STN LCD Driver Market Insights

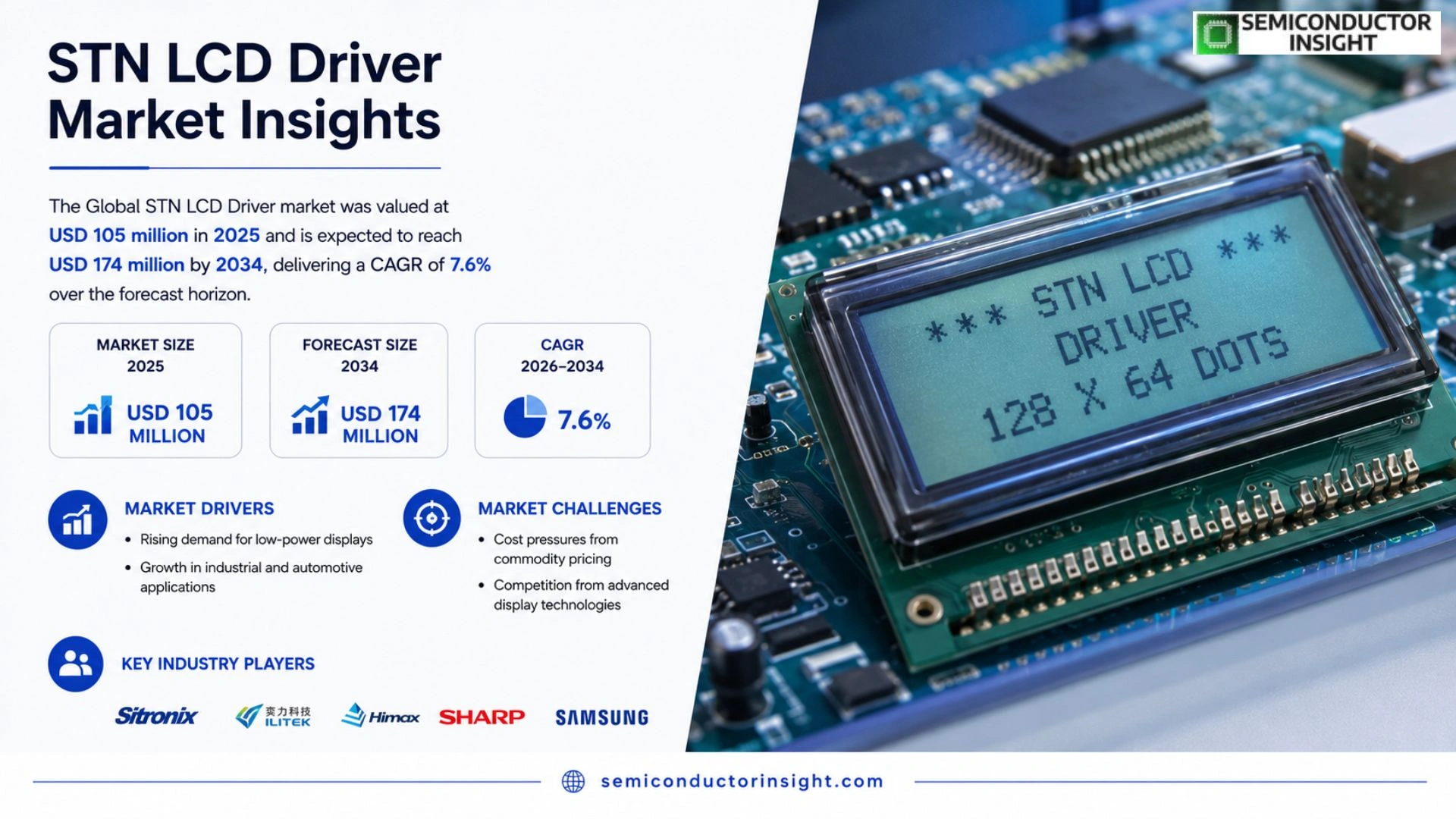

Global STN LCD Driver market was valued at USD 105 million in 2025 and is expected to reach USD 174 million by 2032, delivering a CAGR of 7.6 % over the forecast horizon.

An STN LCD Driver is a dedicated driver‑controller integrated circuit designed for passive monochrome LCD modules such as TN or STN panels. Its core functions include COM and SEG scanning, display RAM addressing, character or graphic data output, contrast‑bias voltage regulation, and host communication via I²C, SPI or parallel interfaces while maintaining low power draw, limited pin count and long operational life. Typical offerings range from low‑duty segment drivers to highly integrated graphic controllers that embed font ROM, key‑scan logic, LED drive or on‑chip VLCD generation, delivered in formats like COG or standard plastic packages.

MARKET DRIVERS

Rising Demand for Low‑Power Displays

The proliferation of battery‑operated gadgets,wearables, handheld diagnostics, and portable instrumentation,has heightened manufacturers’ focus on components that minimize power draw. STN LCD Driver architectures, known for their modest voltage requirements, directly address this need, making them a preferred choice in design specifications for STN LCD Driver Market.

Advancements in Thin‑Film Technology

Recent refinements in thin‑film transistor (TFT) processes have lowered defect rates and improved uniformity across large panels. These technical gains translate into longer product lifecycles and reduced warranty claims, allowing OEMs to justify higher unit costs for drivers that deliver reliable performance.

➤ “Manufacturers that integrate the latest low‑power driver solutions are seeing up to 15 % longer battery endurance in comparable devices.”

Beyond efficiency, regulatory pressures for energy‑conscious electronics in key regions have nudged design teams toward components that help meet stricter standby‑power limits, reinforcing the upward trajectory of driver adoption.

MARKET CHALLENGES

Cost Pressures from Commodity Pricing

Fluctuations in silicon and specialty substrate costs have squeezed margins for suppliers of STN LCD Driver units. While volume discounts can offset some pressure, smaller players often struggle to absorb price volatility, affecting their ability to innovate.

Other Challenges

Integration Complexity

Design teams must reconcile driver specifications with diverse panel technologies, requiring iterative firmware tuning that extends development timelines and raises engineering overhead.

MARKET RESTRAINTS

Emergence of Competing Display Technologies

The accelerating adoption of OLED and micro‑LED modules, which inherently integrate driver functionality, presents a structural limitation for STN LCD Driver Market. As end‑users prioritize ultra‑thin form factors and superior contrast ratios, the incremental value of traditional LCD drivers diminishes in certain high‑end segments.

MARKET OPPORTUNITIES

Expansion into Emerging IoT Devices

Internet‑of‑Things deployments,smart meters, remote sensors, and low‑cost diagnostic kits,still rely heavily on monochrome displays where STN LCD Driver solutions offer an optimal balance of cost, power, and durability. Targeted partnerships with IoT platform providers could unlock a sizeable new revenue stream.

Furthermore, regional initiatives to localize component sourcing in Southeast Asia and Eastern Europe are encouraging domestic manufacturers to adopt locally produced drivers, reducing lead times and opening channels for customized driver variants that meet specific regulatory or environmental standards.

STN LCD Driver Market Trends

Steady Demand from Industrial and Automotive Applications

STN LCD Driver Market is anchored by a cohort of end‑products that require long‑life, low‑power display interfaces. Automotive instrument clusters, industrial HMIs, and utility meters share common design constraints,continuous operation, minimal heat dissipation, and resistance to electromagnetic interference. As vehicle electrification and smart‑metering programs expand, designers favor passive LCD panels because they meet stringent temperature‑range specifications while keeping BOM costs modest. This preference translates into a reliable pipeline of design‑in events, rather than sporadic consumer‑driven spikes, which steadies revenue streams for component suppliers.

Other Trends

Integration and Feature Consolidation

Recent product releases illustrate a shift toward higher integration. Manufacturers now embed font ROM, key‑scan matrices, LED drivers, and on‑chip voltage regulators within a single STN LCD Driver package. By eliminating external discrete components, system architects reduce board space and simplify qualification processes. The added functionality also improves supply‑chain resilience; fewer parts mean fewer failure points and easier long‑term stocking for OEMs that operate on multi‑year production cycles.

Regional Supply Concentration and Long‑Term Partnerships

Supply dynamics remain clustered in East Asia, where legacy expertise in passive display technology is concentrated. Japanese and Taiwanese firms dominate design‑in relationships with automotive and industrial customers, leveraging decades‑long trust and established logistics networks. European players, while present, typically participate through broader LCD driver portfolios rather than dedicated STN solutions. This geographic concentration cushions the market against short‑term demand fluctuations because diversified end‑use segments,automotive, metering, medical, and appliance control,provide overlapping order books that smooth revenue variability across calendar years.

COMPETITIVE LANDSCAPE

Key Industry Players

STN LCD Driver Market – Competitive Overview

The segment is anchored by a handful of veterans whose product breadth spans low‑duty segment drivers to highly integrated graphic controllers. NXP Semiconductors leads the pack with a portfolio that couples robust voltage‑regulation blocks and extensive font‑ROM options, enabling OEMs in automotive instrument clusters to lock‑in a single‑chip solution for long product cycles. ROHM and Sitronix follow closely, offering complementary interfaces (I²C, SPI, parallel) that reduce board‑level complexity for industrial HMIs. Their dominance is reinforced by deep relationships with Taiwanese LCD module assemblers, guaranteeing supply continuity for utilities and medical terminals that cannot tolerate disruptions.

Beyond the incumbents, a cadre of niche innovators is reshaping the value chain. RAIO Technology and UltraChip focus on ultra‑low‑power variants tailored to battery‑operated meters, while Holtek and Solomon Systech supply cost‑effective drivers that integrate LED backlight and buzzer functions for home‑appliance panels. Emerging players such as Renesas Electronics and Toshiba’s display‑IC division are leveraging existing microcontroller ecosystems to embed STN drivers in multi‑function system‑on‑chips, a move that could lower BOM costs for smart‑meter manufacturers. The convergence of these efforts creates a market where differentiation stems from integration depth, temperature‑range certification, and long‑term obsolescence‑management rather than raw performance metrics.

List of Key STN LCD Driver Companies Profiled

- NXP Semiconductors

- ROHM Co., Ltd.

- Sitronix Technology Corporation

- RAIO Technology Inc.

- Solomon Systech (International) Limited

- UltraChip, Inc.

- Holtek Semiconductor Inc.

- Renesas Electronics Corporation

- Toshiba Electronic Devices & Storage

- Analog Devices, Inc.

- Microchip Technology Inc.

- Power Integrations, Inc.

- STMicroelectronics

- Fujitsu Semiconductor

- Samsung Electro‑Mechanics

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Integrated controller‑driver

|

| By Application |

|

Automotive & transportation electronics

|

| By End User |

|

Industrial equipment OEMs

|

| By Interface |

|

I²C/Serial interfaces

|

| By Package Form |

|

Chip‑on‑Glass (COG)

|

Regional Analysis: STN LCD Driver Market

North America

OEMs in the region prioritize driver designs that accommodate ultra‑low power modes, prompting suppliers to embed dynamic current‑limiting features. This focus drives a wave of bespoke solutions tailored to emerging wearable and handheld platforms.

Close proximity between fab facilities and major design houses reduces lead times, while diversified sourcing of passive components cushions the market against geopolitical shocks.

Stringent electromagnetic compatibility (EMC) requirements compel manufacturers to refine driver shielding strategies, influencing both layout choices and package materials.

End‑users increasingly demand longer battery life and wider temperature ranges, prompting a move toward drivers that integrate adaptive biasing and robust thermal protection.

Europe

European manufacturers leverage a strong tradition of precision engineering to refine STN LCD driver performance. Collaboration between semiconductor firms and automotive suppliers yields drivers that meet stringent reliability standards for cockpit displays. Furthermore, the region’s emphasis on circular economy principles encourages the reuse of driver modules in refurbished equipment, extending product lifecycles. Policy incentives aimed at reducing power consumption across consumer devices reinforce the adoption of low‑power driver architectures, prompting vendors to embed intelligent power‑management algorithms. The combined effect of technical expertise, regulatory encouragement, and sustainability focus positions Europe as a nuanced market where incremental improvements translate into competitive advantage.

Asia-Pacific

Asia‑Pacific stands out for its rapid expansion of consumer electronics manufacturing, which fuels demand for cost‑effective STN LCD drivers. Local fabs benefit from economies of scale, allowing them to offer competitive pricing without compromising essential performance attributes. Concurrently, the surge in smart‑city initiatives introduces a breadth of display applications,from public information panels to low‑cost surveillance screens,where STN drivers remain attractive due to their durability and energy profile. However, the market contends with fragmented standards adoption, prompting vendors to develop flexible driver families that can be customized for diverse voltage and interface requirements across the region’s varied industrial landscape.

South America

In South America, STN LCD Driver Market is shaped by the region’s growing adoption of portable diagnostic equipment and agricultural monitoring tools. Limited access to high‑end display technologies drives a reliance on STN panels, which offer sufficient contrast and readability under harsh lighting conditions. Local distributors play a pivotal role in bridging global driver designs with regional system integrators, often adding value through localized firmware adaptation. While macro‑economic volatility poses challenges, targeted government programs aimed at digitizing public services create pockets of demand that sustain driver sales in niche sectors.

Middle East & Africa

The Middle East & Africa region experiences modest but steady interest in STN LCD drivers, primarily driven by defense and oil‑field instrumentation where ruggedness and low power draw are paramount. Harsh environmental conditions necessitate drivers with enhanced temperature tolerance and robust protective coatings. Partnerships between regional engineering firms and multinational semiconductor suppliers have led to co‑development projects that fine‑tune driver parameters for desert‑grade operations. Although market size remains limited, the strategic importance of reliable display solutions in critical infrastructure ensures a consistent, if specialized, demand for STN LCD Driver Market in this area.

Report Scope

This market research report provides a comprehensive analysis of the STN LCD Driver Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of STN LCD Driver Market?

-> Global STN LCD Driver Market was valued at USD 105 million in 2025 and is expected to reach USD 174 million by 2032, growing at a CAGR of 7.6% during the forecast period.

Which key companies operate in STN LCD Driver Market?

-> Key players include NXP Semiconductors N.V., ROHM Co., Ltd., Sitronix Technology Corporation, RAIO Technology Inc., Solomon Systech (International) Limited, Ultra Chip, Inc., Holtek Semiconductor Inc..

What are the key growth drivers?

-> Key growth drivers include low power consumption, low BOM cost, higher integration, application‑specific optimization, policy support for smart metering and energy‑management, and the need for reliable, long‑life passive LCD solutions in industrial, automotive, and medical sectors.

Which region dominates the market?

-> Asia dominates STN LCD Driver market, driven by a strong supplier base in Japan, Taiwan, Hong Kong and extensive demand across automotive, industrial and metering applications.

What are the emerging trends?

-> Emerging trends include integration of RAM, font ROM, key‑scan, LED drive, buzzer control and on‑chip VLCD generation; reduction of external components; enhanced contrast stability; improved EMI robustness; wider temperature‑range operation; and flexible I2C, SPI and parallel interface compatibility.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...