Optical Module DSP Chips Market Insights

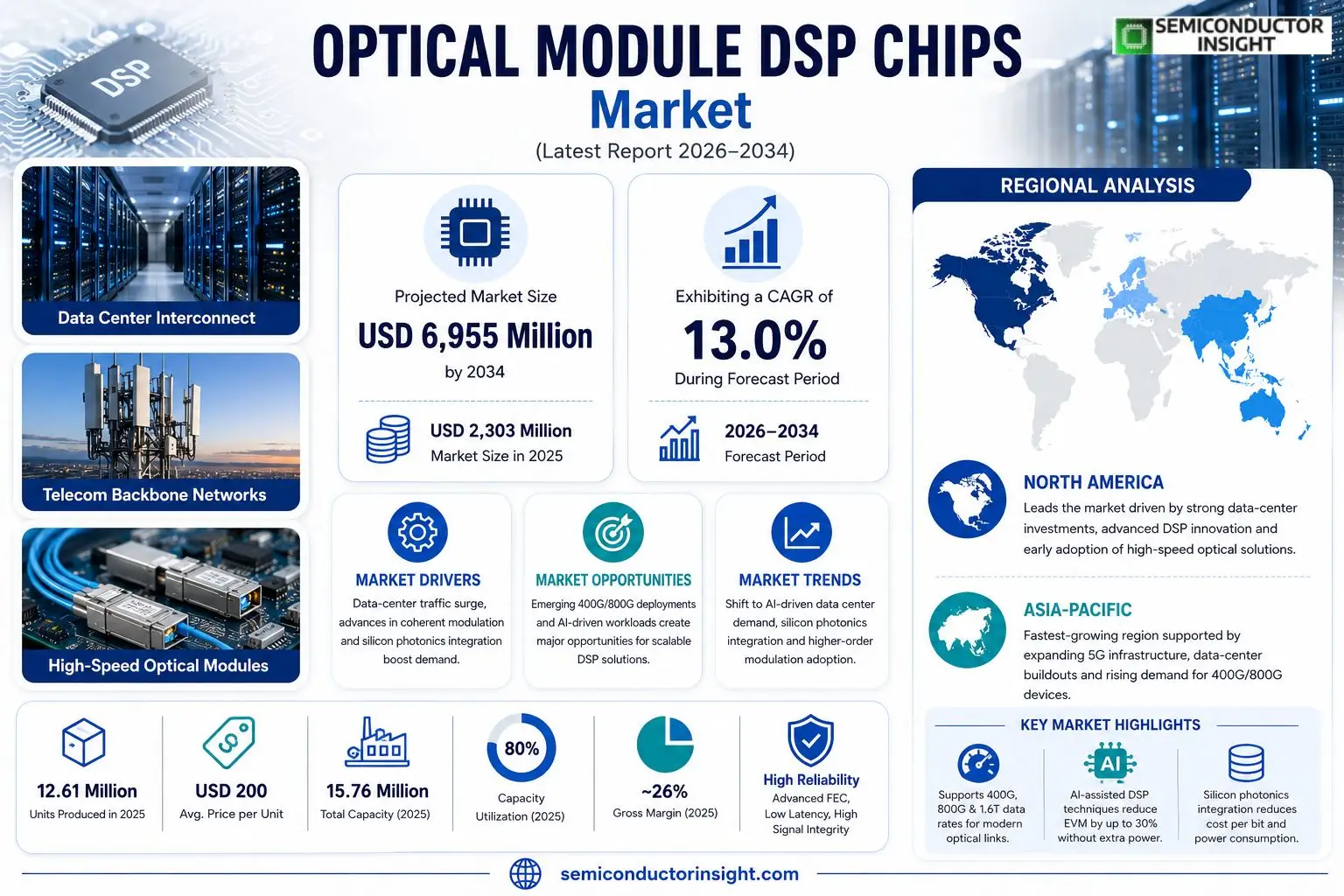

Optical Module DSP Chips market size was valued at USD 2,303 million in 2025. The market is projected to grow from USD 2,603 million in 2026 to USD 6,955 million by 2034, exhibiting a CAGR of approximately 13% during the forecast period.

Optical Module DSP chips are high‑performance digital signal processors that enable modulation, equalization, decoding and forward error correction for coherent optical communication links. By handling data rates of 400G, 800G and even 1.6T, these chips form the computational core of modern high‑speed optical interconnects used in data‑center networking and telecom backbones.The industry’s expansion is anchored by three converging forces: the surge in AI training workloads demanding low‑latency, high‑throughput links; continuous upgrades of data‑center interconnect standards that push bandwidth per rack upward; and broader adoption of silicon‑photonic integration that lowers cost per bit. In 2025 production reached roughly 12.61 million units at an average price of USD 200 each, while total capacity stood at 15.76 million units with an industry gross margin near 26%, underscoring both scale and profitability.

MARKET DRIVERS

Data‑Center Traffic Surge Fuels Demand

data‑center operators are coping with a sustained rise in traffic that now exceeds 60 % year‑over‑year in many regions. This pressure translates directly into a need for higher‑capacity optical interfaces, and the Optical Module DSP Chips Market is responding with increasingly sophisticated signal‑processing silicon that can sustain 200 Gbps, 400 Gbps and emerging 800 Gbps lanes. Vendors that can deliver low‑latency, power‑efficient DSP solutions are gaining preferential access to tier‑one carrier contracts.

Advances in Coherent Modulation Techniques

Recent breakthroughs in coherent modulationparticularly probabilistic constellation shaping and digital back‑propagationhave unlocked spectral efficiencies previously unattainable with traditional NRZ formats. By embedding these algorithms in DSP chips, manufacturers enable operators to push more bits through the same fiber, postponing costly fiber‑laying projects. The ripple effect is a rapid uptake of DSP‑centric optical modules across metro and long‑haul networks.

➤ “Integrating AI‑assisted adaptive equalization into the DSP core cuts error‑vector magnitude by up to 30 % without increasing power draw.”

As integration levels rise, the bill‑of‑materials for each optical transceiver shrinks, allowing system integrators to achieve tighter form factors while maintaining thermal headroom. This cost‑performance balance is a decisive factor for hyperscale cloud providers seeking to expand capacity while preserving CAPEX discipline.

MARKET CHALLENGES

Escalating Design Complexity

Modern DSP chips must support a widening array of modulation formats, forward error correction (FEC) schemes and wavelength‑division multiplexing (WDM) grids. The confluence of these requirements forces design teams to handle multi‑domain verification, extending development cycles and inflating engineering overhead. Companies that cannot streamline their verification pipelines risk missing critical market windows.

Other Challenges

Manufacturing Yield Management

The silicon‑photonic processes used for high‑frequency DSP blocks exhibit tighter defect density thresholds. Even marginal yield drops translate into noticeable price pressure, especially when customers negotiate large‑volume contracts. Suppliers are compelled to invest in advanced test‑and‑repair methodologies, which adds a layer of operational cost that smaller players find hard to absorb.

MARKET RESTRAINTS

Component Cost Sensitivity

While performance gains are attractive, the capital outlay for next‑generation DSP silicon remains a hurdle for budget‑constrained operators. The incremental price premiumoften 15‑20 % over legacy DSP solutionsforces procurement teams to evaluate total cost of ownership versus immediate bandwidth benefits. This cost calculus slows the transition to newer module generations in markets where price elasticity is high.

MARKET OPPORTUNITIES

Emerging 400G and 800G Deployments

Network operators are drafting roadmaps that incorporate 400 Gbps and 800 Gbps per‑channel optics within the next three years. Each step up in line rate demands a corresponding escalation in DSP capability, opening a sizable addressable market for designers who can deliver scalable architectures. Early entrants that license modular DSP IP blocks stand to capture a significant share of the rollout spend.

Optical Module DSP Chips Market Trends

AI‑Centric Data Center Demand Fuels Chip Evolution

The explosion of artificial‑intelligence workloads is stressing data‑center interconnects far beyond legacy capacities. Operators are rapidly replacing 400‑gigabit links with 800‑gigabit and emerging 1.6‑terabit solutions to keep latency low while scaling throughput. At the same time, the rollout of newer Ethernet specifications forces module manufacturers to embed ever more sophisticated signal‑processing functions. These twin pressures compel designers of Optical Module DSP Chips to integrate higher‑order modulation, advanced forward error correction and adaptive equalisation within a single silicon footprint, shortening the time from silicon to rack deployment.

Other Trends

Geographic Concentration and Supply‑Chain Shifts

The upstream landscape remains split between a few design powerhouses in the United States and a dense fabrication network spread across East Asia. While American firms dominate the intellectual property around high‑performance digital signal processing, Chinese assemblers control the bulk of module output, leveraging lower‑cost packaging capacity. Japan and several European nations retain a foothold in premium‑grade photonic components that feed high‑end telecom equipment. This distribution creates a “design‑centered, manufacture‑” model, prompting many players to establish joint‑venture test facilities near key customer clusters to reduce lead‑time and mitigate logistics risk.

Integration of Silicon Photonics and Coherent DSP

Silicon‑photonic platforms are converging with coherent DSP blocks, blurring the line between passive optics and active signal conditioning. The advantage lies in monolithic integration: reduced power envelope, tighter bandwidth alignment and the ability to scale to multi‑terabit per‑second lanes on a single die. Early adopters are seeing a measurable decline in module BOM cost, while end‑users report smoother scaling paths for hyperscale AI clusters. For vendors, the shift implies a strategic choiceeither double‑down on pure DSP ASIC excellence or pursue hybrid silicon‑photonic routes that promise longer‑term differentiation. Investment decisions made today will shape the competitive hierarchy as the market leans more toward AI‑driven traffic patterns than traditional telecom signalling.

COMPETITIVE LANDSCAPEKey Industry Players

Optical Module DSP Chips Market – Competitive Overview

The market is dominated by a handful of vertically integrated firms that control both silicon‑photonic design and large‑scale wafer fabrication. Broadcom and Marvell, for instance, leverage their deep DSP expertise to offer turnkey modules that bundle signal processing with advanced packaging, thereby capturing a sizable share of data‑center demand. Cisco’s strategy of embedding proprietary DSP cores into its networking portfolio creates a barrier for pure‑play chip designers, while Coherent and InnoLight focus on niche high‑performance coherent optics that serve ultra‑low‑latency links in hyperscale environments. This concentration of capabilities reinforces a tiered structure where a few powerhouses negotiate the bulk of high‑value contracts, and regional players align with them through OEM or joint‑venture arrangements.Beyond the top tier, several specialized manufacturers are carving out relevance through differentiated technology or geographic positioning. Huawei’s HiSilicon unit supplies cost‑competitive DSP solutions to Chinese optical module assemblers, capitalising on domestic scale. Fujitsu and Nokia maintain strong footholds in the European telecom equipment arena, where legacy network upgrades still demand reliable DSP integration. NTT Innovative Devices, Effect Photonics, and Sitrus Technology target emerging silicon‑photonic convergence, offering hybrid modules that blend electronic DSP with photonic‑integrated circuits. Meanwhile, newcomers such as Alphawave Semiconductor and Airoha Technology experiment with packaging‑centric innovations that could reshape cost structures for midsized operators.

List of Key Optical Module DSP Chips Companies Profiled

- Broadcom Inc.

- Cisco Systems, Inc.

- Marvell Technology Group Ltd.

- Coherent Inc.

- InnoLight Technology Corp.

- Huawei HiSilicon

- Fujitsu Limited

- Nokia Corporation

- Ciena Corporation

- NTT Innovative Devices Inc.

- Effect Photonics Ltd.

- Sitrus Technology Co., Ltd.

- Airoha Technology Corp.

- Alphawave Semiconductor Ltd.

- Samsung Electronics Co., Ltd.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Coherent DSP Chips are emerging as the dominant type because they deliver ultra‑low latency and superior noise tolerance; they enable the highest modulation formats required for 800G and beyond; they are closely aligned with the shift toward AI‑driven data‑center interconnects, fostering rapid adoption across large‑scale cloud facilities. |

| By Application |

|

Data Center Interconnect drives the market because it demands ever‑higher bandwidth and deterministic latency; the migration from 400G to 800G and future 1.6T standards fuels continuous DSP innovation; DCI deployments are tightly coupled with AI model training workloads that require massive, low‑error optical links. |

| By End User |

|

Cloud Service Providers are the leading end‑user segment as they continuously upscale rack‑level bandwidth, prioritize energy‑efficient optical fabrics, and lead the adoption of coherent DSP architectures to support AI‑intensive workloads across ly distributed data centers. |

| By Transmission Distance |

|

Long Distance segments are gaining prominence because they combine the need for high spectral efficiency with advanced forward error correction, prompting vendors to embed more sophisticated DSP algorithms that can sustain error‑free transmission over metropolitan and regional network spans. |

| By Speed Tier |

|

800 G is currently the focal speed tier as it balances implementation complexity with a clear performance uplift over 400 G, encouraging ecosystem partners to co‑develop DSP architectures that are scalable, power‑efficient, and ready for the imminent transition to 1.6 T. |

Regional Analysis: Optical Module DSP Chips Market

North America

The region’s investment in quantum‑ready networking and edge‑computing clusters fuels demand for DSP chips that can handle higher modulation formats. Customer expectations for energy‑efficient optics compel manufacturers to embed advanced digital signal processing that trims power per bit, a differentiator when operators evaluate total cost of ownership.

Standard‑setting bodies such as the IEEE and the Telecom Infra Project enjoy strong participation from North American firms, ensuring that emerging DSP solutions align with ly accepted specifications. This alignment reduces certification overhead and accelerates cross‑border deployments.

Companies are integrating AI‑assisted error correction into DSP pipelines, allowing real‑time adaptation to fiber impairments. The willingness to pilot such innovations in testbeds shortens the feedback cycle from lab to production, reinforcing the region’s reputation for early adoption.

Consolidation continues as larger fabs acquire boutique design studios, creating platforms that bundle DSP IP with advanced packaging. This trend narrows the field of viable suppliers, heightening barriers to entry while intensifying the strategic focus on differentiation through software‑defined features.

Europe

European operators emphasize sustainability and carbon‑neutral networking, prompting a shift toward DSP chips that enable power‑saving schemes such as adaptive modulation. Policy incentives for green data‑centers have spurred collaboration between telecom carriers and silicon designers, resulting in joint road‑maps that prioritize low‑loss optical modules. Moreover, the region’s fragmented market structure, with several mid‑size vendors, encourages modular DSP solutions that can be customized for niche verticals like high‑frequency trading and scientific research networks.

Asia‑Pacific

Asia‑Pacific’s rapid rollout of 5G and burgeoning demand for regional content delivery networks are stretching the capacity of existing optical infrastructure. Vendors respond by offering DSP chips that support higher baud rates, targeting countries where bandwidth constraints are acute. Governments in the region are also investing in domestic semiconductor capabilities, which nurtures a growing ecosystem of home‑grown DSP designers capable of meeting local standards while reducing reliance on imported silicon.

South America

In South America, telecom operators are modernizing legacy fiber backbones, creating a market for retro‑compatible DSP solutions that can be integrated into existing modules. Economic volatility leads providers to prioritize cost‑effective designs that deliver incremental performance gains without large capital outlays. Partnerships between regional carriers and multinational chip firms are common, facilitating technology transfer and fostering a nascent talent pool focused on optical signal processing.

Middle East & Africa

The Middle East & Africa region is witnessing a surge in sovereign‑wealth‑fund‑backed data‑center projects, which drives interest in high‑density optical transceivers powered by sophisticated DSP chips. Operators seek solutions that can sustain long‑haul submarine cable links, so emphasis is placed on DSP architectures optimized for low‑noise amplification over vast distances. Meanwhile, African markets, still early in fiber deployment, are evaluating modular DSP offerings that allow scalable upgrades as network reach expands.

Report Scope

This market research report provides a comprehensive analysis of the Optical Module DSP Chips Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Optical Module DSP Chips Market?

-> Optical Module DSP Chips Market was valued at USD 2303 million in 2025 and is expected to reach USD 5367 million by 2032 with a CAGR of 13.0% during the forecast period.

Which key companies operate in Optical Module DSP Chips Market?

-> Key players include Broadcom, Cisco, Marvell, Coherent, InnoLight, Huawei HiSilicon, Fujitsu, Nokia, Ciena, NTT Innovative Devices, among others.

What are the key growth drivers?

-> Key growth drivers include explosive AI computing power growth, data center interconnect upgrades, high‑speed Ethernet standard iterations, and the shift from 400G to 800G and 1.6T optical transmission.

Which region dominates the market?

-> United States holds the largest market share for DSP chip manufacturing, while China leads in optical module production.

What are the emerging trends?

-> Emerging trends include the transition from telecom‑driven to AI data‑center‑driven demand and increasing competition between high‑end DSP solutions and silicon photonics integration.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...