Industrial MRAM (Magnetoresistive Random Access Memory) Market Insights

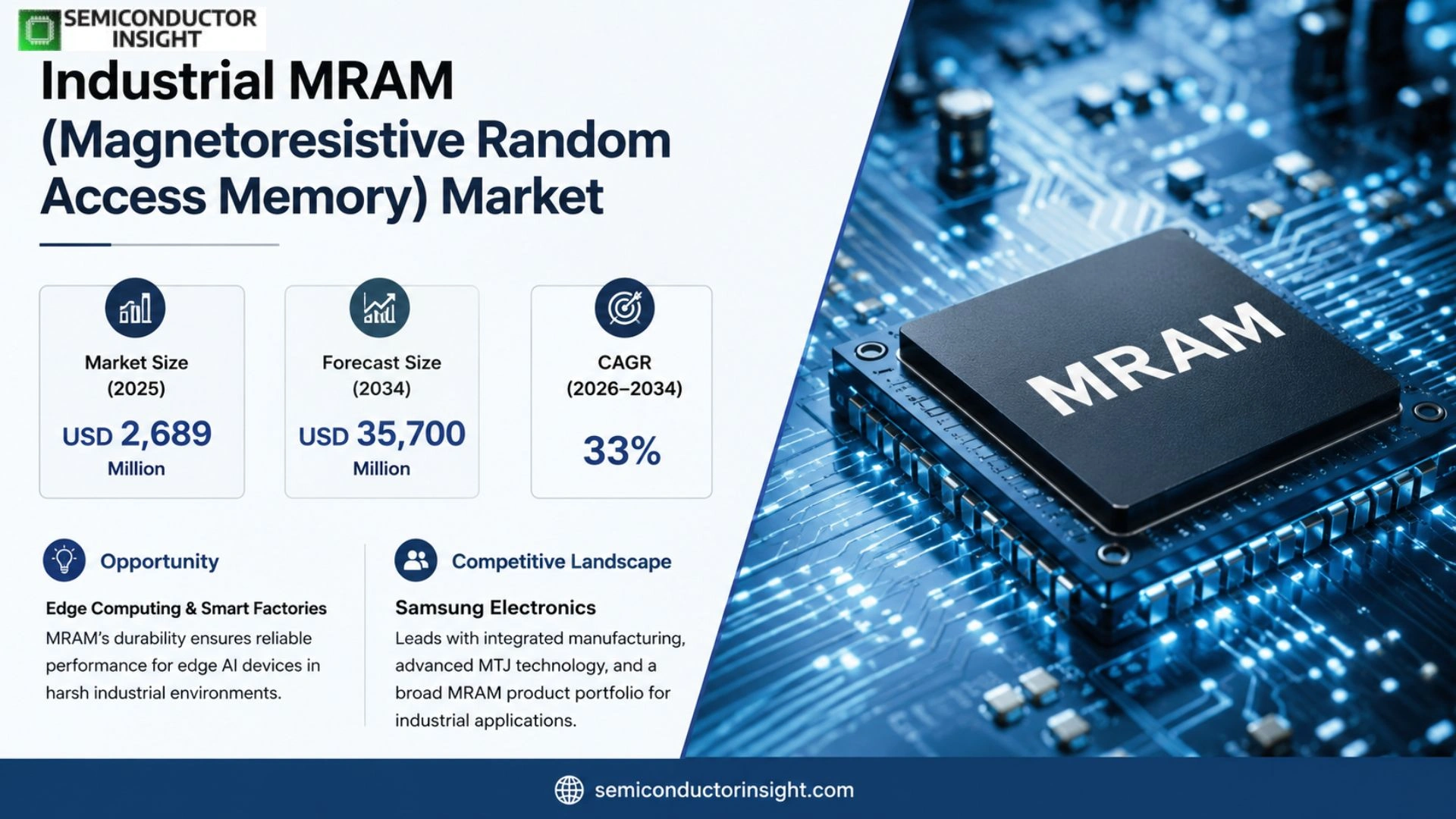

Global Industrial MRAM (Magnetoresistive Random Access Memory) market was valued at USD 2,689 million in 2025 and is expected to reach USD 35,700 million by 2034, reflecting a compound annual growth rate of roughly 33 % over the period.

Industrial MRAM is a non‑volatile memory built on magnetoresistance and magnetic tunnel junctions (MTJs). It merges SRAM‑class speed with DRAM‑level density while retaining Flash‑type persistence, making it suitable for harsh industrial settings where temperature extremes, radiation exposure and vibration are common.

The sector’s expansion stems from rising adoption in automotive electronics, aerospace control units and edge‑computing devices that demand fast write cycles and long endurance. In 2025 production hit about 433 million units at an average price of USD 6.8 per chip, while capacity stands near 620 million units annually,indicating ample room for scaling as foundries broaden eMRAM offerings.

MARKET DRIVERS

Rising Need for Reliable Non‑Volatile Memory in Automation

The surge in robotic cells and PLC‑based control systems has forced OEMs to seek memory that retains state after power loss. ,Industrial MRAM (Magnetoresistive Random Access Memory) Market, satisfies this requirement with near‑zero leakage, allowing factories to slash standby power budgets while preserving critical configuration data.

Stringent Data‑Integrity Standards Across Sectors

Regulatory frameworks in aerospace and medical device manufacturing now mandate error‑free logging of sensor data. Because MRAM offers intrinsic resistance to radiation‑induced bit flips, manufacturers are substituting traditional SRAM/Flash with MRAM to meet compliance without redesigning hardware architectures.

➤ “Switching to MRAM cuts system reboot cycles by roughly 30 % and reduces overall downtime, a decisive factor for high‑value production lines.”

When downtime translates directly into lost revenue, the cost premium of MRAM is justified. ,Capital‑intensive plants, are therefore allocating a larger share of their upgrade budgets to MRAM‑enabled controllers, accelerating market momentum.

MARKET CHALLENGES

Cost Pressures in High‑Volume Manufacturing

Although MRAM’s performance profile is compelling, its per‑bit price remains above that of traditional Flash. Tier‑1 suppliers in consumer electronics are able to absorb the premium, but ,mid‑tier industrial integrators, often struggle to justify the expense when Bill‑of‑Materials targets are razor‑thin.

Other Challenges

Supply‑Chain Complexity

The limited number of fabs capable of producing spin‑torque MRAM creates bottlenecks. Any disruption,whether geopolitical or pandemic‑related,has an outsized impact on lead times, prompting buyers to keep larger safety stocks, which in turn raises inventory costs.

MARKET RESTRAINTS

Technology Maturity Relative to Competing Memories

While MRAM delivers unmatched durability, its ,write‑latency, still lags behind emerging ferroelectric RAM solutions that are gaining traction in niche applications. This performance gap discourages some system designers who prioritize speed over endurance.

Legacy design libraries embedded in decades‑old PLC firmware rarely include MRAM primitives. Engineers must allocate additional design time to validate MRAM‑based blocks, a hurdle that slows adoption in plants that operate on tight development schedules.

Furthermore, the environmental certification process for new memory modules can extend product launch timelines, especially for equipment destined for hazardous zones where intrinsic safety ratings are mandatory.

MARKET OPPORTUNITIES

Edge Computing and Smart Factories

Edge gateways deployed at the plant floor require memory that can survive frequent power cycling and harsh temperature swings. MRAM’s resilience makes it a natural fit for ,edge AI accelerators,, where on‑device inference must continue uninterrupted despite intermittent power.

The upcoming rollout of Industry 4.0 standards across Europe and Asia creates a wave of retrofits. Vendors that bundle MRAM with modular I/O platforms can capture a share of this upgrade market, especially when they emphasize reduced maintenance cycles.

Another promising avenue lies in the electrification of heavy equipment. Battery‑managed controllers for autonomous forklifts and mining trucks benefit from MRAM’s low standby draw, extending operational range and simplifying power‑budget calculations.

Industrial MRAM (Magnetoresistive Random Access Memory) Market Trends

Escalating Adoption in Automotive Electronics

The automotive sector is converting its legacy memory architecture as safety‑critical control units demand faster write cycles and guaranteed data retention after power loss. Industrial MRAM (Magnetoresistive Random Access Memory) offers SRAM‑level speed while preserving the endurance of DRAM, a combination that matches the stringent functional‑safety standards of modern vehicles. As electric‑drive systems and advanced driver‑assistance modules increase in complexity, designers are substituting embedded Flash with MRAM to avoid reboot delays after abrupt voltage events. The shift is reinforced by the technology’s tolerance to high‑temperature operation and vibration, which reduces the need for auxiliary cooling or ruggedization. Consequently, OEMs are allocating a larger share of their electronic budget to MRAM‑based subsystems, prompting suppliers to prioritize automotive‑qualified process nodes.

Other Trends

Cost Structure and Scale Constraints

Despite its technical merits, Industrial MRAM remains a premium component. The average unit price of roughly $6.8 in 2025 reflects the specialized magnetic materials,CoFeB and MgO,and the high‑precision lithography required for magnetic tunnel junctions. Production capacity of 620 million units per year still trails demand, creating a bottleneck that inflates cost. Manufacturers are therefore focusing on incremental yield improvements and strategic partnerships with foundries that can embed MRAM alongside logic circuits, thereby sharing wafer expenses. Until economies of scale materialize, the technology will likely stay confined to high‑value niches where performance outweighs price considerations.

Emergence of Embedded MRAM in Edge Computing

Edge devices operating in remote or intermittently powered environments benefit from non‑volatile memory that can survive power cycling without data loss. Embedded MRAM satisfies this requirement while delivering latency comparable to SRAM, enabling real‑time analytics on the device rather than streaming raw data to the cloud. Industries such as industrial automation and aerospace are trialing MRAM‑based controllers to safeguard mission‑critical parameters against radiation‑induced bit flips. As firmware updates become more frequent and security patches demand rapid write capabilities, developers are gravitating toward MRAM to reduce firmware corruption risk. The cumulative effect is a modest but steady expansion of Industrial MRAM (Magnetoresistive Random Access Memory) Market within the broader edge‑computing ecosystem, where reliability supersedes raw capacity.

COMPETITIVE LANDSCAPE

Key Industry Players

Industrial MRAM Competitive Dynamics and Emerging Opportunities

Samsung Electronics dominates the industrial MRAM arena by leveraging its vertically integrated semiconductor ecosystem and securing early access to advanced eMRAM process nodes at its own foundry. The company’s ability to combine high‑volume wafer production with proprietary magnetic tunnel junction (MTJ) materials gives it a cost advantage that translates into higher gross margins than most pure‑play specialists. Samsung’s portfolio now spans standalone chips, embedded MRAM IP, and hybrid modules, enabling OEMs in automotive and aerospace to substitute legacy SRAM or Flash with a single‑source solution. This breadth of offering consolidates market share around a few large IDM‑foundry hybrids, while also setting a technology benchmark that forces smaller players to pursue differentiated niches or collaborative licensing arrangements.

Beyond Samsung, a constellation of niche innovators underpins the market’s depth. Everspin Technologies remains the only dedicated MRAM fab, focusing on low‑density, high‑reliability parts that serve edge‑computing and industrial control systems. Avalanche Technology and Spin Memory specialize in high‑density STT‑MRAM cells, targeting automotive electronics where endurance and temperature tolerance are paramount. Meanwhile, NVE Corporation and Honeywell International exploit their expertise in magnetic materials to offer custom MTJ stacks for defense and space applications. Regional players such as Shanghai Siproin Microelectronics, Wuhan Xinxin Semiconductor, and Fudan Microelectronics are expanding capacity in China, often coupling government subsidies with OEM partnerships to accelerate adoption in domestic automotive lines. The presence of established silicon giants,Intel, Fujitsu, Infineon, and Toshiba,adds credibility and drives cross‑licensing that broadens the supply base, albeit at higher price points. Collectively, this diverse ecosystem creates a competitive tension between scale‑driven cost efficiency and specialized performance attributes, shaping procurement strategies for end‑users across the industrial spectrum.

List of Key Industrial MRAM Companies Profiled

- Everspin Technologies

- Samsung Electronics

- Avalanche Technology

- Spin Memory

- Honeywell International

- NVE Corporation

- Shanghai Siproin Microelectronics

- Wuhan Xinxin Semiconductor

- IBM

- SST

- Fudan Microelectronics

- Fujitsu

- Intel Corporation

- Toshiba

- Infineon Technologies

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Embedded MRAM

|

| By Application |

|

Automotive Electronics

|

| By End User |

|

Robotics

|

| By Product Form |

|

Medium Density

|

| By Interface Type |

|

HyperBus MRAM

|

Regional Analysis: Industrial MRAM (Magnetoresistive Random Access Memory) Market

Silicon Valley, Austin, and Toronto form a triad of innovation hubs where spin‑orbit research meets chip‑scale integration. The dense network of start‑ups, university spin‑outs, and incubators accelerates proof‑of‑concept cycles, delivering novel MRAM architectures that address latency and endurance constraints typical of industrial workloads.

Established lithography facilities and a reliable consumables market ensure that MRAM production can scale without the material shortages that often hamper emerging memory technologies. This resiliency underpins confidence among OEMs that adopt MRAM for mission‑critical devices.

Defense‑grade certifications and stringent electromagnetic compatibility standards drive OEMs toward memory that offers non‑volatile retention and radiation hardness. North American regulators have streamlined pathways for such certifications, shortening time‑to‑market for qualified MRAM components.

Industrial robot controllers and smart grid substations increasingly embed MRAM to guarantee state retention across power cycles. Early adopters report reduced system downtime and lower maintenance costs, prompting broader procurement programs across the region’s manufacturing base.

Europe

European manufacturers benefit from a coordinated standards framework that encourages interoperability of memory modules across automotive and rail sectors. Collaborative research programmes funded by the EU focus on reducing the energy per bit for MRAM, aligning with the continent’s broader decarbonisation goals. Leading chip designers in Germany and France are leveraging this funding to integrate MRAM into safety‑critical control units, where deterministic performance is paramount. As supply chains diversify post‑Brexit, European firms are also establishing nearer‑term partnerships with Asian fabs to secure wafer capacity, ensuring that regional demand for industrial‑grade MRAM is met without disruption.

Asia-Pacific

The Asia-Pacific region combines massive manufacturing capacity with aggressive cost‑optimization pressures, prompting original equipment manufacturers to explore MRAM as a way to consolidate memory hierarchies. Semiconductor parks in Taiwan, South Korea, and Singapore host joint ventures that bridge design expertise with high‑volume foundry services. Simultaneously, rising automation in automotive assembly lines across China and India is creating a compelling use case for MRDA‑backed control logic that can survive harsh temperature swings. Government incentives targeting next‑generation computing platforms further motivate local firms to embed MRAM in industrial IoT gateways, positioning the region as a burgeoning growth engine for the market.

South America

While overall market size remains modest, Brazil and Argentina are witnessing incremental adoption of MRAM within the mining and oil‑&‑gas sectors, where equipment reliability dictates operational profitability. Local engineering consultancies are advocating for MRAM‑enabled edge devices that can retain configuration data through intermittent power supplies common in remote field sites. Trade agreements that lower tariff barriers for semiconductor imports are also encouraging Brazilian manufacturers to trial MRAM in predictive‑maintenance sensors, signaling the early stages of a niche but strategically important market segment.

Middle East & Africa

In the Middle East, sovereign wealth funds are allocating capital toward startups that specialize in robust memory solutions for autonomous drones and smart‑city infrastructure. The harsh desert environment drives demand for non‑volatile memory that can endure temperature extremes without data loss. Meanwhile, South Africa’s industrial automation sector is experimenting with MRAM‑based controllers to improve uptime in water‑treatment facilities. Collaborative initiatives between regional universities and global chip designers aim to cultivate a talent pipeline capable of sustaining the market’s technical complexity, laying groundwork for future expansion.

Report Scope

This market research report provides a comprehensive analysis of the Industrial MRAM (Magnetoresistive Random Access Memory) Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Industrial MRAM (Magnetoresistive Random Access Memory) Market?

-> Industrial MRAM (Magnetoresistive Random Access Memory) market is expected to reach USD 35,700 million by 2034

Which key companies operate in Industrial MRAM (Magnetoresistive Random Access Memory) Market?

-> Key players include Everspin Technologies, Samsung Electronics, Avalanche Technology, Spin Memory, Honeywell International, NVE Corporation, Shanghai Siproin Microelectronics, Wuhan Xinxin Semiconductor, IBM, SST, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for reliable non‑volatile memory in industrial automation, automotive electronics, aerospace & defense, edge computing, and the need for high endurance and fast write speed under harsh environmental conditions.

Which region dominates the market?

-> Asia-Pacific is the fastest‑growing region, while North America maintains a strong market share.

What are the emerging trends?

-> Emerging trends include increasing adoption of embedded MRAM (eMRAM) in system‑on‑chip designs, development of higher‑density MRAM modules, and integration of MRAM in AI‑enabled edge devices.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...