Smart Electricity Meter Chip Market Insights

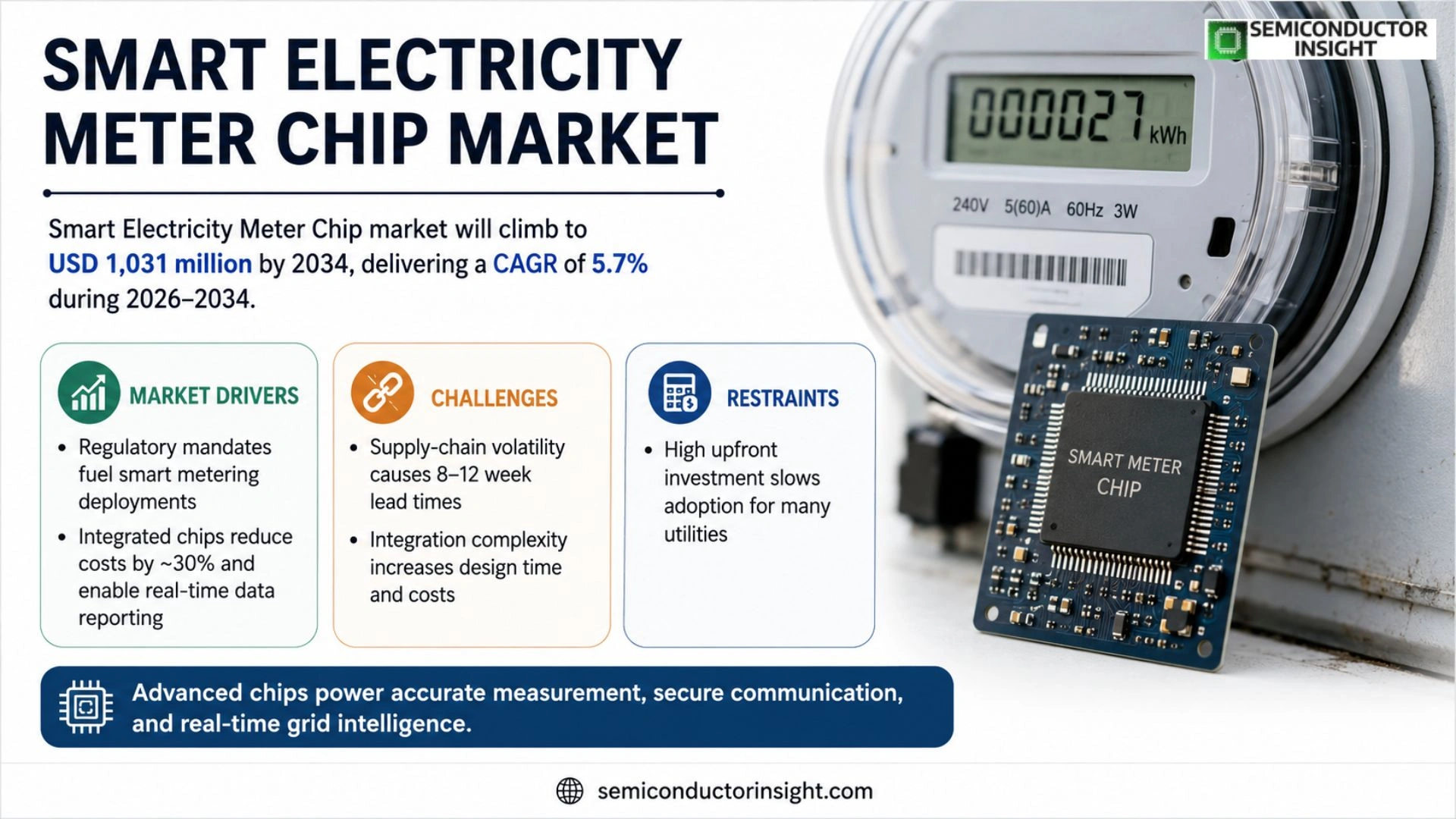

Global Smart Electricity Meter Chip market size was valued at USD 700 million in 2025 and will climb to USD 1,031 million by 2034, delivering a CAGR of 5.7 % over the forecast horizon.

A smart electricity meter chip is a highly integrated semiconductor device embedded within smart meters to perform energy measurement, data processing, communication and control functions. It typically combines a metrology analog front‑end (AFE), microcontroller (MCU), memory and communication interfaces such as RF, PLC or NB‑IoT. These chips enable accurate real‑time monitoring of electricity consumption, two‑way interaction with utilities and advanced capabilities including demand‑response, remote reading and energy analytics. As a core component of advanced metering infrastructure (AMI), the chip underpins digital, automated and intelligent power distribution systems.

MARKET DRIVERS

Regulatory Push for Advanced Grid Management

National electricity regulators across Europe and North America have mandated the rollout of intelligent metering infrastructure, creating a direct requirement for integrated semiconductor solutions. Smart Electricity Meter Chip Market benefits from clear compliance schedules that compel utilities to replace legacy meters within defined timelines, translating policy into measurable demand for high‑precision analog‑to‑digital converters and low‑power radio modules.

Technological Convergence and Cost Reduction

Silicon‑photonic nodes, edge‑AI accelerators, and secure enclave architectures are now co‑fabricated on a single die, slashing the bill‑of‑materials for a smart meter chipset by roughly 30 % compared with a generation ago. This economies‑of‑scale effect prompts manufacturers to broaden portfolio breadth, while utilities reap operational savings from fewer components and simplified firmware updates.

➤ “A unified chip that handles measurement, communication, and security in one package is reshaping procurement models for distribution operators.”

Because the newest generations can report consumption data in sub‑second intervals without draining battery life, distribution companies are able to shift from batch‑billing to real‑time pricing schemes, unlocking new revenue streams and enhancing load‑balancing capabilities.

MARKET CHALLENGES

Supply‑Chain Volatility

Global semiconductor fab capacity remains constrained by periodic capacity cuts and geopolitical tension, forcing many meter manufacturers to hold higher inventory buffers. The resulting lead‑times of 8‑12 weeks for advanced mixed‑signal chips introduce scheduling uncertainty that can delay utility rollouts.

Other Challenges

Integration Complexity

Deploying a multi‑function chip within an existing meter enclosure often requires redesign of power‑regulation stages and electromagnetic shielding, tasks that stretch engineering resources and inflate development budgets.

MARKET RESTRAINTS

High Up‑Front Capital Expenditure

Utilities face sizable budget allocations to replace analog meters with smart versions, and the added cost of sophisticated chips compounds the financial hurdle. Many regional operators defer full‑scale adoption until they secure favorable financing or public‑private partnership models.

Cybersecurity Concerns

As meter firmware becomes a vector for remote attacks, regulators demand robust cryptographic modules and secure boot processes, both of which drive up design complexity and unit cost. Organizations that cannot guarantee end‑to‑end protection are likely to encounter procurement roadblocks.

MARKET OPPORTUNITIES

Emerging Demand in Southeast Asia

Rapid urbanization and government‑led electrification programs in Indonesia, Vietnam, and the Philippines have opened a sizeable gap for smart metering solutions. Early‑stage utilities are evaluating chipsets that can operate under high ambient temperatures while maintaining low power consumption, a niche where several suppliers are positioning differentiated products.

Integration with Renewable Energy Management

Distributed solar and battery installations require meters capable of bidirectional energy flow measurement. Chip manufacturers that embed precise energy‑reversal algorithms and real‑time grid‑support signals stand to capture a growing slice of the installation base as renewables attain higher market share.

Aftermarket Services and Firmware Monetization

Because the underlying hardware can remain in the field for a decade, firmware‑as‑a‑service models present a recurring‑revenue channel. Providers that offer secure OTA update frameworks enable utilities to roll out demand‑response features and tariff changes without costly hardware swaps.

Smart Electricity Meter Chip Market Trends

Integration and Connectivity Surge

The industry is witnessing a decisive shift toward system‑on‑chip (SoC) architectures that fuse metrology front‑ends, microcontrollers and diverse radio interfaces into a single silicon die. This consolidation cuts board‑level component count, trims power envelope, and lowers bill‑of‑materials, allowing meter manufacturers to meet tight cost targets while supporting ultra‑low‑latency two‑way communication. In 2025, average unit pricing hovered near US$1.05, yet SoC‑based designs are already delivering a 12‑15% cost advantage versus discrete‑part solutions, a margin that directly improves gross profitability for chip suppliers, whose 2025 gross margin stood around 41%.

Other Trends

Regulatory and Grid Modernization Drivers

Nation‑wide smart‑grid programmes and renewable‑integration mandates compel utilities to replace legacy electromechanical meters with intelligent equivalents. Policies that enforce real‑time load profiling and demand‑response readiness have created a predictable pipeline of installations, translating into roughly 730 million chip shipments in 2025. The regulatory push also standardizes communication protocols,NB‑IoT, PLC and emerging cellular‑M‑band,forcing vendors to broaden their firmware stacks, which in turn accelerates firmware‑over‑the‑air (FOTA) capabilities across the product line.

Supply‑Chain Synchronization and Value‑Chain Tightening

Upstream, semiconductor foundries are allocating dedicated wafer capacity to meet the 800 million‑unit production ceiling, while downstream meter assemblers coordinate closely with utilities to align delivery schedules with grid‑expansion milestones. This synchronized flow reduces lead‑time variances and curtails inventory excess, allowing chip makers to sustain higher inventory turns. Moreover, the convergence of AI‑enabled analytics at the meter level is prompting chip designers to embed lightweight inference engines, positioning the chip not just as a data conduit but as a decision‑support node within the advanced metering infrastructure.

COMPETITIVE LANDSCAPE

Key Industry Players

Assessing the competitive arena of Smart Electricity Meter Chip manufacturers

STMicroelectronics commands the top tier of the market, leveraging its deep analog‑metering pedigree and extensive global fab capacity to supply integrated metrology‑MCU‑communication SoCs to the majority of utility‑grade roll‑outs. The company’s ability to bundle high‑precision AFE blocks with secure NB‑IoT stacks gives it a pricing advantage that forces downstream meter makers to adopt its reference designs. Analog Devices follows closely, differentiating through ultra‑low‑noise analog front ends and a strong portfolio of field‑programmable security IP, which resonates with regulators demanding tamper‑resistant solutions. Texas Instruments rounds out the elite trio by capitalizing on its massive MCU ecosystem and an aggressive IP‑licensing model that allows smart‑meter OEMs to customize communication modules without redesigning the silicon.

Beyond the tier‑one group, a constellation of niche players intensifies pressure on margins and stimulates innovation. NXP Semiconductors and Renesas Electronics each bring cellular‑grade RF expertise, positioning themselves for hybrid meters that must support both PLC and LTE‑M. Microchip Technology leverages its long‑standing MCU lineage to bundle legacy code bases with emerging AI inference engines for demand‑response analytics. Asian specialists such as CHIPSEA, Shanghai Belling Corp, Hi‑Trend Technology (Shanghai), and Shanghai Fudan Microelectronics focus on cost‑sensitive single‑phase solutions, often integrating memory‑centric designs that reduce bill‑of‑materials for mass‑market residential deployments. Smaller fabless firms,e.g., PowerChip Microsystems and GreenWave Technologies,target the niche of renewable‑energy‑centric meters, embedding grid‑supportive algorithms that orchestrate distributed generation.

List of Key Smart Electricity Meter Chip Companies Profiled

- STMicroelectronics, Analog Devices, Texas Instruments

- NXP Semiconductors, Renesas Electronics, Microchip Technology, CHIPSEA

- Shanghai Belling Corp, Hi‑Trend Technology (Shanghai), Shanghai Fudan Microelectronics, PowerChip Microsystems, GreenWave Technologies, Silicon Labs, Qualcomm Technologies, Infineon Technologies

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Advanced Smart Meter Chip – The market privileges chips that combine metrology, MCU, and communication in a single SoC. • Integration reduces board space and power consumption, enabling compact meter designs. • High‑performance analog front‑ends improve measurement accuracy, supporting demand‑response programs. • Flexibility to support multiple communication standards (NB‑IoT, PLC, cellular) strengthens utility interoperability. |

| By Application |

|

Residential Segment – Residential meters drive widespread adoption of low‑cost, energy‑aware chips. • Focus on simplified firmware and secure OTA updates to maintain consumer trust. • Ability to interface with home energy management systems fuels value‑added services. • Scalability for prepaid and hybrid metering models creates flexible billing options. |

| By End User |

|

Utility Companies – Utilities prioritize chips that enable reliable two‑way communication and robust data security. • Seamless integration with existing AMI platforms reduces deployment friction. • Enhanced diagnostic capabilities support proactive grid maintenance. • Compatibility with emerging AI‑driven analytics enriches load forecasting and outage management. |

| By Integration Level |

|

System‑on‑Chip Solutions – SoC designs dominate strategic discussions. • Consolidation of metrology, MCU, and communications cuts bill of materials. • Lower thermal footprint supports deployment in constrained meter enclosures. • Future‑ready architecture accommodates AI inference and edge analytics. |

| By Functionality |

|

Security & Encryption – Data integrity is a decisive factor for adoption. • Built‑in hardware security modules protect against tampering. • Secure key management enables trusted device onboarding. • Ongoing firmware authentication mitigates cyber‑threats while preserving grid reliability. |

Regional Analysis: Smart Electricity Meter Chip Market

Europe

The EU’s Energy Efficiency Directive obliges member states to replace legacy meters, driving demand for chips that comply with MID and IEC standards. Compliance testing has become a decisive factor in supplier selection, pushing vendors to certify designs across multiple jurisdictions early in the development cycle.

Proximity to semiconductor fabs in the Netherlands and Germany reduces lead times for Europe‑focused chip runs. This geographic advantage enables rapid iteration of design variants, allowing manufacturers to respond swiftly to evolving utility specifications.

Consumer appetite for time‑of‑use tariffs, combined with grid‑balancing incentives, compels utilities to seek chips capable of high‑resolution sampling and secure communications, accelerating rollout schedules across densely populated urban zones.

Established European players leverage deep relationships with utility engineers, while emerging Asian suppliers compete on price. The next wave of competition will hinge on differentiated security features and on‑chip processing power that can support edge analytics.

North America

In North America, Smart Electricity Meter Chip Market is being shaped by utility‑led pilot programs that emphasize demand‑response capabilities. Federal incentives encourage the integration of chips with low‑power, wide‑area network (LP‑WAN) modules, allowing rural utilities to extend coverage without extensive infrastructure upgrades. Vendors that can embed robust encryption and meet NIST cybersecurity standards enjoy a competitive edge, as regulators prioritize data privacy. The regional focus on renewable integration also pushes chip designers toward supporting high‑frequency voltage event detection, a prerequisite for managing distributed generation assets such as rooftop solar and battery storage systems.

Asia‑Pacific

The Asia‑Pacific landscape is defined by rapid urbanization and governmental commitments to smart grid modernization. Countries like China, India and Japan are launching nationwide programs that call for mass deployment of intelligent metering solutions. Chip manufacturers are responding with cost‑optimized designs that still deliver essential features such as multi‑protocol connectivity and adaptive power‑saving modes. Market participants that can localize firmware to accommodate diverse language and tariff structures stand to capture sizable contract volumes, while also benefiting from the region’s expanding semiconductor manufacturing base.

South America

South America’s Smart Electricity Meter Chip Market is emerging from a foundation of legacy analog meters, with Brazil and Chile leading pilot deployments. Energy ministries are linking grid‑digitalization goals to climate‑finance mechanisms, encouraging utilities to adopt chips that support real‑time consumption data and automated outage detection. The primary challenge remains the need for ruggedized solutions capable of withstanding high ambient temperatures and intermittent power supplies. Companies that can deliver reliable, low‑cost silicon while providing localized technical support are gradually gaining footholds in the region.

Middle East & Africa

In the Middle East & Africa, the market is driven by ambitious smart‑city initiatives and a growing appreciation for energy‑efficiency analytics. Gulf Cooperation Council nations prioritize chips that can operate under extreme heat and integrate seamlessly with advanced SCADA systems. Meanwhile, African utilities are focused on resilient, battery‑operated metering chips that can sustain long deployment cycles with minimal maintenance. The convergence of public‑sector funding and private‑sector expertise is fostering a niche for vendors that can balance durability with sophisticated data‑encryption capabilities.

Report Scope

This market research report provides a comprehensive analysis of the Smart Electricity Meter Chip Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Smart Electricity Meter Chip Market?

-> Smart Electricity Meter Chip Market is expected to reach USD 1,031 million by 2034, growing at a CAGR of 5.7% during the forecast period.

Which key companies operate in Smart Electricity Meter Chip Market?

-> Key players include STMicroelectronics, Analog Devices, Texas Instruments, Renesas Electronics, NXP Semiconductors, Microchip Technology, CHIPSEA, Shanghai Belling Corp, Hi-trend Technology (Shanghai), and Shanghai Fudan Microelect.

What are the key growth drivers?

-> Key growth drivers include global grid modernization initiatives, increasing demand for energy efficiency, regulatory mandates for smart meter deployment, rising electricity consumption, urbanization, and the integration of renewable energy sources.

Which region dominates the market?

-> Asia leads the market in terms of volume and revenue, driven by large-scale smart grid projects and rapid urbanization, while Europe remains a significant and mature market.

What are the emerging trends?

-> Emerging trends include higher integration with system‑on‑chip (SoC) solutions, IoT‑enabled smart meters, AI‑driven energy management, NB‑IoT and cellular connectivity, and increased adoption of prepaid and hybrid meters.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...