Micro-Optical Lens Assemblies Market Insights

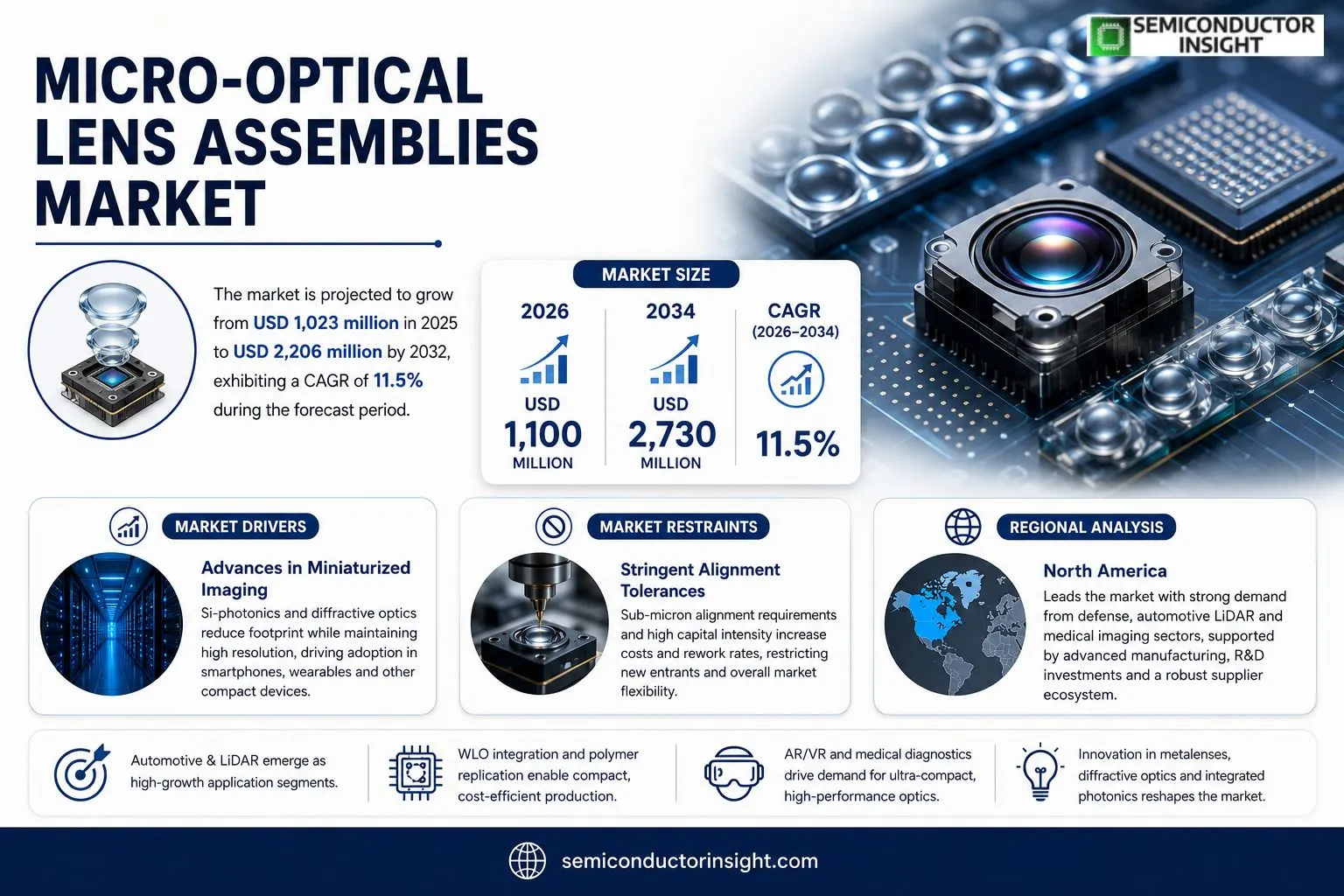

Micro-Optical Lens Assemblies market size was valued at USD 1,023 million in 2025. The market is projected to grow from USD 1,100 million in 2026 to USD 2,730 million by 2034, exhibiting a CAGR of approximately 11½ % during the forecast period.

Micro‑optical lens assemblies are functional optical components built around micrometer‑to‑millimeter‑scale lens elements, lens arrays and micro‑structured surfaces. They are fabricated through photolithography, thermal reflow, reactive‑ion etching, precision glass molding and nano‑imprint lithography, supporting applications such as optical communications, LiDAR, AR/VR, automotive lighting and medical imaging.

MARKET DRIVERS

Advances in Miniaturized Imaging

Recent breakthroughs in silicon photonics and diffractive optics have lowered the footprint of lens assemblies without compromising resolution. Manufacturers are leveraging sub‑micron lithography to embed corrective features directly onto the lens substrate, a shift that trims assembly steps and reduces yield loss. This technical convergence is compelling OEMs in smartphones and wearables to replace conventional optics with micro‑optical modules, thereby expanding the addressable volume of the Micro-Optical Lens Assemblies Market.

Growing Demand in Medical Diagnostics

Point‑of‑care testing devices increasingly rely on compact optical paths to analyze blood or tissue samples on‑chip. Healthcare providers value the ability to obtain high‑definition images from a handheld probe, which drives adoption of micro‑optical lens assemblies in endoscopic and ophthalmic instruments. As regulatory pathways streamline for in‑vitro diagnostics, suppliers see a tangible uptick in order volumes from medical device firms.

➤ Integrating wave‑front engineering directly into lens stacks cuts assembly time by up to 30 %, a cost advantage that is reshaping procurement strategies across consumer electronics.

The convergence of high‑performance optical design software with automated pick‑and‑place machinery creates a feedback loop: faster design cycles feed production lines, which in turn enable rapid iteration of new lens geometries. This virtuous cycle strengthens the competitive posture of firms that can synchronize R&D with scalable manufacturing, reinforcing the upward trajectory of the Micro-Optical Lens Assemblies Market.

MARKET CHALLENGES

Stringent Alignment Tolerances

Micro‑optical lens assemblies demand sub‑micron alignment between individual elements to preserve optical fidelity. Process engineers report that even minor deviations during bonding can cause distortion that nullifies the intended performance gains, inflating rework rates. The necessity for high‑precision tooling raises capital expenditures for smaller suppliers, limiting market entry.

Other Challenges

Material Compatibility

The juxtaposition of glass, polymer, and semiconductor substrates introduces disparate thermal expansion coefficients. When devices undergo temperature cycling, differential expansion can induce stress fractures at the interface, prompting manufacturers to invest in advanced adhesive chemistries or explore a‑thermal designs, both of which add cost and complexity.Furthermore, the rise of alternative imaging modalities such as computational photography reduces reliance on physical lens stacks in some consumer segments. Companies that cannot diversify their product portfolios risk losing relevance as software‑centric solutions gain acceptance.

MARKET RESTRAINTS

High Capital Intensity

Establishing a production line capable of sub‑10 µm tolerances requires precision equipment priced in the multi‑million‑dollar range. For firms operating on thin margins, the payback horizon can extend beyond five years, especially when demand fluctuations compress order books. This financial barrier curtails the speed at which new entrants can scale, consolidating market power among incumbents.Supply chain volatility further compounds the issue. Rare‑earth coatings and specialty glasses experience price spikes driven by geopolitical factors, forcing manufacturers to either absorb costs or pass them downstream, both of which erode profitability.Finally, regulatory scrutiny for medical and aerospace applications introduces additional validation steps. Certification processes that can span 12‑18 months add time‑to‑market delays, discouraging agile product launches and limiting overall market fluidity.

MARKET OPPORTUNITIES

Expansion into Augmented Reality Platforms

AR headsets require ultra‑lightweight, high‑resolution optical bundles that can be positioned mere millimeters from the eye. Lens‑assembly providers that can deliver sub‑millimeter focal lengths with integrated anti‑reflective coatings stand to capture a sizable share of this emerging ecosystem. Early collaborations between optical firms and chipset designers are already yielding prototypes that marry micro‑optical lens stacks with waveguide displays.

Custom Solutions for Autonomous Vehicles

LiDAR and short‑range sensing modules incorporated into driver‑assist systems benefit from compact, high‑precision optics. Tailoring lens assemblies to specific wavelength bands (905 nm, 1550 nm) while maintaining a minimal envelope can differentiate sensor packages in a crowded OEM market. Companies that develop modular, plug‑and‑play micro‑optical kits can unlock recurring revenue streams from automotive suppliers.

Beyond hardware, service‑oriented modelssuch as design‑for‑manufacturing consulting and rapid prototyping on demandaddress the pain points of firms lacking in‑house optical expertise. By monetizing engineering know‑how alongside physical components, providers can deepen client relationships and generate higher-margin revenue in the Micro-Optical Lens Assemblies Market.

Micro-Optical Lens Assemblies Market Trends

Integration of Beam‑Control Functions in Wafer‑Level Packages

The latest valuation of the Micro‑Optical Lens Assemblies Market sits at roughly $1.0 billion in 2025, reflecting the sector’s transition from discrete lens groups to compact, wafer‑level beam‑control modules. Engineers are now embedding collimation, homogenization and wavefront sampling directly into silicon‑photonic platforms, a move that trims package height and reduces alignment steps on the assembly line. This shift is not merely a cost‑saving exercise; it improves coupling efficiency for high‑speed data‑center interconnects and lowers power draw in emerging AI accelerators. As manufacturers adopt precision glass molding and nano‑imprint replication for mass production, the economics tilt in favor of high‑volume sensor and LiDAR suppliers, accelerating the adoption curve across automotive and industrial laser segments.

Other Trends

Regional Supply‑Side Evolution

From a supply‑chain perspective, the ecosystem is decidedly polycentric. Europe continues to dominate high‑NA infrared components, leveraging legacy expertise in optical‑glass processing. The United States supplies the majority of specialty glass formulations and bespoke coating services, while Japan’s precision‑molding firms retain a strong foothold in polymer‑on‑glass hybrids. In Asia, China’s wafer‑level micro‑optics capacity has expanded rapidly, supported by government incentives and a growing domestic client base. Taiwanese firms contribute niche wafer‑stacking capabilities, and Israel’s niche players focus on diffractive‑optics‑enhanced MLA solutions. This geographic dispersion creates competitive pressure that drives continual process refinement and safeguards against single‑source bottlenecks.

Emerging Demand from Autonomous and Immersive Technologies

Automotive projected lighting, LiDAR, and 3D sensing applications have moved from pilot projects to volume production, positioning micro‑optical assemblies as critical enablers of reliable perception stacks. Parallel trends in AR/VR headsets and miniature medical imaging probes are generating a second wave of demand, where size, weight, and alignment tolerance directly influence user experience and regulatory approval timelines. In these fields, the assemblies act as more than passive optics; they dictate signal‑to‑noise ratios and overall system yield. Companies that can offer co‑design services, wafer‑level process control, and application‑specific validation are gaining a decisive edge, reshaping the competitive landscape toward solution‑oriented partnerships rather than transactional component sales.

COMPETITIVE LANDSCAPE

Key Industry Players

Micro‑Optical Lens Assemblies: Competitive Overview

The market is anchored by a handful of firms that combine deep material expertise with advanced wafer‑level processing. Focuslight Technologies (China) leveraged its laser‑optics heritage to acquire a portfolio of micro‑optical assets, positioning itself as a bridge between high‑volume semiconductor fabs and specialized optics customers. In the United States, Coherent Corp. and Himax Technologies bring a blend of optical‑materials know‑how and silicon‑photonic integration, enabling them to capture large‑scale communication‑module contracts. European contenders such as Jenoptik AG, INGENERIC GmbH and Axetris AG maintain a reputation for ultra‑precise alignment and coating capabilities, which is vital for automotive LiDAR and high‑power laser applications. The overall structure resembles a tiered ecosystem: a core of ly diversified manufacturers serve OEMs that demand custom numerical‑aperture and thermal‑stability specifications, while a broader base of regional suppliers focuses on volume‑driven consumer‑sensing and AR/VR segments.Beyond the core, a diverse set of niche players injects specialized know‑how into the supply chain. Zhejiang Lante Optics and Anteryon (Suzhou) have built strong positions in polymer‑replicated microlens arrays for consumer electronics, exploiting low‑cost imprint techniques. Nalux Co. and AGC Inc. differentiate through high‑NA fused‑silica wafer‑level optics targeting data‑center interconnects. PowerPhotonic and FISBA AG excel in metal‑lens and diffractive‑optics hybrids that address emerging metrology markets. Holographix LLC and Teledyne Scientific & Imaging provide ruggedized modules for medical imaging and industrial laser conditioning. VIAVI Solutions, MPNICS and Uroptics round out the list with dedicated offerings for optical‑communications couplers and precision metrology. Their collective focus on co‑design, process control and application‑specific validation reshapes buyer expectations, shifting the competitive battleground from catalog pricing toward integrated engineering services.

List of Key Micro-Optical Lens Assemblies Companies Profiled

- Focuslight Technologies Inc.

- Coherent Corp.

- Jenoptik AG

- INGENERIC GmbH

- Axetris AG

- Himax Technologies, Inc.

- Zhejiang Lante Optics Co., Ltd.

- Anteryon (Suzhou) Optoelectronics Technology Co., Ltd.

- Nalux Co., Ltd.

- AGC Inc.

- Nippon Sheet Glass Co., Ltd.

- PowerPhotonic Ltd.

- FISBA AG

- Holographix LLC

- Teledyne Scientific & Imaging

- VIAVI Solutions Inc.

- MPNICS Co., Ltd.

- Uroptics

- Avantier Inc.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Microlens Arrays dominate due to their versatility in collimation, focusing and homogenization.

|

| By Application |

|

Automotive & LiDAR is emerging as a high‑growth driver.

|

| By End User |

|

Data‑Center Operators prioritize coupling efficiency and thermal stability.

|

| By Technology |

|

Hybrid Multi‑Process Integration is gaining traction.

|

| By Material Platform |

|

Silicon & Fused Silica remain preferred for high‑performance segments.

|

Regional Analysis: Micro-Optical Lens Assemblies Market

North America

The region hosts a network of vertically integrated fabs that combine precision molding, diamond‑turning, and thin‑film deposition. Suppliers increasingly adopt modular production cells, allowing rapid re‑configuration for differing aperture sizes and curvature specifications, thereby shortening lead times for custom orders.

Defense optics, autonomous‑vehicle LIDAR, and ophthalmic imaging dominate spend. Each segment values robustness and dimensional stability, prompting manufacturers to prioritize materials such as fused silica and engineered polymers that tolerate harsh thermal cycles.

Compliance frameworks, especially those governing aerospace and medical devices, require exhaustive traceability. Companies that embed data‑logging throughout the assembly line enjoy smoother audit pathways and can leverage this compliance as a market differentiator.

Emerging trends include integration of meta‑material coatings and hybrid silicon‑glass platforms. Start‑ups are attracting venture capital to pursue on‑chip lens arrays that promise order‑of‑magnitude reductions in system size for consumer electronics.

Europe

European markets exhibit a balanced mix of legacy optics manufacturers and agile startups focused on augmented‑reality devices. Germany’s automotive sector pushes for tighter integration of micro‑lens assemblies within head‑up displays, while the Nordics excel in low‑temperature fabrication techniques essential for space‑grade components. Intellectual‑property frameworks across the EU encourage cross‑border collaborations, allowing firms to tap into specialized expertise without extensive relocation costs. As sustainability criteria gain prominence, several European players are experimenting with recyclable polymer substrates, positioning themselves for future procurement policies that favor environmentally conscious components.

Asia‑Pacific

The Asia‑Pacific region is distinguished by rapid capacity expansion, particularly in China, South Korea, and Taiwan. Manufacturing hubs prioritize cost efficiency while scaling up precision equipment, which creates a competitive pressure on pricing but also opens opportunities for joint‑venture models that combine low‑cost production with North American design expertise. Domestic demand is fueled by burgeoning consumer electronics and a growing defense modernization agenda. However, the fragmented supply chain often results in variable quality control, prompting multinational firms to establish regional quality centers to harmonize standards.

South America

South American activity centers around Brazil and Mexico, where emerging medical‑device firms seek locally sourced micro‑optical components to reduce import reliance. Government incentives for high‑tech manufacturing have spurred modest investments in clean‑room facilities, yet skilled labor shortages constrain the ability to produce highly complex assemblies. Partnerships with established North American suppliers are common, allowing local firms to benefit from transfer‑of‑technology agreements while gradually building indigenous design capabilities.

Middle East & Africa

In the Middle East & Africa, growth is primarily driven by defense procurement programs and nascent renewable‑energy sensor projects. The United Arab Emirates and Israel lead regional R&D initiatives, focusing on ruggedized lens assemblies that can endure extreme temperature swings. African markets remain largely import‑dependent, but emerging telecommunications infrastructure creates a modest demand for high‑precision optical components in fiber‑optic networking, hinting at a gradual market maturation over the next decade.

Report Scope

This market research report provides a comprehensive analysis of the Micro-Optical Lens Assemblies Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Micro-Optical Lens Assemblies Market?

-> Micro-Optical Lens Assemblies Market was valued at USD 1,023 million in 2025 and is expected to reach USD 2,206 million by 2032.

Which key companies operate in Micro-Optical Lens Assemblies Market?

-> Key players include Focuslight Technologies Inc., Coherent Corp., Jenoptik AG, INGENERIC GmbH, Axetris AG, Himax Technologies, Inc., Zhejiang Lante Optics Co., Ltd., Anteryon (Suzhou) Optoelectronics Technology Co., Ltd., Nalux Co., Ltd., AGC Inc., Nippon Sheet Glass Co., Ltd., PowerPhotonic Ltd., FISBA AG, Holographix LLC, Teledyne Scientific & Imaging, HOLO/OR Ltd., temicon GmbH, IMT Masken und Teilungen AG, VIAVI Solutions Inc., MPNICS Co., Ltd., Uroptics, Avantier Inc..

What are the key growth drivers?

-> Key growth drivers include automotive projected lighting, LiDAR, 3D sensing, AR/VR, optical communications, co‑packaged optics, silicon‑photonics coupling, AI data‑center optical interconnects, industrial lasers, and medical‑instrumentation applications.

Which region dominates the market?

-> Europe remains the dominant region, especially for high‑end micro‑optics, while the United States and China are rapidly expanding their capabilities.

What are the emerging trends?

-> Emerging trends include development of metalenses, diffractive optics, integrated photonics, wafer‑level imprinting, polymer replication for high‑volume consumer products, and diversification of material platforms (silicon, fused silica, glass, polymers).

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...