate‑monitoring platforms. Partnerships with global silicon vendors provide the necessary know‑how to accelerate adoption, while regional policy frameworks increasingly favour AI‑centric infrastructure projects.

Report Scope

This market research report provides a comprehensive analysis of the Compute-in-Memory AI Accelerator Chips Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Compute-in-Memory AI Accelerator Chips Market?

-> Global Compute-in-Memory AI Accelerator Chips market is projected to grow from USD 211 million in 2025 to USD 52,368 million by 2034

Which key companies operate in Compute-in-Memory AI Accelerator Chips Market?

-> Key players include Samsung, SK Hynix, Syntiant, D-Matrix, Mythic, Graphcore, EnCharge AI, Axelera AI, Hangzhou Zhicun (Witmem) Technology, Suzhou Yizhu Intelligent Technology, among others.

What are the key growth drivers?

-> Key growth drivers include reduction of data movement leading to lower power consumption, decreased latency, alleviation of memory bandwidth bottlenecks, and the rising demand for energy‑efficient edge AI solutions.

Which region dominates the market?

-> Asia holds the largest market share, driven by strong investments in AI hardware in China, Japan, and South Korea.

What are the emerging trends?

-> Emerging trends include adoption of SRAM, DRAM, and emerging non‑volatile memories such as ReRAM and MRAM for CIM, and growing interest in near‑in‑memory computation (PNM) architectures for edge AI.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...