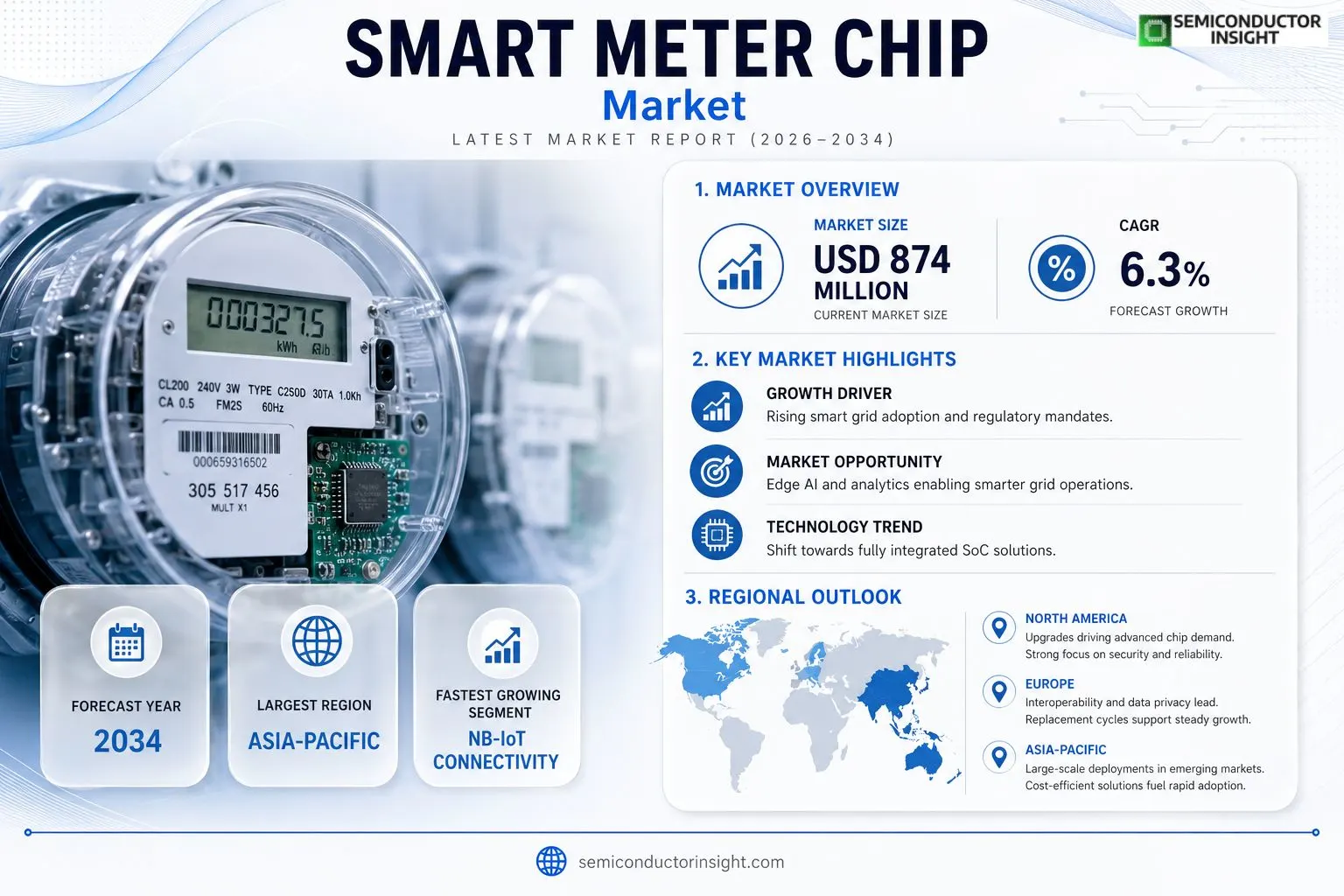

Smart Meter Chip Market Insights

Smart Meter Chip market was valued at USD 874 million in 2025 and is projected to reach USD 1,514 million by 2034, exhibiting a CAGR of 6.3 % during the forecast period.

A Smart Meter Chip is a semiconductor component embedded in electricity, water and gas meters that performs data acquisition, measurement calculation, processing, communication control and security management. It is typically realised as a microcontroller (MCU), metering IC or system‑on‑chip (SoC), providing the core intelligence required for accurate metering and network connectivity.Current production capacity stands near one billion units annually; in 2025 sales reached roughly 855 million units at an average price of USD 1.12 per unit, delivering an estimated gross margin of 38 %. Leading suppliers such as Texas Instruments, NXP Semiconductors and STMicroelectronics dominate high‑performance segments while Chinese manufacturers expand rapidly in cost‑sensitive markets.

MARKET DRIVERS

Regulatory Push for Grid Modernization

National electricity authorities are tightening inter‑connection standards, compelling utilities to replace legacy metering infrastructure. This regulatory climate forces investment in Smart Meter Chip Market solutions that can communicate consumption data in near‑real time, improve outage detection, and support dynamic pricing schemes. Companies that can certify their chips to meet these standards gain immediate market access.

Advances in Semiconductor Technology

Recent breakthroughs in low‑power silicon‑on‑insulator (SOI) processes have reduced energy draw of meter‑head chips by roughly 30 %. The efficiency gain translates into longer battery life for remote meters, lowering operational expenditures for utility operators. Vendors that adopt these processes can price their products more competitively while delivering higher reliability.

➤ Utility pilots in Europe have reported a 15 % reduction in maintenance visits after deploying next‑generation smart‑meter chips with built‑in self‑diagnostics.

These dynamics together create a fertile environment for chip manufacturers to scale production, leverage economies of scale, and negotiate longer‑term supply contracts with major utility groups.

MARKET CHALLENGES

Integration Complexity Across Diverse Grid Architectures

Utilities operate heterogeneous networks that span legacy analog devices, wireless mesh, and cellular back‑haul. Aligning a single chip architecture with such varied protocols demands extensive firmware customization, stretching development timelines and inflating R&D budgets.

Other Challenges

Supply‑Chain Vulnerabilities

shortages of specialty wafers and packaging materials have intermittently constrained the ability of chip makers to meet surge demand, prompting some operators to reconsider sourcing strategies.

MARKET RESTRAINTS

High Initial Capital Outlays

Deploying advanced metering infrastructure requires sizable upfront investment in both hardware and communication back‑haul. For utilities facing tight capital plans, the decision to upgrade chipsets can be deferred, tempering short‑term market expansion.

Stringent Certification Processes

Each chip must pass rigorous electromagnetic compatibility (EMC) and safety tests before field deployment. The time and expense associated with these certifications can deter smaller suppliers from entering Smart Meter Chip Market, consolidating supply among a few large players.

MARKET OPPORTUNITIES

Emergence of Edge‑AI Capabilities

Embedding lightweight machine‑learning inference engines directly onto meter chips opens pathways for on‑board fraud detection, demand‑response optimization, and predictive maintenance. Early adopters that package AI‑ready cores stand to capture premium contracts as utilities seek to enhance grid resilience without extensive backend upgrades.

Smart Meter Chip Market Trends

Integration and Connectivity Shift

The most visible change in Smart Meter Chip Market is the migration from separate micro‑controller and metering IC blocks toward fully integrated system‑on‑chip solutions. By consolidating measurement, processing, radio, and security functions on a single die, suppliers can cut bill‑of‑materials costs and meet the power‑budget constraints of next‑generation meters. The shift is reinforced by utility‑led pilots that demand over‑the‑air firmware updates and real‑time telemetry, capabilities that are cumbersome to implement with discrete components. Consequently, vendors that have already filed SoC roadmaps are capturing design wins in Europe and North America, while Chinese manufacturers are leveraging volume production to offer cost‑competitive alternatives for large‑scale rollouts in Asia.

Other Trends

Policy Support and Market Maturity

Regulatory frameworks across the OECD and emerging economies continue to mandate digital read‑outs for electricity, water, and gas distribution. In regions where the baseline penetration of smart meters exceeds 70 %, the focus has moved to replacement cycles and lifetime extensions. This environment creates a steady demand tail for chips that can retrofit older field units, explaining why many incumbents maintain parallel lines for legacy MCUs alongside their SoC portfolios. The policy backdrop also tempers price pressure, as utilities are often willing to pay a premium for chips that guarantee compliance with data‑privacy standards and anti‑tampering certifications.

Supply Chain Realignment

Upstream, the concentration of wafer fabs capable of advanced analog‑digital mixing has narrowed to a handful of players. Their capacity constraints are prompting chip designers to adopt multi‑source strategies, especially for silicon‑on‑insulator (SOI) substrates that improve low‑power performance. Downstream, smart‑meter assemblers are consolidating around a few large OEMs, which in turn enforce stricter qualification regimes for silicon vendors. This realignment reduces lead times for high‑volume orders but raises the barrier to entry for niche innovators lacking established fabs. Companies that can navigate both the foundry allocation process and the utility‑grade testing regime will be best positioned to translate the integration trend into sustained revenue streams.

COMPETITIVE LANDSCAPE

Key Industry Players

Smart Meter Chip: Competitive Dynamics in a Maturing Market

Texas Instruments, NXP and STMicroelectronics dominate the high‑performance segment of the smart‑meter chip arena. Their product portfolios combine advanced measurement cores, integrated communication stacks and hardened security blocks, enabling utilities to replace legacy meters without compromising reliability. The three firms leverage wafer‑foundry capacity and deep relationships with utility OEMs, translating into sizable design‑win ratios across North America and Europe. Their pricing power allows them to sustain margins despite incremental cost pressures from silicon‑process scaling. The market structure reflects a clear tiered hierarchy: a small group of multinational incumbents controls the majority of shipment volume in premium applications, while a broader set of regional players competes on cost and customization for emerging‑market deployments.Beyond the elite tier, a constellation of niche suppliers is reshaping the competitive set. Analog Devices and Renesas have introduced metering‑centric MCUs that emphasize low power draw and flexible firmware, appealing to water‑and‑gas meter manufacturers seeking longer battery life. Microchip Technology’s portfolio focuses on modular communication chips that support NB‑IoT and PLC, giving it traction in retrofit projects. Chinese firms such as Shanghai Belling, Hi‑trend Technology and Shanghai Fudan Microelectronics exploit domestic policy incentives to deliver price‑competitive SoC solutions, rapidly gaining foothold in China’s large‑scale rollout. CHIPSEA and Silicon Labs target the mid‑range market with security‑first designs that align with evolving regulatory requirements. Infineon’s emphasis on automotive‑grade safety standards provides an additional differentiator for utility partners concerned with tamper‑resistance. Collectively, these companies expand the choice set for system integrators, fostering price‑performance trade‑offs that accelerate overall market penetration.

List of Key Smart Meter Chip Companies Profiled

- Texas Instruments

- NXP Semiconductors

- STMicroelectronics

- Analog Devices

- Renesas Electronics

- Microchip Technology

- Infineon Technologies

- Silicon Labs

- CHIPSEA

- Shanghai Belling Corp

- Hi‑trend Technology (Shanghai)

- Shanghai Fudan Microelectronics

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Microcontroller (MCU) continues to dominate as the core logic element, driven by its flexibility and proven design ecosystem.

|

| By Application |

|

Residential applications drive the most diverse set of feature requirements, reflecting the broad deployment of smart electricity, water and gas meters in homes.

|

| By End User |

|

Electricity Utilities remain the primary end‑user, shaping product road‑maps around grid reliability and demand‑side management.

|

| By Integration Level |

|

Fully Integrated SoC is emerging as the strategic focal point for vendors aiming to combine measurement, processing and connectivity in a single die.

|

| By Connectivity Technology |

|

NB‑IoT is gaining traction as the preferred radio interface for new smart meter deployments.

|

Regional Analysis: Smart Meter Chip Market

North America

State‑level mandates in the U.S. and provincial statutes in Canada require granular consumption data, compelling utilities to upgrade to chips capable of handling frequent data bursts while preserving battery life. These rules also stipulate end‑to‑end encryption, pushing manufacturers toward integrated security blocks.

The migration from legacy 8‑bit MCUs to 32‑bit Cortex‑M platforms has accelerated, driven by the need for real‑time analytics and edge‑computing capabilities that support demand‑response programs without overburdening back‑office systems.

Domestic wafer fabs and specialty foundries have secured priority allocations for low‑power silicon, mitigating the impact of capacity constraints and ensuring a steady flow of components to meter manufacturers.

Leading chip makers are leveraging design‑win partnerships with major utility consultants, embedding proprietary diagnostics that enable predictive maintenance and creating a durable competitive moat.

Europe

European utilities are navigating a patchwork of national directives that prioritize energy efficiency and consumer empowerment. The push for interoperability across borders drives demand for chips that support multiple communication standards, from PLC to cellular NB‑IoT. Security expectations are heightened by GDPR‑aligned data‑privacy rules, prompting chip designers to embed tamper‑evident mechanisms at the silicon level. Collaborative initiatives such as the European Smart Metering Forum foster joint development programmes, allowing smaller OEMs to tap into shared IP libraries and accelerate time‑to‑market. As a result, Europe’s market dynamics favour flexible, multi‑protocol solutions that can be customized for each country’s regulatory nuances.

Asia‑Pacific

The Asia‑Pacific region exhibits a rapid build‑out of grid modernization projects, especially in China, India, and Southeast Asia. Utilities are prioritizing cost‑effective chips that deliver essential metering functions while maintaining low bill‑of‑materials, a necessity given the scale of deployments. Simultaneously, regional standards bodies are endorsing low‑power wide‑area network (LPWAN) protocols, encouraging manufacturers to incorporate ultra‑low‑power radio blocks. A growing emphasis on renewable integration forces utilities to adopt chips capable of handling bi‑directional flow data, supporting net‑metering schemes. The combination of volume‑driven pricing pressures and evolving communication needs shapes a competitive landscape where adaptability and price efficiency dominate.

South America

South American utilities are in the early phases of smart‑meter roll‑outs, often funded through multilateral development banks. The market rewards chips that can operate reliably in diverse climatic conditions, from tropical humidity to high‑altitude environments. Energy‑loss reduction targets lead utilities to seek chips with built‑in load‑profiling capabilities, enabling more accurate billing and loss detection. Moreover, the region’s slower internet penetration motivates the inclusion of offline data buffering within the chip architecture, ensuring data integrity despite intermittent connectivity.

Middle East & Africa

In the Middle East and Africa, smart‑meter initiatives are closely tied to national visions for diversified energy portfolios and water‑management strategies. Utilities value chips that combine metering with advanced analytics for peak‑load shaving, a critical function in markets with high climate‑driven demand spikes. Security considerations are paramount given the geopolitical context; therefore, hardware‑rooted encryption and secure boot processes are becoming baseline requirements. Limited local manufacturing capacity drives reliance on imported silicon, prompting regional distributors to negotiate long‑term supply contracts to guarantee component availability.

Report Scope

This market research report provides a comprehensive analysis of the Smart Meter Chip Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Smart Meter Chip Market?

-> Smart Meter Chip Market was valued at USD 874 million in 2025 and is expected to reach USD 1333 million by 2032, growing at a CAGR of 6.3% during the forecast period.

Which key companies operate in Smart Meter Chip Market?

-> Key players include Texas Instruments, NXP Semiconductors, STMicroelectronics, Analog Devices, Renesas Electronics, Microchip Technology, and leading Chinese vendors expanding in cost‑sensitive segments.

What are the key growth drivers?

-> Key growth drivers include smart‑grid deployment, regulatory mandates for energy efficiency, demand for accurate billing and resource management, rapid expansion of IoT and communication technologies such as NB‑IoT and LoRa, and the need for real‑time data for predictive maintenance.

Which region dominates the market?

-> Asia dominates the market, driven by large‑scale deployments in China, while Europe and North America focus on upgrades and replacement cycles.

What are the emerging trends?

-> Emerging trends include higher integration towards SoC solutions, lower power consumption, enhanced connectivity via NB‑IoT, RF and PLC, increased cybersecurity and anti‑tampering features, and the shift to intelligent, software‑defined metering platforms.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...