Animal Electronic Identification Tags Market Insights

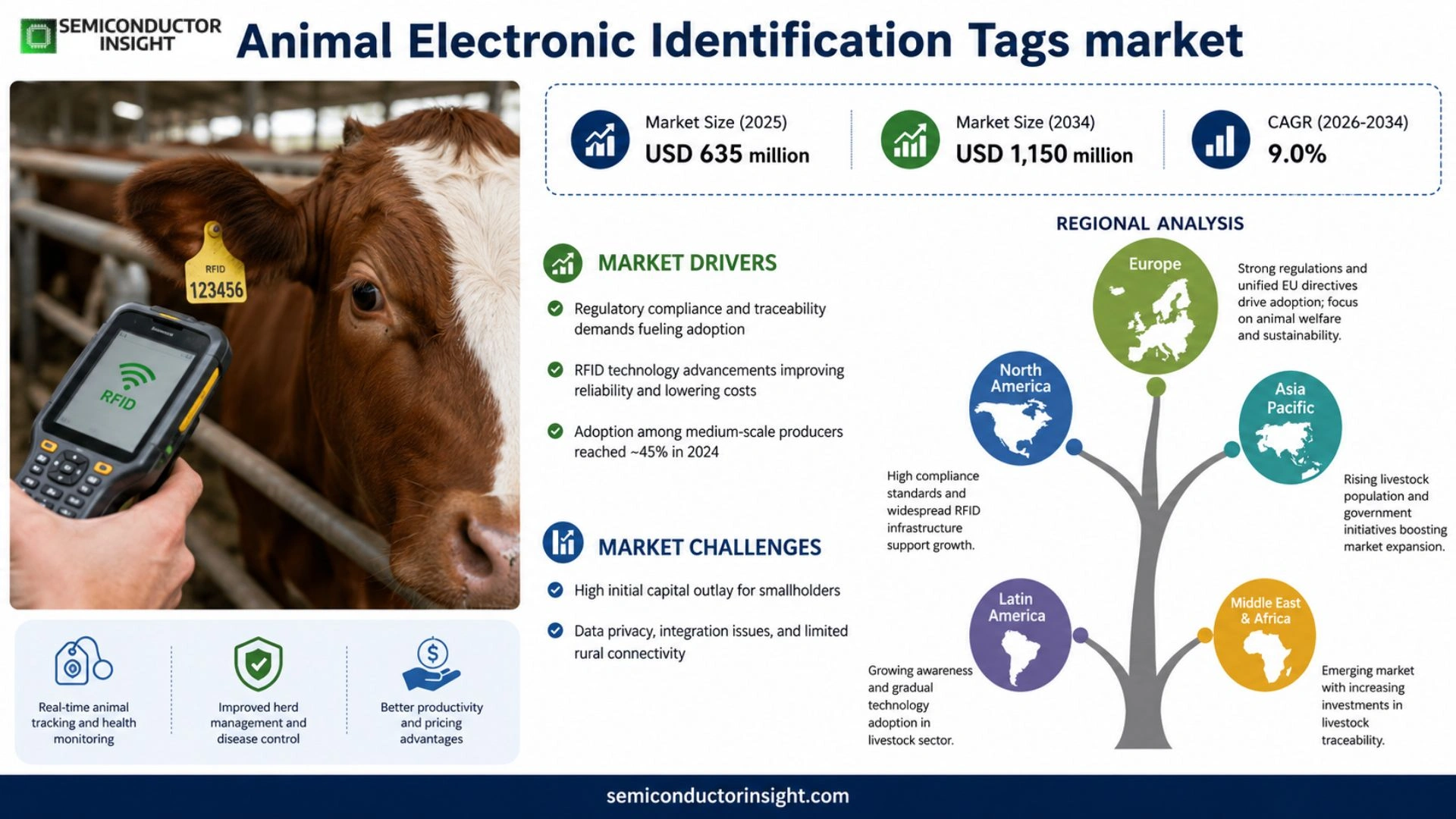

Global Animal Electronic Identification Tags market size was valued at USD 635 million in 2025 and is forecasted to reach USD 1,150 million by 2034, delivering a CAGR of 9.0% over the period.

Animal Electronic Identification Tags are electronic devices that assign and read a unique identity code for each animal through RFID‑based transponders embedded in ear tags, bolus tags, injectable microchips or other carriers. These tags support livestock traceability, herd management, disease control, regulatory compliance, ownership verification and movement recording. Typical unit costs range from a few dollars with profit margins between 30 % and 50 %.

The market expands as livestock disease control programs intensify, food‑safety traceability requirements tighten and farm automation gains traction worldwide. Recent activity includes Allflex’s launch of a battery‑free passive RFID ear‑tag platform in March 2024 that integrates temperature monitoring, while HID Global announced an upgrade of its data‑management software suite for real‑time herd analytics in July 2024. Such innovations improve reading efficiency, lower manual errors and enable seamless linkage of animal data with breeding, vaccination and feeding records.

MARKET DRIVERS

Regulatory Compliance and Traceability Demands

The tightening of livestock traceability legislation across North America and the EU forces producers to adopt electronic identification solutions. Compliance costs for manual tagging have risen, prompting a shift toward RFID‑enabled tags that can be scanned instantly at slaughterhouses, transport checkpoints, and veterinary facilities. This regulatory pressure creates a steady stream of demand for Animal Electronic Identification Tags Market.

Advancements in RFID Technology

Recent improvements in chip mini‑size, battery‑free operation, and read range have lowered total cost of ownership for farms of all sizes. As these tags become more reliable under harsh environmental conditions, producers view them as a long‑term asset rather than a one‑off expense, encouraging broader adoption across dairy, beef, and swine sectors.

➤ Adoption rates among medium‑scale producers have climbed to roughly 45 % in 2024, up from 30 % two years earlier, reflecting the tangible ROI of reduced labor and error‑prone manual tagging.

Beyond compliance, the ability to aggregate real‑time health and location data empowers herd managers to fine‑tune nutrition, predict disease outbreaks, and negotiate better pricing with buyers,benefits that directly reinforce the growth engine of Animal Electronic Identification Tags Market.

MARKET CHALLENGES

High Initial Capital Outlay for Smallholders

For tiny family farms, the upfront expense of RFID readers, software platforms, and tag inventory can exceed annual operating budgets. Although tag prices have fallen, the ancillary hardware and training costs remain a substantial barrier that slows market penetration among low‑margin producers.

Other Challenges

Data Privacy and Integration Issues

Farmers often struggle to integrate tag data with legacy ERP or herd‑management systems. Compatibility concerns, coupled with apprehensions about data ownership, can cause hesitation even when the technology itself is proven.

Moreover, inconsistent broadband coverage in rural regions hampers real‑time data transmission, limiting the perceived value of cloud‑based analytics and slowing investment decisions.

MARKET RESTRAINTS

Fragmented Standards and Interoperability Gaps

Across continents, divergent frequency allocations and tag encoding rules create a patchwork of standards. Producers operating across borders must purchase multiple tag families or risk non‑compliance, which inflates costs and discourages uniform adoption.

These technical silos also inhibit economies of scale for manufacturers, leading to higher unit prices that reinforce the restraint on market expansion.

MARKET OPPORTUNITIES

Integration with Precision Agriculture Platforms

Linking electronic tags with satellite‑derived pasture analytics, automated feed dispensers, and AI‑driven health alerts opens a revenue stream for vendors willing to supply turnkey solutions. Such convergence not only enhances livestock productivity but also creates recurring subscription income for data services.

Emerging markets in South America and Southeast Asia, where livestock density is rising rapidly, present a fertile ground for entry. Early‑stage partnerships with local cooperatives can accelerate penetration and establish brand leadership before competitive pressures intensify.

Animal Electronic Identification Tags Market Trends

Shift Toward Integrated Digital Herd Management

The latest data indicate that livestock producers are replacing manual ear‑tag logs with networked identification solutions that feed directly into farm‑management platforms. By linking RFID transponders to cloud‑based analytics, operators can synchronize weight, health, breeding and movement records without human transcription. This automation reduces the latency between event capture and decision making, allowing early detection of disease clusters and more precise feed allocation. The economic incentive arises from lower labor costs and a measurable drop in medication usage, as health alerts become actionable within minutes rather than days. Consequently, equipment manufacturers that bundle tags with software services are seeing higher average order values, reshaping the revenue model of Animal Electronic Identification Tags Market.

Other Trends

Supply‑Chain Consolidation

Upstream component suppliers are aligning with a handful of dominant tag makers, creating semi‑integrated production lines for RFID chips, antenna coils and durable housings. This consolidation trims lead times and improves quality consistency, which matters for regulators that demand traceability records be error‑free. Smaller niche players that focus on specialty substrates,such as biodegradable polymers for eco‑certified farms,are carving out modest but defensible market slices. Downstream, large integrators are negotiating multi‑year contracts with feed‑lot operators, securing predictable volume while offering volume‑based discounts that improve margin stability across the value chain.

Regulatory Momentum Enhances Adoption

Governmental identification mandates across North America, the European Union and several Asian economies have tightened over the past three years, specifying that each animal must carry an electronically readable tag. Compliance requirements now extend beyond border checks to routine veterinary inspections, prompting farms to upgrade legacy visual tags to RFID‑enabled alternatives. The ripple effect is evident in export‑oriented producers, who adopt the technology pre‑emptively to avoid shipment delays. Software vendors are responding by embedding regulatory data fields directly into their dashboards, simplifying audit trails for farmers. This regulatory push not only expands the addressable base of Animal Electronic Identification Tags Market but also accelerates the shift from point‑of‑sale tagging to ecosystem‑wide digital identity, a development that will shape investment decisions for years to come.

COMPETITIVE LANDSCAPE

Key Industry Players

Animal Electronic Identification Tags: Competitive Overview

Allflex, operating under MSD Animal Health, commands the lion’s share of the global market through a vertically integrated model that combines in‑house RFID chip engineering with proprietary ear‑tag manufacturing. Its extensive patent portfolio around low‑frequency transponders creates a barrier to entry, while a worldwide distribution network secures contracts with the largest cattle, pig and sheep operations in North America, Europe and Asia. By synchronising product roadmaps with national livestock‑identification programs, Allflex enjoys repeat‑order stability and can attach a modest software‑as‑a‑service premium for herd‑management analytics. The company’s profit margins, typically ranging from 30 % to 45 %, reflect the premium placed on durability and data integrity, reinforcing its position as the de‑facto supplier for government‑mandated identification schemes.

Chasing the leader, a mosaic of specialists sustains competition across price‑sensitive and technology‑focused niches. HID Global leverages its security‑card heritage to deliver high‑readability microchips for companion animals and laboratory rodents, while Avery Dennison concentrates on low‑cost ear‑tags that appeal to small‑holder sheep farms in Europe and Africa. Regional innovators such as Kupsan (Turkey) and ARDES (France) specialise in bolus and implantable formats tuned to local regulatory requirements, thereby locking in dairy‑herd contracts. Smaller but agile firms,including Dalton Tags, CowManager, Somark Innovations, Moocall, Ceres Tag, Laipson Information Technology, Xiamen Innov Information Technology and Wuxi FOFLA Technology,target bespoke applications ranging from estrus detection to wildlife telemetry, often bundling their hardware with third‑party software platforms. Recent joint‑ventures and selective acquisitions have amplified their market reach, creating a fragmented tier that pressures pricing while simultaneously driving incremental feature adoption throughout the value chain.

List of Key Animal Electronic Identification Tags Companies Profiled

- Allflex (MSD Animal Health)

- HID Global

- Avery Dennison

- Shearwell Data

- Caisley

- Kupsan

- ARDES

- Dalton Tags

- CowManager

- Somark Innovations

- Moocall

- Ceres Tag

- Laipson Information Technology

- Xiamen Innov Information Technology

- Wuxi FOFLA Technology

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Ear Tags dominate because they offer robust field readability, easy attachment to a wide range of livestock, and seamless integration with farm‑management software – they reduce manual recording errors, support real‑time health monitoring, and enable rapid verification during movement checks. |

| By Application |

|

Animal Husbandry Management is the primary driver, delivering precise herd tracking, automated feeding and breeding schedules, and compliance with traceability regulations – it strengthens disease control, improves productivity insights, and simplifies audit processes for large‑scale farms. |

| By End User |

|

Livestock Farmers lead adoption as electronic tags enable real‑time herd analytics, streamline movement documentation, and align with national identification mandates – they also support precision feeding and genetic selection programs across cattle, sheep, goats and pigs. |

| By Power Supply Method |

|

Passive RFID Tags are preferred for most livestock because they require no battery, keep costs low, and deliver reliable read ranges when paired with farm‑level readers – they also simplify regulatory compliance and reduce maintenance overhead. |

| By Regulatory Framework |

|

Mandatory National ID Programs shape market direction by enforcing electronic identification for disease control and export certification – they accelerate technology diffusion, create uniform data standards, and drive investment in reader infrastructure across the supply chain. |

Regional Analysis: Animal Electronic Identification Tags Market

North America

Federal agencies have codified electronic tagging as a prerequisite for interstate animal movement, prompting producers to upgrade legacy systems. State‑level initiatives reinforce data‑sharing mandates, ensuring that every tag can be cross‑referenced with health and provenance databases. This regulatory certainty accelerates market confidence and reduces barriers for new entrants.

RFID‑based tags dominate, yet Bluetooth Low Energy prototypes are gaining attention for real‑time monitoring. Early adopters experiment with hybrid solutions that couple location data with biometric sensors, opening pathways for predictive health alerts. The convergence of these technologies elevates the overall value proposition of the market.

Established manufacturers leverage deep supply‑chain relationships to secure raw materials, while niche innovators focus on software ecosystems that translate tag reads into actionable insights. Partnerships between hardware firms and agritech platforms create bundled offerings that appeal to large‑scale operations seeking integrated solutions.

Proximity to major livestock clusters shortens lead times and reduces logistics costs. Domestic production of antennae and encoding equipment buffers the market from global component shortages, while strategic warehousing near feedlots ensures rapid deployment during peak breeding seasons.

Europe

European stakeholders view electronic identification as a cornerstone of animal welfare policy. Harmonized EU directives mandate tag usage across member states, fostering a uniform market environment. Producers increasingly align tagging data with sustainability reporting, linking animal performance metrics to carbon‑footprint calculations. Local manufacturers benefit from a dense network of research institutes that explore low‑power chip designs, positioning Europe as a fertile ground for next‑generation tag concepts.

Asia‑Pacific

Rapid modernization of dairy and aquaculture farms fuels demand for digital animal IDs in the Asia‑Pacific corridor. Governments are rolling out incentive programs that offset equipment costs for smallholders, accelerating diffusion beyond large commercial operations. Cultural emphasis on traceability for export markets drives exporters to adopt high‑resolution tagging, while regional trade shows spotlight emerging chipset suppliers eager to capture market share.

South America

In South America, the expansion of pasture‑based cattle enterprises creates a natural laboratory for electronic tagging adoption. Producers prioritize rugged tag designs that withstand harsh climatic conditions, prompting manufacturers to tailor casings and antennae. Growing export pressure for certified meat products amplifies the need for transparent animal histories, nudging the market toward broader acceptance of data‑centric herd management.

Middle East & Africa

The Middle East & Africa region presents a mosaic of opportunities, with arid‑zone livestock operations seeking resilient identification solutions. Pilot projects in United Arab Emirates and Kenya integrate tags with satellite‑linked telemetry, enabling remote monitoring of nomadic herds. While infrastructure constraints limit scale, partnerships with telecom providers are laying the groundwork for continent‑wide data networks that could unlock new use cases for Animal Electronic Identification Tags Market.

Report Scope

This market research report provides a comprehensive analysis of the Animal Electronic Identification Tags Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Animal Electronic Identification Tags Market?

-> Animal Electronic Identification Tags Market was valued at USD 635 million in 2025 and is expected to reach USD 1150 million by 2032 with a CAGR of 9.0% during the forecast period.

Which key companies operate in Animal Electronic Identification Tags Market?

-> Key players include Allflex (MSD Animal Health), HID Global, Avery Dennison, Shearwell Data, Caisley, Kupsan, ARDES, Dalton Tags, CowManager, Somark Innovations, Moocall, Ceres Tag, Laipson Information Technology, Xiamen Innov Information Technology, Wuxi FOFlA Technology.

What are the key growth drivers?

-> Key growth drivers include livestock disease control, food safety traceability, cross‑border animal movement management, farm automation, digital herd management, and regulatory adoption of electronic identification systems.

Which region dominates the market?

-> Asia‑Pacific shows the fastest growth owing to large cattle, sheep, goat and pig populations, while North America remains a mature and sizable market.

What are the emerging trends?

-> Emerging trends include integration of RFID tags with IoT platforms, AI‑driven herd analytics, and development of durable, waterproof passive tags for harsh farm environments.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...