AI Smart Glasses Chip Market Insights

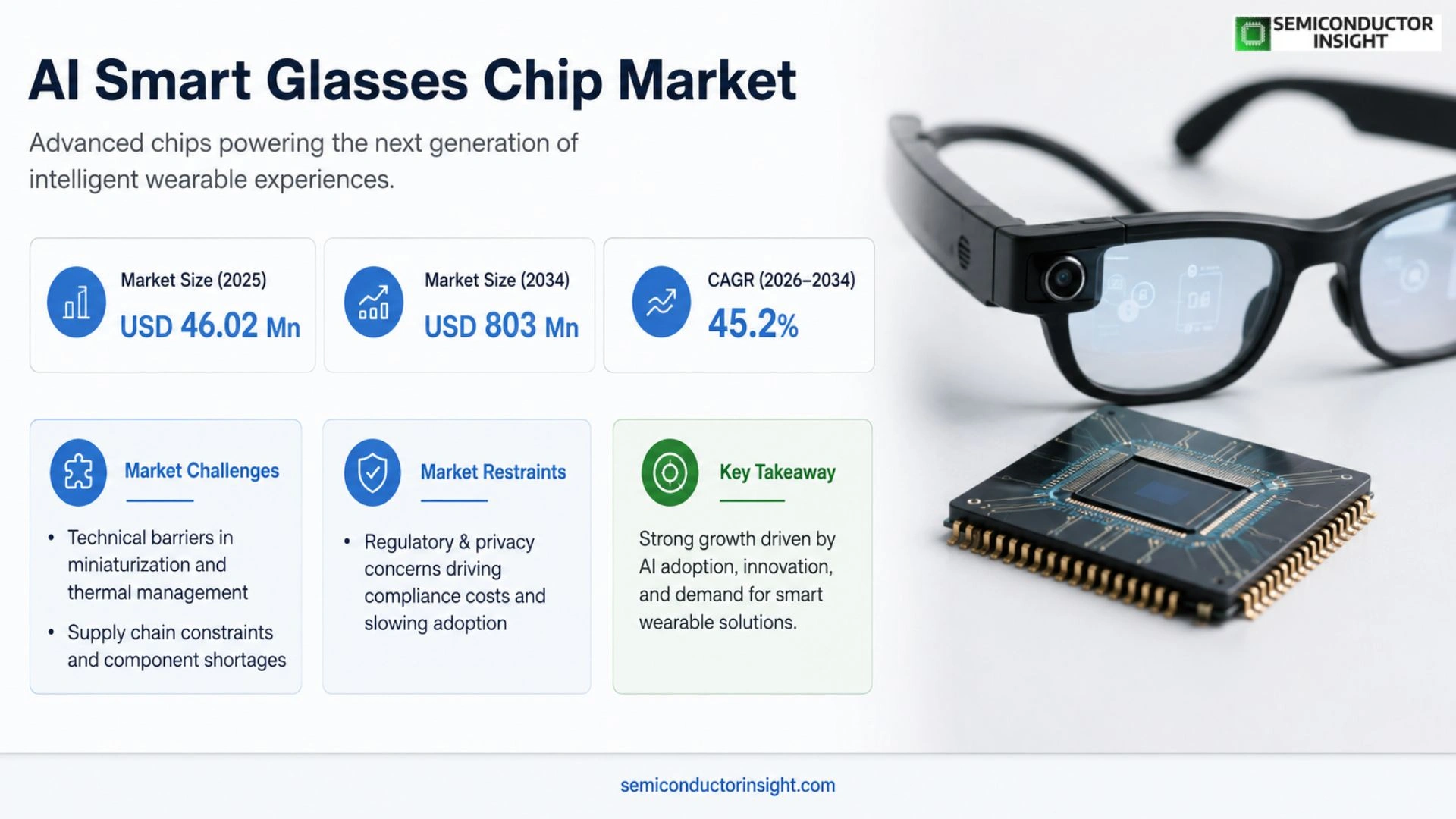

Global AI Smart Glasses Chip market was valued at USD 46.02 million in 2025 and reached USD 803 million by 2034, reflecting a compound annual growth rate of 45.2% over the period.

An AI smart glasses chip is a highly integrated system‑on‑chip designed for eyewear devices that require on‑device artificial intelligence. It combines a general‑purpose CPU, neural processing unit (NPU), graphics/image engine, display controller, audio processor, memory interfaces, sensor‑fusion logic and wireless connectivity on a single die. The architecture prioritises ultra‑low power consumption, compact footprint and real‑time inference so that functions such as computer vision, voice interaction and spatial positioning operate within the tight battery and thermal limits of glasses.

The market expands because wearable augmented reality adoption accelerates in consumer entertainment and enterprise training, while advances in semiconductor process nodes (4 nm–5 nm) improve energy efficiency enough for prolonged use on head‑mounted platforms. Upstream suppliers such as TSMC for advanced wafers and Samsung for memory enable the supply chain, whereas midstream designers,including Qualcomm, MediaTek and NXP,deliver customized SoCs to OEMs. Downstream adoption by leading smart‑glasses brands fuels demand, creating opportunities for new entrants that can meet stringent power‑budget requirements.

MARKET DRIVERS

Advances in Edge AI Processing

The emergence of ultra‑low‑power neural engines has enabled AI Smart Glasses Chip Market participants to embed sophisticated perception algorithms directly on the frame. By shifting inference from cloud to device, manufacturers can deliver sub‑second response times, a factor that end‑users increasingly regard as essential for seamless augmented experiences. Consumer tolerance for latency has become a decisive metric, pushing vendors to adopt next‑gen silicon that balances compute density with battery endurance.

Integration with Wearable Ecosystems

Strategic alliances between chipset designers and leading wearable platforms are accelerating the diffusion of smart‑glass solutions across health, logistics, and field service domains. When a chip can speak the same protocol as smart watches or IoT hubs, deployment cycles shorten dramatically, and the overall value proposition becomes more compelling for enterprise buyers. This cross‑device harmony is turning smart glasses from niche accessories into integral components of broader digital workspaces.

➤ “The convergence of on‑device AI and standardized wear‑able connectivity is the single most decisive catalyst reshaping AI Smart Glasses Chip Market today.”

Manufacturers that can fuse high‑resolution sensor fusion with real‑time decision engines are positioned to capture premium segments where accuracy and reliability outweigh cost considerations. As organizations prioritize data security and edge compliance, the demand for chips that guarantee on‑premise processing is set to intensify, reinforcing this market’s upward trajectory.

MARKET CHALLENGES

Technical Barriers to Miniaturization

Designing chips that fit within the thin‑profile frames of smart glasses while still delivering adequate thermal management remains a persistent hurdle. Engineers must reconcile the heat generated by AI inference with the limited surface area available for dissipation, often resorting to exotic materials that raise production complexity.

Other Challenges

Supply Chain Constraints

The reliance on rare‑earth substrates and advanced lithography steps has exposed AI Smart Glasses Chip Market to geopolitical volatility. Recent semiconductor shortages have elongated lead times, compelling OEMs to hold larger inventories or redesign modules to accommodate alternative components.

MARKET RESTRAINTS

Regulatory and Privacy Concerns

Data captured by on‑body cameras and microphones is subject to stringent privacy statutes across key regions. Legislators are tightening consent requirements, which forces chip manufacturers to embed robust encryption and on‑device anonymization features. These added compliance layers inflate development costs and may deter early‑stage adopters wary of legal exposure.

MARKET OPPORTUNITIES

Enterprise Use Cases in Remote Assistance

Industries such as aerospace maintenance, surgical training, and field engineering are actively piloting AI‑enhanced smart glasses to reduce error rates and accelerate knowledge transfer. The chips that power these devices must support high‑definition video overlay, real‑time language translation, and secure edge analytics. Companies that can deliver a turnkey silicon solution aligned with these operational demands stand to secure multi‑year contracts and shape a sizable portion of AI Smart Glasses Chip Market’s future growth.

AI Smart Glasses Chip Market Trends

Integration of AI Acceleration in Wearable SoCs

The newest generation of chips designed for smart‑glasses now embeds a dedicated neural‑processing unit alongside a lightweight CPU. This architecture enables on‑device inference for vision and voice tasks while keeping power draw within the strict envelope of eyewear batteries. Manufacturers are prioritising architectures that combine image signal processing, sensor fusion and communications in a single die, because the resulting form factor satisfies both ergonomic and thermal constraints. The transition from discrete components to monolithic solutions is reshaping design cycles: OEMs can shorten time‑to‑market, while system integrators gain tighter control over latency, a decisive factor for applications such as real‑time translation and augmented reality overlays.

Other Trends

Supply‑Chain Consolidation

Upstream, the reliance on a narrow set of advanced‑node foundries and memory providers is intensifying. Companies that secure multi‑year capacity in 4‑5 nm processes can differentiate by offering higher compute density without compromising the thin profile demanded by eyewear. Meanwhile, packaging specialists that master fan‑out wafer‑level solutions are becoming pivotal, as they deliver the thermal dissipation required for continuous AI workloads. Downstream, a handful of enterprise‑focused smart‑glasses brands are locking in exclusive silicon partners, which is prompting smaller designers to pursue niche verticals such as medical imaging or field‑service assistance.

Shift Toward Edge‑Optimized Architectures

Because smart‑glasses operate in environments where network connectivity is intermittent, vendors are engineering chips that execute the majority of AI models locally. Edge‑centric designs reduce reliance on cloud latency, preserve user privacy, and lower data‑plan expenses. This trend is prompting a re‑evaluation of software stacks: developers are adopting quantised neural networks and pruning techniques to fit sophisticated algorithms into the limited SRAM budgets of wearable SoCs. The business implication is clear,players that align their hardware roadmaps with edge‑first AI frameworks will capture the premium segment of customers demanding seamless, always‑on experiences.

COMPETITIVE LANDSCAPE

Key Industry Players

AI Smart Glasses Chip Market: Competitive Overview

In the upper tier of the AI smart‑glasses chip arena, Qualcomm, MediaTek and NXP dominate the design ecosystem. Their platforms integrate a CPU, neural‑processing unit, graphics block and wireless stack on a single die, delivering the performance‑per‑watt ratios that OEMs demand for battery‑constrained eyewear. By leveraging long‑standing relationships with leading foundries such as TSMC and Samsung, these three firms secure early access to leading‑edge process nodes, enabling them to offer sub‑5 nm solutions that keep thermal budgets in check. Their market share is reinforced by extensive software toolchains and reference designs that accelerate time‑to‑market for consumer‑grade smart glasses, giving them pricing leverage and a strong foothold in both the U.S. and Chinese high‑volume segments.

The remainder of the landscape is populated by a diverse set of specialists that address niche requirements or regional market segments. Ambiq and Nordic Semiconductor have carved out a reputation for ultra‑low‑power architectures, making them attractive to enterprise‑focused wearables where battery life is paramount. Companies such as Bestechnic, Unisoc, Fullhan Microelectronics, StarFive Technology and SigmaStar provide cost‑effective SoCs that emphasize integrated sensor interfaces and compact packaging, appealing to emerging manufacturers in Southeast Asia and Africa. Rockchip, Espressif, Ingenic Semiconductor, Allwinner and Hunan Goke round out the field with flexible licensing models and strong ties to domestic supply chains, allowing them to respond quickly to local demand spikes and regulatory nuances.

List of Key AI Smart Glasses Chip Companies Profiled

- Qualcomm

- MediaTek

- NXP

- Ambiq

- Nordic Semiconductor

- Bestechnic

- Unisoc

- Fullhan Microelectronics

- StarFive Technology

- SigmaStar

- Rockchip

- Espressif

- Ingenic Semiconductor

- Allwinner

- Hunan Goke

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

4nm‑5nm is emerging as the leading technology tier because:

These attributes are driving OEMs to prioritize the most advanced nodes despite higher design complexity. |

| By Application |

|

Consumer retains primacy because:

Enterprise and medical applications are gaining traction, yet consumer‑centric feature sets still shape the overall product roadmap. |

| By End User |

|

Individual Consumers dominate the end‑user landscape due to:

Corporate deployments focus on productivity and safety, while healthcare users prioritize precision sensing, both of which are emerging niches. |

| By Integration Level |

|

Full SoC is the preferred integration because:

Hybrid approaches serve cost‑sensitive designs but often sacrifice the seamless experience of a monolithic SoC. |

| By Distribution Channel |

|

Direct OEM Partnerships drive market momentum because:

Distributor and integrator channels complement the ecosystem by reaching niche verticals and regional markets. |

Regional Analysis: AI Smart Glasses Chip Market

North America

The region leverages a legacy of advanced wafer fabs that have been retooled for heterogeneous integration, shortening the lead‑time from design to silicon. Proximity of fabs to design houses reduces logistics overhead and enables rapid iteration, a critical factor for AI‑enabled vision chips where every nanosecond counts.

Universities and research labs in the corridor between Silicon Valley and Boston continuously feed the market with PhD‑level talent skilled in computer vision, low‑power architecture, and neuromorphic computing, thereby sustaining a pipeline of proprietary algorithms that differentiate chip offerings.

Early‑adopter enterprises in logistics, healthcare, and field services are piloting AI‑powered glasses to augment worker productivity, creating a feedback loop that informs hardware refinements and fuels broader market confidence.

Harmonised safety standards and streamlined FCC approval pathways lower entry barriers for manufacturers, encouraging a steady influx of new designs that keep AI Smart Glasses Chip Market dynamic and responsive to emerging use‑cases.

Europe

European nations are leveraging strong cross‑border collaborations to nurture a fragmented but innovative chip landscape. Initiatives such as the European Chips Act funnel public funds into joint R&D programs focused on energy‑efficient vision processors, aligning with the continent’s broader sustainability agenda. While scale remains lower than North America, niche players excel in custom ASICs designed for specific industry verticals,particularly automotive and aerospace,where safety certifications dovetail with AI‑driven optics. Intellectual property regimes across the EU also provide a protective backdrop that encourages incumbents to invest in proprietary AI inference engines embedded within glasses. Consequently, the region is carving a specialty niche that complements larger volume markets, positioning itself as a source of differentiated technology rather than sheer output.

Asia‑Pacific

The Asia‑Pacific arena is distinguished by rapid consumer adoption of wearable technologies and aggressive cost‑targeting by manufacturers. China’s expansive foundry capacity, combined with aggressive government incentives for AI hardware, fuels a surge in volume‑oriented chip designs that prioritize low cost over absolute performance. Meanwhile, Japan and South Korea contribute high‑precision imaging expertise, leading to hybrid solutions that blend superior optics with AI acceleration. The market here is driven less by regulatory uniformity and more by a race to capture market share in emerging sectors such as smart retail and entertainment. This competitive pressure accelerates product cycles, compelling vendors to balance price competitiveness with incremental functional upgrades in AI Smart Glasses Chip Market.

South America

South American markets are still nascent but exhibit growing interest as multinational firms establish regional testbeds for AI‑enhanced augmented reality in field service operations. Brazil’s sizable manufacturing base offers a low‑cost assembly platform, yet the region lacks a deep design ecosystem, relying heavily on technology imports. Nevertheless, local universities are beginning to launch specialised programmes in embedded AI, which could seed home‑grown talent over the next decade. Governmental push for digital transformation in logistics and agriculture hints at future demand for ruggedized smart‑glass solutions, suggesting a gradual but steady ascent in market relevance.

Middle East & Africa

In the Middle East & Africa, strategic investments in smart‑city infrastructure and defense modernization present unique entry points for AI Smart Glasses Chip Market. Gulf Cooperation Council states allocate substantial budgets toward advanced command‑and‑control platforms, where AI‑augmented vision is a priority. Africa’s burgeoning telecom expansions also create a peripheral demand for low‑power chips that can operate on limited energy grids. While the region’s overall manufacturing footprint remains limited, partnerships with Asian fab operators enable local assemblers to offer competitive solutions, laying groundwork for a modest but growing market segment.

Report Scope

This market research report provides a comprehensive analysis of the AI Smart Glasses Chip Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of AI Smart Glasses Chip Market?

-> AI Smart Glasses Chip market was valued at USD 803 million by 2034, reflecting a compound annual growth rate of 45.2% over the period.

Which key companies operate in AI Smart Glasses Chip Market?

-> Key players include Qualcomm, NXP, MediaTek, Ambiq, Nordic Semiconductor, Bestechnic, Unisoc, Fullhan Microelectronics, StarFive Technology, SigmaStar, among others.

What are the key growth drivers?

-> Key growth drivers include rising adoption of AI‑enabled smart glasses in consumer and enterprise segments, increasing demand for ultra‑low‑power SoCs, advances in on‑device AI inference, and the need for compact, energy‑efficient designs.

Which region dominates the market?

-> North America and Asia lead the market, with the United States and China representing the largest individual country markets.

What are the emerging trends?

-> Emerging trends include migration to 4nm‑5nm process nodes, integration of SoC+MCU solutions, and expanded edge‑AI capabilities for real‑time vision and voice interaction in smart‑glasses.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...