Semiconductor Peltier Module Market Insights

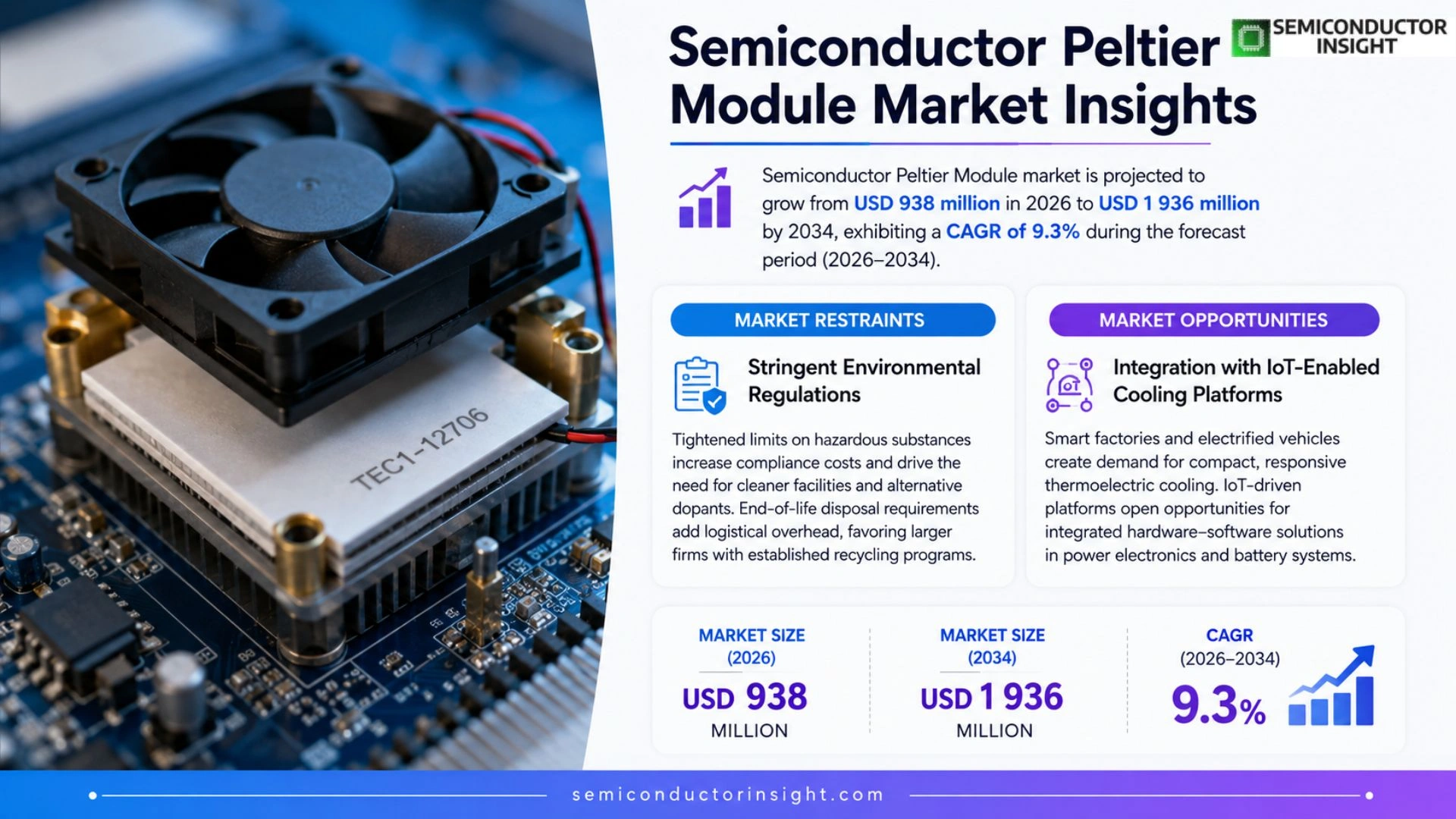

Global Semiconductor Peltier Module market size was valued at USD 858 million in 2025. The market is projected to grow from USD 938 million in 2026 to USD 1 936 million by 2034, exhibiting a CAGR of 9.3% during the forecast period.

A Semiconductor Peltier Module is a solid‑state thermal‑management device that exploits the Peltier effect to deliver active cooling and precise temperature control without moving parts or refrigerants. It consists of alternating p‑type and n‑type thermoelectric semiconductor elements bonded to ceramic substrates and equipped with electrodes and thermal interface layers; when direct current passes through, one side absorbs heat while the opposite side dissipates it.

The upward trajectory is driven by expanding demand in optical communications, high‑performance lasers, AI‑enabled data centers, and automotive battery thermal management, where compact size, fast response and reversible heating/cooling are essential.

MARKET DRIVERS

Rising Demand for Thermal Management Solutions

Manufacturers of power‑dense equipment are increasingly turning to thermoelectric cooling to meet the tight thermal envelopes of next‑generation processors. The shift away from traditional fan‑based systems reduces acoustic noise and maintenance costs, prompting OEMs to embed Semiconductor Peltier Module Market offerings directly into chassis designs. This preference is reinforced by the need for precise temperature control in data‑center racks, where even a 1 °C variation can affect uptime.

Growth of Renewable Energy Systems

Photovoltaic farms and concentrated solar power installations rely on active cooling to preserve inverter efficiency under harsh sunlight. As renewable capacity expands, the requirement for compact, low‑maintenance thermoelectric modules rises, driving new engineering specifications that favor semiconductor‑based solutions. In parallel, wind‑turbine power electronics benefit from point‑source cooling that mitigates degradation caused by temperature cycling.

➤ “Thermoelectric modules are becoming the default choice for niche cooling where space, reliability, and silent operation outweigh raw efficiency.”

The convergence of these forces is reshaping procurement strategies; suppliers that can guarantee material purity and scalable production are securing multi‑year contracts, while end‑users report lowered total‑cost‑of‑ownership thanks to reduced service intervals.

MARKET CHALLENGES

Supply Constraints for High‑Purity Semiconductor Materials

Demand for gallium‑arsenide and bismuth‑telluride wafers has outstripped the output of a limited number of certified fabs. This bottleneck elevates lead times and inflates unit prices, especially for modules targeting high‑efficiency applications. Companies that lack direct access to wafer manufacturers are forced to rely on intermediaries, which adds complexity to their supply chain.

Other Challenges

Cost Competitiveness

The capital expense of thermoelectric assemblies remains higher than that of conventional heat‑sink solutions. While operating savings are evident, many customers hesitate to adopt the technology unless they can demonstrate a clear return‑on‑investment within a short horizon.

MARKET RESTRAINTS

Stringent Environmental Regulations

Regulatory bodies in Europe and North America have tightened limits on hazardous substances used in semiconductor processing. Compliance drives up production costs, as manufacturers must invest in cleaner‑room facilities and adopt alternative dopants that may affect module performance.

Moreover, end‑of‑life disposal requirements compel manufacturers to develop take‑back programs, adding logistical overhead that smaller players often cannot absorb. This environment favors larger firms with established recycling infrastructure.

MARKET OPPORTUNITIES

Integration with IoT‑Enabled Cooling Platforms

Smart factories are deploying sensor‑driven thermal management networks that dynamically adjust cooling output based on real‑time load data. Thermoelectric modules, with their rapid response time, fit naturally into these closed‑loop systems, opening a revenue stream for vendors able to provide integrated hardware‑software bundles.

The automotive sector’s transition to electrified drivetrains creates a niche for compact cooling of power‑electronics and battery‑management units. As vehicle architectures shrink, space‑efficient Peltier devices become attractive alternatives to bulky liquid‑cooling loops.

Medical imaging equipment, particularly portable MRI and CT units, require stable temperature environments to maintain calibration. Embedding semiconductor‑based cooling allows manufacturers to meet stringent health‑care standards while keeping device weight within transportable limits, representing a growing segment for specialized module designs.

Semiconductor Peltier Module Market Trends

Shift Toward High‑Precision Thermal Management

Semiconductor Peltier Module Market is increasingly anchored in applications that demand tight temperature control, such as laser communication, advanced medical diagnostics, and electric‑vehicle battery packs. Manufacturers are introducing modules with heat‑absorption capacities up to 21 % higher than legacy products, a response to the escalating thermal densities in AI‑computing platforms and 800 Gb/s optical networking equipment. This transition is not merely a volume story; it reshapes product pricing, as customers are willing to pay premiums for units that combine compact form factors with extended cycle life and low power draw. Consequently, firms that pair thermoelectric innovation with system‑level integration are gaining a decisive edge.

Other Trends

Material Supply Landscape

From a supply standpoint, Japanese and European firms continue to dominate high‑grade bismuth‑telluride alloys and precision‑engineered ceramic substrates, while Chinese manufacturers are expanding capacity for standard TECs and micro‑TEC assemblies. The competitive balance reflects a dual‑track dynamic: legacy players secure contracts that prioritize material consistency and reliability verification, whereas emerging Chinese suppliers leverage lower production costs and rapid scale‑up to service cost‑sensitive segments. Upstream raw‑material providers such as Furukawa and Rogers remain pivotal, but the growing domestic sourcing in China is eroding import reliance, subtly shifting bargaining power across the value chain.

Product Differentiation and Integration

Product strategies are moving beyond simple cooling toward holistic thermal‑management solutions. Recent launches incorporate cold‑plate interfaces, integrated temperature controllers, and enhanced welding techniques that improve grain uniformity and prolong module lifespan. Companies like Coherent and Kyocera are segmenting their portfolios to address distinct reliability tiers, from mid‑range offerings capable of 100 k cycles to premium lines that survive extreme cycling regimes. This granularity enables end‑users in aerospace, defense, and high‑performance computing to select modules that align with specific lifetime and performance criteria, fostering a marketplace where differentiation is rooted in engineering depth rather than price alone.

COMPETITIVE LANDSCAPE

Key Industry Players

Semiconductor Peltier Module Competitive Overview

The market is anchored by a handful of firms that control premium material supply and high‑reliability system integration. Ferrotec, with its long‑standing expertise in bismuth‑telluride sourcing and advanced packaging, commands a disproportionate share of the high‑end optical and aerospace segments. Kyocera’s recent 2024 module, delivering a 21 % increase in heat‑absorption capacity, has solidified its position in automotive battery thermal management and precision medical devices. Coherent (formerly II‑VI) leverages a broad portfolio that spans from mid‑range CT‑Series coolers to customized cold‑plate solutions, enabling it to serve both semiconductor equipment manufacturers and AI‑computing data centers. Phononic’s aggressive push into solid‑state cooling for next‑generation servers illustrates how a focused R&D pipeline can translate into sizable deployments, reinforcing the dominance of established western players in applications where reliability and cycle life are non‑negotiable.

Chinese manufacturers are rapidly expanding the volume‑oriented tier of the market. Guangdong Fuxin Technology, Zhejiang Wangu Semiconductor, and Xianghe Oriental Electronic have built domestic supply chains that reduce lead times and price points for standard TEC and micro‑TEC modules. ARCTIC TEC and KJLP, while smaller, specialize in niche cooling solutions for consumer electronics and industrial sensors, carving out defensible market slices. Emerging entrants such as Thermion Company and Same Sky (formerly CUI Devices) are targeting system‑level integration, coupling modules with controllers and liquid‑cooling loops to meet the growing demand from automotive seat‑heating and high‑precision laboratory instruments. This dual‑track structure—premium reliability versus cost‑effective mass production—creates a competitive environment where collaboration, joint‑venture R&D, and strategic sourcing of raw materials become critical success factors.

List of Key Semiconductor Peltier Module Companies Profiled

- Ferrotec Corp.

- Kyocera Corporation

- Coherent Corp.

- Phononic Ltd.

- Guangdong Fuxin Technology

- Zhejiang Wangu Semiconductor

- ARCTIC TEC

- KJLP

- Thermion Company

- Same Sky (formerly CUI Devices)

- TE Technology

- Tark Thermal Solutions

- Peltron GmbH

- Sensor Controls Co., Ltd.

- Wakefield Thermal

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Multi-stage Type offers enhanced heat‑flux capability and is favored for high‑precision thermal management.

|

| By Application |

|

Communication drives adoption of Peltier modules for high‑density optical networking and emerging AI data‑center cooling.

|

| By End User |

|

Electronics OEMs prioritize modules that combine miniaturization with rapid thermal response.

|

| By Material |

|

Bismuth Telluride remains the core material due to its mature processing and high‑efficiency thermoelectric performance.

|

| By Reliability Level |

|

High Cycle Life segment attracts customers requiring extensive thermal cycling, such as laser systems and battery thermal management.

|

Regional Analysis: Semiconductor Peltier Module Market

Asia‑Pacific

Concentrated clusters in Shenzhen, Suzhou, and Taipei host vertically integrated fabs that combine wafer processing with module assembly. The tight integration shortens time‑to‑market for custom‑spec Peltier devices, granting regional manufacturers the agility to respond to rapid design cycles in consumer electronics and automotive cooling.

Government‑backed research parks in Japan and South Korea dedicate considerable resources to thermoelectric material science. Breakthroughs in nanostructured bismuth‑telluride alloys are translating into higher efficiency modules that attract premium contracts from aerospace and medical device manufacturers.

Proximity to rare‑earth element exporters in Southeast Asia reduces exposure to geopolitical disruptions. Regional players have cultivated multi‑tiered supplier networks, enabling rapid substitution of critical components and preserving production continuity during global material shortages.

Rapid growth of 5G infrastructure and edge‑computing nodes in the region drives demand for compact, solid‑state cooling. Companies designing server racks for telecom equipment are increasingly specifying Peltier modules to meet stringent temperature stability targets while maintaining a small footprint.

North America

In North America, Semiconductor Peltier Module Market is shaped by a focus on high‑performance applications such as aerospace thermal regulation and advanced medical imaging. U.S. defense contractors prioritize modules that can operate under extreme temperature swings, prompting suppliers to develop ruggedized packages. Parallelly, a network of university‑industry collaborations in the Midwest is fostering niche material innovations, though commercial scale remains limited compared with Asia‑Pacific. Customers here value reliability and compliance with stringent safety standards, which influences procurement cycles and drives a preference for established, fully certified suppliers.

Europe

European stakeholders emphasize sustainability and regulatory compliance. The European Union’s energy‑efficiency directives encourage adoption of solid‑state cooling in industrial machinery and data‑center infrastructure. German and French firms are integrating Peltier technology into precision manufacturing equipment to reduce coolant usage and lower overall carbon footprints. While the market size is modest, the premium positioned on low‑emission solutions incentivizes long‑term contracts with manufacturers that can demonstrate measurable environmental benefits.

South America

South American activity revolves around niche agricultural and mining uses where temperature control of sensor arrays is critical. Brazil’s emerging electronics sector is experimenting with Peltier modules for solar‑powered refrigeration units in remote locations. Constraints such as limited local component supply and higher import duties curtail rapid market expansion, but the region’s growing focus on renewable‑energy integration presents a gradual pathway for increased adoption.

Middle East & Africa

In the Middle East and Africa, the market is still embryonic, yet specific climate‑driven needs create pockets of opportunity. Oil‑field equipment providers are trialing thermoelectric cooling to protect monitoring electronics from extreme heat. Meanwhile, South‑African research institutes are exploring low‑cost Peltier solutions for medical diagnostic devices in off‑grid clinics. The primary barrier remains a shortage of skilled assembly facilities, prompting many buyers to source modules from established Asian manufacturers while awaiting local capability development.

Report Scope

This market research report provides a comprehensive analysis of the Semiconductor Peltier Module Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Semiconductor Peltier Module Market?

-> Semiconductor Peltier Module market is projected to grow from USD 938 million in 2026 to USD 1 936 million by 2034, exhibiting a CAGR of 9.3%

Which key companies operate in Semiconductor Peltier Module Market?

-> Key players include Ferrotec, KELK Ltd., Kyocera, Coherent Corp, Tark Thermal Solutions, Phononic, Guangdong Fuxin Technology, ARCTIC TEC, and others.

What are the key growth drivers?

-> Key growth drivers include rising demand for precision temperature control in optical modules, lasers, medical testing, automotive battery and seat temperature management, and the expansion of AI computing and high‑density data‑center cooling.

Which region dominates the market?

-> Asia‑Pacific is the fastest‑growing region, with China expanding large‑scale manufacturing, while Japan and Europe retain leadership in high‑end material reliability.

What are the emerging trends?

-> Emerging trends include integration of cold plates and liquid‑cooling systems, development of high heat‑flux, low‑power modules, and increasing deployment of thermoelectric solutions in AI servers, optical networking equipment, and automotive thermal management.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...