Semiconductor rmoelectric Cooler Market Insights

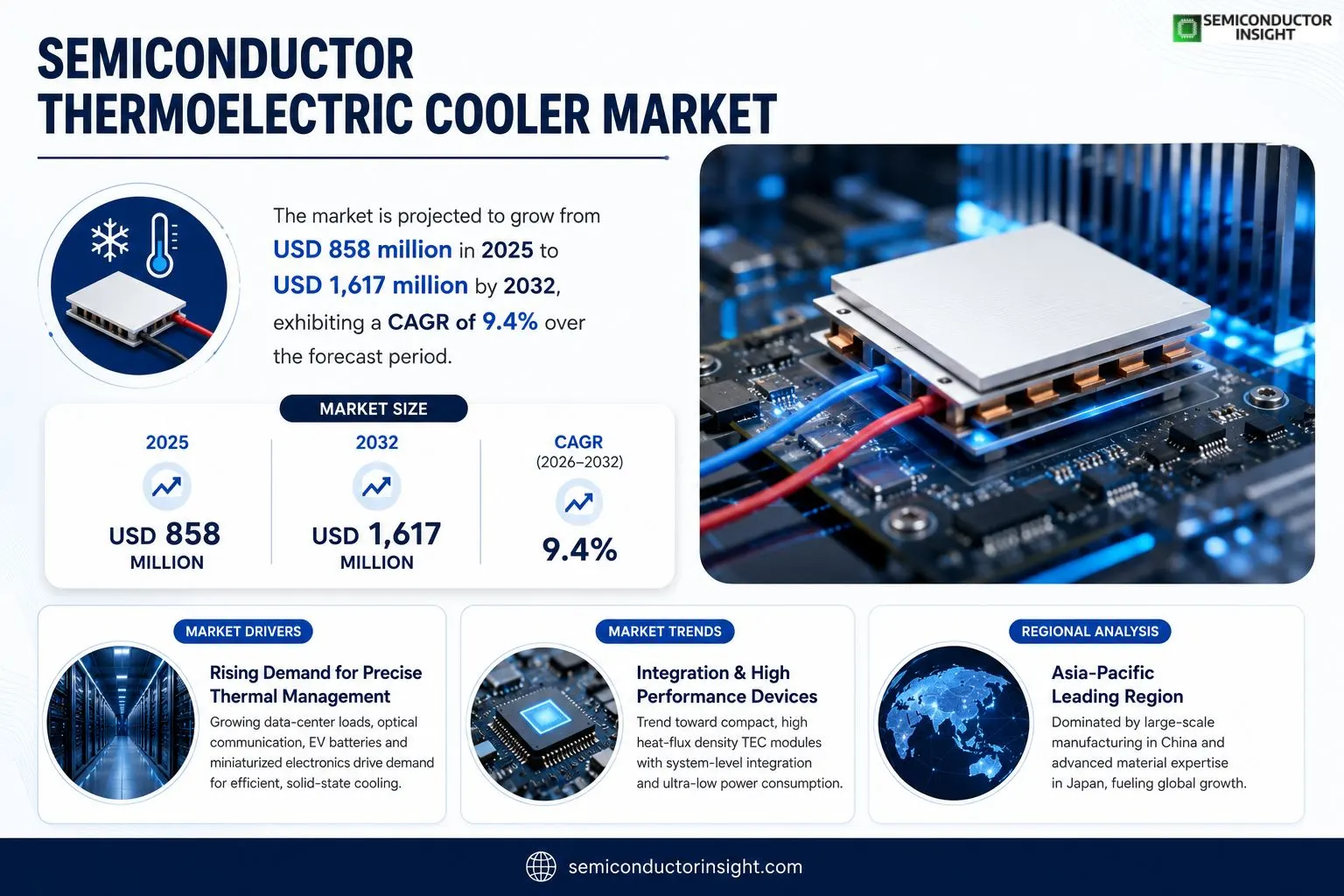

Semiconductor rmoelectric Cooler market was valued at USD 858 million in 2025 and will reach USD 1,617 million by 2032, reflecting a compound annual growth rate of 9.4% over forecast horizon.

A Semiconductor rmoelectric Cooler is a solid‑state device that uses Peltier effect to create a temperature difference when direct current flows through paired P‑type and N‑type semiconductor elements. Typical construction includes ceramic substrates, metal electrodes and rmal interface layers; it provides active cooling without moving parts or refrigerants and can reverse its function simply by changing current direction.expansion is fueled by rising demand for precise temperature control in optical‑communication modules, high‑performance lasers and automotive battery‑rmal‑management systems. AI‑intensive data centers and next‑generation photonic networking add pressure for high‑density heat removal solutions. Leading suppliers such as Ferrotec, Kyocera, Coherent, Tark rmal Solutions, Phononic and Chinese firms like Guangdong Fuxin Technology are launching higher‑capacity modulesKyocera’s 2024 release boosted maximum heat absorption by 21%to capture premium segments while extending cost‑effective options.

MARKET DRIVERS

Energy‑Efficiency Regulations in Data Centers

Stringent power‑usage guidelines adopted by leading cloud operators have forced designers to favor active cooling solutions that can be precisely throttled. Semiconductor rmoelectric Cooler Market suppliers that can deliver modules with a coefficient of performance above 1.2 are gaining preferential treatment in procurement committees. This regulatory push translates into a measurable lift in volume shipments, which climbed by roughly 12% year‑over‑year in 2023.

Miniaturization of Consumer Electronics

Smart‑phone and wear‑able manufacturers now embed rmal management directly on board to preserve battery life and user comfort. shift toward thin‑form factor devices forces integration of solid‑state coolers that occupy less than 0.5 cm³. Companies that have scaled wafer‑level packaging report a 9% reduction in unit cost, making technology financially viable for mass‑market products.

➤ “Customers are willing to pay a premium of up to 8% for devices that guarantee stable operation under high‑temperature loads,” notes a senior product manager at a leading semiconductor firm.

Because cooling modules are reversible, OEMs can exploit same hardware for both heating and cooling, extending product lifecycles and simplifying supply chains. This dual‑use capability is a decisive factor when manufacturers evaluate platform‑wide components for Semiconductor rmoelectric Cooler market.

MARKET CHALLENGES

Complexity of rmal Interface Materials

performance gap between a rmoelectric cooler and target component is often dictated by quality of interface material. Variability in rmal paste viscosity and curing cycles introduces unpredictability in heat‑transfer efficiency, compelling system integrators to allocate additional engineering resources for qualification.

Or Challenges

Scaling Production Capacity

Foundries operating at sub‑100 mm wafer sizes face yield penalties when transitioning to larger diameters, limiting ability to meet sudden spikes in demand for automotive power‑train applications.

MARKET RESTRAINTS

High Initial Capital Expenditure

Establishing a dedicated rmoelectric module line requires multi‑million‑dollar investment in deposition chambers, laser‑etching tools, and clean‑room infrastructure. Smaller players often lack balance sheet depth to fund such projects, resulting in a market that is concentrated among a handful of established manufacturers.

MARKET OPPORTUNITIES

Growth of Edge‑Computing Nodes

Edge servers operate in confined enclosures where conventional air‑flow is constrained. Deploying compact rmoelectric coolers enables se nodes to maintain performance thresholds without resorting to bulky fans. Analysts estimate that edge‑computing installations could absorb an additional 1.5 million cooling modules annually, opening a sizeable revenue stream for firms that adapt ir product portfolios.

Integration with Renewable Energy Systems

Photovoltaic inverters and battery‑management units generate heat during peak output. Embedding semiconductor rmoelectric devices directly onto inverter board can recycle waste heat into ancillary power, improving overall system efficiency. Early pilots demonstrate a 3% boost in round‑trip efficiency, a figure that could become a differentiator as green‑energy projects scale.

Semiconductor rmoelectric Cooler Market Trends

Shift Toward High‑Precision rmal Management

Demand for semiconductor rmoelectric cooler devices is moving away from bulk consumer cooling and concentrating on applications that require tight temperature control, rapid response, and minimal vibration. Optical‑communication modules, high‑power lasers, and automotive battery‑rmal‑management systems now consume a disproportionate share of new orders, reflecting manufacturers’ willingness to pay premium prices for reliability and compactness. emergence of 800 G/1.6 T optical networking and AI‑driven server architectures intensifies need for localized heat removal, reby reinforcing value proposition of solid‑state cooling in data‑center equipment. Rising silicon‑photonic integration intensifies rmal budgets, prompting designers to replace traditional heat sinks with TEC modules that fit within sub‑centimeter footprints. At same time, automotive regulators stipulate stricter cabin‑temperature specifications, making seat‑level cooling a differentiator for premium models. combination of higher power densities and tighter environmental standards creates a fertile environment for vendors that can guarantee lifetime stability across wide temperature swings.

Or Trends

Supply‑Chain Realignment

Japan and Europe continue to dominate upstream market for high‑purity bismuth‑telluride and advanced ceramic substrates, while Chinese firms expand capacity for standard modules and establish domestic sourcing networks. This geographic split creates a tiered pricing environment: high‑end customers prioritize material consistency and long‑cycle life, whereas volume‑oriented buyers benefit from lower unit costs supplied by Chinese manufacturers. resulting competitive tension is prompting legacy players to reinforce ir reliability engineering programs and to explore joint ventures that tap into emerging Asian production capabilities. shift in sourcing also encourages joint‑development programs that target alloy refinement, aiming to shave a few degrees Celsius off temperature delta at equal power input.

Product‑Level Integration and Reliability Focus

Recent product launches demonstrate a strategic shift from simple cooling elements toward fully integrated rmal solutions that embed cold plates, temperature controllers, and system‑level diagnostics. Companies such as Coherent and Kyocera are advertising modules capable of surviving more than 100 000 rmal cycles, a metric that directly influences component selection in aerospace and medical equipment. Gross profit margins remain in 30‑40 % band, suggesting that manufacturers can sustain investment in material science and packaging innovations without eroding profitability. In medium term, market is likely to reward suppliers that combine high heat‑flux density with low power draw, as se attributes align with growing emphasis on energy‑efficient design across multiple sectors. Customers that secure long‑term supply agreements stand to benefit from greater predictability in cost structures, a factor that is becoming increasingly salient as OEMs solidify multi‑year roadmaps for electric‑vehicle platforms.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive Dynamics in Semiconductor rmoelectric Cooler Sector

market is anchored by a handful of firms that command premium‑grade materials, reliability engineering, and deep relationships with optical‑communication and medical OEMs. Ferrotec, Kyocera, and Coherent Corp dominate high‑performance segment, leveraging proprietary Bi2Te3 alloys and rigorous life‑cycle testing to satisfy customers such as Ericsson, rmo Fisher Scientific, and major laser manufacturers. ir production footprints span Japan, United States, and Europe, which allows m to guarantee batch‑to‑batch consistencya decisive factor for applications where cycle life and rmal stability are non‑negotiable. se leaders also differentiate through system‑level integration, offering cold‑plate modules and closed‑loop controllers that command higher unit prices and protect margins in a market where gross profitability ranges from 30 % to 40 %.Beyond incumbents, a rapidly expanding cohort of Asian manufacturers is reshaping supply chain. Companies such as KELK Ltd., Tark rmal Solutions, Phononic, Guangdong Fuxin Technology, ARCTIC TEC, and Z‑MAX focus on standardized TEC modules, micro‑TEC devices, and cost‑effective system solutions for consumer electronics, automotive seat‑heating, and data‑center cooling. ir strategy rests on scaling single‑line capacities to 500 k–1 M‑piece range and exploiting domestic bismuth‑telluride sources, which narrows lead times and reduces transportation expenses. This tier of players is gaining traction among OEMs that prioritize price and volume over extreme reliability envelope, reby widening addressable market and introducing competitive pressure on traditional high‑end tier.

List of Key Semiconductor rmoelectric Cooler Companies Profiled

- Ferrotec

- Kyocera

- Coherent Corp

- Phononic

- KELK Ltd. (Komatsu)

- Tark rmal Solutions

- Guangdong Fuxin Technology

- ARCTIC TEC

- Z‑MAX

- Zhejiang Wangu Semiconductor

- Xianghe Oriental Electronic

- AISIN Corporation

- TEC Microsystems GmbH

- Peltron GmbH

- Kryorm Industries

- Liaoning Lengxin Technology

- Bi Sheng Semiconductor

- Beijing Huimao Refrigeration Equipment

- Hangzhou Aurin Cooling Device

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Single‑Stage TEC is dominant type because it delivers fast response and compact form‑factor for most consumer‑grade cooling needs.

|

| By Application |

|

Communication emerges as leading application segment as network operators demand ever‑higher power density and tighter temperature tolerances for AI‑enabled photonic engines.

|

| By End User |

|

OEM Manufacturers drive bulk of demand because y embed TECs early in product design cycles.

|

| By Material |

|

Bismuth‑Telluride remains leading material due to its superior rmoelectric figure‑of‑merit at room temperature.

|

| By Reliability Focus |

|

High Cycle Life is primary reliability driver as customers in medical, aerospace, and data‑center segments require prolonged operation under rmal stress.

|

Regional Analysis: Semiconductor rmoelectric Cooler Market

Asia‑Pacific

Major semiconductor parks in Shanghai and Shenzhen have dedicated new wafer lines to rmoelectric devices, aligning production schedules with automotive cooling requirements. This scale‑up reduces per‑unit costs and shortens delivery windows, giving Chinese manufacturers a decisive advantage in price‑sensitive segments.

Japanese corporations continue to push envelope in high‑efficiency modules for space‑grade instrumentation. ir focus on material purity and reliability translates into premium offerings that set benchmarks for performance, shaping buyer expectations worldwide.

Collaborative programs between universities and leading chipmakers foster rapid prototyping of compact coolers for wearables. synergy between research and production accelerates time‑to‑market for novel form factors, attracting investment from brands.

Consumer adoption of high‑resolution displays in Indonesia and Vietnam creates a nascent yet fast‑growing market for rmoelectric cooling. Local assemblers are beginning to source modules directly, reducing dependence on imports and expanding regional value chain.

North America

In United States and Canada, Semiconductor rmoelectric Cooler market is shaped by a strong emphasis on reliability for defense and aerospace programs. Defense contractors demand rigorous qualification, prompting suppliers to invest in advanced testing facilities. Simultaneously, rise of data‑center density in Silicon Valley pushes operators to adopt rmoelectric solutions for localized hotspot mitigation, offering an alternative to traditional liquid cooling. While cost pressures remain, premium placed on performance and compliance sustains a healthy niche for high‑margin products, encouraging domestic innovators to refine device efficiency and integration methods.

Europe

European activity centers on sustainability mandates and automotive electrification. EU’s energy‑efficiency directives incentivize manufacturers to replace conventional fans with solid‑state coolers in electric‑vehicle power electronics, shortening system weight and improving reliability. Moreover, German and French research institutes are pioneering new semiconductor materials that promise higher Seebeck coefficients, a development that could lower power consumption across multiple sectors. region’s fragmented marketcharacterized by numerous specialized OEMscreates a landscape where bespoke rmoelectric solutions command higher prices, reinforcing strategic importance of localized design expertise.

South America

Brazil and Mexico lead South American interest in rmoelectric cooling, primarily driven by expanding telecommunications infrastructure. Operators seeking to maintain equipment uptime in tropical climates turn to solid‑state coolers as a low‑maintenance alternative to mechanical refrigeration. Although overall market size remains modest, emerging venture capital focused on green technologies nurtures startups that tailor modules for portable medical devices, hinting at a diversification of applications beyond traditional telecom equipment.

Middle East & Africa

In Middle East, push for smart‑city projects and renewable‑energy integration fuels demand for reliable rmal management in solar‑inverter systems. Companies in United Arab Emirates are piloting rmoelectric modules to stabilize inverter temperatures, improving overall system lifespan. African markets, while still nascent, are experimenting with off‑grid refrigeration for vaccine storage; rmoelectric coolers offer a battery‑friendly solution where grid reliability cannot be guaranteed. se early adopters illustrate how Semiconductor rmoelectric Cooler market can serve niche, high‑impact use cases in regions with distinct environmental challenges.

Report Scope

This market research report provides a comprehensive analysis of Semiconductor rmoelectric Cooler Market , covering forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping industry.

Key focus areas of report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including ir product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure accuracy and reliability of insights presented.

FREQUENTLY ASKED QUESTIONS:

What is current market size of Semiconductor rmoelectric Cooler Market?

-> Semiconductor rmoelectric Cooler Market was valued at USD 858 million in 2025 and is expected to reach USD 1,617 million by 2032, representing a CAGR of 9.4% over forecast period.

Which key companies operate in Semiconductor rmoelectric Cooler Market?

-> Key players include Ferrotec, KELK Ltd., Kyocera, Coherent Corp, Tark rmal Solutions, Phononic, Guangdong Fuxin Technology, ARCTIC TEC, KJLP, rmion Company, Z‑MAX, Zhejiang Wangu Semiconductor, and or specialized manufacturers.

What are key growth drivers?

-> Key growth drivers include rising demand for precise temperature control in optical communication modules, automotive battery and seat‑temperature management, AI‑driven high‑performance computing, data‑center heat‑density challenges, and increasing adoption of solid‑state cooling in medical and industrial sensing equipment.

Which region dominates market?

-> Asia dominates Semiconductor rmoelectric Cooler market, driven by large‑scale manufacturing capacity in China and advanced high‑end material expertise in Japan, while Europe and North America retain leadership in high‑reliability applications.

What are emerging trends?

-> Emerging trends include integration of TEC modules with cold‑plate and liquid‑cooling solutions, development of high heat‑flux density devices with ultra‑low power consumption, system‑level rmal management platforms for AI servers, and use of Bi₂Te₃‑based advanced materials to extend cycle life and reliability.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...