Thermoelectric Peltier Module Market Insights

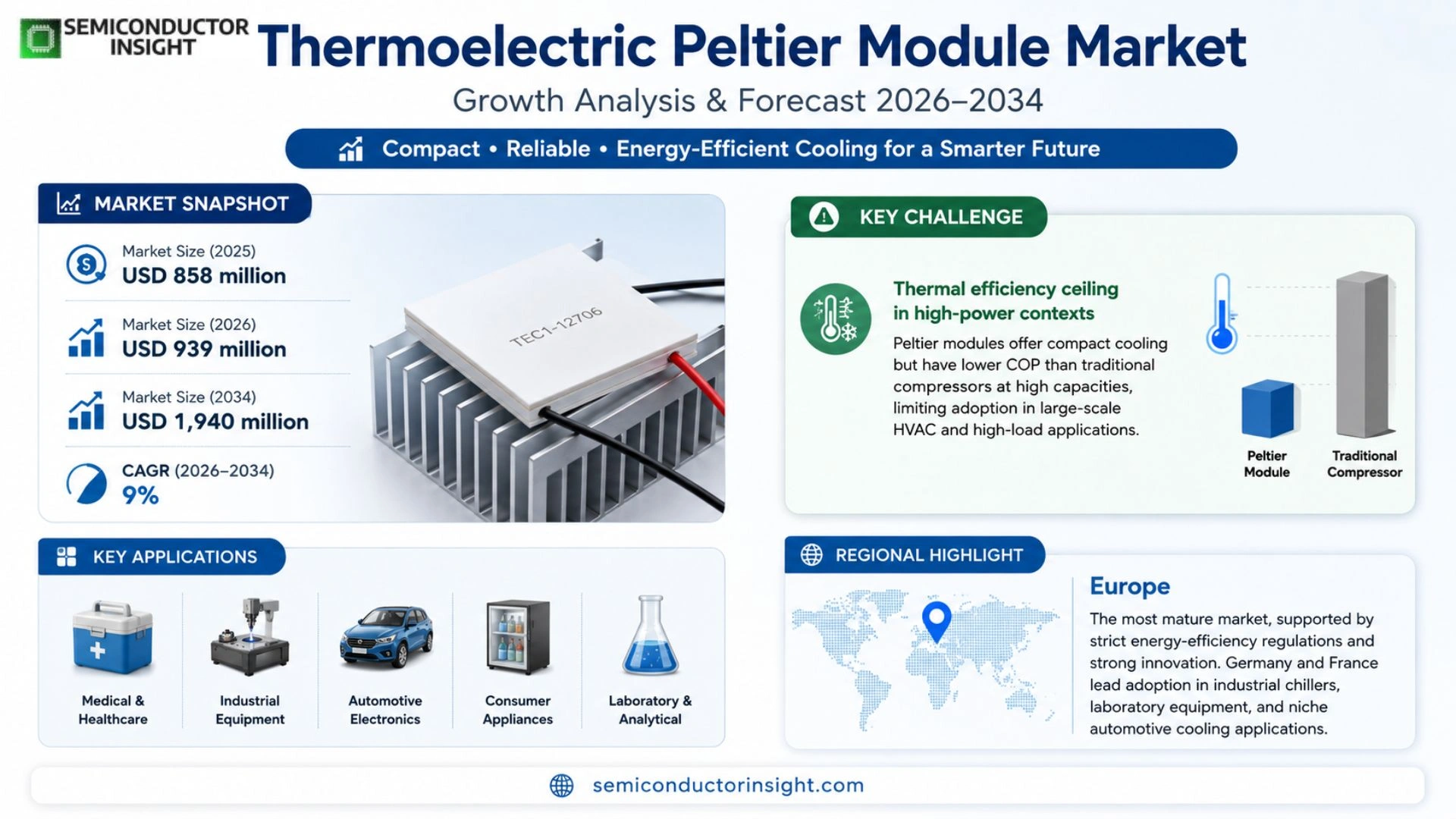

Thermoelectric Peltier Module market size was valued at USD 858 million in 2025.

The market is projected to grow from USD 939 million in 2026 to USD 1,940 million by 2034, exhibiting a CAGR of approximately 9 % during the forecast period.

A Thermoelectric Peltier Module is a solid‑state thermal‑management device that exploits the Peltier effect to deliver active cooling and precise temperature regulation.

Typically it comprises alternating p‑type and n‑type semiconductor couples bonded between ceramic substrates and equipped with electrodes and thermal interface layers.

When direct current passes through the couples, one side absorbs heat while the opposite side rejects it, enabling rapid temperature differentials without moving parts or refrigerants.

Key attributes include compact form factor, fast response time, reversible heating/cooling by polarity reversal, and low vibration,features that make these modules attractive for optical communication hardware, laser systems, semiconductor processing equipment, medical instrumentation, automotive thermal management, consumer electronics, industrial sensors, and aerospace/defense platforms.

The market momentum stems from several converging forces.

First, rising bandwidth demands in optical networking and AI‑driven data centers are pushing designers toward high‑density heat‑flux solutions where traditional fans or liquid coolers are impractical.

Second, automotive electrification,particularly battery thermal control and seat‑temperature systems,creates premium‑price opportunities for modules offering higher heat‑absorption efficiency.

Third, advances in bismuth‑telluride material processing and ceramic substrate reliability are lowering unit costs while extending cycle life.

Finally, strategic investments by established players such as Ferrotec, Kyocera and Coherent,combined with rapid capacity expansion among Chinese manufacturers,are tightening supply chains and fostering localized support structures.

These dynamics collectively underpin the sustained double‑digit growth trajectory anticipated through 2034.

MARKET DRIVERS

Solid‑state cooling adoption in consumer devices

Manufacturers of smartphones, wearables and compact refrigeration are replacing vapor‑compression components with Thermoelectric Peltier modules because they eliminate moving parts and enable precise temperature control. This shift reduces maintenance cycles and aligns with sustainability targets, prompting a measurable uptick in module orders.

Waste‑heat recovery initiatives across industry

Heavy‑duty processes in steel, glass and chemicals generate abundant low‑grade heat. Deploying Peltier devices to capture a fraction of that heat for power generation or localized cooling is attracting attention as firms seek to improve overall plant efficiency without major capital outlays.

➤ “When a system can convert 5‑7 % of waste heat into useful cooling, the ROI period shortens to under two years, a compelling proposition for asset‑intensive operators.”

The convergence of tighter emissions regulations and the falling price of advanced semiconductor materials creates a fertile environment for Thermoelectric Peltier Module Market to broaden its application base.

MARKET CHALLENGES

Thermal efficiency ceiling in high‑power contexts

Although Peltier technology excels at compactness, its coefficient of performance (COP) remains lower than that of traditional compressors when handling kilowatt‑scale loads. End‑users therefore hesitate to substitute for large‑scale HVAC, limiting market penetration in sectors that demand high‑capacity cooling.

Other Challenges

Supply‑chain volatility

The reliance on rare‑earth elements such as bismuth and tellurium subjects manufacturers to price swings and geopolitical risk, complicating long‑term cost forecasting for OEMs.

MARKET RESTRAINTS

Capital intensity versus perceived value

Investment decisions often weigh the higher upfront price of Thermoelectric modules against the incremental benefit of silent operation. In price‑sensitive markets, buyers frequently revert to legacy solutions, suppressing broader adoption until cost parity improves.

Lifecycle analysis frequently reveals that the modest energy‑saving advantage does not offset the initial expense for short‑duration applications, prompting manufacturers to limit module deployment to niche products.

Regulatory certification processes for safety and electromagnetic compatibility add another layer of complexity, especially for devices destined for medical or aerospace certification pathways.

MARKET OPPORTUNITIES

Electric‑vehicle cabin climate management

Automakers are integrating compact cooling modules to service seat‑level temperature zones without drawing heavily from the battery pack. This niche addresses consumer comfort expectations while preserving driving range, representing a high‑margin segment for module suppliers.

Data‑center operators are exploring edge‑node cooling where space constraints preclude traditional chillers. The ability of Peltier devices to provide localized temperature regulation enables higher equipment density and reduces overall energy consumption.

Aerospace manufacturers are evaluating thermoelectric solutions for avionics thermal control, where weight and vibration resistance are paramount. Early prototypes demonstrate that modest cooling capacity can be achieved without compromising aircraft performance.

Thermoelectric Peltier Module Market Trends

Shift Toward High‑Precision Thermal Management

The demand profile for Thermoelectric Peltier Module Market solutions is moving from generic consumer electronics toward applications that require tight temperature tolerance and rapid response. Optical communication links, laser systems, and semiconductor testing equipment now prioritize stability over sheer cooling capacity, prompting OEMs to opt for solid‑state devices that can deliver sub‑degree control without refrigerants. Simultaneously, automotive power‑train developers are integrating modules to manage battery pack heat and cabin seat temperature, leveraging the reversible heating capability to enhance occupant comfort while preserving energy efficiency. This migration reflects a broader industry push for miniaturization, low vibration, and localized heat removal in next‑generation AI servers and high‑density photonic networks.

Other Trends

Supply‑Side Realignment and Cost Competition

On the supply front, traditional high‑end material providers in Japan and Europe continue to dominate bismuth‑telluride sourcing, ensuring long cycle life and reliability certifications prized by aerospace and medical customers. Chinese manufacturers, however, have expanded single‑line capacities to approach one million units annually, driving gross margins toward the upper‑30 % range. This scale advantage translates into lower price points for standard‑grade modules, pressuring incumbents to differentiate through advanced packaging and extended reliability testing. The divergent cost structures are reshaping procurement strategies, with multinational system integrators splitting orders between premium‑grade suppliers for critical nodes and volume‑focused Chinese firms for peripheral cooling tasks.

Product Diversification and System Integration

Manufacturers are broadening their portfolios beyond isolated cooling blocks to complete thermal‑management subsystems that incorporate cold plates, liquid‑flow interfaces, and intelligent controllers. Recent launches highlight modules capable of sustaining 100 k thermal cycles, signaling a transition from pure cooling to hybrid heating‑cooling solutions that address battery thermal runaway and on‑demand heating in cold climates. Material innovation remains centered on Bi₂Te₃ alloys and refined ceramic substrates, yet the strategic emphasis is now on reducing parasitic power draw while maximizing heat‑flux density. For end‑users, these advances open pathways to embed active temperature regulation directly into compact devices, unlocking new product designs that were previously constrained by conventional compressor or heat‑pipe architectures.

COMPETITIVE LANDSCAPE

Key Industry Players

Thermoelectric Peltier Module Market – Competitive Overview

The high‑end segment continues to be anchored by firms that combine proprietary Bi2Te3‑based material expertise with deep relationships in optical, medical and aerospace applications. Ferrotec, Kyocera and Coherent dominate this tier by leveraging long‑standing reliability programs, extensive test infrastructure and a portfolio that stretches from single‑stage modules to rugged multi‑stage units capable of surviving over 100,000 thermal cycles. Their pricing power stems from consistent supply of high‑purity bismuth‑telluride alloys and tight process control, which translates into gross margins in the mid‑30 % range. The strategic focus of these leaders has shifted toward system integration,adding cold plates, temperature controllers and predictive diagnostics,allowing them to capture value beyond the raw module. This approach not only creates differentiation but also reinforces client lock‑in through turnkey thermal management solutions for data‑center AI servers and next‑generation laser platforms.

Parallel to the premium tier, a growing cohort of Chinese and European manufacturers is expanding capacity in standard‑grade TECs and customized form factors. Companies such as Guangdong Fuxin Technology, ARCTIC TEC, Z‑MAX, Zhejiang Wangu Semiconductor and Thermion have built vertically integrated supply chains that source bismuth‑telluride, copper‑clad laminates and ceramic substrates locally, thereby achieving cost structures that undercut imported equivalents by 15‑20 %. Their product lines emphasize modularity and rapid volume scaling, targeting consumer electronics, automotive seat heating and mid‑range communication equipment. The entrance of firms like Phononic and Tark Thermal Solutions, which blend material science with advanced packaging, introduces a middle ground where performance meets price, nudging traditional buyers toward diversified sourcing strategies.

List of Key Thermoelectric Peltier Module Companies Profiled

- Ferrotec

- KELK Ltd. (Komatsu)

- Coherent Corp

- Tark Thermal Solutions

- Kyocera

- Phononic

- Guangdong Fuxin Technology

- ARCTIC TEC

- KJLP

- Thermion Company

- Z‑MAX

- Zhejiang Wangu Semiconductor

- Xianghe Oriental Electronic

- Thermonamic Electronics

- TE Technology

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Single‑stage Type

|

| By Application |

|

Communication

|

| By End User |

|

Automotive Thermal Management

|

| By Package Geometry |

|

Standard Type

|

| By Cooling Capacity |

|

100W Above

|

Regional Analysis: Thermoelectric Peltier Module Market

Europe

German equipment producers are integrating Peltier modules into precision temperature‑controlled machining centers, lowering energy draw while improving process stability. The move reflects a broader industry push toward greener footprint metrics and tighter tolerances, prompting suppliers to develop customized module packages that align with CNC control software.

French consumer brands are exploring solid‑state cooling for high‑performance laptops and wearables, where silent operation and compact form factor matter. The transition is spurred by consumer demand for devices that stay cool under load without relying on noisy fans, opening opportunities for module miniaturization.

Italian and British automotive engineers are piloting Peltier‑based battery thermal‑management systems for electric vehicles, aiming to balance cooling efficiency with reduced part count. Early field trials indicate potential gains in charge‑rate consistency, prompting joint ventures with module manufacturers.

Scandinavian renewable‑energy firms are evaluating thermoelectric modules as passive heat exchangers within solar‑thermal collectors, where solid‑state reliability can extend service intervals. The approach aligns with regional sustainability targets and stimulates niche product development.

North America

In North America, adoption of thermoelectric Peltier technology is closely linked to defense‑related research and high‑end data‑center cooling. U.S. federal programs fund projects that replace conventional HVAC units with solid‑state alternatives, citing reduced acoustic signatures and finer temperature control. Canadian manufacturers, meanwhile, capitalize on the country’s strong materials‑science sector to produce high‑performance ceramic substrates, feeding a niche market for medical imaging equipment that demands precise thermal regulation. These dynamics encourage cross‑industry partnerships that accelerate module reliability improvements and foster a supply chain capable of scaling to enterprise‑level deployments.

Asia-Pacific

The Asia‑Pacific region presents a heterogeneous landscape where rapid electronics manufacturing coexists with emerging renewable‑energy initiatives. Chinese original‑design manufacturers are embedding Peltier modules into affordable consumer coolers, leveraging low‑cost production to test market acceptance. At the same time, Japanese firms lead in advanced module design for aerospace applications, where thermal stability under extreme conditions is non‑negotiable. Indian startups are experimenting with Peltier‑enabled portable refrigeration for last‑mile vaccine distribution, reflecting a public‑health driven demand for reliable cold‑chain solutions. The region’s blend of cost efficiency and high‑tech innovation makes it a crucible for both volume‑driven and premium‑segment growth.

South America

South American interest in thermoelectric Peltier modules centers on agricultural technology and remote monitoring equipment. Brazilian agritech companies are trialing solid‑state cooling for post‑harvest storage units, aiming to reduce spoilage in tropical climates without reliance on grid power. Argentine research institutes collaborate with European partners to develop low‑maintenance thermal sensors for mining operations, where ruggedness and minimal upkeep are paramount. These applications underscore a strategic shift toward self‑sufficient cooling solutions that can operate in regions with limited infrastructure, offering a pathway for module providers to enter emerging markets.

Middle East & Africa

In the Middle East and Africa, Thermoelectric Peltier Module Market is being shaped by extreme ambient temperatures and a growing emphasis on energy‑independent solutions. United Arab Emirates projects are integrating Peltier cooling into smart‑building façades to mitigate heat gain while maintaining aesthetic design. South African telecom operators are exploring solid‑state thermal management for base‑station equipment deployed in remote desert sites, where reliability outweighs cost considerations. The regional narrative revolves around leveraging thermoelectric technology to achieve climate resilience and operational continuity, prompting local investors to fund pilot programs that test long‑term durability under harsh conditions.

Report Scope

This market research report provides a comprehensive analysis of the Thermoelectric Peltier Module Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Thermoelectric Peltier Module Market?

-> Thermoelectric Peltier Module Market was valued at USD 858 million in 2025 and is expected to reach USD 1,617 million by 2032 with a CAGR of 9.4% during the forecast period.

Which key companies operate in Thermoelectric Peltier Module Market?

-> Key players include Ferrotec, KELK Ltd. (Komatsu), Coherent Corp, Tark Thermal Solutions, Kyocera, Phononic, Guangdong Fuxin Technology, ARCTIC TEC, KJLP, Thermion Company, Z-MAX, Zhejiang Wangu Semiconductor, Xianghe Oriental Electronic, Thermonamic Electronics, TE Technology, P&N Technology, AISIN Corporation, Sensor Controls Co., Ltd., Wakefield Thermal, Same Sky (formerly CUI Devices), TEC Microsystems GmbH, Peltron GmbH, Kryotherm Industries, Crystal Ltd, Liaoning Lengxin Technology, Thermoelectric New Energy Technology, Jianju Technology, Bi Sheng Semiconductor, Henan Hongchang Electronic, Wei County Zhongtian Electron Stock Cooperative, Beijing Xinyu Kaimeng Electronic Technology, Beijing Huimao Refrigeration Equipment, Hangzhou Aurin Cooling Device, Henan Guanjing Semiconductor Technology, and Hubei Sagreon New Energy Technology.

What are the key growth drivers?

-> Key growth drivers include the shift toward high‑precision temperature control applications such as optical modules, lasers, medical testing, automotive battery and seat temperature management, as well as rising demand from AI computing, high‑speed optical networking, and data‑center thermal management, which drive adoption of compact, efficient thermoelectric cooling solutions.

Which region dominates the market?

-> Asia dominates the market, driven primarily by China’s large‑scale manufacturing capacity and rapid expansion in standard and micro‑TEC production, while Japan and Europe retain strong positions in high‑end material supply and reliability‑focused applications.

What are the emerging trends?

-> Emerging trends include the integration of thermoelectric modules with cold plates, liquid‑cooling systems, and advanced temperature controllers, development of high heat‑flux, low‑power devices, and increasing deployment of TECs in AI servers, 800G/1.6T optical networking equipment, and next‑generation data‑center infrastructures.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...